SMR Data Center Projects, 960 MW Amazon Deal, 835 MW Microsoft PPA, and 6 Key Agreements (2023-2026)

Data Center Power Strategy, 6 Major Tech Firms Secure Nuclear PPAs and Assets

Technology firms are shifting from treating electricity as a utility expense to integrating power generation as a core component of their compute infrastructure, driven by the failure of public grids to meet AI-driven demand.

- Prior to 2024, tech firms primarily relied on the grid and intermittent renewable PPAs, but the explosive power demand of AI, projected to grow at a 15% CAGR to 2030, exposed this as an untenable long-term strategy.

- Starting in March 2024, the strategy pivoted toward securing baseload power through direct asset control, highlighted by Amazon’s $650 million acquisition of a nuclear-powered data center campus from Talen Energy.

- This trend accelerated through 2024 and into 2026, with Microsoft funding the restart of the 835 MW Three Mile Island plant and Google signing a 500 MW deal with SMR developer Kairos Power, indicating a move beyond existing assets to enabling new nuclear capacity.

- The Digi Power X and NNE MOU represents the next phase, where specialized HPC developers, not just hyperscalers, are partnering to develop new, co-located nuclear facilities from the ground up, aiming to create a decisive competitive advantage by bypassing the grid entirely.

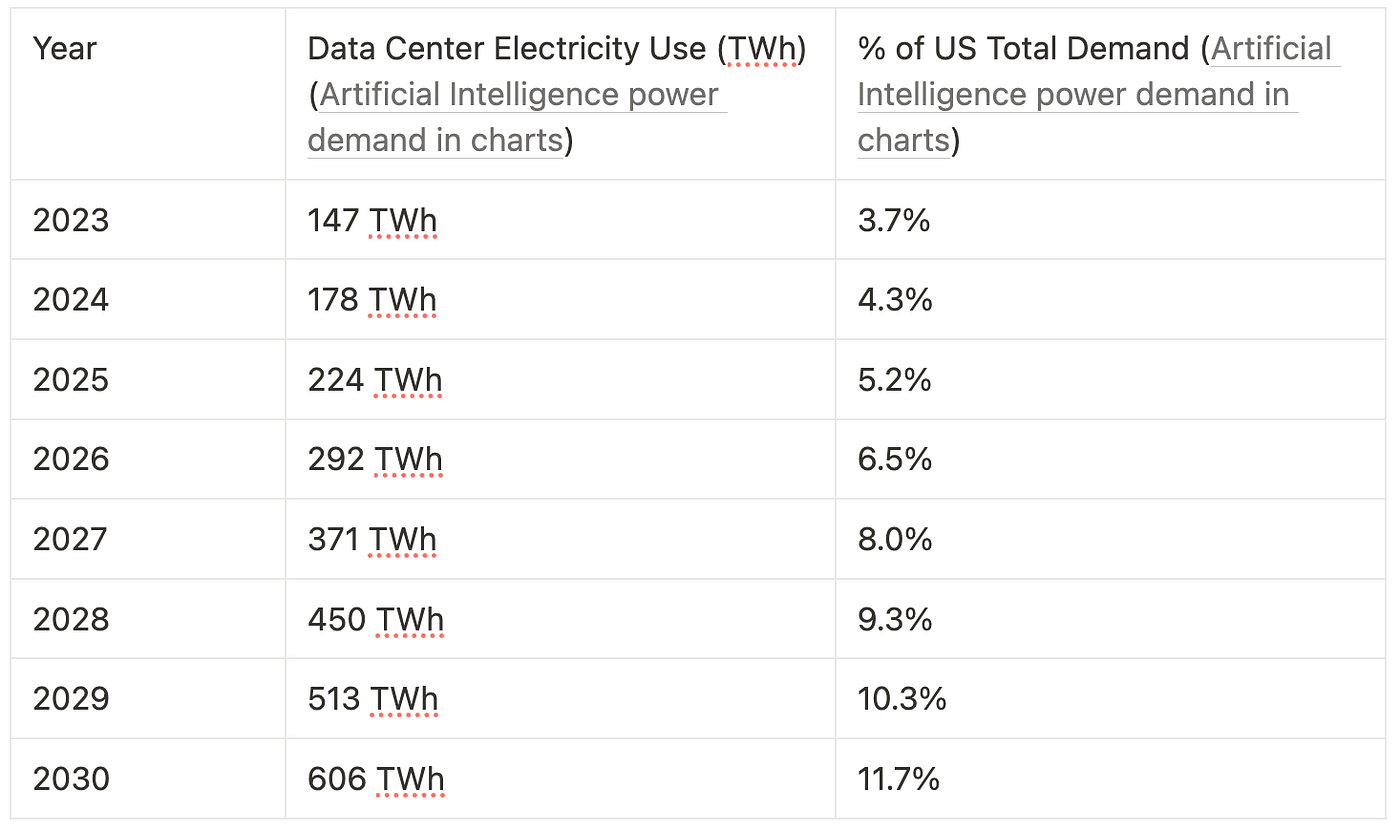

AI Power Demand to Exceed 11% of US Total by 2030

This forecast quantifies the ‘explosive power demand of AI’ mentioned in the text, showing a projected quadrupling by 2030. This growth is the core driver behind the strategic pivot to nuclear power.

(Source: James Soldinger – Medium)

$650 M Amazon Acquisition, Microsoft & Google Lead Nuclear Data Center Investment

Capital allocation has decisively shifted from passive renewable energy credits to direct investment in nuclear assets and development partnerships, de-risked by federal incentives like the Inflation Reduction Act’s Production Tax Credit (PTC).

- Amazon‘s $650 million acquisition of the Talen Energy campus in March 2024 was a landmark transaction, moving beyond PPAs to direct ownership of power-adjacent infrastructure.

- Microsoft‘s $1.6 B deal in March 2026 to restart Three Mile Island and its earlier September 2024 PPA with Constellation Energy show a dual strategy of supporting existing and revived nuclear fleets.

- Despite the momentum, investment risk remains, as shown by the cancellation of the Nu Scale Power SMR project in Idaho, which cited rising costs that pushed the target price above $89/MWh.

- The 2022 Inflation Reduction Act (IRA) provides critical financial underpinning, offering a PTC of up to $15/MWh for nuclear generation and a significant Investment Tax Credit (ITC) that improves the economic case for high-CAPEX new builds.

Table: Nuclear Data Center Capital Events

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Microsoft / Three Mile Island | Mar 2026 | Microsoft committed $1.6 B to support the restart of the Three Mile Island Unit 1 nuclear reactor to power its data centers, signaling a willingness to fund major capital projects to secure carbon-free baseload power. | Introl Blog |

| Amazon / Talen Energy | Mar 2024 | Amazon Web Services acquired the Cumulus data center campus from Talen Energy for $650 million. The campus is directly connected to the 2.5 GW Susquehanna nuclear plant, providing 960 MW of power capacity. This represents a strategic move toward owning power-adjacent infrastructure. | ANS News |

| Nu Scale Power / UAMPS (Cancelled) | Nov 2023 | Nu Scale’s first-of-a-kind SMR project with Utah Associated Municipal Power Systems was cancelled due to escalating costs, with the target power price rising from $58/MWh to over $89/MWh. This highlights the significant financial risk of new nuclear builds. | Union of Concerned Scientists |

Big Tech 6 Nuclear Partnerships, Amazon and Microsoft Lead SMR Integration (2023-2026)

A new ecosystem of partnerships is forming to distribute the immense technical, financial, and regulatory risk of developing first-of-a-kind SMR-powered data centers.

- Hyperscalers like Amazon, Microsoft, and Google are acting as anchor offtakers, providing the revenue certainty needed to secure project financing for nuclear developers.

- SMR technology developers such as Nu Scale, X-energy, Kairos Power, and Oklo are partnering with both tech firms and specialized data center developers like Standard Power to gain a commercial foothold.

- Utilities and energy companies, like Talen Energy and Constellation, are leveraging their existing nuclear assets and operational expertise to create new revenue streams by directly serving the data center market.

- The Digi Power X and NNE MOU exemplifies this model, pairing an HPC demand aggregator (Digi Power X) with a nuclear project developer (NNE) for a vertically integrated approach.

Table: Key Nuclear Data Center Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Google / Kairos Power | Oct 2024 | Google signed a deal for 500 MW of power from advanced reactor developer Kairos Power. This partnership is aimed at securing carbon-free power for Google‘s data centers and helping commercialize a new reactor technology. | Utility Dive |

| Microsoft / Constellation Energy | Sep 2024 | Microsoft signed a 20-year PPA with Constellation to offtake power from the restart of the Three Mile Island Unit 1 reactor, providing a long-term revenue stream to support the plant’s revival. | Microsoft Blog |

| Oklo / Wyoming Hyperscale | May 2024 | SMR developer Oklo partnered with Wyoming Hyperscale to provide 100 MW of power from its Aurora microreactors, demonstrating a model for powering smaller, dedicated data center campuses. | Oklo.com |

| Standard Power / Nu Scale Power | Oct 2023 | Data center developer Standard Power chose Nu Scale‘s SMR technology to power two planned facilities in Ohio and Pennsylvania, aiming to develop nearly 2 GW of clean energy for its operations. | Business Wire |

US Focus, Digi Power X and Amazon Concentrate Nuclear Data Centers in Key States

The development of nuclear-powered data centers is currently concentrated in the United States, specifically in states with existing nuclear infrastructure, favorable regulatory environments, and proximity to data center alleys.

- States like Pennsylvania and Ohio are primary targets due to their industrial history and existing nuclear sites, as seen in Amazon‘s acquisition in Pennsylvania and Standard Power‘s planned SMR sites in both states.

- Wyoming is emerging as a key location for new advanced reactor projects, with Oklo partnering with Wyoming Hyperscale and Terra Power developing its Natrium reactor project in the state.

- The geographic strategy involves co-locating on or near existing nuclear plant sites, which simplifies permitting, grid connection (if needed), and leverages an existing skilled workforce.

- However, state-level politics introduce risk. For example, Illinois, a major data center hub, announced a two-year suspension of data center tax incentives in February 2026 due to concerns over resource strain, signaling potential local headwinds against unrestrained growth.

SMR Technology Readiness, Digi Power X Faces TRL 6-7 to TRL 9 Commercialization Gap

While conventional large-scale nuclear technology is mature, the Small Modular Reactors (SMRs) envisioned for these new data center projects are largely at the prototype demonstration phase (TRL 6-7), posing a significant commercialization risk.

- Prior to 2024, most deals, like Amazon‘s PPA for the Cumulus campus, relied on power from existing, proven large-scale reactors.

- The current wave of partnerships, including those by Google with Kairos Power and Standard Power with Nu Scale, depend on SMR designs that have not yet achieved full commercial operation (TRL 9).

- This transition from prototype to commercial scale is the “valley of death” for hard tech, where projects face risks of cost overruns and delays, as exemplified by the cancellation of the Nu Scale UAMPS project.

- Success hinges on developers like NNE, X-energy, and Kairos Power proving their technology can be manufactured and operated reliably and cost-effectively, a process that will unfold over the next 3-5 years.

$1.6 B Microsoft Deal, A SWOT Analysis of Nuclear Power for Data Centers

The strategy to power data centers with nuclear energy presents a powerful solution to the AI power crisis but is constrained by significant execution, regulatory, and financial risks.

- Strengths: The primary strength is securing a 24/7, carbon-free, gigawatt-scale power source that bypasses public grid constraints, offering a decisive competitive moat.

- Weaknesses: The strategy is dependent on SMR technologies that are not yet commercially proven and faces major supply chain bottlenecks for critical nuclear components.

- Opportunities: Favorable federal policy, including massive tax credits under the IRA, has fundamentally improved project economics, while ESG pressure on AI’s energy footprint creates a strong market pull.

- Threats: Nuclear project execution is notoriously difficult, with high risks of construction delays and cost overruns. Shifting political winds, loss of social license, or competition from breakthroughs in other clean firm power technologies pose long-term threats.

Table: SWOT Analysis for Nuclear Data Center Strategy

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Theoretical advantage of 24/7 clean power. Small-scale PPAs from existing nuclear plants. | Proven via multi-billion dollar deals (Amazon, Microsoft) for GW-scale capacity. Bypassing grid queues becomes a key competitive advantage. | The strategic value of grid independence and baseload power was validated by hyperscaler capital allocation. |

| Weaknesses | High perceived cost of new nuclear. Lack of recent construction experience. Public opposition. | SMR “first-of-a-kind” costs remain a major hurdle (e.g., Nu Scale cancellation). Supply chain bottlenecks for forgings and vessels are now acute. | The execution risk, both in cost and supply chain, was validated as the primary internal weakness of the strategy. |

| Opportunities | Anticipation of federal support for clean energy. Growing corporate demand for carbon-free power. | The 2022 IRA and 2025 OBBBA provided massive, bankable tax credits (30-50% ITC). Explosive AI demand created an existential need for new power generation. | The policy and market drivers materialized far more strongly and quickly than anticipated, creating a powerful tailwind. |

| Threats | Political risk. Long regulatory timelines for new plant approvals. Competition from cheap natural gas. | State-level friction against data centers emerges (e.g., Illinois). Tight timelines for tax credit eligibility (2026/2027 deadlines). | The threat shifted from federal opposition to local/state-level resistance and the practicalities of meeting policy deadlines. |

Forward Signals, Digi Power X MOU Conversion to PPA is the Key Catalyst

The most critical near-term signal to watch is the conversion of non-binding MOUs, like the one between Digi Power X and NNE, into definitive, bankable Power Purchase Agreements (PPAs).

- A binding, long-term PPA announcement would validate the project’s initial feasibility and signal a move toward securing billions in project financing.

- The submission of a formal license application to the U.S. Nuclear Regulatory Commission (NRC) by a developer like NNE would represent a costly and legally significant milestone, confirming serious commitment.

- Watch for further replication by competitors. If other specialized data center firms or hyperscalers announce similar MOUs with SMR developers, it will confirm a fundamental industry-wide shift.

- The speed and cost at which the first few SMR projects are completed will be the ultimate validation. A successful first-of-a-kind project completed on time and budget would significantly de-risk the entire sector.

The questions your competitors are already asking

This report covers one angle of the direct integration of nuclear power with AI data center infrastructure. The questions that matter most depend on your work.

- DigiPower X and NNE activities. Is the MOU for nuclear-powered HPC data centers progressing to a firm contract and site selection?

- Which tech companies are gaining or losing ground in the race to secure dedicated nuclear power for AI workloads?

- What is the outlook for SMR (Small Modular Reactor) deployment to power data centers by 2030?

- How does the strategy of co-locating new-build SMRs compare to acquiring existing nuclear assets for powering AI data centers?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.