Gas Turbine Supply Chain, AI-Driven Demand Risks New Crunch, 97 GW Data Center Need, and GE/Siemens Backlogs (2025 to 2030)

Gas Turbine Backlogs, GE and Siemens Face AI-Driven Demand Surge

An unprecedented surge in electricity demand, driven by artificial intelligence and data center proliferation, has created a critical manufacturing bottleneck for heavy-duty gas turbines. This supply constraint, centered on key manufacturers like General Electric and Siemens Energy, threatens to delay the construction of new natural gas power plants essential for grid stability and industrial growth. The market shifted abruptly in 2025 as long-term, predictable order cycles were disrupted by urgent, large-scale demand from the tech sector, creating backlogs that now extend for years.

- Prior to 2024, the gas turbine market operated on predictable utility planning cycles, with stable lead times. The primary challenge was integrating higher shares of renewables, not a lack of generation hardware.

- The landscape changed in 2025, as projected power requirements for the global data center sector alone are now estimated to require an additional 97 GW of capacity between 2025 and 2030. This sudden demand spike has overwhelmed the manufacturing capacity of an industry not designed for rapid scaling.

- The strain on the supply chain is compounded by the concurrent build-out of Liquefied Natural Gas (LNG) export terminals, which also rely on large gas turbines for their liquefaction processes. The development of major facilities, including projects from firms like Commonwealth LNG, adds a second major source of demand competing for limited production slots.

- As a result, lead times for new heavy-duty gas turbines have extended significantly, with some reports indicating backlogs stretching through the end of the decade. This directly impacts the timeline for bringing new, reliable power generation online to support economic activity.

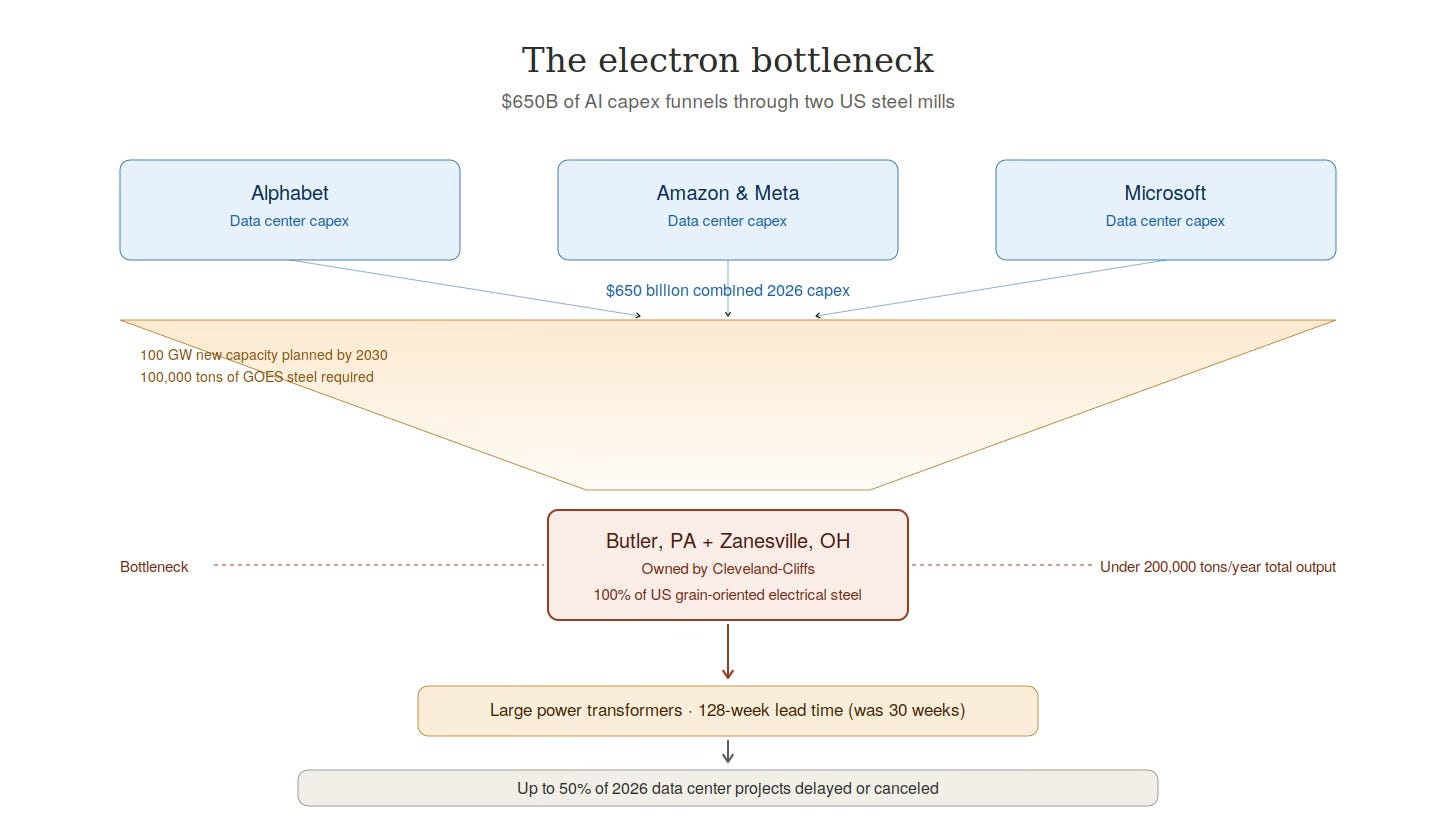

AI Capex Creates Power Transformer Bottleneck

This chart directly supports the section ‘Gas Turbine Backlogs, GE and Siemens Face AI-Driven Demand Surge’ by illustrating a key cause of the demand surge (AI capex) and a resulting infrastructure issue (transformer bottleneck) that contributes to backlogs.

(Source: Macro Notes – Substack)

Corporate AI Investment, $90 B Pennsylvania Hub Anchored by Natural Gas (2025)

Massive capital inflows from the technology sector are a primary catalyst for the new gas turbine demand, creating a direct link between corporate AI strategy and power generation infrastructure. These investments, exemplified by the announced $90 billion plan to establish an AI hub in Pennsylvania, are explicitly tied to the availability of abundant and reliable natural gas, signaling a long-term structural demand shift that is putting pressure on the entire energy equipment supply chain.

- The $90 billion commitment announced in July 2025 to develop a Pennsylvania-based AI hub is a clear validation of natural gas’s role in powering next-generation computing infrastructure. This single initiative represents a substantial new regional load that requires new power generation capacity.

- This trend extends beyond specific projects. The U.S. industrial sector’s natural gas consumption is projected to hit record highs, driven by both traditional industries and the rapidly expanding footprint of data centers, according to the Energy Information Administration (EIA).

- This wave of corporate investment acts as a strong leading indicator for future gas power plant orders. The financial commitment to build data centers precedes the necessary power infrastructure, creating urgency and intense competition for generation equipment like turbines.

Table: Strategic Investments Driving Gas Turbine Demand

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Corporate AI Hub Investment | July 2025 | A $90 billion investment by multiple corporations to establish Pennsylvania as an AI hub. The initiative is explicitly fueled by the state’s natural gas resources, creating a massive new, concentrated demand for gas-fired power. | Inside Climate News |

| Global Data Center Expansion | 2025 – 2030 | The global data center sector is projected to require an additional 97 GW of power capacity. Natural gas is identified as a key fuel to meet this demand and alleviate grid constraints, directly driving orders for new gas turbines. | JLL Research |

| Next Decade (Rio Grande LNG) | January 2026 | JERA signed a long-term agreement to purchase 2 million tons per annum (MTPA) of LNG. Large-scale LNG projects like this require significant numbers of gas turbines for mechanical drive, competing with power generation for supply. | Tailwater Capital |

US Power Grid Strain, GE Turbine Demand Driven by Data Center Hotspots

The gas turbine supply constraint is most acute in the United States, with demand geographically concentrated in regions experiencing rapid data center development and facing existing grid limitations. This localized demand surge creates intense competition for equipment and puts immense pressure on regional transmission and generation infrastructure. While demand is global, the speed and scale of the AI-driven power crunch is a distinctly American phenomenon that turbine manufacturers are struggling to address.

- Between 2021 and 2024, new power generation demand was more geographically dispersed and aligned with traditional population and industrial growth patterns.

- From 2025 forward, demand has become highly concentrated in data center hotspots such as Northern Virginia, Texas, Arizona, and now Pennsylvania. These areas are seeing electricity demand forecasts revised sharply upward, forcing utilities to fast-track plans for new generation.

- This regional concentration means that securing a few large turbine orders for data center power can absorb a significant portion of the available manufacturing slots, creating scarcity for other utilities and industrial users across North America.

- While Europe and Asia are also expanding data infrastructure, the current U.S. policy environment and the scale of domestic tech investment have made the U.S. the epicenter of the turbine demand surge, placing companies like GE Vernova at the center of the supply challenge.

Gas Turbine Technology, GE and Siemens Mature TRL 9 Designs Face Capacity Limits

The current bottleneck is not a failure of technology but a crisis of manufacturing capacity. Heavy-duty gas turbine designs are a mature and proven technology (Technology Readiness Level 9), but the highly specialized industrial base that produces them was not structured to accommodate the explosive and sudden demand growth seen since 2025. Manufacturers are now caught between meeting urgent customer needs and the significant financial risk of investing in new production lines for a demand curve whose long-term trajectory remains uncertain.

- In the period from 2021 to 2024, innovation in gas turbines focused on increasing efficiency, fuel flexibility for hydrogen blending, and reducing emissions. The supply chain was considered stable and sufficient to meet market needs.

- The post-2025 market dynamic has shifted the core problem from technological advancement to industrial production scale. Manufacturers are reportedly hesitant to commit the massive capital required to build new factories, fearing that the AI demand bubble could burst, leaving them with stranded assets.

- This industrial constraint is the root cause of the lengthening lead times. The inability to rapidly scale production of precision-engineered, multi-ton equipment means that new orders placed today may not be fulfilled for several years, creating a significant lag between power demand and supply.

SWOT Analysis, Gas Turbine Manufacturers Face High Demand and Production Risks

Gas turbine original equipment manufacturers (OEMs) are navigating a market defined by immense opportunity and significant operational risk. The surge in demand provides substantial pricing power and revenue certainty, but the inability to meet this demand due to production constraints creates vulnerabilities to market shifts and competitive technologies.

Table: SWOT Analysis for Gas Turbine Manufacturing

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strength | Mature TRL 9 technology, established service revenue streams, high barriers to entry for competitors. | Surging, high-margin demand from AI/data centers; significant pricing power due to supply scarcity; long-term order backlogs providing revenue visibility. | The value of reliable, dispatchable power was validated, moving gas turbines from a “bridge fuel” to a critical enabler of the digital economy. |

| Weakness | Slow growth in mature markets; pressure from renewable energy mandates and ESG investors. | Inelastic manufacturing capacity unable to meet demand surge; extended lead times risking customer frustration and project cancellations; reliance on a complex global sub-component supply chain. | The industry’s lean manufacturing posture, optimized for a stable market, was revealed as a critical vulnerability in a high-growth scenario. |

| Opportunity | Develop turbines with higher hydrogen-blending capabilities; expand service offerings for aging fleets. | Secure multi-year, premium-priced contracts with tech companies and utilities; invest in advanced/modular manufacturing to reduce lead times; expand into ancillary grid services. | A new, highly profitable customer segment (data centers) emerged, offering opportunities for long-term strategic partnerships beyond traditional utility clients. |

| Threat | Accelerated adoption of utility-scale battery storage; stringent emissions regulations (e.g., on methane). | A potential downturn in AI infrastructure spending could lead to a wave of order cancellations; faster-than-expected cost declines in long-duration storage could erode demand for new peaker plants; geopolitical events disrupting sub-component supply. | The supply bottleneck itself became a threat, as it incentivizes customers to aggressively pursue alternatives that may not have been previously viable. |

Scenario Modelling for GE and Siemens: Gas Turbine Supply Chain in 2026

The single most critical variable for the gas power sector in 2026 is whether leading turbine manufacturers announce definitive plans to expand production capacity. This decision will directly dictate the pace at which new power generation can be built to meet soaring electricity demand, influencing project economics and technology choices across the energy industry.

- If major OEMs like GE Vernova or Siemens Energy announce significant capital investment in new factory lines or advanced manufacturing capabilities by mid-2026, watch for a potential stabilization in lead time quotes for deliveries in the 2028-2030 timeframe. This would signal confidence in the long-term demand curve and likely encourage more Final Investment Decisions (FIDs) for gas-fired power plants.

- If manufacturers remain cautious and do not announce major capacity expansions, watch for continued price increases for available production slots and an uptick in project delays or cancellations. This scenario would force utilities and developers to more seriously consider alternatives, such as uprating existing power plants, large-scale battery storage projects, or even a renewed look at smaller, modular generation technologies.

- Key signals to monitor include OEM quarterly earnings reports for guidance on capital expenditures and backlog growth, FERC filings for new gas power plants (or withdrawals of existing applications), and strategic announcements from major data center operators regarding their long-term power sourcing strategies.

Natural Gas Investment to Reach $330B in 2026

This chart’s projection of natural gas investment for 2026 directly informs the ‘Scenario Modelling for GE and Siemens: Gas Turbine Supply Chain in 2026’ section by providing a key financial data point for modeling future demand and supply chain capacity.

(Source: Discovery Alert)

The questions your competitors are already asking

This report covers one angle of the gas turbine supply chain bottleneck driven by AI and data center demand. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the heavy-duty gas turbine market amid the AI demand surge?

- What is the outlook for deploying 97 GW of new gas-fired power for the AI and data center sector by 2030?

- Which data center and AI operators are driving the urgent demand for new gas turbine capacity?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.