US-Iran War 2026: How Asia’s Energy Security Overhaul Exposes Critical Supply Chain Risks

Strait of Hormuz Disruption: A Systemic Risk to Asian Economies

The early 2026 military conflict involving the United States, Israel, and Iran has definitively severed Asia’s primary energy lifeline, forcing a radical and non-negotiable overhaul of the continent’s energy security strategy. The closure of the Strait of Hormuz, a chokepoint for nearly a third of global seaborne oil, has moved the long-discussed theoretical risk of Middle East dependency into a catastrophic reality, triggering immediate supply-chain collapse and extreme price shocks for Asia’s largest economies.

- Prior to 2025, Asian economies operated with a high-risk tolerance for their dependence on the Strait of Hormuz, through which approximately 80% of its energy flows were directed. The conflict has weaponized this dependency, cutting off a critical supply source with no viable short-term alternative.

- China faces an acute crisis, having previously sourced over 52% of its seaborne crude from the Middle East, with Iran being a cornerstone supplier. The disruption nullifies Beijing’s strategy of using sanctioned Iranian crude as an economic and geopolitical buffer.

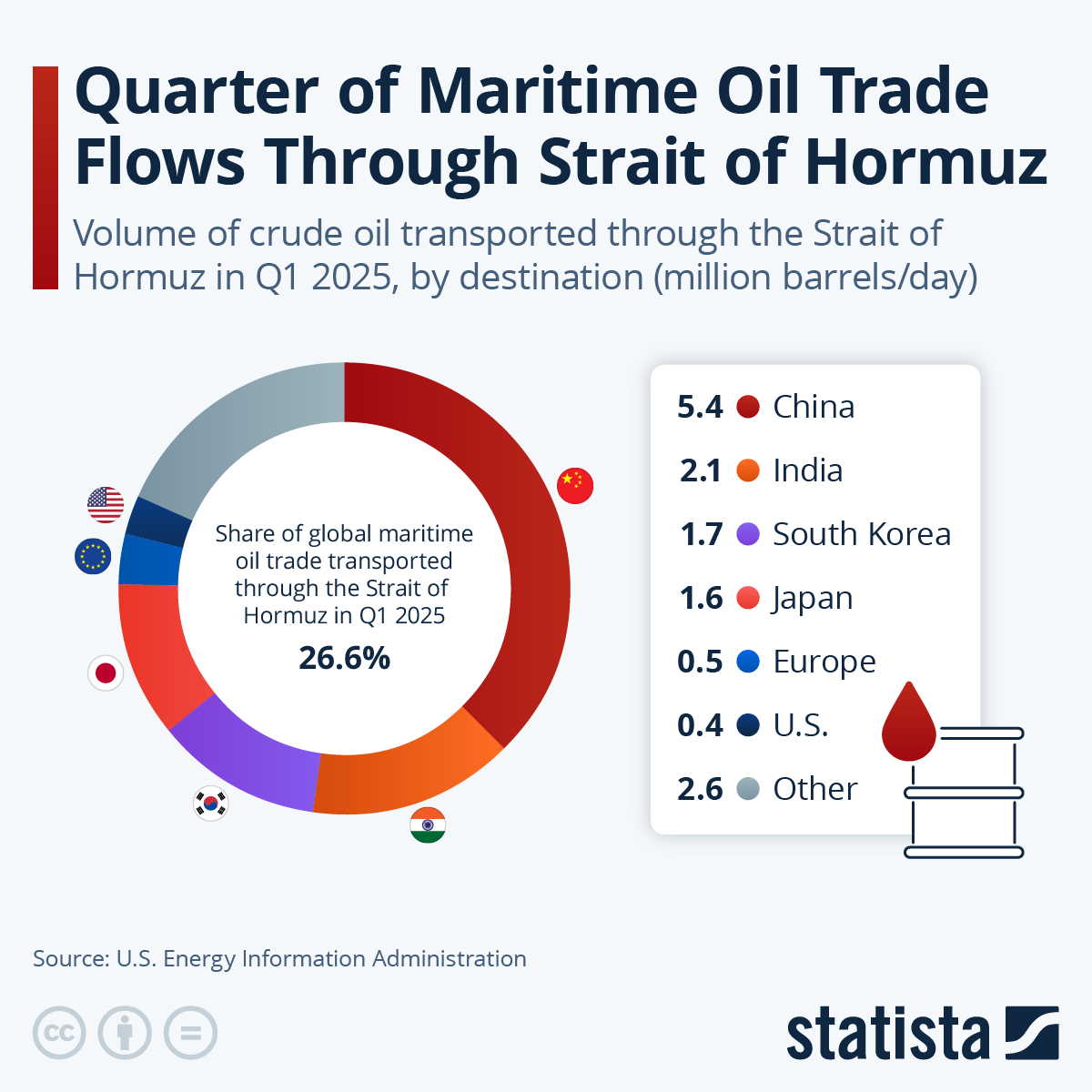

- The impact is continent-wide, with nations like Japan (90% dependence on Middle East crude), India (60%), and South Korea (70%) facing an immediate inability to source contracted volumes. This has triggered a desperate scramble for alternative supplies and a surge in freight and insurance costs for any vessel operating near the conflict zone.

- Physical infrastructure is already compromised. Saudi Aramco was forced to halt Liquefied Petroleum Gas (LPG) exports from its Juaymah facility following damage, a direct blow to its key Asian buyers and a signal of the widening collateral risk to regional energy assets.

Asian Nations are Primary Importers from Hormuz

This chart quantifies the significant volume of crude oil destined for Asian economies via the Strait of Hormuz, directly illustrating the ‘systemic risk’ and dependency described in the section.

(Source: Statista)

Financial Shocks and Sanctions Paralyze Energy Trade

The conflict has unleashed severe price volatility across global markets, with Asian economies, as net importers, absorbing the full impact. This is compounded by a new, aggressive sanctions regime that is financially isolating Iran’s petroleum sector and increasing compliance risks for any refiner or trader dealing with the region.

US-Iran Conflict Triggers Major Oil Price Spike

This chart’s line graph shows the Brent crude price jumping in January 2026, perfectly visualizing the ‘financial shocks’ and immediate ‘price jump’ detailed in the text.

(Source: Geopolitical Futures)

- In the conflict’s immediate aftermath, Brent crude prices jumped by $10/bbl to nearly $80/bbl. Analyst projections indicate a sustained disruption could push prices well over $100 per barrel, a level that threatens to induce recession in energy-intensive Asian economies.

- The price shock extends to natural gas, where European prices nearly doubled, creating intense competition for available spot LNG cargoes and driving up prices for Asian buyers. This disruption to LNG supply chains is shattering the perception of gas as a reliable transition fuel.

- The United States imposed a new wave of sanctions on February 6, 2026, designating 15 entities involved in Iranian petroleum shipping. This action significantly increases the legal and financial risk for Asian refiners, who must now navigate a complex and hazardous compliance environment or abandon regional trade entirely.

Table: Corporate and Sanctions Impact on Asian Energy Trade (2026)

| Date | Entity / Market Segment | Details and Strategic Purpose | Source |

|---|---|---|---|

| Feb 8, 2026 | Petroleum Shipping | The U.S. announced sanctions on 15 entities within Iranian petroleum shipping networks, aimed at crippling Iran’s ability to export crude and increasing compliance risk for Asian buyers. | Times CA |

| Feb 3, 2026 | Crude Oil & LNG | Conflict disrupted oil and LNG flows as vessels became trapped inside the Middle East Gulf, creating a physical bottleneck that halted deliveries to Asian importers. | Hydrocarbon Processing |

| Recent | Saudi Aramco (LPG Exports) | The company halted LPG exports from its Juaymah facility after sustaining structural damage, directly removing a key supply source for its Asian customers. | Times of India |

Geopolitical Realignment: Asia’s Scramble for New Suppliers

The crisis is forcing an immediate and sharp geopolitical realignment as Asian nations confront the reality that their economic stability is tied to a single, volatile maritime chokepoint. This has triggered high-level diplomatic efforts to secure new energy routes and suppliers, fundamentally redrawing the global energy map.

Flowchart Shows How Conflict Disrupts Oil Supply

This flowchart visualizes the chain reaction from conflict to sanctions to disrupted exports, providing a clear illustration of the systemic impacts detailed in the section’s table.

(Source: LinkedIn)

- China, as the primary buyer of Iranian oil, is in a strategic bind, balancing its immediate energy needs with the risk of being drawn into the conflict. Beijing has publicly stated it will take “necessary measures” to protect its energy security, signaling a potential accelerated pivot toward Russian and other non-Gulf suppliers.

- India’s government has warned of “serious economic risks” from the disruption. Prime Minister Modi has launched a significant diplomatic outreach to other Gulf nations to secure trade routes and guarantee supplies, highlighting the nation’s profound vulnerability.

- Between 2021-2024, Asian importers diversified their portfolios but maintained a core reliance on long-term contracts with Middle East producers like Saudi Arabia, the UAE, and Qatar. The 2026 conflict has demonstrated that diversification on paper is meaningless without resilient and geographically diverse logistics.

Technology Maturity: Renewables Reframed as a National Security Imperative

The 2026 war has permanently reframed the energy transition in Asia from a climate-related goal to an urgent national security necessity. The extreme volatility of fossil fuel markets has made the operational and economic benefits of renewable energy technologies undeniable, forcing an acceleration of their deployment to insulate economies from geopolitical shocks.

- Between 2021-2024, the deployment of renewables in Asia was driven primarily by falling costs and climate policy. Post-conflict, the key driver is energy independence and risk mitigation. The shock to the global energy transition is not a slowdown but a redirection of capital toward technologies that offer domestic control.

- Technologies like battery storage and green hydrogen, once viewed as future solutions, are now seen as critical strategic buffers. Their ability to provide grid stability and store energy during periods of supply constraint offers a direct countermeasure to the price volatility inherent in global oil and gas markets.

- China, having already invested billions in its renewable and electric vehicle supply chains before 2025, is best positioned to leverage this crisis. While these assets cannot solve the immediate supply crunch, the conflict validates this long-term strategy and will trigger a doubling-down of investment to accelerate its build-out.

SWOT Analysis: Asia’s Energy Security Risk Profile

The conflict has exposed the structural weaknesses in Asia’s energy strategy while simultaneously creating a powerful, if painful, incentive for fundamental change. The strategic calculus has shifted from optimizing cost to ensuring survival, with a clear re-evaluation of strengths, weaknesses, opportunities, and threats.

Table: SWOT Analysis of Asia’s Energy Security

| SWOT Category | 2021 – 2024 (Pre-Conflict) | 2025 – 2026 (Post-Conflict) | What Changed / Validated |

|---|---|---|---|

| Strengths | Established long-term supply contracts with Middle East producers; large-scale refining infrastructure. | Strong domestic manufacturing base for renewables (especially in China); existing, albeit insufficient, strategic petroleum reserves. | The value of physical assets (contracts, refineries) was negated by logistical failure. The strength shifted to domestic, controllable assets like manufacturing capacity. |

| Weaknesses | Extreme dependence on the Strait of Hormuz for crude and LNG; status as a price-taker in global energy markets. | The weakness was validated and transformed into a full-blown crisis; inability to influence geopolitical events in the Middle East. | The theoretical weakness of over-reliance on a single chokepoint was validated as a catastrophic, systemic failure point for the entire Asian economy. |

| Opportunities | Gradual diversification of energy mix toward renewables; exploring new suppliers in Africa and the Americas. | Forced, rapid acceleration of clean energy transition; aggressive pursuit of non-Gulf suppliers (Russia, Africa); massive state investment in renewables as a national security issue. | The opportunity for a transition shifted from a gradual, market-led process to a state-directed, urgent strategic imperative. |

| Threats | Geopolitical instability in the Middle East; oil price volatility; potential for supply disruptions. | Realized closure of the Strait of Hormuz; unprecedented price shocks; cascading economic recession; regional conflict escalation. | All previously identified threats were realized simultaneously, creating a multi-dimensional crisis far exceeding previous worst-case scenarios. |

Scenario Modelling: A Permanent Fragmentation of Global Energy Markets

The US-Iran conflict is a watershed event that will permanently alter global energy trade flows. The immediate crisis response will solidify into long-term strategic shifts as Asian nations refuse to remain exposed to such profound vulnerability. If the disruption in the Strait of Hormuz persists, watch for decisive actions that signal a structural break from the old energy order.

- If the Strait of Hormuz remains partially or fully closed for more than 90 days, watch for China and India to sign large-scale, long-term supply agreements with Russia, West African nations, and Latin American producers. This would signal a permanent diversification away from the Middle East, fundamentally weakening the influence of OPEC+ on its largest customer base.

- A key signal to monitor is government-led investment in strategic infrastructure. Expect announcements of massive, state-backed funding for LNG import terminals on coastlines that do not face the Persian Gulf, cross-country pipelines, and a dramatic acceleration of national targets for solar, wind, and battery storage deployment, framed as national security projects.

- The most significant outcome could be the creation of bifurcated energy markets. One market will be centered on Atlantic basin and Russian supplies priced and traded independently of a second, more volatile market centered on the Persian Gulf. Asian consumers will lead the development of the former to ensure their long-term security.

Frequently Asked Questions

What is the primary impact of the 2026 US-Iran conflict on Asia’s energy security?

The primary impact is the closure of the Strait of Hormuz, which has severed Asia’s main energy lifeline. This has cut off approximately 80% of the continent’s energy flows from the Middle East, leading to an immediate supply-chain collapse, extreme price shocks, and forcing a desperate search for alternative suppliers.

How are specific Asian countries like China, India, and Japan affected?

These nations are severely impacted due to their high dependency on Middle East crude: Japan (90%), South Korea (70%), and India (60%). China faces an acute crisis as over 52% of its seaborne crude, including sanctioned oil from Iran, came through the region. This has nullified its geopolitical strategy and triggered a continent-wide inability to source contracted energy volumes.

What are the immediate financial consequences of the conflict for Asian economies?

The conflict has caused severe financial shocks. Brent crude prices jumped by $10/bbl to nearly $80/bbl, with projections exceeding $100/bbl, threatening recession. Natural gas prices also doubled in Europe, creating intense competition for LNG cargoes and driving up costs for Asian buyers. Furthermore, new US sanctions on Iranian petroleum shipping have increased compliance risks and costs, paralyzing energy trade.

How has the war changed the role of renewable energy in Asia?

The war has permanently reframed the energy transition in Asia from a climate-related goal to an urgent national security imperative. The extreme price volatility of fossil fuels has made the domestic control and stability offered by renewables, battery storage, and green hydrogen strategically essential. The focus has shifted from cost-reduction to energy independence and risk mitigation.

What long-term changes are expected in global energy markets if the disruption continues?

If the Strait of Hormuz remains closed for an extended period (e.g., over 90 days), the article predicts a permanent fragmentation of global energy markets. Asian nations are expected to make a structural pivot away from the Middle East, signing large-scale deals with Russia, West African nations, and Latin American producers. This would be accompanied by massive state-led investment in new strategic infrastructure like pipelines and non-Gulf LNG terminals, creating a bifurcated market with separate pricing systems for different geopolitical blocs.