US LNG vs Qatar LNG: How the 2026 Iran Conflict Redefines Global Energy Reliability

LNG Supply Chain Risk: 2026 Conflict Exposes Middle East Fragility

The 2026 US-Iran conflict has transformed LNG supply chain risk from a theoretical vulnerability into a realized disruption, fundamentally elevating the strategic value of secure US supply over cost-competitive but fragile Middle Eastern sources. Before 2025, global buyers balanced Qatar’s low production cost against its geopolitical risks; the conflict has now made that risk quantifiable and unacceptable for ensuring energy security, triggering a structural flight to safety.

- Prior to 2025, the market tolerated Middle Eastern geopolitical risk, demonstrated by events like the Houthi attacks in the Red Sea, which caused delivery delays for Qatar Energy but did not halt production. The primary competition was economic, weighing Qatar’s low production cost against the contractual flexibility of US suppliers.

- The onset of the conflict in 2026 triggered a severe disruption centered on the Strait of Hormuz, a chokepoint for approximately 20% of global LNG supply. This was not a theoretical exercise; Qatar Energy halted production at its Ras Laffan complex, immediately removing a massive volume of supply from the market.

- This event caused a violent price shock in import-dependent regions, with European natural gas prices surging by as much as 45%. In stark contrast, domestic natural gas prices in the U.S. remained stable, highlighting the insulation of U.S. supply from the conflict and widening the economic arbitrage for its LNG exports.

- The disruption validates the strategic pivot toward supply diversification that began after the 2022 European energy crisis. Nations in both Europe and Asia must now reassess their energy security with a much higher weighting on supplier reliability and geographical insulation from conflict zones.

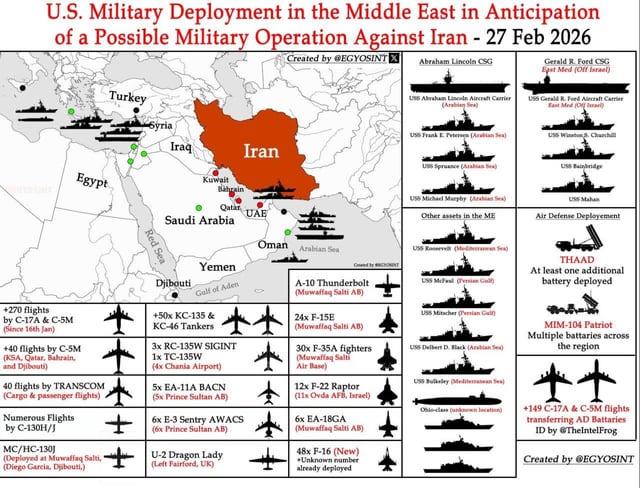

US Deploys Forces Near Iran in 2026

This map details the US military deployment in February 2026, providing direct visual context for the conflict that exposes Middle East LNG supply fragility.

(Source: Reddit)

Investment Accelerates: US LNG Projects Gain Unmatched Momentum in 2026

The conflict acts as a powerful catalyst, accelerating Final Investment Decisions (FIDs) for a new wave of U.S. LNG projects as global buyers rush to secure long-term offtake agreements from geographically insulated suppliers. While Qatar’s massive expansion plans remain formidable, the demonstrated unreliability of its core export route makes securing financing and long-term contracts for new Middle Eastern capacity more challenging, directly benefiting North American developers.

- The crisis provides an urgent demand signal for the massive expansion of U.S. LNG capacity, which is projected to grow by 75% by 2030. The reversal of the Biden administration’s pause on new LNG export licenses in February 2025 provided the regulatory certainty needed for these projects to capitalize on the new market reality.

- This market shift enhances the bankability of next-generation U.S. projects. Developers are de-risking projects by using modular construction to lower capital expenditures and integrating decarbonization technologies like Carbon Capture, Utilization, and Storage (CCUS) to meet buyer demands for lower-carbon energy.

- Leading technology selections, such as Conoco Phillips’ Optimized Cascade process for the 22.5 MTPA Coastal Bend LNG project, ensure high efficiency and lower emissions, making new U.S. facilities more competitive for the long term.

- The surge in contracting for U.S. projects mirrors the trend seen in 2022, when the European energy crisis drove the signing of 65 mmtpa of long-term U.S. LNG contracts. The 2026 conflict provides an even stronger impetus for buyers to lock in secure, non-Middle Eastern supply.

Table: Key U.S. LNG Project and Technology Developments

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| U.S. LNG Modular Construction | Sept 2025 | Industry-wide trend among LNG developers to use modular processes to reduce labor, equipment costs, and construction timelines, lowering CAPEX for new export facilities. | Reuters |

| Coastal Bend LNG | Aug 2025 | Conoco Phillips’ low-emission Optimized Cascade process was selected for this planned 22.5 million tons per annum (mtpa) facility, enhancing its efficiency and environmental profile. | Offshore Energy |

| PKN ORLEN and Sempra Infrastructure | Jan 2023 | Long-term LNG Sales and Purchase Agreement (SPA) highlighting the trend of European buyers securing U.S. supply. Sempra’s model is built on destination-flexible contracts. | ORLEN |

Geographic Realignment: US Gulf Coast Becomes the Anchor of LNG Reliability

The US-Iran conflict starkly delineates the global LNG market along geographical lines, exposing the acute chokepoint dependency of Qatari exports and establishing the U.S. Gulf Coast as the preeminent hub for reliable energy supply. The conflict provides physical proof that geography is now a primary determinant of energy security, a lesson learned after Russia’s invasion of Ukraine and now reinforced in the Middle East.

US LNG Exports Pivot to Europe

This chart shows the US bolstering European energy supply after 2022, providing historical proof of the reliability that makes the US Gulf Coast an anchor for global LNG.

(Source: Natural Gas Intelligence)

- Qatar’s entire LNG export volume is dependent on passage through the Strait of Hormuz, a 33-km wide waterway that Iran can disrupt or close. The 2026 conflict moved this from a distant threat to an active disruption, forcing production halts.

- In contrast, U.S. LNG export terminals are located on the Gulf of Mexico, geographically isolated from the conflict. Cargoes have diverse and secure maritime routes to key markets in Europe and Asia, avoiding Middle Eastern chokepoints entirely.

- Between 2021 and 2024, U.S. LNG exports to Europe surged over 100% as the continent pivoted away from Russian gas, proving the reliability of U.S. supply chains during a major geopolitical crisis. The 2026 conflict cements this role on a global scale.

- For LNG buyers, the risk-adjusted cost of supply has fundamentally changed. The higher insurance, freight, and potential disruption costs associated with Middle Eastern supply now favor U.S. contracts, even if their headline price is higher.

Technology and Capacity: US Positioned to Absorb Global Demand Shock

The United States’ combination of a massive, well-defined project pipeline and advanced LNG technologies provides the unique capacity to absorb the demand shock created by the Middle East crisis. While Qatar is a low-cost producer, its operational status is binary in a conflict: on or off. The U.S. offers a resilient, scalable, and technologically advanced alternative that is now the market’s preferred choice for growth and reliability.

- Before 2025, the narrative often focused on a race between U.S. and Qatari expansion. The U.S. was already on track to more than double its export capacity to over 24.3 Bcf/d by 2028, but the 2026 crisis ensures offtake for this capacity and accelerates demand for the next wave of projects.

- U.S. developers are embedding advanced technology to improve their techno-economic profile. This includes the use of industrial AI to optimize complex plant operations for reliability, as deployed by firms like Cheniere Energy, and advanced gas treatment from Honeywell UOP, used in approximately 40% of global LNG feedstock.

- The ability to offer lower-carbon LNG is a growing requirement. New U.S. projects are integrating CCUS and electrification (“e LNG”), making them more attractive to climate-conscious buyers in Europe and Asia and enhancing their long-term viability beyond the current shock to the global energy transition.

SWOT Analysis: US LNG vs. Qatar LNG Post-Conflict

The 2026 conflict fundamentally re-weighted the strategic calculus for global LNG, shifting the primary market driver from cost to security. This pivot validated the strengths of the U.S. supply model while transforming Qatar’s primary geographic weakness from a theoretical risk into a material liability.

Mideast Conflict Puts Over $80B at Risk

This chart quantifies the significant financial exposure of energy majors’ gas assets in the region, highlighting a key threat within the post-conflict SWOT analysis.

(Source: Wood Mackenzie)

Table: SWOT Analysis of US vs. Qatari LNG Reliability

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | US: Destination-flexible, Henry Hub-linked contracts. Qatar: World’s lowest production cost (as low as $0.30/MMBtu). | US: Geographic insulation and proven supply reliability during crisis. Qatar: Low production cost remains, but is negated by delivery risk. | The conflict validated U.S. supply reliability as its paramount strength, overtaking Qatar’s cost advantage as the primary purchasing consideration for security-focused buyers. |

| Weaknesses | US: Higher production and liquefaction costs ($3-$5/MMBtu). Qatar: 100% reliance on the Strait of Hormuz chokepoint (a theoretical risk). | US: Higher cost structure remains, but is offset by reliability premium. Qatar: Chokepoint dependency becomes a realized, catastrophic weakness, forcing production halts. | Qatar’s long-understood geographic weakness was physically demonstrated, transforming it from a line item in a risk register to a primary driver of market avoidance. |

| Opportunities | US: Capitalize on European diversification from Russian gas. Qatar: Lock in price-sensitive Asian buyers with long-term, oil-indexed contracts. | US: Accelerate FIDs for the second wave of LNG projects and become the global supplier of last resort. Qatar: Limited ability to capitalize on price spikes due to inability to deliver. | The U.S. has a clear opportunity to capture permanent market share and solidify its role as the anchor of global LNG supply, a process that began in 2022 and was cemented by the 2026 crisis. |

| Threats | US: Regulatory uncertainty over new project approvals. Qatar: Regional geopolitical instability and competition from growing U.S. supply. | US: Construction bottlenecks for its massive expansion. Qatar: Direct military conflict makes exports impossible and jeopardizes long-term contracts. | The primary geopolitical threat in the market materialized, directly impacting Qatar while creating a powerful tailwind for its main competitor, the United States. The transition fuel narrative for LNG is now under severe scrutiny. |

Scenario: A Permanent Security Premium on US LNG

Looking ahead, energy executives must model a permanent “security premium” on U.S. LNG, where buyers worldwide prioritize supply chain integrity over lowest-cost production. This new market paradigm, born from the crises in Ukraine and the Middle East, will define LNG contracting, investment, and trade flows through the end of the decade, triggering a permanent shift in LNG supply chains.

Asian Buyers Rely on Qatari LNG

This chart identifies the key Asian customers dependent on Qatar’s exports, highlighting the markets most likely to pay a new security premium for reliable US supply.

(Source: Yahoo Finance)

- If this trend holds: Watch for a continued wave of long-term offtake agreements signed with second-wave U.S. LNG developers, even as construction costs rise. The urgency to secure non-Middle Eastern supply will outweigh near-term price considerations.

- A key signal to monitor: The pricing differential in the secondary market between U.S.-origin and Middle East-origin LNG cargoes. A sustained premium for U.S. cargoes will confirm that the market has structurally de-risked away from the Persian Gulf.

- This could be happening: Major portfolio players and national oil companies may seek to acquire equity stakes in U.S. LNG infrastructure as a physical hedge against their exposure to Middle Eastern geopolitical risk, further accelerating investment in the U.S. Gulf Coast.

Frequently Asked Questions

Why did the 2026 conflict make US LNG more valuable than Qatari LNG?

The 2026 conflict disrupted the Strait of Hormuz, a critical chokepoint for all of Qatar’s LNG exports, forcing production to halt. This event transformed the geopolitical risk associated with Middle Eastern supply from a theoretical concern into a realized disruption. In contrast, US LNG export facilities on the Gulf Coast are geographically isolated from the conflict, ensuring reliable delivery. As a result, global buyers began to prioritize the security and reliability of US supply over Qatar’s lower production cost, creating a ‘security premium’ for US LNG.

How did the conflict impact global energy prices?

The disruption to Qatari supply caused a violent price shock in import-dependent regions like Europe, where natural gas prices surged by as much as 45%. Conversely, domestic natural gas prices in the United States remained stable, highlighting the insulation of the US market from the Middle Eastern conflict and increasing the economic attractiveness of its LNG exports.

What advantages does the US Gulf Coast offer as an LNG hub?

The US Gulf Coast’s primary advantage is its geographic isolation from major geopolitical chokepoints like the Strait of Hormuz. LNG cargoes from the Gulf of Mexico have diverse and secure maritime routes to key markets in both Europe and Asia. The 2026 conflict provided physical proof of this advantage, establishing the US Gulf Coast as the world’s preeminent hub for reliable LNG supply.

How is the US LNG industry able to meet the sudden increase in demand for secure supply?

The US is uniquely positioned due to its massive, pre-existing pipeline of LNG projects, which were projected to significantly increase export capacity by 2030. The crisis accelerated investment decisions (FIDs) for these projects. Furthermore, US developers are using advanced technologies like modular construction to lower costs, and integrating Carbon Capture (CCUS) and AI-driven operational optimization to improve efficiency and meet buyer demands for lower-carbon energy.

What is the ‘security premium’ on US LNG?

The ‘security premium’ refers to the higher value and willingness of buyers to pay more for US LNG contracts due to their proven reliability and insulation from geopolitical conflicts. After the 2026 conflict exposed the fragility of Middle Eastern supply chains, energy security became the top priority for importing nations. This means buyers are now willing to prioritize the integrity of their supply chain over securing the lowest possible production cost, a shift that directly benefits US suppliers.