Clean Energy Manufacturing US Policy Risk, $18.6 B in Cancellations, and 21 GW of Capacity Abandoned (2025-2026)

US Policy Reversal, US Clean Energy Risks from the OBBBA Act

The primary risk to the global clean energy sector is not technological but political, with the 2025 “One Big Beautiful Bill Act” (OBBBA) in the United States creating a market crisis by dismantling the financial incentives of the Inflation Reduction Act (IRA). Prior to 2025, the IRA fueled a domestic manufacturing and deployment boom. The subsequent policy reversal has triggered widespread financial fallout, shifting the central challenge from managing growth to surviving a policy-induced market collapse.

- Before January 1, 2025, the IRA’s tax credits spurred massive investment announcements in US-based clean energy manufacturing and deployment, aiming to build a secure domestic supply chain.

- After the OBBBA was signed into law on July 4, 2025, the landscape inverted, with the act initiating an aggressive rollback of key incentives. This includes the termination of the Section 25 D residential clean energy credit and the Section 45 X advanced manufacturing credit after December 31, 2025, creating a severe investment cliff.

- The immediate impact was catastrophic. In Q 1 2025 alone, projects valued at nearly $8 billion were canceled or downsized. By mid-2025, total project cancellations exceeded $22 billion, illustrating a rapid collapse in investor confidence.

- This policy whiplash undermines the strategic goal of energy security, leaving the US increasingly dependent on Chinese supply chains, which already account for over 80% of solar panel manufacturing.

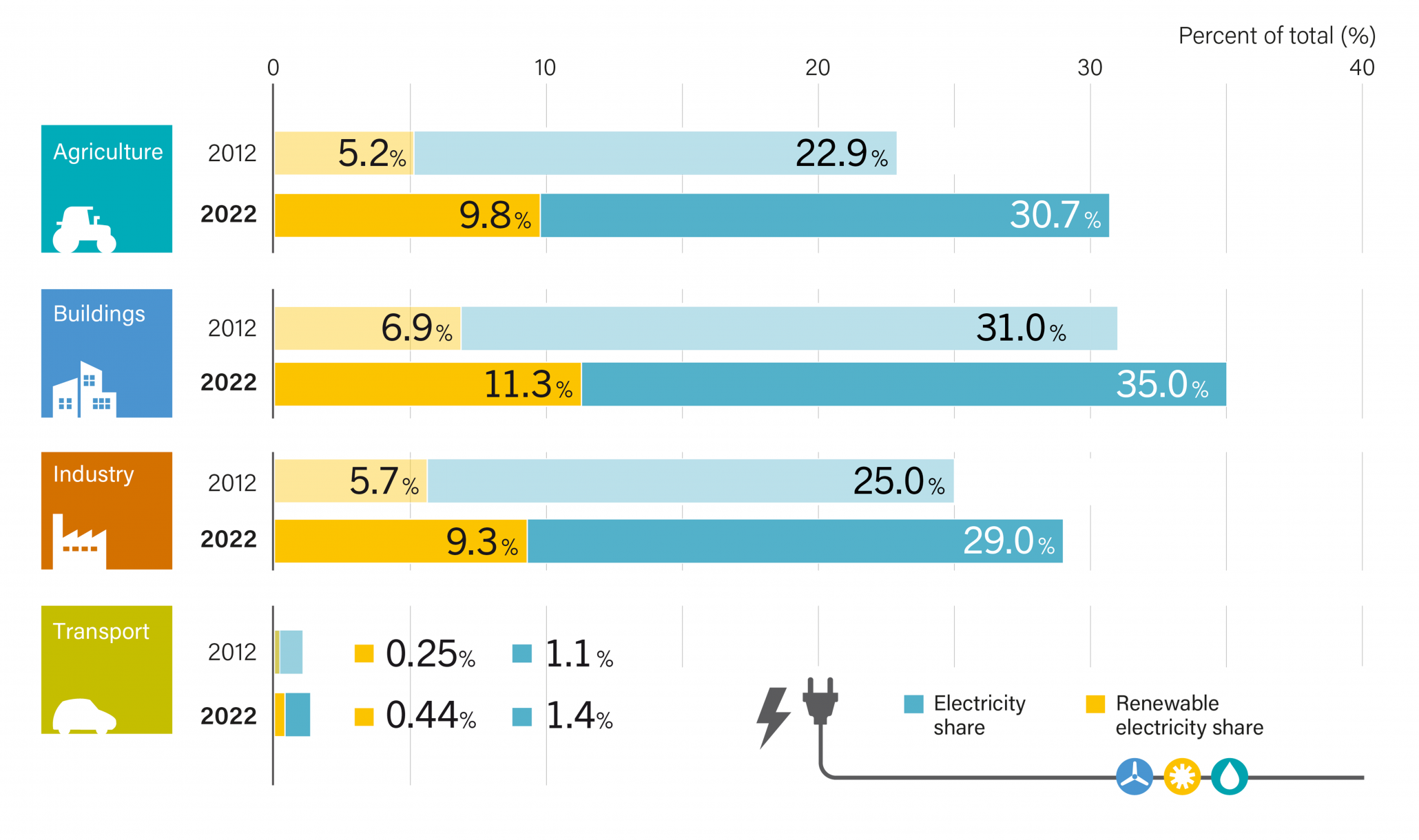

Renewable Electricity Share Increased Through 2022

This chart illustrates the positive historical momentum in renewable energy adoption, highlighting the progress that is now at risk due to the policy reversal discussed in the section.

(Source: REN21)

$22 B in Cancellations, US Clean Energy Investment Freezes (2025 to 2026)

The direct financial impact of the OBBBA has been immediate and severe, leading to the cancellation of tens of billions of dollars in planned investments and a net loss of expected jobs in 2025. The data shows a 3-to-1 ratio of abandoned investment for every new dollar announced in 2025, signifying a rapid and deep freeze in capital deployment for the US clean energy sector.

- Total clean energy investment cancellations in the US exceeded $22 billion through mid-2025, a direct consequence of the removal of IRA incentives.

- The year 2025 saw a net loss of over 15, 000 expected clean energy jobs, as project reversals creating 38, 031 job losses far outweighed new announcements.

- US renewable energy M&A deal value fell 41% in the first nine months of 2025 compared to the previous year, reflecting deep investor uncertainty.

- The project pipeline has also been severely impacted. More than 8 GW of clean power capacity was canceled in Q 1 2026 alone, bringing total cancellations since the start of 2025 to over 21 GW and exacerbating the existing backlog of projects awaiting grid connection.

Global Clean Energy Supply Glut in 2025

A global supply glut creates downward pressure on prices and profitability, providing a strong macroeconomic rationale for the US investment freezes and project cancellations detailed in the section.

(Source: The Economic Times)

Table: US Clean Energy Project and Funding Cancellations (2025-2026)

| Time Frame | Metric | Value | Details and Strategic Purpose | Source |

|---|---|---|---|---|

| Q 1 2026 | Canceled Capacity | >8 GW | Brings total cancellations since the start of 2025 to over 21 GW, reflecting sustained negative momentum following the OBBBA implementation. | EDF |

| Full Year 2025 | Net Job Impact | -15, 126 jobs | Project reversals (38, 031 jobs lost) far outweighed new announcements (22, 905 jobs created), showing a net contraction in the workforce. | E 2 |

| Full Year 2025 | Investment Ratio | 3-to-1 | Three dollars of clean energy investment were abandoned for every one dollar announced, indicating a massive capital retreat. | The Guardian |

| Through mid-2025 | Canceled Investment | >$22 Billion | Businesses closed, canceled, or cut back projects, wiping out a significant portion of the planned domestic manufacturing expansion. | RMI |

| Q 1 2025 | Canceled Investment | ~$8 Billion | The initial wave of cancellations following the policy shift, including $6.9 billion from six major projects from firms like KORE Power and Freyr. | Utility Dive |

US vs. China, US Clean Energy Geographic Fragmentation

The US policy reversal creates a stark geographic divergence, crippling its domestic manufacturing ambitions and increasing reliance on Chinese supply chains, while the EU and other regions are forced to recalibrate their own industrial strategies. While global manufacturing oversupply, driven by China, has reduced hardware costs, the US is unable to capitalize on this trend due to its self-inflicted policy crisis. This leaves major US developers like Next Era navigating extreme market uncertainty.

- China maintains its dominant position, accounting for over 80% of solar module production and at least 60% of manufacturing capacity across most clean technologies. This oversupply, from firms like LONGi Solar and Jinko Solar, is the primary driver of the global price collapse.

- The European Union is caught between Chinese oversupply and the US policy shift, responding with defensive measures like the Net-Zero Industry Act to protect its own nascent manufacturing base from being hollowed out.

- In stark contrast, other regions are accelerating their clean energy ambitions. India is pursuing ambitious energy storage targets, while Middle Eastern players such as Aramco and Altaaqa are making significant investments in solar and renewable infrastructure.

- The US market, once a leader in demand and investment, has become a significant source of global risk, with its policy instability creating ripple effects for international supply chains and investment strategies.

China Dominates Renewable Energy Manufacturing

This chart directly supports the section’s ‘US vs. China’ theme by quantifying China’s dominance in the renewable energy manufacturing supply chain, a key point of geopolitical and economic comparison.

(Source: The Economic Times)

Stranded Assets, US Clean Energy Technology Deployment Stalls

The market crisis is stranding commercially mature technologies like solar PV and wind (Technology Readiness Level 9) by removing their economic viability, while simultaneously creating a more hostile environment for emerging technologies to reach scale. The core issue is no longer technological readiness but the absence of a stable financial and policy framework to support deployment, a problem affecting both established and innovative solutions.

- Between 2021-2024, the focus was on scaling TRL 9 technologies, with the IRA providing the financial pull needed for massive deployment. Companies were investing heavily in manufacturing facilities based on these proven technologies.

- From 2025 onward, the OBBBA has rendered many of these projects uneconomical, turning recently announced factories and planned deployments into potential stranded assets. Solar is already the cheapest energy source in history, but without supportive policy, its cost advantage is neutralized.

- This creates a more difficult pathway for emerging technologies. Innovations like perovskite solar cells and sodium-ion batteries, which promise higher efficiencies and reduced reliance on critical minerals, now face a much higher barrier to commercialization in the US.

- As a result, investment is shifting away from capital-intensive manufacturing and toward less policy-dependent adjacent opportunities, such as AI for grid optimization and energy-as-a-service (Eaa S) models that leverage low-cost hardware without manufacturing risk.

Renewables Cannibalize California Power Prices in 2026

This chart provides a specific example of a dynamic that leads to ‘Stranded Assets’ and stalls deployment. Price cannibalization in a major market like California demonstrates the economic challenges facing renewable projects.

(Source: LinkedIn)

SWOT Analysis, US Clean Energy Policy-Driven Strengths and Weaknesses

The sector’s strategic profile has inverted since 2025, with former strengths like strong policy support becoming critical weaknesses, and external threats from Chinese oversupply now compounded by domestic political hostility. The period under the IRA represented a concerted effort to build domestic strengths, while the period under the OBBBA has exposed and magnified deep-seated vulnerabilities.

- Strengths have shifted from policy-driven manufacturing incentives to inherent technological maturity and the falling global cost of hardware.

- Weaknesses are now dominated by extreme policy uncertainty in the US, which has become the single largest barrier to investment and deployment.

- Opportunities are moving toward business models that can operate in a volatile environment, such as grid management software and corporate power purchase agreements (PPAs), especially from power-hungry data centers.

- Threats have intensified, with the risk of a Chinese supply chain monopoly now appearing more likely as US and European manufacturers face financial ruin.

US Clean Energy Share Reached 42% in 2024

The achievement of a 42% clean energy share represents a key ‘Strength’ for the US market, providing an essential data point for the SWOT analysis presented in this section.

(Source: LinkedIn)

Table: SWOT Analysis for US Clean Energy Market Shift

| SWOT Category | 2021 – 2024 (IRA Era) | 2025 – Today (OBBBA Era) | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong federal policy support (IRA); robust tax credits (45 X, 25 D); surging domestic investment announcements. | Mature TRL 9 technology; globally low hardware costs due to oversupply; strong corporate demand (e.g., data centers). | Strengths shifted from policy-driven to market-driven fundamentals, which are now being undermined by the removal of policy. |

| Weaknesses | Supply chain bottlenecks (transformers, minerals); long grid interconnection queues; nascent domestic manufacturing base. | Extreme policy and regulatory uncertainty; termination of key tax credits; collapsing investor confidence and project cancellations ($22 B+). | Pre-existing structural weaknesses have been massively amplified by the new, overarching weakness of hostile federal policy. |

| Opportunities | Building a resilient domestic supply chain; onshoring manufacturing; leading the global energy transition. | AI for grid optimization; energy-as-a-service models; battery recycling; green hydrogen production using cheap renewable electricity. | Opportunities have pivoted from manufacturing to services and software that are less exposed to capital investment and policy risk. |

| Threats | Geopolitical tensions with China; reliance on foreign supply chains; commodity price volatility. | Financial collapse of US/EU manufacturers; increased dependence on China; stranded assets from canceled projects. | The primary threat is now internal (policy-driven market collapse) compounding the external threat of Chinese market dominance. |

Key Catalysts to Watch, US Clean Energy Future Scenarios for 2026

The forward outlook for the US clean energy market hinges almost exclusively on political and regulatory stability, with investors closely monitoring any modification of the OBBBA, China’s export policies, and the EU’s defensive trade and industrial actions. The market’s trajectory is no longer about technological innovation but about political risk mitigation.

- If the OBBBA framework remains unchanged or is expanded, watch for further project cancellations, bankruptcies among non-Chinese manufacturers, and a deepening of US reliance on imported clean energy components.

- The most critical signal to monitor is any shift in US federal policy. A future administration could potentially reverse course, but the damage to investor confidence and the manufacturing investment cycle will take years to repair.

- A key catalyst would be China’s response to its own oversupply. Any move to rationalize domestic production or alter export rebates could significantly change global price dynamics, either alleviating or worsening the pressure on Western manufacturers.

- Also critical is the European Union’s strategy. If the EU implements strong trade defenses and robust domestic industrial support, it could create a viable, albeit high-cost, alternative to Chinese dominance, offering a potential lifeline for a non-Chinese supply chain.

Global Energy Storage Capacity Surges in 2024

The surge in energy storage capacity is a critical ‘Key Catalyst to Watch,’ as it enables greater renewable integration and will fundamentally shape the future deployment scenarios discussed in the section.

(Source: REN21)

The questions your competitors are already asking

This report covers one angle of the clean energy investment collapse following the 2025 repeal of the Inflation Reduction Act. The questions that matter most depend on your work.

- What is the outlook for US clean energy manufacturing deployment through 2026 after the repeal of the Section 45X credit?

- What is the status of the $22 billion in US clean energy manufacturing projects canceled since the OBBBA Act of 2025?

- Which overseas solar manufacturers are gaining US market share as domestic production plans are abandoned?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.