Qatar’s Hydrogen Dominance at Risk: How 2026 Geopolitical Shocks Expose Infrastructure Vulnerability

From Blueprints to Battlefields: Qatar’s Hydrogen Projects Face New Geopolitical Realities in 2026

Qatar Energy’s calculated strategy to dominate the global blue ammonia market has transitioned from a phase of planning and partnerships into a period of execution marked by significant geopolitical risk. The period between 2025 and 2026 validated the commercial model but also revealed its acute vulnerability to regional conflict, shifting the primary risk from market acceptance to physical asset security. The hypothetical but plausible suspension of LNG and downstream production in March 2026 due to military attacks transformed theoretical risks into tangible operational and financial threats, fundamentally altering the calculus for investors and offtakers reliant on Qatari supply.

- Between 2021 and 2024, Qatar Energy focused on establishing the commercial framework for its hydrogen ambitions, signing foundational partnerships with Shell to develop UK hydrogen markets and with South Korea’s H 2 Korea to build an Asian supply chain. These moves were about securing future demand.

- The 2025-2026 period shifted focus to execution and immediate risk. The impending April 2026 commissioning of the world’s largest blue ammonia plant in Mesaieed was a major milestone, but its significance was immediately challenged by regional instability.

- The reported production shutdowns in March 2026 at Qatari facilities, including those for methanol and urea, underscore the high degree of centralization in its industrial hubs. This event demonstrates that a disruption to LNG feedstock production creates a cascading failure across the entire value chain, including low-carbon ammonia.

- This escalation of risk directly impacts the bankability of long-term offtake agreements, such as the 25-year condensate supply deal with Shell. The reliability of Qatar as a supplier is now a primary concern, potentially impacting future LNG supply chains and the global energy transition.

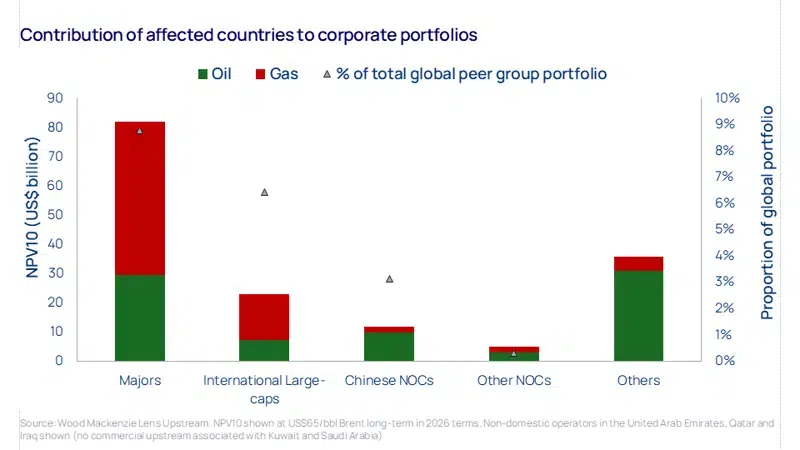

Geopolitical Risk Threatens Billions in Assets

The section discusses new geopolitical risks to Qatar’s hydrogen projects in 2026. This chart quantifies the exposure, showing the 2026 Net Present Value of assets in sensitive countries like Qatar totals over $82 billion for major energy companies.

(Source: EnkiAI)

Investment Under Fire: Securing Qatar’s Multi-Billion Dollar Hydrogen Bet

Qatar Energy’s aggressive capital deployment into blue ammonia and its enabling infrastructure is now directly exposed to regional military conflict, making asset security and operational resilience paramount. While the period from 2021 to 2024 was defined by financial commitments to massive feedstock and production projects, the events of 2026 highlight that the return on these multi-billion-dollar investments is contingent on regional stability. The concentration of these high-value assets within a limited geographic area creates a critical vulnerability that market participants can no longer ignore.

Qatar’s Investment Focus Shifts to Gas

The section highlights Qatar’s multi-billion dollar capital deployment into its hydrogen strategy, which uses gas as a feedstock. This chart visualizes that investment, showing gas activities jumping to 83% of Qatar’s total energy investment by 2022.

(Source: Al Jazeera Centre for Studies)

- The cornerstone investment, the blue ammonia plant in Mesaieed, represents a direct capital deployment into low-carbon fuels, but its location makes it susceptible to the same threats facing Qatar’s broader energy infrastructure.

- Feedstock for this plant is secured by the massive North Field expansion. The award of a major contract for the North Field West project to Technip Energies in February 2026 demonstrates continued investment, yet the entire upstream and midstream value chain is exposed.

- Qatar Energy’s ambition to scale rapidly is evidenced by an EPC tender issued in August 2025 for a second major low-carbon ammonia and urea complex. This planned expansion now faces a much higher risk premium from investors and contractors.

Table: Qatar Energy’s Key Feedstock and Low-Carbon Investments (2025-2026)

| Project / Investment | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| North Field West LNG Project | Feb 2026 | Awarded major EPC contract to Technip Energies to develop upstream gas infrastructure, securing feedstock for both LNG and future blue ammonia production. | Technip Energies |

| New Low-Carbon Ammonia & Urea Complex | Aug 2025 | Issued an Engineering, Procurement, and Construction (EPC) tender for a second large-scale facility in Mesaieed, signaling intent to rapidly scale blue ammonia capacity. | Straits Research |

| Petrochemical Capacity Expansion Plan | Jun 2025 | Announced a broad strategy to more than double petrochemical production capacity, leveraging the natural gas value chain that underpins its hydrogen activities. | Portfolio-pplus.com |

Strategic Alliances Tested: Qatar’s Hydrogen Partnerships in a Volatile Region

The value of Qatar Energy’s strategic partnerships, once centered on market access and technology collaboration, is now being tested by the urgent need for supply chain resilience. Alliances formed between 2021 and 2024 were designed to build future demand in key markets like Europe and Asia. However, the operational disruptions of 2026 have shifted the focus for partners like Shell and Uniper toward securing reliable, uninterruptible supply, a factor that now overshadows cost and volume considerations.

Partnerships Hinge on Key Asian Markets

The section describes how alliances are being tested to secure supply for key markets like Asia. The chart confirms Asia’s importance, showing nations like China and India are the dominant destinations for Qatar’s LNG exports in 2025.

(Source: EnkiAI)

Qatar to Dominate New LNG Wave

The section’s table details new investments in feedstock projects like the North Field West LNG expansion. This chart projects that Qatar will be a dominant force in the ‘Third wave’ of global LNG capacity expansion beginning in 2025.

(Source: Center on Global Energy Policy – Columbia University)

- The partnership with Technip Energies, awarded in February 2026 for the North Field West project, is critical for feedstock supply. Its success is now directly tied to Qatar’s ability to protect its upstream assets from disruption.

- Long-term offtake agreements with Shell for condensate and naphtha, signed in 2025, were intended to de-risk investments. Now, these deals face counterparty risk from potential supply interruptions, a scenario that could trigger a re-evaluation of the US LNG vs Qatar LNG security premium.

- The partnership with Eni in Egypt’s offshore gas sector, announced in October 2025, represents a move to diversify gas sourcing. This could become a critical hedge against disruptions to its domestic production, although it does not secure the massive downstream assets located within Qatar.

Table: Qatar Energy’s Key Commercial Partnerships (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Technip Energies | Feb 2026 | Awarded EPC contract for the North Field West LNG project, foundational for securing natural gas feedstock for blue ammonia. | Technip Energies |

| Uniper | Dec 2025 | Signed a long-term sales agreement for liquid helium, strengthening the commercial viability of integrated gas processing operations at Ras Laffan. | Uniper |

| Eni | Oct 2025 | Acquired interests in six offshore concessions in Egypt, diversifying upstream natural gas sourcing beyond Qatar. | Oil & Gas Middle East |

| Shell | Apr-May 2025 | Signed 25-year condensate and 20-year naphtha supply agreements, securing long-term offtake for key products from the gas value chain. | Chem Analyst |

Geographic Centralization: Qatar’s Hydrogen Strategy as a Single Point of Failure

Qatar’s hydrogen strategy is built on a foundation of extreme geographic concentration, which has now emerged as its single greatest vulnerability. While the 2021-2024 period saw Qatar Energy establishing a global footprint through international partnerships, the physical reality is that its entire blue ammonia production capability is centralized in domestic industrial cities like Mesaieed and Ras Laffan. The events of 2026 demonstrate that this concentration creates a critical single point of failure, where a regional conflict can halt the nation’s entire low-carbon export capacity.

Economy Heavily Reliant on Gas Exports

The section warns that centralizing all hydrogen production creates a single point of failure. This chart illustrates that kind of extreme economic concentration, showing that fuels and petroleum products comprise over 81% of a typical exporter’s economy.

(Source: ScienceDirect.com)

Visualizing QatarEnergy’s Global Partnership Network

This section tables QatarEnergy’s key commercial partners, detailing their role in new projects. The chart provides a direct visual representation of this global network of assets and partnerships, centered around Qatar.

(Source: AInvest)

- Between 2021 and 2024, Qatar Energy’s geographic strategy appeared diversified, with partnership announcements targeting markets in the UK (with Shell) and South Korea (with H 2 Korea).

- The 2025-2026 period has exposed the flaw in this strategy: while demand is global, production is hyper-local. The planned commissioning of the blue ammonia plant in Mesaieed in April 2026, followed by a tender for a second plant in the same location, doubles down on this geographic concentration.

- The hypothetical military attacks in March 2026, which reportedly halted downstream activity, confirm that the industrial hubs of Mesaieed and Ras Laffan are the nexus of this risk. A disruption in one part of this integrated system can paralyze the whole.

- While the October 2025 partnership with Eni in Egypt shows some effort to diversify upstream assets, it does nothing to mitigate the risk to the multi-billion-dollar downstream and export facilities located exclusively inside Qatar.

Blue Ammonia at Scale: Qatar’s Technology Deployed Amidst Rising Threats

Qatar Energy has successfully advanced its blue ammonia production technology from concept to commercial-scale deployment, but this technological achievement is now overshadowed by the operational inability to guarantee production. The period from 2021-2024 was characterized by planning and engineering for the Ammonia-7 project, integrating steam-methane reforming with Carbon Capture and Storage (CCS). The 2025-2026 period saw this technology become a physical reality, only to be immediately threatened by external forces beyond its control.

Decarbonization Roadmap Touts CCS Growth

The section focuses on deploying blue ammonia technology, which relies on Carbon Capture and Storage (CCS). The chart details QatarEnergy’s specific strategy to dramatically increase its CO2 injection (CCS) capacity to 9.5 MTA by 2030.

(Source: QatarEnergy LNG – Sustainability)

- In the 2021-2024 timeframe, the key technology milestone was the final investment decision and engineering design for the Ammonia-7 plant, which integrates conventional ammonia synthesis with a large-scale CCS facility.

- The impending April 2026 commissioning of the Mesaieed plant marks the successful deployment of this technology at world scale. This facility is designed to produce blue ammonia by capturing and sequestering the associated CO₂, a key differentiator.

- However, the production halts of March 2026 demonstrate that the technological sophistication of the plant is irrelevant if feedstock from the North Field is interrupted or if the facility itself is at risk.

- While the company continues to explore novel production methods, evidenced by research into “aqua hydrogen, ” its entire near-term strategy and capital investment rest on a blue hydrogen pathway that has proven vulnerable to physical disruption.

SWOT Analysis: Qatar’s Hydrogen Ambitions at a 2026 Crossroads

Qatar Energy’s hydrogen strategy is at an inflection point where its formidable strengths in natural gas reserves and capital are being directly challenged by severe, external geopolitical threats. The company successfully executed its initial strategy of leveraging hydrocarbon incumbency to build a dominant position in blue ammonia. However, the events of 2026 have validated the threat scenario, shifting the focus from market creation to infrastructure defense and supply chain resilience.

Framework Outlines Hydrogen Strategy Options

This section introduces a high-level SWOT analysis of Qatar’s hydrogen strategy at a crossroads. The chart provides an ideal strategic framework, modeling different hydrogen pathways and investment levels for fossil fuel exporting nations.

(Source: ScienceDirect.com)

- Strengths: Unmatched natural gas reserves and low production costs remain the core advantage, enabling large-scale, cost-competitive blue hydrogen production.

- Weaknesses: The extreme geographic concentration of its production and export infrastructure in Mesaieed and Ras Laffan has been validated as a critical single point of failure.

- Opportunities: If it can secure its infrastructure, Qatar can still capture a dominant share of the nascent global blue ammonia market, particularly in Asia and Europe where buyers seek large, reliable volumes.

- Threats: Regional military conflict has been validated as the primary threat, capable of causing cascading failures across the entire value chain and undermining Qatar’s status as a reliable energy supplier, triggering a potential supply crisis.

Table: SWOT Analysis for Qatar Energy’s Hydrogen Strategy

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Vast, low-cost natural gas reserves. Financial capacity from LNG profits to fund large-scale projects. Established partnerships with majors like Shell and Exxon Mobil. | Massive LNG expansion (North Field East, West) secures feedstock for decades. Proven ability to finance and construct world-scale projects like the Ammonia-7 plant. | The core strength of low-cost gas as a feedstock for blue ammonia was validated. Financial firepower from LNG expansions was confirmed as a key enabler. |

| Weaknesses | High dependence on a single resource (natural gas). Geographic concentration of industrial assets. Nascent market for blue ammonia. | Over-reliance on the Strait of Hormuz for exports. High centralization of new ammonia plants (Mesaieed) and CCS hubs (Ras Laffan). | The weakness of geographic concentration was validated by the March 2026 production halts, demonstrating a critical single point of failure. |

| Opportunities | First-mover advantage in large-scale blue ammonia exports. Potential to supply key decarbonizing markets in Asia (Korea, Japan) and Europe (UK, Germany). | Ammonia-7 plant commissioning in 2026 positions Qatar as the world’s largest blue ammonia supplier. Long-term offtake deals with Shell and Uniper secure demand. | The market opportunity was validated by securing long-term deals, but the ability to capitalize on it is now conditional on mitigating new threats. |

| Threats | Geopolitical instability in the Persian Gulf. Competition from green hydrogen projects in other regions. Fluctuations in natural gas prices. | Regional military conflict leading to direct attacks on infrastructure and production stoppages (March 2026). Supply chain disruptions undermining its role as a reliable supplier. | The theoretical threat of geopolitical conflict was validated as a tangible, operational risk that can halt the entire export value chain. This is now the primary strategic threat. |

2026 Outlook: Can Qatar Energy De-Risk its Hydrogen Supply Chain?

The critical strategic imperative for Qatar Energy in the year ahead is to prove it can defend its centralized infrastructure and re-establish itself as a secure, reliable supplier of low-carbon fuels. The company’s ability to prevent further disruptions and maintain operational uptime at its Mesaieed and Ras Laffan facilities will be the single most important signal for the market. Failure to do so will undermine confidence in its multi-billion-dollar hydrogen investments and cede market share to more secure, albeit potentially higher-cost, producers.

Meeting Future Export Demand Is Critical

The outlook section questions if Qatar can de-risk its supply chain and remain a reliable supplier. This chart forecasts significant growth in hydrogen export demand, highlighting the market Qatar must reliably supply to succeed.

(Source: ScienceDirect.com)

Hydrogen Investment Scenarios Show Financial Scale

The SWOT table in this section lists financial capacity and funding large-scale projects as a key strength. This chart illustrates the potential scale of the financial bet, showing investment and revenue scenarios for hydrogen peaking at over $22 billion.

(Source: ScienceDirect.com)

- Watch Signal 1: Operational Resilience. The market will closely monitor the operational performance of the Mesaieed Ammonia-CCS plant following its April 2026 commissioning. Any further unplanned outages or signs of ongoing security threats will severely damage market confidence.

- Watch Signal 2: Progress on Second Ammonia Plant. The final investment decision and EPC contract award for the second ammonia complex will be a key indicator. A delay or cancellation would signal that the perceived risk is too high, while moving forward would signal a high degree of confidence in its mitigation strategies.

- Watch Signal 3: Diversification Strategy. Look for any new investments or partnerships aimed at geographically diversifying production or creating strategic reserves outside the Persian Gulf. The existing partnership with Eni in Egypt is a start, but more significant moves are needed to hedge against its core geographic risk.

Frequently Asked Questions

What is the primary risk to Qatar’s hydrogen dominance according to the article?

The primary risk has shifted from market acceptance to physical asset security. The article argues that the extreme geographic concentration of Qatar’s entire hydrogen and LNG production infrastructure in domestic industrial cities like Mesaieed and Ras Laffan creates a critical single point of failure, making it highly vulnerable to regional military conflict, as highlighted by the hypothetical events of March 2026.

Why were the hypothetical military attacks in March 2026 so significant?

The March 2026 attacks were significant because they transformed a theoretical risk into a tangible operational threat. The resulting production shutdowns demonstrated that an attack on LNG feedstock facilities could cause a cascading failure across the entire value chain, halting downstream production of products like methanol, urea, and the soon-to-be-commissioned blue ammonia. This undermines Qatar’s status as a reliable supplier.

What is Qatar’s core strategy for becoming a leader in the hydrogen market?

Qatar’s strategy is to leverage its core strength: vast, low-cost natural gas reserves from projects like the North Field expansion. By using this natural gas as a feedstock, it aims to produce blue ammonia at a massive scale and at a competitive cost. This is exemplified by the construction of the world’s largest blue ammonia plant (Ammonia-7) in Mesaieed, which integrates steam-methane reforming with Carbon Capture and Storage (CCS).

How have the events of 2026 affected Qatar’s partnerships with companies like Shell?

The events have shifted the focus for partners like Shell from securing long-term volume and favorable pricing to prioritizing supply chain resilience and reliability. The risk of supply interruptions, as demonstrated by the production halts, directly threatens the bankability of long-term offtake agreements, such as the 25-year condensate supply deal. This forces partners to re-evaluate the security premium of sourcing from Qatar.

What are the key signals to watch for in Qatar’s hydrogen strategy going forward?

The article suggests three key watch signals. First, the operational resilience of the new Mesaieed blue ammonia plant after its April 2026 commissioning. Second, whether Qatar moves forward with a final investment decision on its planned second ammonia complex. Third, any new strategic moves to geographically diversify its production assets beyond the Persian Gulf, building on its small upstream investment in Egypt with Eni.