US-Iran War 2026: How Geopolitical Shock Fractures the Global Energy Transition

The US-Iran conflict of early 2026 has fundamentally altered the global energy transition, creating a bifurcated world where national security, not climate policy, is the primary driver of renewable energy deployment. The immediate turmoil of soaring fossil fuel prices and macroeconomic instability creates significant short-term headwinds, threatening to slow progress. The long-term impact, however, is a powerful and irreversible acceleration of the transition in major energy-importing regions like the EU and Asia, which now view domestic renewable generation as a critical component of economic and national security. This fractures the global transition into two distinct paths: security-driven accelerators and fossil-focused resistors.

Geopolitical Risk in 2026: How US-Iran Conflict Disrupts Global Energy Markets

The initial military conflict created immediate and severe disruptions across global energy markets, exposing the profound fragility of a supply chain dependent on geopolitical chokepoints. This shockwave of volatility sent energy prices soaring and demonstrated the acute economic costs of fossil fuel dependency.

- The blockade of the Strait of Hormuz, which controls about 20% of the world’s oil supply, was the main driver of volatility. Benchmark Brent crude prices surged, with initial reports showing a 7% jump to over $74 a barrel as tensions built, while scenarios involving a sustained closure projected prices reaching as high as $140 per barrel.

- The conflict’s impact quickly spread to LNG supply chains, a critical fuel source for Europe and Asia. European gas prices jumped after Qatar Energy, a major global supplier, halted LNG production following an Iranian drone attack, with a full Hormuz blockade scenario showing prices could exceed $40/MMBtu.

- Operational costs for energy transport increased dramatically. War risk insurance premiums for tankers transiting the Persian Gulf, which were 0.1-0.5% of cargo value pre-conflict, spiked to between 1.0-2.0% during the initial phase of hostilities, adding significant costs to every shipment.

Investment Headwinds 2026: Why Rising Costs and Policy Shifts Stall Renewable Projects

Despite making renewables more competitive on paper, the conflict’s macroeconomic fallout created powerful near-term headwinds that stalled investment and delayed projects. The combination of high inflation, rising interest rates, and divergent policy responses made financing capital-intensive clean energy projects significantly more challenging.

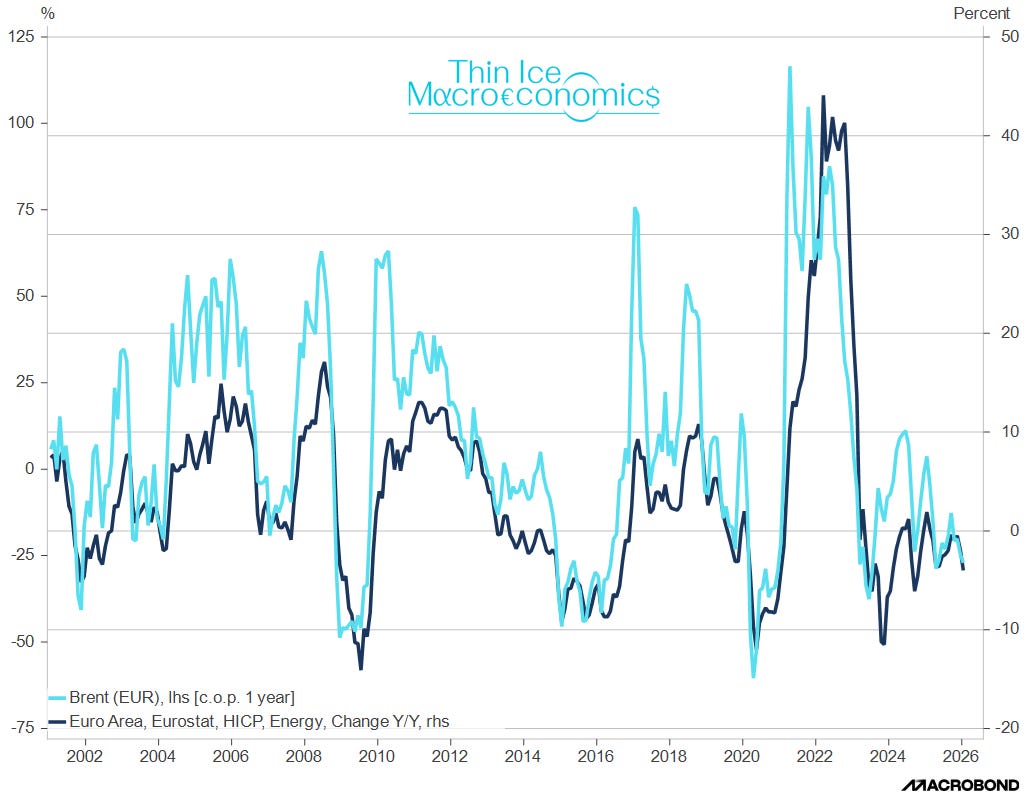

Oil Price Shocks Directly Fuel Inflation

This chart demonstrates the direct correlation between oil price shocks and inflation, visually explaining the mechanism described in the text where higher energy prices fuel the inflation stalling renewable projects.

(Source: Thin Ice Macroeconomics – Substack)

- Higher energy prices fueled inflation, forcing central banks to maintain high interest rates. This disproportionately impacts renewables, as a 2% rise in interest rates increases the levelized cost of energy (LCOE) for a new solar or wind project by 20%, compared to just an 11% increase for a less capital-intensive gas plant.

- This cost pressure was evident even before the conflict. In late 2023, high interest rates and supply chain issues led Ørsted to cancel two major offshore wind projects in New Jersey, citing a “perfect storm” of rising costs that made the projects financially unviable. The war amplified these pre-existing vulnerabilities across the sector.

- The political response to the crisis was not uniform, creating policy uncertainty for investors. The Trump administration signaled a strategy of “Energy Dominance, ” prioritizing increased US fossil fuel production to manage global prices, which included delaying approvals for renewable energy projects and creating a significant drag on the domestic transition.

Table: Cost Dynamics and Economic Viability: LCOE Sensitivity to Interest Rates

| Energy Source | Capital Intensity | LCOE Increase from 2% Interest Rate Rise | Source |

|---|---|---|---|

| Solar / Wind | High | 20% | Reuters |

| Natural Gas Plant | Low | 11% | Reuters |

A Fractured Globe: Regional Divergence in the Post-Conflict Energy Transition

The conflict’s most profound long-term consequence is the fracturing of the global energy transition into distinct, competing blocs. National interests and energy import dependency, not unified climate goals, now dictate the pace and direction of decarbonization, creating a world of divergent energy strategies.

Asia’s Heavy Reliance on Strait of Hormuz

The chart highlights the critical import dependency of Asian nations like China and India on energy transiting the Strait of Hormuz, supporting the section’s argument that these importers are ‘Security-Driven Accelerators’.

(Source: The National News)

- The Security-Driven Accelerators: The European Union, China, and India, all major energy importers, are interpreting the crisis as a definitive mandate to accelerate their transition to domestic renewables. Having learned from its dependency on Russian gas after 2022, the EU is fast-tracking its green energy build-out, while Asian powers are moving to mitigate their exposure to Middle Eastern supply disruptions.

- The Fossil-Focused Resistors: In contrast, the United States, possessing significant domestic fossil fuel reserves, has leaned on its “Energy Dominance” policy. The strategic focus has shifted to increasing oil and gas output to stabilize global prices and exert geopolitical influence, a move that provides short-term economic relief but risks delaying long-term investment in clean energy infrastructure.

- The Stranded Nations: Iran and other nations directly impacted by the conflict are being left behind. Before the war, Iran had ambitions to add 10 GW of solar capacity. The conflict and subsequent economic collapse have rendered these goals impossible, cementing the country’s dependence on fossil fuels and isolating it from the global transition.

Technology Maturity Post-2026: Green Hydrogen and Domestic Supply Chains Become National Security Imperatives

The US-Iran conflict has elevated certain clean energy technologies from long-term climate solutions to immediate national security necessities. The focus on energy independence is accelerating the technological and commercial maturity of sovereign energy sources like green hydrogen and localized battery manufacturing.

Solar and Wind Poised to Dominate Growth

As the section discusses a post-conflict focus on specific clean technologies, this chart’s future scenarios show that wind and solar are expected to comprise the vast majority of renewable capacity growth through 2030.

(Source: ScienceDirect.com)

- Green Hydrogen has emerged as a key strategic alternative to volatile natural gas. The conflict amplified its importance for energy independence, building on momentum from policies like the Inflation Reduction Act. The market, valued at $2.79 billion in 2025, is now projected to expand to $74.81 billion by 2032, a compound annual growth rate of 60%.

- The crisis has exposed the strategic risk of concentrated supply chains, particularly the world’s reliance on China for battery components. This has intensified efforts in the US and EU to onshore manufacturing, leveraging policies like the IRA to build resilient, domestic supply chains for next-generation battery technologies.

- Sustained high oil and gas prices permanently improve the economic case for mature renewables. Technologies like solar panels, wind turbines, and heat pumps, which offer stable and predictable energy costs insulated from geopolitical shocks, become the default choice for new capacity in energy-importing nations.

SWOT Analysis: The US-Iran War’s Impact on the Energy Transition

The conflict acts as a powerful external shock that both exacerbates existing weaknesses in the energy transition while creating undeniable long-term strategic opportunities. It fundamentally reframes the core drivers of the transition from environmentalism to national security.

Geopolitical Tensions Drive Energy Market Volatility

This conceptual image perfectly sets the theme for the SWOT analysis by visually linking geopolitical tensions in Iran with the volatility of energy markets, framing the core conflict the section introduces.

(Source: SCMP)

Table: SWOT Analysis for the Global Energy Transition Post-Conflict

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Maturing technologies (solar/wind LCOE falling); Strong policy support (e.g., US Inflation Reduction Act). | Inherent price stability of renewables; Value of energy independence becomes paramount; Domestic manufacturing base growing. | The core value proposition of renewables shifted from being primarily climate-focused to a critical tool for national and economic security. |

| Weaknesses | High capital intensity of projects; Sensitivity to interest rates (e.g., Ørsted cancellations); Concentrated supply chains (e.g., China). | Acutely exposed to inflation and high cost of capital; Macroeconomic instability deters private investment; Policy divergence creates market uncertainty. | The conflict validated that the transition’s financial and supply chain vulnerabilities were its Achilles’ heel, turning theoretical risks into acute crises. |

| Opportunities | Growing public and corporate demand for clean energy; Innovation in next-generation technologies (e.g., hydrogen, batteries). | Accelerated, state-sponsored deployment in energy-importing regions (EU, Asia); Massive market creation for green hydrogen; Permanent geopolitical risk premium on fossil fuels. | The war created an undeniable strategic imperative for energy independence, unlocking levels of state-driven investment and policy support previously unattainable. |

| Threats | Geopolitical tensions in energy-producing regions; Global inflation; Grid integration challenges. | Direct military conflict disrupting 20% of global oil supply; Global recession triggered by energy price shock; Policy reversals favoring fossil fuel security. | The conflict transformed simmering geopolitical tensions into a full-blown energy security crisis, proving that fossil fuel dependency is a direct threat to economic stability. |

Forward Outlook: A Volatile but Accelerated Path to Energy Independence

The critical forward-looking expectation is that major energy-importing blocs, particularly the EU and parts of Asia, will now treat investment in domestic clean energy infrastructure as a non-negotiable national security strategy. This will sustain the transition’s momentum despite near-term economic pain and financial market volatility.

Geopolitical Shocks Accelerate EU Renewables Adoption

This chart provides a powerful historical precedent for the section’s forward outlook, showing how a previous geopolitical shock spurred a dramatic acceleration in EU renewable installations, supporting the prediction for 2026.

(Source: Bloomberg.com)

- If sustained high energy prices persist through 2026, watch for accelerated policy support in the EU and India for renewables and grid infrastructure. This will validate that energy security has become the primary driver, outweighing short-term cost concerns.

- If central banks maintain high interest rates to combat inflation, expect continued pressure on renewable project financing. The key signal will be whether governments step in with enhanced subsidies or guarantees to offset the high cost of capital, separating the “accelerators” from those who will see their transitions stall.

- The trend gaining the most traction is the strategic pivot to green hydrogen. Previously a long-term goal, it is now seen as a near-term tool for energy sovereignty. Watch for an increase in final investment decisions for large-scale electrolyzer projects in 2026 and 2027.