Hydrogen Market 2026: Why Shell Abandoned Cars for Industrial-Scale Production

Hydrogen Adoption 2026: Shell’s Pivot from Retail Mobility to Industrial Decarbonization

The hydrogen market is undergoing a strategic realignment, with major energy firms like Shell pivoting from speculative, consumer-facing applications to concentrate on large-scale industrial decarbonization where demand is certain and commercially viable. This shift prioritizes supplying existing industrial assets, such as refineries, and building infrastructure for heavy-duty transport, marking a definitive move away from the light-duty passenger vehicle market.

- The period between 2021 and 2024 involved validating technology in diverse applications, exemplified by Shell’s launch of a 20 MW electrolyser in Zhangjiakou, China, partly to supply hydrogen for mobility during the Olympics. In stark contrast, March 2025 saw Shell execute a complete reversal in the passenger vehicle sector by permanently closing its entire network of hydrogen refueling stations in California, citing supply complications and other market-related factors.

- This strategic focus sharpened in January 2025 when Shell paused its green hydrogen pilot project at Brazil’s Port of Açu. The decision was driven by a need to reallocate capital to higher-return projects, signaling a reduced appetite for early-stage ventures in regions with less certain commercial frameworks.

- The company’s new focus is on leveraging its existing industrial footprint. The commissioning of the 200 MW Holland Hydrogen I plant in 2025 is a primary example, as its output will directly supply the Shell Energy and Chemicals Park Rotterdam to decarbonize its own refinery processes, creating a captive and reliable demand source.

- This industrial pivot extends to a re-evaluation of the mobility sector. An August 2025 partnership announcement with an automotive manufacturer, viewed in the context of the California exit, indicates a strategic focus on heavy-duty hydrogen trucks. This targets an industrial logistics market segment projected to grow at a CAGR of 43.7% through 2032.

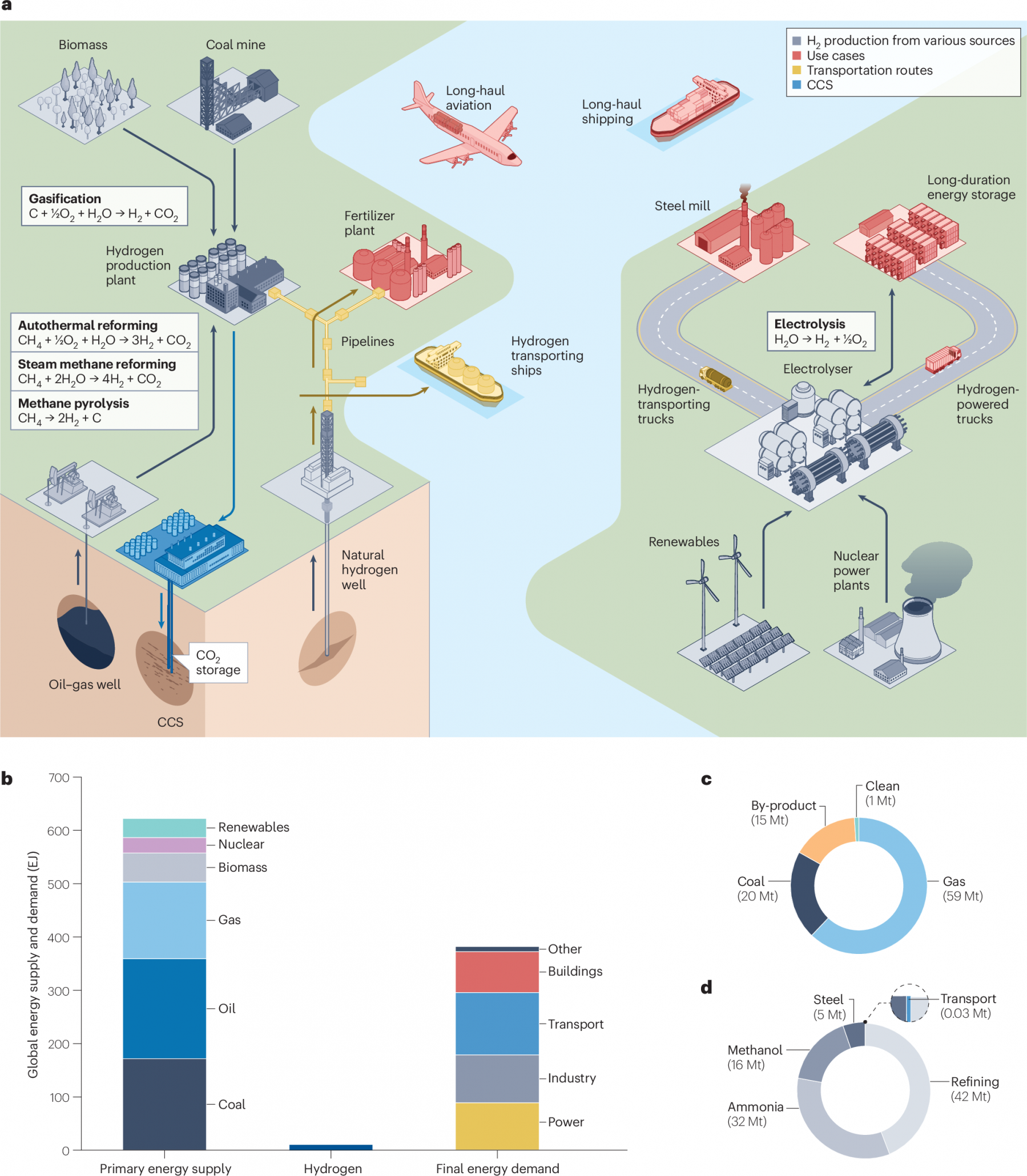

Industrial Demand Dwarfs Mobility Hydrogen Use

This chart validates Shell’s pivot by showing that industrial applications like refining represent the vast majority of hydrogen demand, while transport’s share is negligible. This data underscores the commercial logic of focusing on established industrial markets.

(Source: Nature)

Hydrogen Investment Signals: Shell’s 2025 Capital Realignment and Divestments

Shell‘s 2025 investment activity reveals a disciplined capital reallocation, systematically divesting from underperforming or speculative ventures to fund large-scale European green and blue hydrogen projects that offer clearer paths to profitability. This disciplined approach amid rising costs, supply chain challenges, and the need to solve the fundamental energy cost challenge for green hydrogen production underscores a pragmatic shift toward commercially secure investments.

- A primary divestment action was the March 2025 closure of Shell‘s hydrogen refueling station network for passenger cars in California. This move eliminated a capital-intensive and operationally complex business unit, allowing resources to be redirected toward industrial-scale projects.

- The investment portfolio was further streamlined in January 2025 with the suspension of the green hydrogen pilot in Brazil. This decision to prioritize projects like Holland Hydrogen I demonstrates a clear strategy of concentrating capital in mature markets with strong policy support and existing infrastructure.

- The cornerstone of its new investment strategy, the 200 MW Holland Hydrogen I project, became operational in 2025. This represents the successful deployment of significant capital into a revenue-generating asset designed to serve an immediate industrial need.

- Forward-looking investment is evident in the 100 MW electrolyser project at the Energy and Chemicals Park Rheinland in Germany. Securing critical power purchase agreements in November 2025 was a key de-risking milestone that moves the project closer to a final investment decision.

- Parallel to its green hydrogen investments, Shell continues to fund its Quest Carbon Capture and Storage (CCS) facility in Canada. This ongoing investment is crucial for enabling the company’s proprietary Shell Blue Hydrogen Process, providing a dual-track approach to producing low-carbon hydrogen.

Table: Shell’s 2025 Hydrogen Divestments and Paused Projects

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| California H 2 Station Network | March 2025 | Ceased operations at all light-duty passenger car hydrogen refueling stations. The move marked a definitive exit from the U.S. consumer hydrogen vehicle market to reallocate capital to industrial applications. | Hydrogen Central |

| Brazil Green Hydrogen Pilot | January 2025 | Paused the R&D pilot project at the Port of Açu. This decision was made to prioritize capital on higher-return European projects like Holland Hydrogen I amid rising global costs. | Fuel Cells Works |

Strategic Hydrogen Alliances: How Shell’s 2025 Partnerships Target Industrial Scale

In 2025, Shell’s partnering strategy shifted toward targeted collaborations designed to enable industrial-scale hydrogen ecosystems. The focus is on deploying proven technology and establishing infrastructure for heavy-duty transport, moving away from the more exploratory alliances that characterized the market in earlier years.

Visualizing Shell’s Hydrogen Logistics and Infrastructure

This image aligns with the section’s focus on partnerships for infrastructure by depicting Shell’s vision for a large-scale hydrogen distribution network. The branded tanker trucks represent the tangible outcome of strategic alliances for heavy-duty transport.

(Source: EnkiAI)

- The strategic collaboration agreement with global energy technology company SLB in December 2025 is aimed at developing digital solutions for the energy industry. For hydrogen, this partnership is expected to optimize large-scale production, storage, and associated CCS projects, enhancing efficiency and reducing operational costs for industrial-grade facilities.

- In August 2025, Shell Hydrogen announced a partnership with a leading automotive manufacturer to co-develop a hydrogen fueling station network. Given the company’s simultaneous exit from the passenger car market, this alliance is strategically aimed at building out infrastructure for the heavy-duty truck sector, a critical component of industrial decarbonization.

- These targeted 2025 partnerships contrast with the broader, more exploratory initiatives seen before 2024. The new focus is on creating commercially viable value chains with clear offtake partners, rather than simply proving technological feasibility in nascent markets.

Table: Shell’s Key Hydrogen Partnerships in 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| SLB | December 2025 | A strategic collaboration to develop and deploy new digital technologies for the energy industry. The goal is to accelerate innovations applicable to optimizing hydrogen production, storage, and CCS efficiency. | SLB |

| Unnamed Automotive Manufacturer | August 2025 | Partnership to co-develop a network of hydrogen fueling stations. The focus is presumed to be on heavy-duty trucks, aligning with the strategic pivot away from light-duty vehicles. | Market Research Future |

Hydrogen’s Geographic Shift: Why Europe Became Shell’s Core Focus in 2025

Shell‘s hydrogen strategy geographically consolidated in 2025, pivoting from a globally diversified exploratory approach to a concentrated investment in core European industrial hubs. This strategic consolidation in regions like the Netherlands and Germany reflects a broader trend where companies prioritize investments in stable jurisdictions with strong policy support and established industrial demand to de-risk against geopolitical shocks that could disrupt global LNG supply chains and energy markets.

- Between 2021 and 2024, Shell‘s hydrogen activities were more geographically dispersed, including the launch of a 20 MW electrolyser in China and exploratory R&D work for a pilot in Brazil. This represented an effort to gain first-mover experience in multiple key regions.

- A distinct geographic retreat became evident in 2025. The company paused its Brazilian pilot project in January 2025 and fully exited the U.S. consumer hydrogen market by closing its California station network in March 2025, signaling a withdrawal from less certain or profitable markets.

- Simultaneously, Europe emerged as the clear center of gravity for Shell‘s hydrogen ambitions. This was solidified by the commissioning of the 200 MW Holland Hydrogen I plant in the Port of Rotterdam in 2025 and the advancement of the 100 MW electrolyser project in Germany, which secured power deals in November 2025.

- Canada remains a key geography for Shell‘s blue hydrogen strategy, anchored by the operational Quest CCS facility. This highlights a technology-specific geographic focus, with investments directed to regions that possess the necessary infrastructure and supportive policies for either green or blue hydrogen production.

From Pilot to Production: Shell’s Hydrogen Technology Matures to Commercial Scale in 2025

By 2025, Shell‘s hydrogen strategy transitioned from validating technology at the pilot and demonstration scale to deploying commercially sized production systems. This maturation is confirmed by the commissioning of its 200 MW European flagship project and the active commercialization of its proprietary blue hydrogen technology, indicating a clear shift toward revenue generation and industrial market supply.

Electrolyzer Projects Trend Toward Massive Scale

This chart reflects the industry-wide maturation from pilot to production, contextualizing Shell’s own move to commercial-scale systems. The global pipeline’s shift towards very large-scale projects validates Shell’s strategic transition.

(Source: thyssenkrupp nucera)

- The period leading up to 2025, including the 2022 launch of the 20 MW Zhangjiakou plant in China, served to validate PEM electrolyser technology and build operational expertise at a significant, yet not fully commercial, scale.

- A major leap in scale occurred in 2025 with the 200 MW Holland Hydrogen I plant becoming operational. This ten-fold increase in capacity from the China project marks the transition from large-scale demonstration to an industrial-grade production asset capable of supplying a major refinery.

- This commitment to deploying mature technology at scale is reinforced by the plan for a 100 MW electrolyser in Germany. Securing power purchase agreements in 2025 moves this next large-scale project from concept to a concrete development phase.

- In the blue hydrogen sector, the continued operation of the commercial-scale Quest CCS facility provides the mature, proven carbon storage infrastructure required to deploy the Shell Blue Hydrogen Process. In 2025, Shell began actively marketing this proprietary process as a cost-effective, large-scale, low-carbon hydrogen solution for industrial clients.

SWOT Analysis: Shell’s Evolving Hydrogen Strategy in 2025

A SWOT analysis of Shell‘s hydrogen activities shows that in 2025, the company effectively leveraged its industrial integration strengths to de-risk major investments. It decisively addressed weaknesses in nascent consumer markets through divestments, although its large-scale projects remain exposed to policy shifts and the pace of third-party offtake development.

Table: SWOT Analysis for Shell’s Hydrogen Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Global footprint and existing refinery assets provide a basis for hydrogen projects. Early experience with a 20 MW electrolyser in China. | Industrial integration (using own refineries as anchor customers), proven CCS expertise (Quest), and a proprietary, marketable technology (Shell Blue Hydrogen Process). | The strategy shifted from leveraging a global footprint for exploration to leveraging specific industrial assets to de-risk large-scale projects by creating captive demand. |

| Weaknesses | Exposure to the unprofitable and slow-developing light-duty passenger vehicle market. Capital spread across speculative, early-stage pilots. | High capital dependency on a few very large projects. Heavy reliance on favorable policy frameworks and subsidies in Europe. | The weakness in the consumer mobility market was resolved through the decisive closure of the California station network, focusing capital on more certain industrial applications. |

| Opportunities | First-mover advantage in multiple markets (e.g., China, Netherlands). Exploration of hydrogen for mobility. | Achieve market leadership in core European industrial hydrogen hubs. Dominate the emerging heavy-duty hydrogen trucking infrastructure market. License proprietary blue hydrogen technology. | The opportunity in industrial hubs was validated and pursued aggressively, while the consumer mobility opportunity was abandoned in favor of a more focused, industrial-oriented heavy-duty transport segment. |

| Threats | Rising costs for renewable energy, global supply chain disruptions, and slow adoption of hydrogen vehicles by consumers. | Persistent cost and supply chain challenges (as evidenced by the Brazil pause). Intensifying competition from other energy majors (e.g., Air Liquide) building similar-scale projects. Risk of slow third-party offtake. | The threat of rising costs was mitigated by consolidating investments into fewer, higher-return projects. The competitive threat is now more direct and concentrated in the European industrial hydrogen market. |

2026 Hydrogen Outlook: What to Watch After Shell’s Industrial Pivot

The most critical signal to watch in 2026 will be the final investment decision (FID) for Shell‘s next wave of large-scale hydrogen projects, particularly the 100 MW German electrolyser. A positive FID would confirm that the company’s disciplined, industrial-focused strategy is not just a course correction but an accelerating, long-term commitment.

Electrolyzer Market Forecasts Explosive Future Growth

This projection supports the 2026 outlook by showing the immense market potential for electrolyzers, the core technology in Shell’s next wave of projects. The forecast highlights the significant value at stake in future investment decisions.

(Source: Persistence Market Research)

- If the FID for the 100 MW German electrolyser is confirmed, watch for announcements of additional projects in other European industrial clusters, which would signal an intent to replicate and expand its hydrogen hub model.

- If Shell announces significant, long-term offtake agreements with third-party industrial customers for output from Holland Hydrogen I, this could mean that the commercial model for large-scale renewable hydrogen is validated beyond captive, internal use.

- If the August 2025 automotive partnership translates into a concrete deployment plan for a heavy-duty truck fueling network, watch for details on the timeline and scale, as this would clarify Shell‘s new, focused strategy for re-entering the hydrogen mobility sector.

- If the first commercial licensing agreement for the Shell Blue Hydrogen Process is signed with an external company, this could mean the technology is gaining market acceptance as a competitive, large-scale solution for producing low-carbon hydrogen.

Frequently Asked Questions

Why did Shell close its hydrogen refueling stations for cars in California?

Shell closed its California hydrogen refueling stations in March 2025 due to a combination of supply complications and other market-related factors. The move marked a strategic decision to exit the unprofitable and slow-developing passenger car market to reallocate capital toward large-scale industrial hydrogen projects with more certain demand.

What is Shell’s new hydrogen strategy focused on instead of cars?

Shell’s new strategy is focused on large-scale industrial decarbonization. This includes using hydrogen to decarbonize its own refineries (creating a captive demand) and developing infrastructure for the heavy-duty transport sector, such as hydrogen-powered trucks, which is seen as a more commercially viable market.

What are the major projects that highlight Shell’s new industrial focus?

The flagship project is the 200 MW Holland Hydrogen I plant, which became operational in 2025 to supply Shell’s refinery in Rotterdam. The company is also advancing a 100 MW electrolyser project in Germany and continues to operate its Quest Carbon Capture and Storage (CCS) facility in Canada to support its blue hydrogen production.

Why did Shell shift its geographic focus primarily to Europe?

Shell concentrated its investments in European industrial hubs like the Netherlands and Germany because these regions offer strong policy support, established industrial demand, and existing infrastructure. This makes large-scale projects less risky compared to regions with less certain commercial frameworks, leading Shell to pause projects in other areas like Brazil.

Is Shell only pursuing green hydrogen, or does it also have a blue hydrogen strategy?

Shell is pursuing a dual-track strategy involving both green and blue hydrogen. While it is building large-scale green hydrogen projects in Europe, it is also actively commercializing its proprietary Shell Blue Hydrogen Process. This process is supported by its investment in the commercial-scale Quest Carbon Capture and Storage (CCS) facility in Canada.