Global Oil Market Demand Destruction, IEA Forecasts 1.1 M b/d Decline, 2 Major Downward Revisions, and a 2.45 M b/d Q 2 Drop (2025 to 2026)

Oil Market Risks, IEA and EIA Signal 1.1 M b/d Demand Decline in 2026

The initial price shock following the Strait of Hormuz disruption has triggered severe global demand destruction, which has now become the primary mechanism capping further crude oil price increases. While the supply-side shock was historically large, removing an estimated 8 million barrels per day (bpd) in March 2026, the market’s reaction has been dominated by a rapid and deep contraction in consumption. This price-induced demand response is the core reason that prices, while elevated, have not sustained a trajectory toward catastrophic levels above $150 per barrel.

- Prior to the crisis in late 2025, the consensus forecast was for continued growth. The International Energy Agency (IEA), for example, projected a 0.93 million bpd increase in global demand for 2026 as of its January 2026 report.

- Following the Hormuz closure and the subsequent price surge, which saw Dated Brent physical prices hit $144 per barrel, forecasts inverted sharply. By June 2026, both the U.S. Energy Information Administration (EIA) and the IEA projected a demand contraction of 1.1 million bpd for the year.

- This swing of over 2 million bpd from expected growth to forecasted decline represents a historic revision. The sharpest impact is expected in Q 2 2026, where the IEA forecasts demand will fall by a staggering 2.45 million bpd year-over-year.

- The market’s ability to self-regulate through price-induced demand destruction is a recurring feature of the global oil market, but the speed and scale of the 2026 contraction are significant, acting as the main buffer against the massive supply deficit.

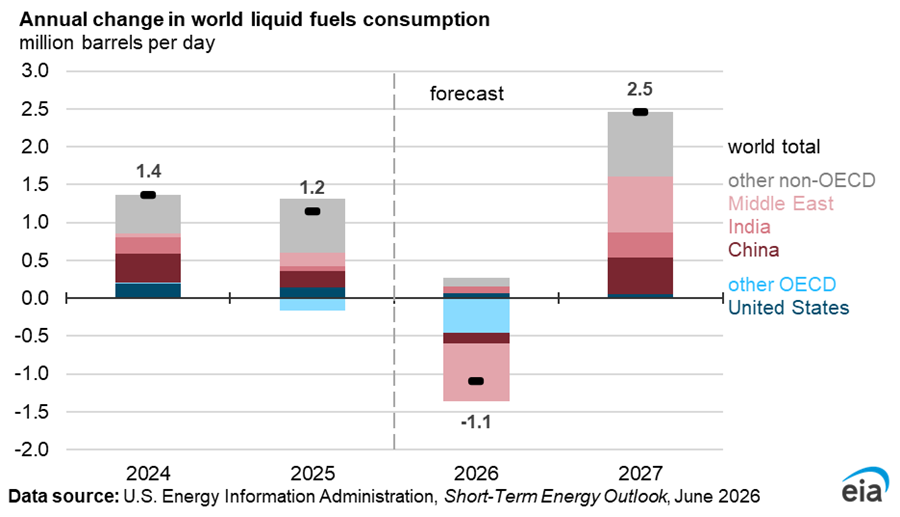

EIA Forecasts 1.1M b/d Oil Demand Drop

The section heading explicitly mentions the IEA and EIA signaling a ‘1.1 M b/d Demand Decline in 2026’. The chart headline ‘EIA Forecasts 1.1M b/d Oil Demand Drop’ directly visualizes this exact data point, making it a perfect match.

(Source: Short-Term Energy Outlook – U.S. Energy Information Administration (EIA))

Table: Global Oil Demand Growth Forecast Revisions for 2026

| Agency | Forecast Date | 2026 Demand Growth Forecast (Million b/d) | Key Commentary | Source |

|---|---|---|---|---|

| IEA | Jun 17, 2026 | -1.1 | Cut forecast again, now expecting a 1.1 MMbpd decline for the year, citing Hormuz disruptions and high prices. | World Oil |

| EIA | Jun 10, 2026 | -1.1 | Forecasts a 1.1 million bpd decline in 2026 vs 2025, stating this will limit price increases. | E&E News |

| IEA | May 13, 2026 | -0.42 | Forecasted a full-year contraction of 420 kb/d, with a sharp 2.45 mb/d Yo Y drop in Q 2. | IEA |

| IEA | Apr 14, 2026 | -0.08 | First forecast of a net annual decline, projecting an 80 kb/d drop vs. prior month’s 730 kb/d growth expectation. | IEA |

| IEA | Jan 21, 2026 | +0.93 | Pre-crisis baseline showing strong demand growth of 930, 000 bpd expected for the year. | Oil Price.com |

OECD vs. Non-OECD, EIA Demand Shock Exposes Geographic Divergence

The impact of demand destruction is not uniform, with developed OECD nations sensitive to high fuel prices contracting sharply, while the economic resilience of non-OECD countries, particularly China, presents the largest uncertainty for future demand recovery.

- In the period from 2021 to 2024, demand growth was largely driven by a synchronized post-pandemic recovery across both OECD and non-OECD regions.

- The 2026 price shock disproportionately affects OECD economies where higher fuel costs translate more directly into changed consumer behavior. The prospect of $7 per gallon gasoline in the United States, for example, creates a powerful incentive for reduced consumption.

- Conversely, as the world’s largest oil importer, China’s economic trajectory is a critical variable. A deeper-than-expected economic slowdown there would amplify the global demand destruction trend, while a resilient economy could provide a floor for global demand.

- This divergence creates a complex geographic dynamic. Government policies and consumer behavior in OECD nations are driving demand reduction, while the structural energy needs of major non-OECD importers remain a powerful force that could quickly tighten the market if supply normalizes.

EIA Forecasts Sharp Drop in OECD Oil Inventories

The section discusses a ‘Geographic Divergence’ with a focus on ‘OECD vs. Non-OECD’ dynamics following a demand shock. This chart specifically illustrates a major impact on the OECD bloc, showing a sharp drop in their inventories, which is a key component of the divergence story.

(Source: Short-Term Energy Outlook – U.S. Energy Information Administration (EIA))

Energy Transition, EIA Crisis Accelerates EV and Efficiency Adoption

The 2026 oil crisis serves as a powerful market catalyst, validating the economic case for mature, commercially available energy transition technologies by making the cost of inaction prohibitively high.

- Between 2021 and 2024, the adoption of technologies like electric vehicles (EVs) and energy efficiency measures progressed steadily, driven primarily by policy incentives and long-term climate goals.

- The current crisis, with its extreme price volatility, has shifted the primary driver from policy to immediate economic necessity. The total cost of ownership for an EV becomes far more compelling when conventional fuel prices are sustained at the high levels seen since Q 1 2026.

- This accelerates the deployment of not just EVs, but also established technologies like smart grid infrastructure and demand response programs, which offer immediate tools to reduce consumption and mitigate price exposure. Investment in grid and power infrastructure is gaining renewed attention as a result.

- The crisis therefore validates that the maturity of these technologies is sufficient for them to act as effective, market-based responses to an energy shock. This includes large-scale renewables like wind energy and alternative industrial processes like carbon capture.

Oil Demand Collapses Sharply in Early 2026

The section heading describes a ‘Crisis’ that ‘Accelerates EV and Efficiency Adoption’. The chart’s depiction of a sharp ‘Oil Demand Collapse’ provides the visual evidence for the crisis event that would catalyze the accelerated energy transition discussed in the section.

(Source: MarketWatch)

SWOT Analysis, EIA Highlights Oil Market Strengths and Risks in 2026

A SWOT analysis reveals that while the oil market’s inherent ability to balance through demand destruction is a key strength, this mechanism comes at a high economic cost and is vulnerable to the duration of the underlying supply shock.

Hormuz Closure Halts Over 11M Barrels Daily

This section covers a ‘SWOT Analysis’ focusing on oil market ‘Strengths and Risks’. The potential closure of the Strait of Hormuz is a classic and significant geopolitical ‘Threat’ (risk) to global oil supply. This chart quantifies that specific risk, making it an ideal illustration for the ‘Threats’ component of the SWOT analysis.

(Source: Short-Term Energy Outlook – U.S. Energy Information Administration (EIA))

Table: SWOT Analysis for Global Oil Market Demand Dynamics

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Market demonstrated price elasticity, with demand responding to price signals during post-COVID volatility. | Rapid and severe demand destruction in response to the Hormuz price shock acts as a natural price ceiling. | The market’s ability to self-correct via price is validated as its most powerful short-term balancing mechanism. |

| Weaknesses | Global supply chains were already strained, with low inventory levels providing a limited buffer. | The primary balancing mechanism (demand destruction) equates to a severe economic slowdown or recession. Inventories are drawn down to unsustainable levels, reaching lows not seen since 2024. | The reliance on demand destruction as a fix is exposed as a painful, economically damaging process. The weakness of low inventory buffers is fully realized. |

| Opportunities | Steady policy-driven growth in energy transition technologies (EVs, renewables). | High oil prices create a powerful, market-driven business case for accelerating the adoption of EVs, energy efficiency, and renewables. Nations seek to “friend-shore” energy supplies from stable regions. | The energy transition is validated not just as a climate solution but as a critical energy security strategy, accelerating adoption curves. |

| Threats | Geopolitical risk was a known but often discounted factor in pricing models. | A prolonged Hormuz closure could exhaust inventory buffers, overwhelming the demand-destruction effect and causing a second, more severe price spike. Geopolitical escalation is an imminent market threat. | The threat of geopolitical chokepoints is validated as the single largest risk to market stability, capable of overriding traditional supply/demand fundamentals. |

EIA Scenario Modeling, A Bifurcated Outlook for Brent Prices (2026)

The global oil market’s trajectory for the second half of 2026 and beyond is defined by two divergent scenarios, with the viability of the recent U.S.-Iran 60-day ceasefire and subsequent reopening of the Strait of Hormuz as the sole determining factor.

- Scenario 1 (Strait Reopens): If the ceasefire holds and maritime traffic normalizes by Q 4 2026, the market faces a potential supply glut. Production returning to a market with structurally lower demand would reinforce the EIA’s forecast for prices to fall toward $89/bbl in Q 4 2026 and average $79/bbl in 2027. The key signal to watch is a slowdown in global inventory draws and a narrowing of physical price premiums.

- Scenario 2 (Strait Remains Closed): If the diplomatic process fails, the current rate of inventory draws becomes unsustainable. The demand destruction seen to date would prove insufficient to balance the market. In this scenario, prices would need to rise significantly, likely back above $120/bbl, to force an even deeper economic contraction and bring the market back into a volatile balance. The key signal here would be continued rapid inventory declines.

EIA Chart Shows Oil Prices Spiking in 2026

The section heading focuses on ‘EIA Scenario Modeling’ and a ‘Bifurcated Outlook for Brent Prices (2026)’. This chart, showing oil prices ‘spiking in 2026’ according to the EIA, directly illustrates one of the key scenarios (the high-price case) that would be central to a discussion about a bifurcated, or split, price outlook.

(Source: Short-Term Energy Outlook – U.S. Energy Information Administration (EIA))

The questions your competitors are already asking

This report covers one angle of the oil market’s reaction to supply shocks: demand destruction. The questions that matter most depend on your work.

- What is the status of the IEA and EIA’s historic downward revisions for global oil demand?

- What is the updated price outlook for Dated Brent crude, given that demand destruction is capping the upside above $150?

- Which economic sectors are contributing most to the forecasted 1.1 M b/d demand decline for 2026?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.