CCUS LNG Project Divestment, BP Sells 5% Stake to GS Energy in $35 B Browse Project Deal (2023 to 2026)

The global Liquefied Natural Gas (LNG) market is undergoing a structural realignment, where European energy majors are actively de-risking their portfolios while Asian national energy companies are investing heavily to secure long-term supply. The recent transaction involving BP’s sale of a 5% stake in the Woodside-operated Browse LNG project to South Korea’s GS Energy is a clear signal of this divergence. This move reshapes the joint venture for the estimated $35 billion Australian project, highlighting a strategic pivot away from capital-intensive, long-cycle fossil fuel assets by companies like BP, and a simultaneous push by state-backed entities like GS Energy to lock in physical energy resources ahead of anticipated market shifts.

LNG Project De-risking, BP Divestment Signals Broader IOC Strategy Shift

A strategic divide is widening between European International Oil Companies (IOCs) and Asian National Oil Companies (NOCs) regarding long-cycle LNG projects. European majors are prioritizing capital discipline and portfolio optimization by divesting non-operated, high-cost assets, while Asian NOCs are acquiring these same stakes to guarantee national energy security against market volatility.

- The June 2026 sale of a 5% stake in the Browse LNG project by BP to GS Energy shows this trend in action. For BP, the divestment reduces its future capital expenditure exposure to a complex A$48.7 billion ($35 billion) project and aligns with its strategy to fund higher-return businesses. For GS Energy, the acquisition is a direct move to secure stable, long-term LNG supply for South Korea.

- This action contrasts with BP‘s strategy between 2021 and 2024. In April 2023, BP agreed to acquire Shell‘s 27% interest in Browse, consolidating a larger position. The subsequent sell-down to GS Energy demonstrates a two-step “acquire and syndicate” strategy, where BP takes a controlling position before syndicating risk and capital requirements to strategic partners.

- This pattern is part of a broader pivot among European energy majors who are increasingly cautious about committing to decades-long, capital-intensive hydrocarbon projects. This allows capital to be reallocated to designated “transition growth engines” such as bioenergy and EV charging.

- Meanwhile, Asian buyers view these equity stakes as a critical physical hedge. Owning a share of the production provides a buffer against price spikes on the spot market and ensures a reliable supply chain, a lesson reinforced by the energy security challenges of recent years.

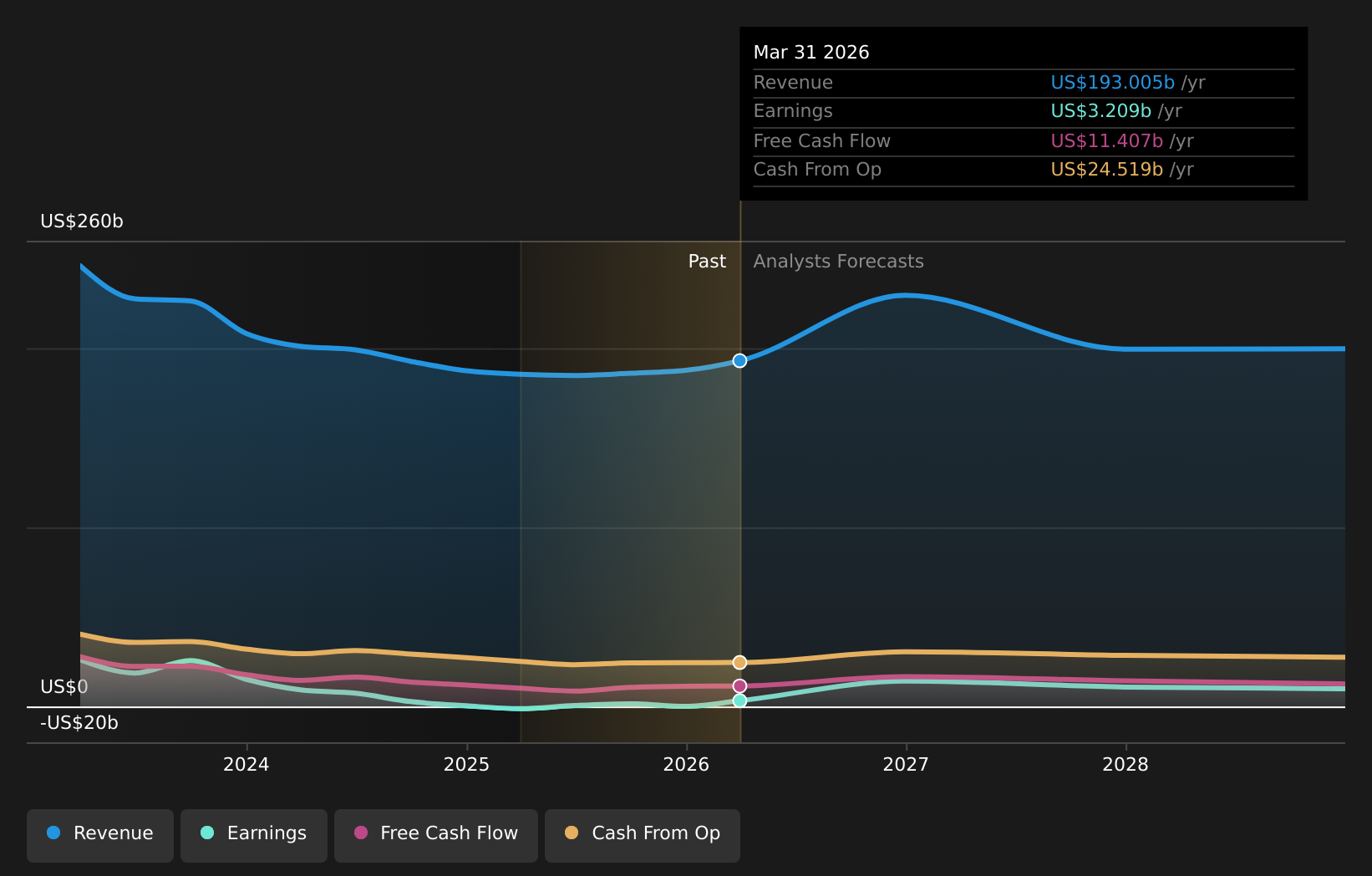

BP Financial Forecasts Amid Portfolio Shift

This chart’s focus on financial forecasts resulting from a portfolio shift directly complements the section’s theme of BP’s broader strategy shift and divestment strategy.

(Source: Simply Wall St)

$35 B Project Valuation, BP and GS Energy Stake Restructuring

The capital flows surrounding the Browse LNG project reveal the differing financial drivers and risk appetites of European sellers and Asian buyers. The transaction structure highlights a clear reallocation of capital from a European major focused on shareholder returns toward a national energy champion focused on long-term supply security.

- The transaction values the 5% stake at approximately $1.75 billion, based on the project’s total estimated cost of $35 billion. This investment secures equity gas for GS Energy but also commits it to significant future capital outlays for the project’s construction.

- For BP, this sale is a component of its broader asset disposal program. The company has a demonstrated history of divesting minority stakes in large, non-operated projects to manage capital exposure and fund strategic priorities that align with its net-zero ambitions, such as its $4.1 billion acquisition of Archaea Energy.

- In contrast, GS Energy‘s investment represents a vertical integration strategy. The equity gas from Browse is expected to support its downstream and international assets, including a planned $3.13 billion, 3, 000 MW LNG-to-power facility in Vietnam scheduled to begin operations in 2029.

- This financial maneuvering is essential for advancing the project toward a Final Investment Decision (FID). Bringing in a creditworthy partner and potential offtaker like GS Energy significantly improves the project’s bankability, which is a prerequisite for securing the massive debt financing required for a development of this scale, a dynamic also seen in projects like Commonwealth LNG.

Browse LNG Project Stakes and Valuation Detailed

This chart directly visualizes the project’s valuation and the stake restructuring mentioned in the section heading, providing the specific data for the discussion.

(Source: Discovery Alert)

Table: Strategic Capital Reallocation in LNG Projects

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| GS Energy (Buyer) | June 2026 | Acquired a 5% stake in the Browse LNG project from BP. The move is designed to secure long-term LNG supply for South Korea and provide a physical hedge against volatile energy prices. | Reuters |

| BP (Seller) | June 2026 | Sold a 5% stake to GS Energy, reducing its holding to 39.33%. This divestment aligns with BP‘s strategy of recycling capital from non-operated assets to fund its energy transition goals. | Guru Focus |

| BP (Acquirer) | April 2023 | Agreed to acquire Shell‘s 27% stake in the Browse project. This initial consolidation gave BP a larger, more influential position before it began syndicating risk to partners. | Reuters |

| GS Energy (Investor) | March 2025 | Announced plans to operate a $3 billion LNG-to-power project in Vietnam. This downstream investment highlights the strategic need for upstream gas supply, which the Browse stake helps fulfill. | The Investor Vina Capital |

Australia vs. Qatar, BP’s Browse Project Faces Cost and Supply Headwinds

Australia’s status as a top-tier LNG exporter is facing significant economic and competitive pressure. The country’s high-cost, complex regulatory environment makes its new projects less competitive just as a wave of lower-cost supply from Qatar and the United States is poised to enter the global market.

- The $35 billion Browse LNG project in Western Australia exemplifies the high capital intensity of Australian developments. Its estimated CAPEX per tonne is substantially higher than new projects in Qatar, such as the $28.75 billion North Field East project, which offers greater economies of scale.

- Starting from 2026, Browse will need to compete in a market absorbing a historic supply expansion. An additional 300 billion cubic meters per year of new LNG capacity is forecast to come online by 2030, dominated by Qatari expansion and the significant US LNG expansion. This could create a supply glut and exert downward pressure on long-term prices.

- The investment climate in Australia has also become more challenging. During the 2021-2024 period, the government’s review of the Petroleum Resource Rent Tax (PRRT) created fiscal uncertainty for developers, adding another layer of risk to long-term investment decisions. This contrasts sharply with the state-directed, streamlined expansion programs in competing jurisdictions like Qatar.

- For buyers like South Korea’s GS Energy, Australia remains a strategically important and politically stable source of energy. However, the economic case for Australian projects is increasingly challenged by the availability of cheaper and more flexible supply from other regions, complicating offtake negotiations.

Browse LNG’s $35 B CCUS Test, BP Manages Technology Risk

The commercial success of the Browse LNG project is fundamentally tied to the effective deployment of a massive Carbon Capture, Utilization, and Storage (CCUS) facility. This technological necessity, driven by the high CO 2 content of the Browse gas fields, introduces considerable cost, complexity, and execution risk that all partners must manage.

- The project’s foundational technology is a brownfield integration strategy. This plan, solidified between 2021 and 2024, involves processing gas from the offshore Browse fields through the existing North West Shelf (NWS) Karratha Gas Plant, avoiding the cost of building a new liquefaction facility.

- Since 2025, the project’s CCUS component has become a central and escalating risk factor. The total project cost estimate has risen to A$48.7 billion, partly due to the expanded scope and cost of the required carbon capture and injection infrastructure.

- This positions Browse as a critical global test for integrating CCUS with new large-scale gas production. Its performance will be a key validation point for whether CCUS can be a viable tool for mitigating emissions from LNG projects with high-CO 2 feed gas, which is essential for meeting climate targets.

- For BP, divesting a portion of its stake is a prudent financial move to mitigate its exposure to this specific technological and execution risk. It effectively transfers a share of the uncertainty to partners like GS Energy, who are willing to underwrite that risk in exchange for securing long-term energy supply.

SWOT Analysis, BP’s Browse Divestment and Market Dynamics

The strategic rationale for the Browse LNG project is supported by robust long-term demand projections from Asia but is simultaneously challenged by significant threats. These include an impending global LNG supply glut, high Australian operating costs, and substantial execution risks tied to its large-scale CCUS component.

- Strengths for the project are its access to vast, undeveloped gas reserves and its cost-effective brownfield integration with the existing North West Shelf infrastructure.

- Its primary Weakness is the high CO 2 content of the raw gas, which necessitates a costly and technologically complex CCUS system.

- The main Opportunity lies in securing long-term offtake agreements with energy-hungry Asian buyers like GS Energy, which de-risks revenue streams and enables project financing.

- However, the project faces material Threats from a potential oversupply of LNG post-2026, Australia’s challenging regulatory landscape, and the technical and financial risks of executing one of the world’s largest CCUS projects.

Table: SWOT Analysis for Browse LNG Project

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Vast gas reserves (Brecknock, Calliance, Torosa fields). Plan to use existing NWS Karratha Gas Plant infrastructure to lower costs. | Brownfield integration with NWS remains a core strength. The JV includes financially strong partners like Woodside, BP, and now GS Energy. | The brownfield strategy was validated as the only economically viable path, but its cost-saving benefit is being eroded by other project cost increases. |

| Weakness | High CO 2 content (~10-12%) in reservoir gas, requiring large-scale CCUS. Remote, deep-water offshore location adds to complexity and cost. | Cost of CCUS and project execution becomes a more acute weakness, with total project CAPEX rising to A$48.7 billion. Long project timeline creates market uncertainty. | The financial and technical burden of the CCUS requirement has become more tangible, contributing directly to cost escalations and highlighting execution risk. |

| Opportunity | Strong long-term LNG demand forecasts from Asian markets seeking to displace coal. Potential to secure foundational offtakers to enable FID. | The entry of GS Energy as an equity partner and potential offtaker provides a clear path to de-risking project financing and securing revenue. | The strategic imperative for Asian energy security was validated by GS Energy‘s investment, confirming a key market for the project’s output. |

| Threat | Anticipated LNG supply wave from Qatar and the U.S. post-2025. Regulatory uncertainty in Australia, including potential tax changes. | The impending supply glut is now a near-term threat, with 300 bcm/y of new capacity expected by 2030. Environmental and regulatory opposition remains a significant hurdle. | The threat of a market oversupply has become more imminent, raising the stakes for securing favorable long-term contracts before committing to the $35 billion spend. |

FID Hurdles, BP and Woodside Need Offtake Agreements for Browse LNG

The path to a Final Investment Decision (FID) for the Browse LNG project now depends almost entirely on the joint venture’s ability to secure binding, long-term offtake agreements. These contracts are needed to underwrite the project’s massive $35 billion cost, a commercial challenge made more difficult by the looming global supply glut and the increasing availability of flexible, hub-priced LNG.

- If the Browse JV, led by operator Woodside, can successfully leverage GS Energy‘s equity participation into a cornerstone Sales and Purchase Agreement (SPA), then watch for other Asian buyers to commit, creating the commercial foundation needed to approve the project.

- A key signal to monitor is the pricing structure of these new offtake contracts. A strong preference for traditional oil-linked pricing would protect the project’s economics, while a shift toward hub-based pricing (e.g., JKM) would expose Browse to more direct price competition from lower-cost producers.

- This could be happening as buyers assess the value of Australian supply security against the coming wave of LNG. The negotiation of these offtake agreements will be the ultimate determinant of the project’s bankability and its ability to proceed in a market facing a potential supply surplus.

The questions your competitors are already asking

This report covers one angle of the strategic divergence between European and Asian companies in the global LNG market. The questions that matter most depend on your work.

- Which European IOCs are de-risking from Australian LNG, and which Asian NOCs are gaining ground by acquiring these stakes?

- Woodside’s Browse LNG investments. Is the $35 billion project on track for a Final Investment Decision (FID) by 2026?

- BP’s activities in LNG divestment. Is its portfolio de-risking strategy progressing from one-off sales to a broader program?

- What are the acquisition opportunities for other Asian buyers in the non-operated Australian LNG equity market?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.