Onshore Wind 2026: Europe’s Supply Chain Crisis Threatens Energy Security

European Wind Projects Accelerate as Supply Chain Risks Mount

Europe’s accelerated onshore wind deployment in 2025 is creating a critical conflict between financially strained domestic turbine manufacturers and developers seeking cost-effective supply chains, who are now turning to Chinese alternatives. This strategic pivot threatens to trade one form of energy dependency for another, undermining the continent’s industrial base just as it scales up renewable generation to meet climate and security goals.

- Between 2021 and 2024, European Original Equipment Manufacturers (OEMs) like Vestas and Siemens Gamesa faced severe profitability challenges from rising material costs and intense price pressure in auctions, despite controlling the domestic market.

- This dynamic reached a critical point in 2025, when Danish developers Eurowind and Wind Estate were reported to be actively considering Chinese-made turbines. This move represents a direct reaction to cost pressures and an attempt to optimize project capital expenditure.

- The shift from theoretical competition to tangible commercial consideration by established European developers validates the threat of market share erosion for incumbent OEMs and signals a potential realignment of Europe’s entire wind manufacturing value chain.

Chinese Manufacturers Dominate Global Wind Turbine Supply

This chart illustrates the supply chain risk facing Europe, as six of the top ten global turbine suppliers in 2024 are Chinese firms. This market dominance underpins the trend of developers seeking cost-effective alternatives outside of Europe.

(Source: Windletter – Substack)

Investment Surges into Projects While Policy Scrambles to Protect Manufacturing

Investment patterns in 2024-2025 reveal a dual strategy: while massive private capital flows into new project deployment, public financial institutions are simultaneously deploying targeted instruments to de-risk and support the struggling European manufacturing base. This bifurcation highlights the market’s confidence in wind as an asset class but acknowledges the underlying weakness of its industrial foundation.

European Onshore Wind Investment Hits Eight-Year High

Confirming the surge in project deployment, investment in European onshore wind recovered to €24.7 billion in 2024. This marks its highest level since 2016, highlighting market confidence in wind projects as an asset class.

(Source: WindEurope)

- Major developers are committing substantial capital to deployment. RWE, for example, plans to make net investments of approximately €35 billion between 2025 and 2030 in new wind, solar, and battery storage projects.

- The commercial viability of new projects is strengthening, reducing reliance on subsidies. In 2025, European Energy demonstrated this by securing 20 long-term Power Purchase Agreements (PPAs) for 1.2 GW of renewable assets, proving project bankability through market-based offtake.

- In direct response to manufacturing fragility, the European Investment Bank (EIB) approved a €5 billion initiative in late 2023 specifically to support European wind equipment manufacturing. This program is a clear policy countermeasure designed to bolster the domestic supply chain against external price competition.

Table: Key Financial Commitments in European Onshore Wind (2023-2025)

| Entity / Initiative | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| RWE | 2025 – 2030 | Announced plan for €35 billion in net investments into its green portfolio, with a significant portion allocated to onshore wind and solar build-out in key European and North American markets. | RWE |

| European Energy | 2025 | Secured 20 long-term offtake agreements (PPAs) covering a 1.2 GW portfolio of renewable projects, signaling a strong market for subsidy-free development. | European Energy |

| European Investment Bank (EIB) | Dec 2023 | Committed €5 billion in financing to support the European wind energy manufacturing industry, aiming to de-risk investment and maintain the continent’s industrial competitiveness. | EIB |

Partnerships in 2025 Aim to Secure Supply Chains and Enter Growth Markets

Strategic partnerships formed in 2024 and 2025 have shifted focus toward securing technology pipelines and accessing new high-growth geographies. These alliances are a direct response to supply chain volatility and the need to build large, multi-gigawatt portfolios to meet national and EU-level targets.

- The April 2025 letter of intent between German utility RWE and turbine OEM Enercon for long-term cooperation on European onshore wind projects exemplifies a vertical collaboration strategy. It aims to secure turbine supply and streamline project execution for a large-scale deployment pipeline.

- Developers are using joint ventures to establish a foothold in emerging European markets. Uniper entered a development partnership for a 600 MW onshore wind portfolio in Poland, while Renewable Power Capital and Tundra Advisory formed a JV to develop up to 1, 000 MW in the same market.

- OEMs are proactively securing future demand. In November 2024, ENERCON signed a Memorandum of Understanding with Turkish partners to install a further 2, 500 MW of its turbines, locking in a significant order book in Europe’s sixth-largest onshore market.

Table: Strategic Partnerships Shaping Europe’s Onshore Wind Sector

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| RWE & Enercon | Apr 2025 | Signed a letter of intent for a long-term cooperation on onshore wind projects, linking a major developer with a key OEM to secure future turbine supply. | Blue Cluster |

| ENERCON, İs-Enerji, & Polat Enerji | Nov 2024 | Mo U for the installation of an additional 2, 500 MW of wind turbines in Türkiye, securing a large-scale pipeline for the German OEM in a key regional market. | ENERCON |

| Uniper & Partner | Jun 2024 | Entered a development partnership for a 600 MW onshore wind portfolio in Poland across six early-stage projects, establishing a strong presence in a key Eastern European growth market. | Uniper |

| Low Carbon & Rezolv Energy | Sep 2022 | Partnered to deliver the 450 MW ‘Vis Viva’ wind farm in Romania, one of the largest onshore projects in the region, signaling the rise of Southeast Europe as a development hub. | Low Carbon |

Geography of Onshore Wind: Germany Accelerates as Eastern Europe Emerges

While Germany remains Europe’s onshore wind powerhouse, a significant wave of new large-scale project development is now concentrated in Eastern Europe. Countries like Romania and Poland are becoming critical demand centers, driven by decarbonization goals and the pursuit of energy independence.

Germany Leads Europe in New Wind Installations

Germany reaffirmed its role as Europe’s onshore wind leader in 2024, accounting for a quarter of all new capacity. This data supports the section’s focus on Germany’s accelerated deployment compared to other European nations.

(Source: WindEurope)

- Germany continues to lead in both installed capacity and generation, producing 106.5 billion k Wh from its onshore fleet in 2025. Its market is now a testbed for the transition from subsidies to a hybrid PPA model.

- The most significant new projects announced for the 2024-2025 period are located in Romania. This includes a 476 MW project by PPC Renewables using GE Vernova turbines and the 450 MW ‘Vis Viva’ project developed by Low Carbon and Rezolv Energy.

- Poland has solidified its position as a major growth frontier. Development partnerships from Uniper (600 MW) and a joint venture between Renewable Power Capital and Tundra Advisory (up to 1, 000 MW) underscore a massive future project pipeline.

- The UK market is positioned for a significant resurgence post-2025 following the lifting of de facto planning restrictions, with analysis indicating a need for an additional 12.8 GW to 14.8 GW of onshore capacity to meet climate targets.

Technology Maturity: Focus Shifts from Turbine Innovation to Supply Chain Origin

Onshore wind is a fully commercialized and cost-competitive technology, but the defining variable in 2025 is no longer turbine performance alone. The strategic focus has shifted to the manufacturing origin of components and the associated geopolitical, economic, and security implications of sourcing decisions.

Chinese OEM Market Share Is Concentrated Domestically

Highlighting the strategic importance of supply chain origin, this chart shows that Chinese OEM dominance in 2023 was primarily confined to their domestic market. This context is critical for understanding the potential geopolitical impact of their expansion into Europe.

(Source: Wood Mackenzie)

- Between 2021 and 2024, the primary technology trend involved incremental gains in turbine efficiency and the repowering of aging wind farms with more powerful units, as seen in projects like Germany’s Waldfeucht repowering with new Nordex turbines.

- The pivotal change in 2025 is the open and viable consideration of Chinese turbines by established European developers. While technologically mature, these machines introduce new variables related to long-term operational support, cybersecurity, data governance, and political risk that are not priced into the initial capital cost.

- European OEMs are now attempting to compete on factors beyond cost and output. Vestas‘s introduction of low-emission steel offerings for its turbines, starting with projects in 2025, is a clear strategy to differentiate on sustainability and life-cycle metrics, creating an alternative value proposition.

SWOT Analysis for European Onshore Wind

The European onshore wind market’s core strength, which is its mature technology and strong policy support, is directly challenged by the critical weakness of its strained domestic supply chain. This tension creates a clear opportunity for non-European OEMs to gain market share and poses a significant threat to the continent’s long-term industrial competitiveness and energy security.

European Wind Installations Remained Strong in 2023

This chart illustrates a key ‘Strength’ from the SWOT analysis: a mature and robust market. Europe’s addition of 18.3 GW of new wind capacity in 2023 demonstrates the strong developer ecosystem and policy support mentioned in the text.

(Source: Evwind)

Table: SWOT Analysis for European Onshore Wind (2021-2025)

| SWOT Category | 2021 – 2024 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Strong policy support (EU Green Deal); proven, cost-competitive technology; established developer ecosystem. | Accelerated permitting under new EU rules; robust PPA market emerges as a viable alternative to subsidies. | The effectiveness of EU permitting reforms was validated in 2025 with 23 GW of onshore projects approved in 18 months. The PPA model was validated by European Energy‘s 1.2 GW in offtake agreements. |

| Weaknesses | Slow and complex permitting processes; financial instability and low profitability for European OEMs. | OEM profitability remains weak despite growing order books; dependence on a concentrated European supply chain. | Despite policy support like the EIB’s €5 B fund, the core profitability issue for OEMs like Siemens Gamesa was not resolved. Permitting began to ease, but was not fully eliminated as a bottleneck. |

| Opportunities | Expansion into new markets (e.g., Eastern Europe); large-scale repowering of aging wind farms. | Massive capacity needs in the UK market; leveraging partnerships (e.g., RWE/Enercon) to secure supply; sourcing lower-cost turbines from China. | The opportunity to source from China moved from theoretical to practical in 2025, as confirmed by developers like Eurowind. The scale of the UK opportunity became clearer with new capacity requirement estimates. |

| Threats | Rising material and logistics costs; potential for Chinese OEMs to enter the European market. | Tangible consideration of Chinese turbines by European developers; risk of shifting supply chain dependency from Russian gas to Chinese hardware. | The threat of Chinese competition was validated in 2025. It is no longer a future risk but a current commercial dynamic that threatens to cause a severe energy crisis for the European industrial base. |

Scenario for 2026: Europe at a Trade Policy Crossroads

For 2026, if a major European developer or utility formalizes a large-scale order for Chinese-made turbines, the primary signal to watch will be the initiation of EU-level trade defense measures, such as anti-subsidy investigations or tariffs, aimed at protecting Europe’s domestic manufacturing base.

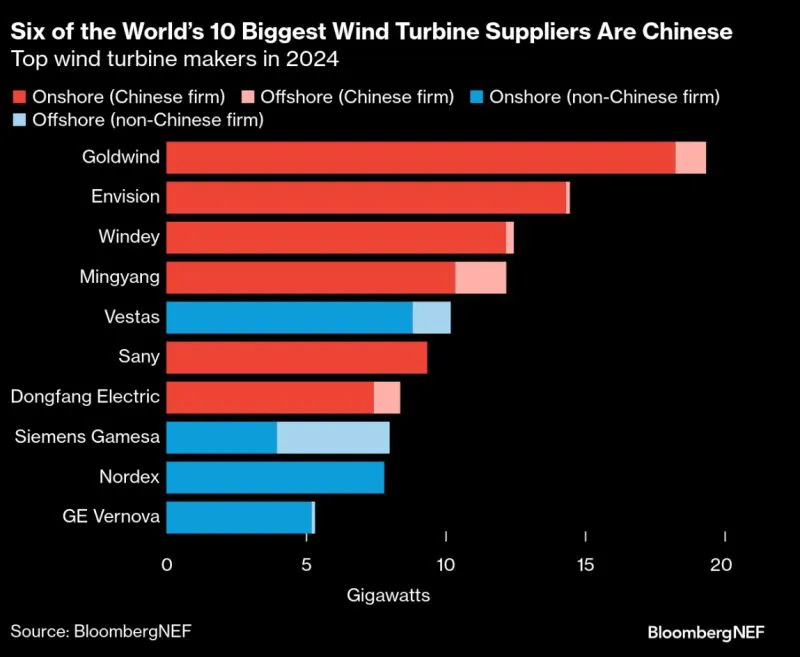

Goldwind and Envision Led Global Turbine Market

This chart substantiates the 2026 scenario by showing that Chinese firms Goldwind and Envision were the top two global turbine makers in 2023. Their massive scale makes the prospect of a large European order, and subsequent trade policy conflict, a credible threat.

(Source: Clean Energy Wire)

- The most critical leading indicator is a firm, multi-hundred-megawatt turbine order from a European developer for a project on European soil placed with a Chinese OEM like Goldwind, Envision, or Mingyang.

- The public consideration of Chinese turbines by Danish developers Eurowind and Wind Estate in 2025 is the most potent signal that this trend is gaining traction and that cost pressures may be outweighing geopolitical and supply chain risks for some developers.

- A counter-signal is the strategic deepening of all-European partnerships, such as the RWE-Enercon alliance. This suggests the market could fragment, with one segment prioritizing lowest-cost CAPEX via imports and another prioritizing supply security, political alignment, and life-cycle value with domestic OEMs. The outcome of this tension will define the European wind industry for the next decade.

Frequently Asked Questions

Why are European wind developers considering buying Chinese turbines?

European developers, such as Denmark’s Eurowind and Wind Estate, are considering Chinese turbines primarily to reduce costs. Faced with intense price pressure, they are looking for more cost-effective supply chains to optimize project capital expenditure, even though it creates a strategic conflict with struggling domestic manufacturers.

What is being done to help the struggling European turbine manufacturers?

There are two main responses. First, financial institutions like the European Investment Bank (EIB) have launched initiatives, such as a €5 billion fund, to de-risk and support European manufacturing. Second, companies are forming strategic partnerships, like the one between RWE and Enercon, to create a stable, long-term demand for European-made turbines.

Which European manufacturers are mentioned as facing challenges, and why?

The article highlights that major European Original Equipment Manufacturers (OEMs) like Vestas and Siemens Gamesa faced severe profitability challenges between 2021 and 2024. This was caused by a combination of rising material costs and intense price pressure in project auctions.

How is investment in European wind power split?

Investment is split into two streams. On one hand, private developers like RWE are committing massive capital (€35 billion from 2025-2030) into new wind project deployment. On the other hand, public institutions like the EIB are deploying funds (€5 billion) specifically to support the fragile manufacturing base that supplies these projects.

What is the biggest long-term risk for Europe in this situation?

The biggest long-term risk is trading one form of energy dependency for another. By relying heavily on Chinese turbines to meet renewable energy goals, Europe risks undermining its own industrial base and shifting its dependency from Russian gas to Chinese-made energy hardware, which introduces new risks related to geopolitics, cybersecurity, and data governance.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.