Grid Infrastructure Bottlenecks, 25% of Global Capacity Stalled, $34 B in Project Cancellations, and Surging PJM Capacity Prices (2025 to 2026)

Project Cancellations and Delays, Over $34 B in Clean Energy Projects Halted (2025)

Regulatory and policy uncertainty has become the primary impediment to energy investment, leading to a significant increase in project cancellations and development delays. This shift marks a departure from the 2021-2024 period when technology and market risks were the main concerns. Now, unstable federal policies, contentious permitting reforms, and persistent grid interconnection delays are paralyzing capital, even as demand for energy from data centers and electrification surges.

- In a stark validation of this risk, companies canceled or downsized over $34 billion in U.S. clean energy projects in 2025. This trend is driven by the unpredictable nature of federal incentives, particularly the Inflation Reduction Act (IRA), which faces persistent threats of repeal or modification.

- The problem extends beyond incentives to fundamental administrative barriers. An analysis of half-year reports from 2026 reveals that grid constraints and policy uncertainty are now the top risks cited by investors, holding back nearly a quarter of new global generation capacity from connecting to the grid.

- This “permitting paralysis” is not a new issue, but its collision with surging energy demand has created an acute bottleneck. The revision of the National Environmental Policy Act (NEPA) implementing regulations in February 2026 added another layer of complexity, further stalling projects in development purgatory.

- The impacts are felt across the energy spectrum, not just in renewables. The historic failure to plan and build adequate transmission infrastructure increases congestion and costs for all generation types, threatening both climate goals and overall energy security.

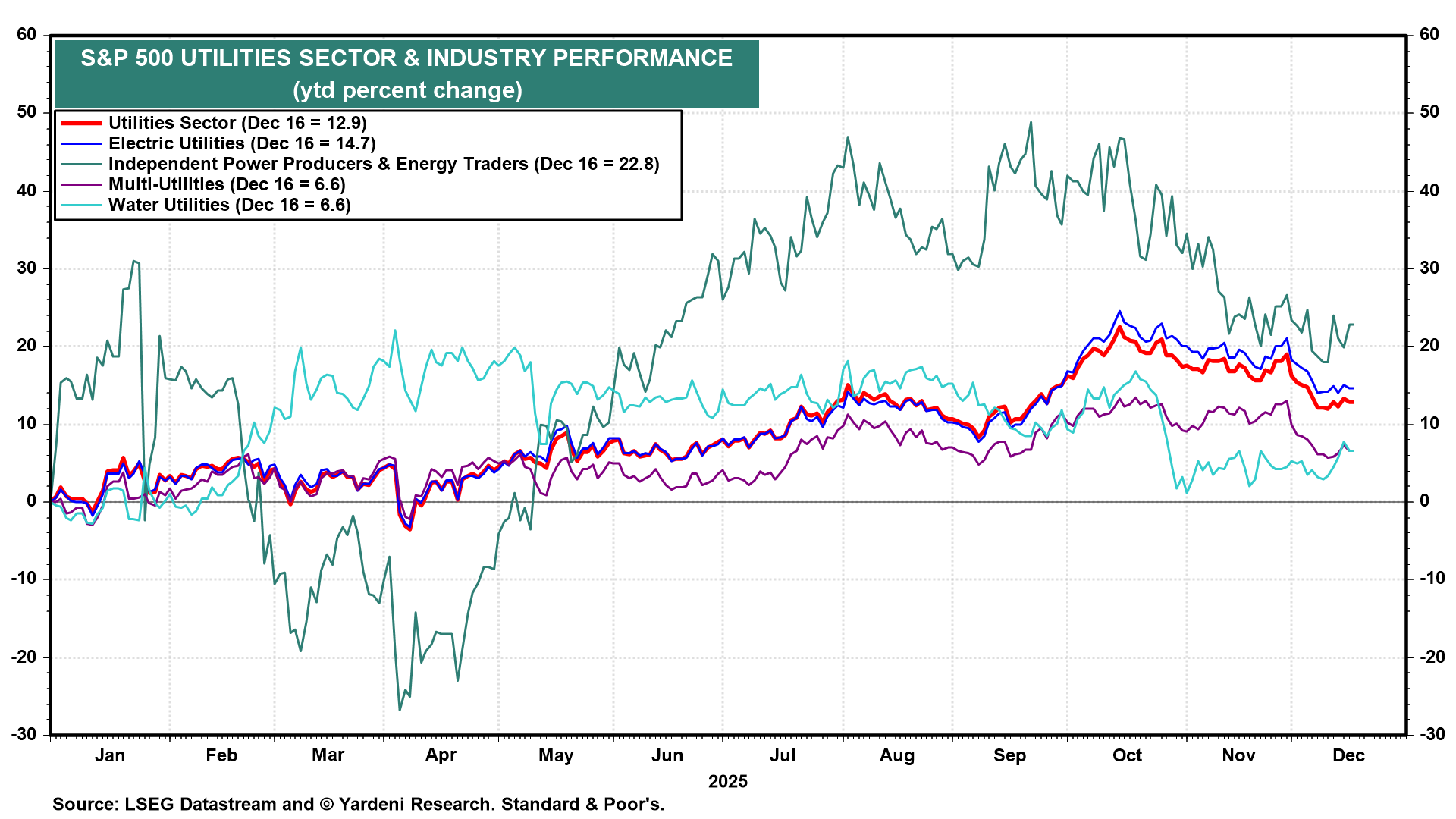

Independent Power Producers See Volatile Stock Performance

The section’s focus on project cancellations and financial halts directly correlates with the volatile stock performance of Independent Power Producers, who are key developers of such projects. The chart illustrates the financial market’s instability resulting from these industry-wide challenges.

(Source: Yardeni Research)

Energy Investment Headwinds, $34 B in Cancellations and PJM Price Spikes (2026)

The financial consequences of regulatory paralysis are now clearly visible in both capital investment trends and wholesale energy markets. The uncertainty has directly translated into billions in abandoned projects and record-high capacity prices, forcing a strategic retreat by investors away from projects with any exposure to merchant risk.

- The more than $34 billion in U.S. clean energy project cancellations during 2025 serves as the most direct financial metric of policy instability. This figure reflects capital that was ready for deployment but was withdrawn due to an untenable risk environment created by potential tax credit modifications and permitting hurdles.

- In the wholesale markets, the 2026–2027 PJM capacity auction clearing at the highest price ever recorded provides a clear signal of impending supply shortages. These prices reflect the market’s expectation that new generation will fail to come online in time to meet demand, a direct result of the development pipeline being stalled.

- Market volatility was further demonstrated during Winter Storm Fern in January 2026, when PJM wholesale electricity prices spiked to between $400-$700/MWh. These events highlight the fragility of a grid that is not being expanded and reinforced with new, dispatchable assets.

- In response, investors are heavily prioritizing projects with de-risked revenue streams, primarily through long-term offtake agreements like Power Purchase Agreements (PPAs). This flight to safety is narrowing the field of “bankable” projects.

Table: Financial Impacts of Regulatory Uncertainty

| Event / Metric | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Clean Energy Project Cancellations | 2025 | Over $34 billion in U.S. projects were canceled or downsized due to uncertainty around tax credits and permitting, halting capital deployment. | E&E News |

| PJM Capacity Auction Price | 2026-2027 | The auction cleared at the highest price ever recorded, signaling severe supply constraints caused by the inability of new projects to navigate the development pipeline. | Integrity Energy |

| PJM Wholesale Price Spike | Jan 2026 | During Winter Storm Fern, prices reached $400-$700/MWh, exposing the grid’s vulnerability and the financial risk of insufficient generation capacity. | Integrity Energy |

| Global Capacity Stall | H 1 2026 | Nearly 25% of new generation capacity worldwide is held back by grid interconnection bottlenecks, a direct consequence of regulatory and administrative delays. | Womble Bond Dickinson |

Corporate vs. Utility PPAs, Microsoft Secures 500 MW in Offtake Agreements

As investors flee from market risk, offtake agreements have become the central mechanism for de-risking new energy projects. A notable shift is occurring within this space, as large corporate buyers, particularly hyperscale data center operators, are becoming the dominant procurers of clean energy, structuring deals that provide the revenue certainty required to secure financing.

- In the current environment, investors are almost exclusively prioritizing projects with mature, long-term offtake agreements, such as PPAs. These contracts are now essential for achieving bankability and are a prerequisite for project finance.

- Corporate PPAs are increasing relative to traditional utility PPAs. This trend is driven by massive energy demand from the tech sector, exemplified by Microsoft‘s deal in February 2026 to secure 500 MW from developers like Pivot Energy. While this provides developers with a reliable buyer, it can also introduce higher counterparty and credit risk compared to utility agreements.

- The market is also adapting with innovative financing structures designed to navigate IRA uncertainty. In March 2026, Arevon closed $920 million in financing for its Nighthawk energy storage project using a combination of debt, preferred equity, and a tax credit transfer commitment, a model built to mitigate policy risk.

- Public-private partnerships remain crucial for de-risking next-generation technologies. Government bodies like the Australian Renewable Energy Agency (ARENA) are providing direct funding to bridge the “missing middle” for technologies like green hydrogen, a role private capital is increasingly hesitant to play in the U.S.

US Data Center Power Demand Projected to Surge

The section mentions Microsoft, a major data center operator, securing large power agreements. This chart provides the direct context and rationale, illustrating the massive projected surge in power demand from data centers that is driving such corporate offtake deals.

(Source: Distilled)

Table: De-Risking Partnerships and Agreements

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Arevon / Nighthawk Project | Mar 2026 | Secured $920 million for a 1, 200 MWh storage project using a blended debt, equity, and tax credit transfer structure to secure financing amid policy uncertainty. | PR Newswire |

| Microsoft / Pivot Energy | Feb 2026 | Signed PPAs for 500 MW of renewable energy to power data centers, showcasing the central role of corporate offtakers in driving new project development. | Microsoft |

| Australian Renewable Energy Agency (ARENA) | Jan 2026 | Committed over AUD $300 million in grant funding for hydrogen R&D, demonstrating a public-led model to de-risk emerging technologies. | DCCEEW |

| ACWA Power | Feb 2026 | Announced plans to invest $100 billion in clean energy projects, often with backing from sovereign wealth funds, insulating its development from private market volatility. | CATF.us |

$34 B in US Cancellations, Regulatory Uncertainty Varies by Region

While regulatory risk is a global concern, its severity and nature differ significantly by region, with the United States emerging as the primary hotspot for policy-driven investment paralysis. The political polarization around energy policy in the U.S. creates a uniquely volatile environment compared to regions where state-directed investment provides a more stable foundation for development.

- The U.S. is the epicenter of the investment crisis, with the $34 billion in project cancellations in 2025 directly tied to domestic political and policy uncertainty. A 2026 survey found that 75% of U.S. financial leaders view regulatory uncertainty as a top risk, well above the global average of 65%.

- This uncertainty is particularly acute in areas with high data center growth, like Virginia, where grid operator PJM and utilities like Dominion Energy face immense challenges in planning transmission to meet new load, a process complicated by unpredictable state and federal permitting.

- In contrast, other regions are mitigating this risk through different models. In the Middle East, state-backed entities like Saudi Arabia’s ACWA Power are driving large-scale development with sovereign capital, insulating projects from the volatility of private finance markets.

- Australia is using a public-private partnership model, with government agencies like ARENA providing direct grants to de-risk projects in emerging sectors like green hydrogen, ensuring that capital continues to flow to next-generation technologies.

Grid Infrastructure, a Mature Technology Stalled by “Soft Costs”

The core of the energy sector’s current crisis is not a failure of technology but a failure of process. Mature, proven technologies like high-voltage transmission, wind turbines, and solar panels are being stalled by administrative and regulatory hurdles, often referred to as “soft costs, ” which have become more significant barriers than technological or manufacturing challenges.

- The primary bottleneck for energy development has decisively shifted from technology readiness or manufacturing capacity, which were key concerns between 2021-2024, to project deployment in 2025-2026. The problem is no longer building the equipment but getting it approved and connected.

- “Permitting paralysis” and grid interconnection queues are the main drivers of this slowdown. These are not technology problems; they are systemic failures in planning, regulation, and stakeholder management that add years and significant cost to project timelines.

- Even the most well-established technologies are not immune. For example, deploying new transmission lines, a century-old technology, now faces a labyrinth of federal, state, and local approvals that makes timely development nearly impossible.

- This environment also stifles innovation. The deep uncertainty and long delays make it exceptionally difficult for “missing middle” technologies, those proven but not yet at full commercial scale, to attract the private capital needed for deployment, as investors are unwilling to take on both technology and extreme policy risk.

SWOT Analysis, Regulatory Risk vs. Surging Energy Demand

The energy sector is defined by a fundamental conflict between its greatest strength, surging end-user demand, and its most profound weakness, an unstable and unpredictable policy environment. This dynamic creates opportunities for sophisticated players who can manage systemic risk but poses an existential threat to developers exposed to regulatory volatility.

- The sector’s primary strength is the powerful, long-term demand signal from data centers, AI, and the broader electrification of transport and industry. This demand has been validated as a durable driver of growth.

- The critical weakness is the extreme regulatory and policy volatility in key markets like the U.S., which has led to gridlock in permitting and interconnection, neutralizing the strong demand signal.

- This environment creates opportunities for vertically integrated utilities and large infrastructure funds that possess the capital and expertise to navigate complex regulatory processes and structure de-risked financial agreements.

- The overarching threat is that continued policy instability will lead to widespread capital flight, causing the U.S. to fail in meeting its energy security and decarbonization goals as project pipelines wither.

Energy Demand Forecasts Surge in Recent Years

The section heading explicitly mentions “Surging Energy Demand” as a key component of its SWOT analysis. This chart directly visualizes that macro trend, providing the evidence for the “Opportunity” side of the SWOT.

(Source: POWER Magazine)

Table: SWOT Analysis on Energy Investment Risks

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Focus on technology cost reductions and initial benefits of the IRA. | Massive, sustained demand growth from data centers, AI, and electrification. | The strength of the demand signal was validated, but it proved insufficient on its own to overcome systemic policy risk. |

| Weaknesses | Primarily physical supply chain constraints (e.g., polysilicon, critical minerals). | Regulatory uncertainty, permitting paralysis, and grid interconnection queues. | The primary bottleneck shifted definitively from physical “hard costs” to administrative and regulatory “soft costs.” |

| Opportunities | Leveraging IRA tax credits for new project announcements. | M&A of distressed assets, innovative financing, and corporate PPAs. | The opportunity moved from simple project development to complex financial structuring designed to insulate projects from risk. |

| Threats | Competition from low-cost overseas manufacturing and inflation. | Systemic policy reversal, mass project cancellations ($34 B+), and capital flight. | The threat became political and systemic, with the wave of project cancellations validating the real-world impact of policy risk. |

Energy Infrastructure Outlook, Watch PPA Structures and M&A Activity (2026)

Looking ahead through the remainder of 2026, the market is poised for a bifurcation, where well-structured, de-risked projects proceed while others are either canceled or acquired. The key indicators to watch will be the terms of new offtake agreements and the pace of consolidation in the developer space, as these will signal how capital is adapting to the high-uncertainty environment.

- If this happens: If significant policy and regulatory uncertainty persists, expect a rise in M&A activity. Well-capitalized utilities and infrastructure funds will likely acquire distressed renewable assets and development pipelines from smaller players who lack the balance sheet to endure prolonged delays.

- Watch this: The specific terms and duration of corporate PPAs. A shift toward shorter-term agreements or more flexible offtake structures would indicate growing concern among corporate buyers about long-term grid reliability and the viability of the projects they are backing.

- These could be happening: A “flight to quality” is likely to accelerate, where private investment narrows to focus only on the most mature projects in jurisdictions with clear regulatory support. This will further starve the “missing middle” of innovative technologies of the growth capital needed to scale.

Global Energy Investment Pivots to Renewables

This section provides a future outlook on energy infrastructure. The chart, showing a clear pivot in global investment towards renewables, offers a foundational trend that is critical for understanding the sector’s future landscape.

(Source: The Energy Mix Weekender – Substack)

The questions your competitors are already asking

This report covers one angle of the impact of regulatory and policy uncertainty on energy project investments. The questions that matter most depend on your work.

- What is the outlook for new generation capacity connecting to the grid by 2030, given the current interconnection delays?

- How is the risk of Inflation Reduction Act (IRA) repeal or modification impacting project financing and development timelines?

- What is the status of the National Environmental Policy Act (NEPA) revision and its impact on project permitting?

- What are the opportunities for transmission development in congested markets like PJM to alleviate infrastructure bottlenecks?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.