Green Hydrogen in India’s Energy Security, 85% Oil Import Risk, 400 K BPD LPG Shortage, and E 20 Policy (2021 to 2026)

India’s Energy Security Risks, 85% Import Dependency and 2.9% CAD Projection

India’s chronic energy import dependency, a long-term risk managed through the price volatility of 2021-2024, transformed into an acute economic crisis by mid-2026 due to physical supply disruptions. The escalation of conflict in the Middle East and subsequent interference with maritime traffic through the Strait of Hormuz exposed the fragility of India’s energy supply chain, shifting the primary challenge from cost management to securing physical barrels and managing severe shortages.

- In the 2021-2024 period, the primary pressure was price-related, driven by post-pandemic demand and the war in Ukraine. The current account deficit (CAD) widened to 2.8% of GDP in Q 1 2022-23 due to high commodity costs, but supply was not physically constrained.

- By 2026, the problem escalated to a physical supply threat. Projections indicate the CAD could widen to approximately 2.9% of GDP in FY 27, now driven by both high prices and a severe Liquefied Petroleum Gas (LPG) shortage estimated at 400, 000 barrels per day.

- India’s fundamental vulnerability stems from importing over 85% of its crude oil and 50% of its natural gas. This exposure was directly triggered by the early 2026 disruptions in the Strait of Hormuz, a chokepoint for a significant portion of its energy imports.

- The government’s response shifted from proactive energy transition policies to reactive crisis management. By June 2026, it had implemented fuel curbs and conservation measures, a stark contrast to the earlier focus on managing market-based price pass-throughs.

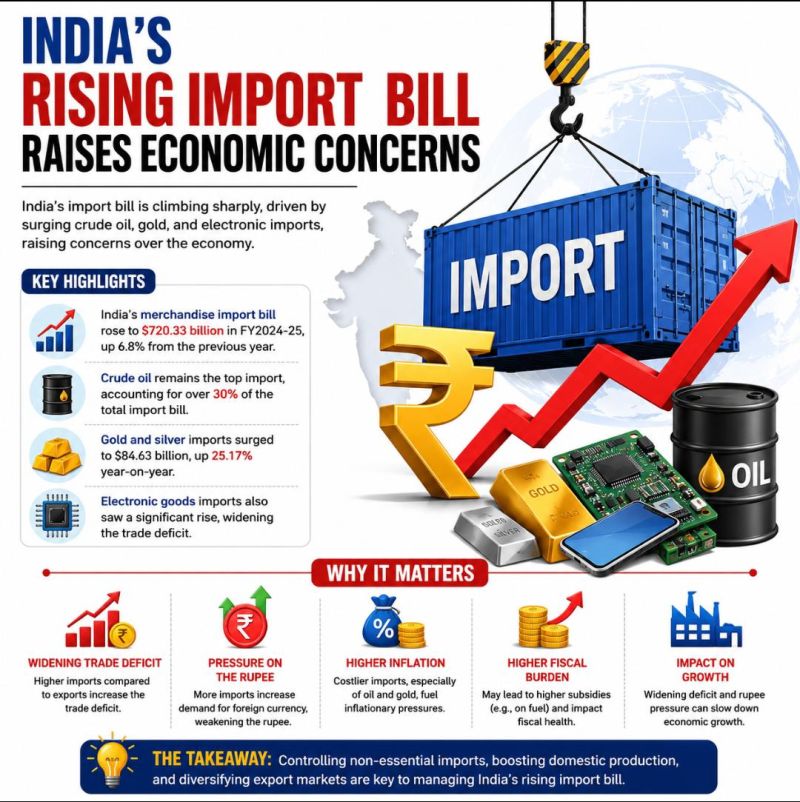

India’s Import Bill Rises to $720B, Driven by Oil

This chart directly quantifies the “Import Dependency” risk mentioned in the section heading. The rising import bill, explicitly “Driven by Oil,” is the primary cause of energy security concerns and contributes directly to the Current Account Deficit (CAD).

(Source: LinkedIn)

$2.4 B Green Hydrogen Mission, India’s Long-Term vs. Crisis Spending

India’s fiscal approach to the energy sector pivoted sharply from strategic long-term investments between 2021-2024 to immediate, fiscally-straining crisis expenditures in 2025-2026. While ambitious programs to build future energy independence were initiated in the earlier period, the recent crisis forced a return to costly, short-term subsidy measures to protect consumers and manage social stability.

- Between 2021 and 2024, the government’s focus was on long-term capital allocation for energy transition. This was headlined by the launch of the National Green Hydrogen Mission with an initial outlay of INR 19, 744 crore (approx. $2.4 billion) to build 5 MMT of annual production capacity by 2030.

- The 2026 crisis forced a reallocation of fiscal priorities toward immediate relief. The Union Budget for 2026-27 allocated ₹9, 200 crore (approx. $1.1 billion) for LPG subsidies and an additional ₹1, 500 crore (approx. $180 million) for direct benefit transfers to cushion the blow of the LPG shortage.

- This reactive spending puts significant pressure on India’s fiscal deficit, particularly as subsidy bills for other imported commodities like fertilizers also surged. For example, urea import prices hit $950/MT in April 2026, up from $390/MT a year prior, compounding the financial strain.

Fossil Fuels Remain 75% of India’s Power Mix

This chart establishes the underlying reason for the policies discussed in the section. The high percentage of fossil fuels in the power mix demonstrates the vulnerability to price shocks and highlights the strategic importance of long-term investments like the Green Hydrogen Mission to diversify the energy basket.

(Source: Observer Research Foundation)

Table: India’s Energy Policy Spending (Strategic vs. Crisis)

| Policy / Expenditure | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| LPG & DBTR Subsidies | 2026-2027 | Total allocation of ₹10, 700 crore (~$1.3 billion) for consumer subsidies and direct transfers to mitigate acute LPG price shocks and shortages during the 2026 crisis. | PRS India |

| National Green Hydrogen Mission | Announced 2023 | Initial outlay of INR 19, 744 crore (~$2.4 billion) to establish India as a global production hub, targeting 5 MMT of annual capacity by 2030 to reduce long-term fossil fuel imports. | MNRE |

| PLI for Batteries & Auto | Announced 2021 | A multi-year incentive scheme to build domestic manufacturing capacity for Advanced Chemistry Cell batteries and electric vehicles, shifting focus from demand subsidies to supply-side ecosystem building. | Columbia SIPA |

Geopolitical Exposure, India’s Reliance on the Strait of Hormuz

The 2026 crisis crystallized the geopolitical risk inherent in India’s energy supply chain, shifting the problem from a theoretical vulnerability to a tangible economic threat. While reliance on the Middle East was a known factor during the 2021-2024 period, the disruption in the Strait of Hormuz provided a stark demonstration of India’s exposure to regional instability far from its borders.

- The Strait of Hormuz is the central node of failure. The crisis was directly triggered by its disruption, impacting a critical transit route for much of India’s crude oil, LNG, and LPG feedstock, exposing a severe concentration of supply risk.

- Prior to the acute crisis, India’s supply portfolio was already concentrated, with the Middle East and Russia serving as major sources. The 2026 disruption made clear that this concentration is untenable in a volatile global oil market.

- The impact was specific and immediate. Asian jet fuel use, especially in India, was directly impacted by flight disruptions to and from the Gulf region, illustrating how geopolitical events translate into direct economic consequences.

- In response, a key strategic pivot announced during the crisis is the diversification of energy supply sources. This moves diversification from a long-term policy goal to an urgent, short-term national security imperative to reduce over-reliance on any single region or chokepoint.

India’s Energy Transition Acceleration, E 20 Biofuel Target and EV Policy

The 2025-2026 energy crisis is a powerful, if painful, accelerant for energy transition technologies, recasting them as tools of national security rather than just environmental policy. Policies initiated between 2021 and 2024, such as advancing biofuel blending and promoting EVs, now carry far greater strategic weight as immediate solutions to reduce foreign oil dependency.

- During the 2021-2024 period, the government’s approach was proactive but measured. It amended the National Policy on Biofuels in May 2022 to advance the 20% ethanol blending (E 20) target to 2025-26 from 2030, a move that now appears prescient.

- The 2026 crisis adds immense urgency to this policy. With fuel curbs in place, domestically produced ethanol is no longer just a method to lower emissions but a critical resource for extending fuel supplies and reducing the immediate need for gasoline imports.

- Similarly, the push for electric mobility through the FAME II scheme and PLI for batteries, a key policy direction in the earlier period, gains new importance. Every EV deployed is a direct reduction in future oil demand and import dependency.

- The crisis creates a stronger business case for long-term projects like the National Green Hydrogen Mission. While not a short-term solution, the current import crisis validates the strategic necessity of developing domestic, non-fossil energy sources to prevent future crises.

SWOT Analysis, India’s Economic Strengths vs. Energy Vulnerabilities

The strategic landscape for India’s economy shifted significantly, with strengths like high GDP growth becoming tools for crisis mitigation rather than expansion. The 2026 crisis exposed deep-seated weaknesses that were previously manageable risks, while simultaneously heightening the importance of opportunities in the energy transition.

India’s Fiscal Deficit Shows Steady Improvement

This chart represents an economic “Strength” within a SWOT analysis framework. It provides a crucial balancing element to the discussion, showing the fiscal capacity and macroeconomic stability that India can leverage to address its energy vulnerabilities.

(Source: Financial Post)

Table: SWOT Analysis for India’s Energy & Economic Security

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | High GDP growth provided a buffer against rising commodity prices. A large domestic market supported industrial demand. | Resilient GDP growth (7.7% in FY 26) provided fiscal space for subsidies, but this is now under severe threat from slowing growth forecasts (6.4%–6.6%). | The strength of high growth was validated as a critical tool for absorbing shocks, but its sustainability in the face of an energy crisis was shown to be limited. |

| Weaknesses | High import dependency (85% oil) was a known vulnerability, primarily manifesting as price risk and a widening CAD (2.8% in Q 1 FY 23). | The weakness escalated from a price risk to a physical supply risk with the Hormuz disruption, leading to acute LPG shortages (400, 000 bpd) and fuel curbs. | The fundamental weakness of import dependency was validated as the single greatest threat to India’s macroeconomic stability. |

| Opportunities | Energy transition policies (biofuels, EVs, green hydrogen) were pursued as long-term strategic goals for decarbonization and eventual energy independence. | The crisis provides a powerful catalyst to accelerate these transitions as a matter of urgent national security, creating a stronger mandate for investment in renewables and domestic manufacturing. | The opportunity for energy transition was validated as the primary strategic pathway to mitigate the core weakness of import dependency. |

| Threats | Geopolitical shocks (e.g., Ukraine war) were the primary external threat, manifesting as commodity price inflation and a higher import bill. | The threat evolved to include physical chokepoint disruption (Strait of Hormuz), currency depreciation (Rupee forecast at 95/USD), and a global economic slowdown. | The threat of geopolitical events impacting energy was validated, with the severity and nature of the threat escalating from price shocks to supply chain collapse. |

Scenario Modeling for India, Renewable Investment and Supply Diversification

The critical question for India is whether it can leverage the current crisis to enforce a permanent, structural pivot towards energy self-reliance. The path forward will be determined by its ability to translate reactive crisis management into sustained investment in domestic energy infrastructure and diversified supply chains, even after the immediate pressures subside.

- If the crisis deepens, watch for more aggressive government intervention, including potential rationing of fuels for industrial and commercial users and a significant drawdown of strategic petroleum reserves. This would also likely trigger emergency diplomatic outreach to secure supply from non-traditional partners.

- A key signal to watch is the pace of investment in domestic energy infrastructure, particularly in renewable energy generation, grid and power infrastructure, and energy storage. Companies like Adani Green Energy and Re New Power are positioned to lead this buildout, and an acceleration of their project pipelines would be a strong positive indicator.

- These developments could be happening: a renewed push for domestic manufacturing under the PLI scheme, with a focus on the entire energy supply chain from solar panels to electrolyzers. This would signal a commitment to capturing the industrial benefits of the energy transition and reducing reliance on imported energy technology. The recent experience with renewable energy investment cycles globally highlights the need for stable policy to secure such long-term commitments.

News Headlines Corroborate India’s 2026 Economic Crisis

This chart serves as a powerful visual output for a “Scenario Modeling” exercise. The collection of crisis-related news headlines effectively communicates the potential negative outcomes of failing to address energy risks, making the case for proactive investment and diversification.

(Source: LinkedIn)

The questions your competitors are already asking

This report covers one angle of India’s energy security crisis, focusing on the shift from price volatility to physical supply disruption. The questions that matter most depend on your work.

- What is actually happening with India’s National Green Hydrogen Mission and E20 ethanol blending policy in the face of the 2026 fuel supply crisis?

- What is the outlook for Green Hydrogen deployment in India’s energy mix by 2030, considering the new priority of immediate supply security over long-term transition?

- What are the opportunities for domestic energy technologies, from Green Hydrogen to biofuels, created by the government’s crisis-driven fuel curbs and conservation measures?

- How does Green Hydrogen compare to accelerated ethanol blending (E20) for reducing India’s immediate crude oil import dependency?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.