Exxon Mobil M&A Strategy, $59.5 B Pioneer Deal, $53 B Hess Rivalry, and Woodside Target (2023 to 2026)

Upstream M&A Projects, Exxon Mobil Consolidation Accelerates Post-2023

The oil and gas industry has entered a phase of aggressive consolidation, where large-scale M&A has replaced organic exploration as the primary strategy for growth, reserve replacement, and securing market control.

- Between 2021 and 2023, M&A activity began to build, but it escalated dramatically in late 2023 with a series of megamergers valued at over $230 billion in North America alone, signaling a fundamental shift toward industry concentration.

- Exxon Mobil’s $59.5 billion acquisition of Pioneer Natural Resources, announced in October 2023, was a defining moment, creating the dominant producer in the Permian Basin and setting a precedent for acquiring premier, low-cost domestic assets at scale.

- This trend continued into 2024 and 2025 with other major deals, including Chevron’s $53 billion bid for Hess Corporation and Diamondback Energy’s $26 billion purchase of Endeavor, reinforcing that scale is now a prerequisite for competition.

- Looking forward, Exxon Mobil’s reported evaluation of international targets like Australia’s Woodside Energy Group in early 2024 indicates the consolidation strategy is expanding beyond U.S. shale to secure global LNG and deepwater assets.

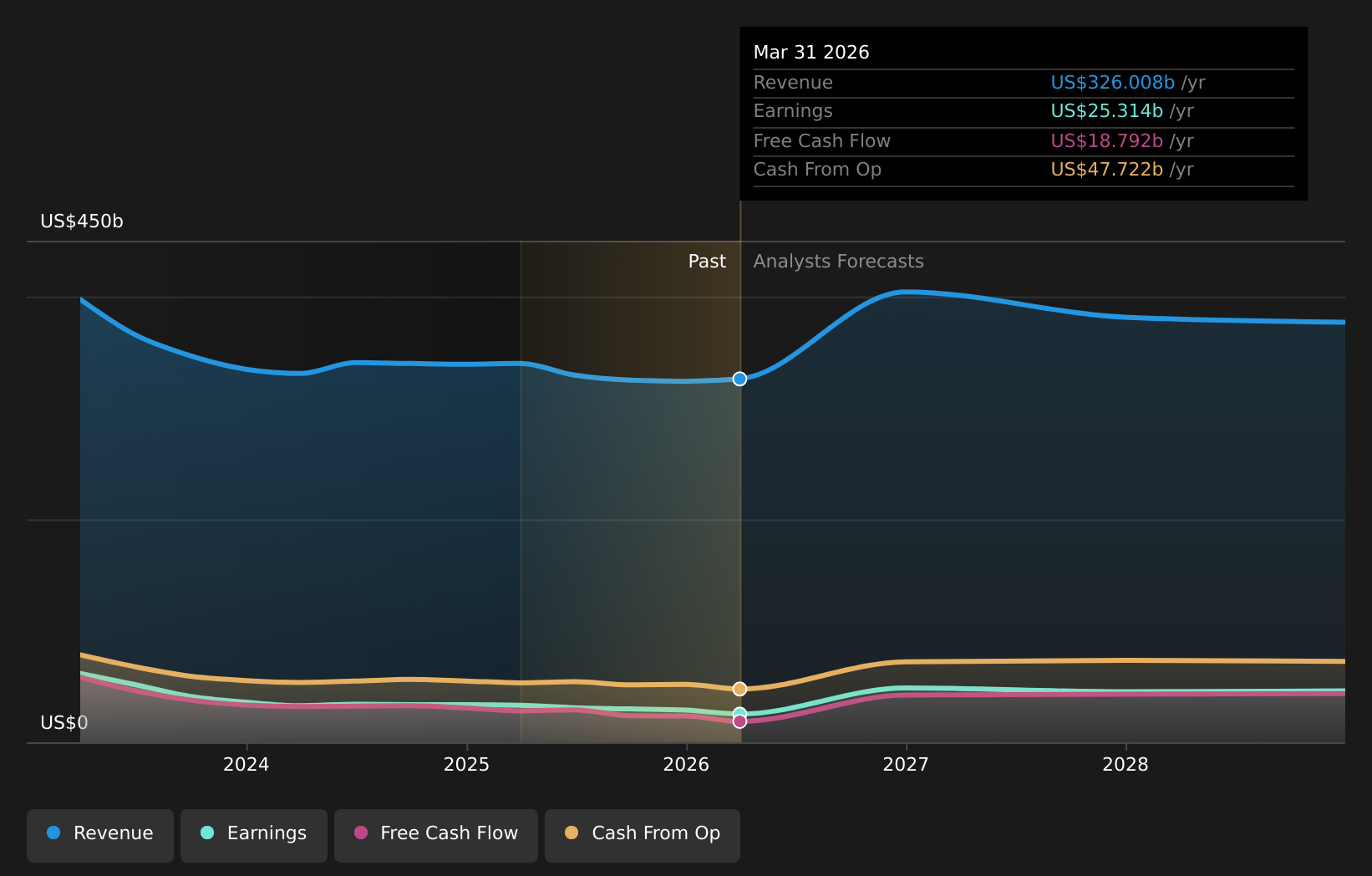

Exxon Mobil Financials Forecast Future Growth

The section discusses Exxon Mobil’s accelerating consolidation strategy post-2023. The chart showing the company’s financial forecast and future growth provides the underlying rationale, as strong financials and growth prospects enable and fund large-scale M&A activities.

(Source: Yahoo Finance)

$234 B in 2023 Deals, Exxon Mobil Leads Sector-Wide Investment in Consolidation

The energy sector is deploying immense capital not into speculative new ventures, but into acquiring proven, cash-generating assets from competitors, a move that prioritizes shareholder returns and operational efficiency over high-risk exploration.

- The total value of upstream M&A deals surged to $234 billion in 2023, the highest level in over a decade, driven almost entirely by megadeals among the largest U.S. producers.

- Exxon Mobil’s nearly $65 billion commitment in 2023, through its acquisitions of Pioneer Natural Resources ($59.5 billion) and Denbury Inc. ($4.9 billion), demonstrates a clear dual strategy of fortifying its core oil business while making targeted investments in low-carbon infrastructure.

- Unlike peers pursuing strategies in renewable generation, such as Total Energies’ wind asset acquisitions, the dominant capital flow from US supermajors has been directed at consolidating existing oil and gas production.

- This investment pattern highlights a belief that acquiring existing, efficient production is a more capital-effective and less risky path to meeting future energy demand and delivering shareholder value than developing new technologies or exploring greenfield sites.

Table: Recent Major M&A Transactions in the Oil & Gas Sector

| Acquirer / Target | Announcement Date | Details and Strategic Purpose | Source |

|---|---|---|---|

| Conoco Phillips / Marathon Oil | May 2024 | $22.5 billion all-stock transaction to acquire complementary U.S. onshore assets, particularly in the Eagle Ford and Bakken shales. | Offshore Technology |

| Diamondback Energy / Endeavor Energy Resources | Feb 2024 | $26 billion transaction creating a dominant, pure-play operator focused on the Permian Basin. | Diamondback Energy |

| Chevron / Hess Corporation | Oct 2023 | $53 billion deal to acquire a 30% stake in Guyana’s prolific Stabroek Block, a major deepwater oil discovery. The deal is currently delayed by arbitration. | Chevron |

| Exxon Mobil / Pioneer Natural Resources | Oct 2023 | $59.5 billion acquisition that more than doubled Exxon’s footprint in the Permian Basin, making it the largest producer in the field. | Exxon Mobil |

| Occidental Petroleum / Crown Rock | Dec 2023 | $12 billion transaction to add high-margin production and scale in the Midland Basin, part of the Permian. | Occidental Petroleum |

Woodside Energy Outlines Capital Allocation Strategy

While the section is titled as a table of major transactions, this chart provides a relevant case study. Woodside recently completed a major merger, and its subsequent capital allocation strategy is a direct result and key component of the M&A landscape.

(Source: Seeking Alpha)

US vs. Global, Exxon Mobil Expands M&A Focus Beyond Permian Basin

The geographic focus of oil and gas M&A is undergoing a strategic expansion, moving from a land-centric consolidation in the U.S. Permian Basin to a global pursuit of long-life assets in key regions like Australia and South America.

- Between 2022 and 2024, the primary geographical battleground was the Permian Basin in Texas and New Mexico, where Exxon Mobil (Pioneer), Diamondback (Endeavor), and Occidental (Crown Rock) all executed deals to build insurmountable scale in the top U.S. shale field.

- Starting in 2024 and looking toward 2026, the strategy is shifting to international assets. Chevron’s pursuit of Hess is primarily a play for its stake in Guyana’s Stabroek Block, one of the world’s most significant deepwater discoveries.

- Exxon Mobil’s reported interest in Australia’s Woodside Energy signals a pivot toward securing global LNG supply chains. An acquisition would add significant assets in Australia and the Gulf of Mexico, positioned to serve high-demand Asian and European markets.

- This geographic diversification reflects a two-part strategy: first, dominate low-cost, short-cycle U.S. shale, and second, acquire long-life, large-scale international assets that provide durable cash flow and leverage to global commodity prices. This contrasts with other firms focusing on domestic infrastructure needs, such as new power sources for AI and data center energy.

Mature Asset Acquisition, Exxon Mobil Prioritizes Proven Production Over R&D

The current M&A wave is characterized by a flight to safety, with acquirers targeting mature, commercially proven technologies and cash-flowing assets rather than investing in speculative, next-generation energy technologies.

- The deals from 2023 to 2024, including the Pioneer and Endeavor acquisitions, focused on acquiring extensive inventory of shale assets that rely on well-understood and highly optimized unconventional drilling and completion technologies. The goal is manufacturing-style efficiency, not technological discovery.

- Exxon Mobil’s $4.9 billion acquisition of Denbury in 2023 followed this pattern by acquiring the largest existing CO 2 pipeline network in the U.S., a mature infrastructure asset, rather than developing a new network from scratch.

- A potential acquisition of Woodside Energy in 2025 or beyond would continue this trend, targeting established LNG liquefaction plants and deepwater production facilities, which represent decades-old, capital-intensive technologies that are fully de-risked and operational.

- This strategy of acquiring mature, high-quality assets stands in contrast to venture-style investments in emerging energy sectors. While supermajors maintain R&D budgets, the largest capital allocations are decisively focused on integrating proven, large-scale hydrocarbon production.

SWOT Analysis, Exxon Mobil Balances Scale Advantages with ESG Risks

The aggressive M&A strategy offers supermajors like Exxon Mobil significant competitive advantages in scale and cost, but it also amplifies exposure to regulatory, environmental, and execution risks that could undermine long-term value.

- The primary strength is the ability to leverage immense balance sheets and highly-valued stock to acquire competitors and immediately add cash-flow positive production.

- The key opportunity lies in capturing cost and operational synergies, dominating key production basins, and expanding into the growing global LNG market.

- However, a significant weakness is the increased scrutiny from ESG investors and the challenge of meeting decarbonization targets while substantially growing the company’s fossil fuel production base.

- The most immediate threat comes from antitrust regulators, who have shown increased willingness to challenge large deals, and from geopolitical risks associated with expanding into new international territories.

O&G Companies Target Renewables in M&A

The section discusses the balance between scale advantages and ESG risks in a SWOT analysis. The chart illustrates a key strategic action—M&A in renewables—that companies are using to address the ‘Threats’ and ‘Opportunities’ related to ESG.

(Source: S&P Global)

Table: SWOT Analysis for Oil & Gas Consolidation Strategy

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong balance sheets post-COVID; operational expertise in core basins. | Use of highly-valued equity as acquisition currency (e.g., Exxon’s all-stock Pioneer deal); ability to achieve massive G&A and operational cost synergies. | The market validated that scale and low-cost operations are the primary drivers of valuation, making supermajors’ stock an effective tool for consolidation. |

| Weaknesses | Pressure from ESG investors to diversify away from fossil fuels; aging asset portfolios. | Increased absolute Scope 1, 2, and 3 emissions from acquisitions; integration risk of merging large, complex organizations with different cultures. | Megamergers confirmed that core business growth takes precedence over emissions reduction targets, increasing the gap between climate rhetoric and capital allocation. |

| Opportunities | Consolidate fragmented U.S. shale assets; grow shareholder returns through buybacks and dividends. | Dominate key basins (Permian); expand into high-growth LNG market (e.g., Woodside target); leverage integrated trading arms to optimize global commodity flows. | The bull case for LNG as a transition fuel was validated, making LNG-heavy companies prime acquisition targets for long-term cash flow. |

| Threats | Commodity price volatility; long-term demand uncertainty due to energy transition policies. | Intensified antitrust scrutiny from regulators (FTC review of Exxon/Pioneer); inter-company disputes (Exxon’s arbitration claim on Chevron/Hess Guyana asset); stranded asset risk. | Regulatory and legal risks have become concrete barriers to deal completion, moving from theoretical concerns to active impediments. |

Exxon Mobil Leads in Announced Hydrogen Capacity

The section refers to a SWOT analysis for consolidation. The chart highlights a key ‘Strength’ and ‘Opportunity’ for Exxon Mobil. Leadership in a transition fuel like hydrogen is a strategic advantage that strengthens the rationale for its consolidation strategy.

(Source: Enverus)

Exxon Mobil M&A Scenarios, Watch for Regulatory Rulings and LNG Targets

The future of the energy consolidation wave hinges on two critical variables: the stance of global antitrust regulators and the strategic decisions of supermajors like Exxon Mobil on whether to pursue global LNG assets next.

- If this happens: Regulators in the U.S., Australia, and Europe approve the current slate of megadeals without demanding significant divestitures. Watch this: A new wave of M&A among mid-tier producers ($5-$20 billion market cap) who will be forced to consolidate to compete on scale and cost with the newly enlarged supermajors.

- If this happens: Exxon Mobil proceeds with a formal, public offer for Woodside Energy or a similar-sized LNG player before the end of 2025. Watch this: A re-rating of all independent LNG producers, as the market prices in an acquisition premium and validates LNG as the premier long-term growth asset for integrated energy companies.

- These could be happening: Heightened ESG and shareholder pressure force Exxon Mobil and Chevron to accelerate and expand investments in their low-carbon solutions businesses to offset the emissions impact of their acquisitions. This could lead to more deals similar to the Denbury acquisition or larger partnerships for clean energy, similar to the Microsoft nuclear PPA with Constellation, but at a scale that remains secondary to the core hydrocarbon business.

Chart Maps Potential Oil & Gas Merger Landscape

This is a direct match. The section discusses future M&A scenarios, and the chart visually represents this by mapping out the potential merger and acquisition landscape, illustrating possible future deals and consolidation pathways.

(Source: Oil Price)

The questions your competitors are already asking

This report covers one angle of the M&A-driven consolidation reshaping the global oil and gas industry. The questions that matter most depend on your work.

- Which supermajors are gaining or losing ground in the race to consolidate U.S. shale and global LNG assets?

- What is the status of Exxon’s $59.5B Pioneer integration and the rival Chevron-Hess deal?

- What are the next acquisition targets for Exxon Mobil beyond U.S. shale, including Woodside Energy?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.