Solar PV Grid Risk: 68 GW Export Flood, 35 GW Curtailment, and Rising PPA Prices (2026)

Grid Integration as Primary Risk, Jinko Solar 68 GW Export vs. Stranded Asset Warnings

The primary constraint to solar adoption has shifted from upstream panel manufacturing to downstream grid infrastructure, creating a market paradox where cheap, abundant modules collide with transmission bottlenecks and financial risk. While a geopolitical crisis in West Asia during March 2026 created a security-driven demand for renewables, the global energy system’s ability to absorb them is now the central challenge. The defining issue is no longer module supply but the physical capacity to connect new projects and the financial models to de-risk them.

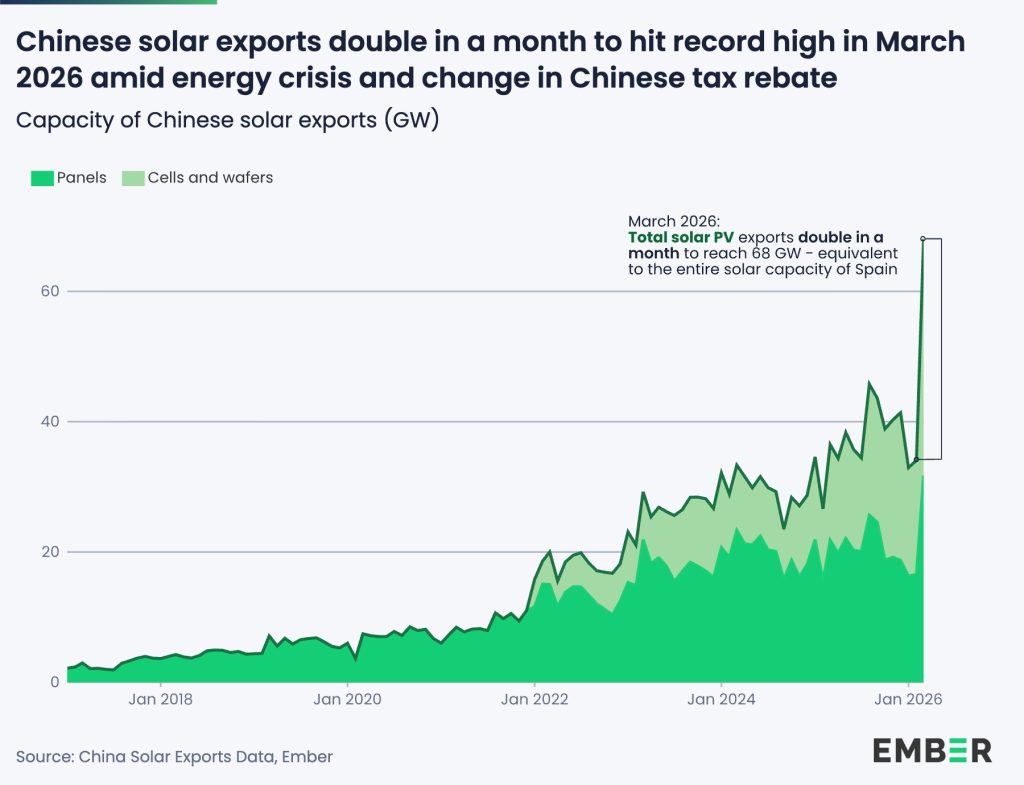

- Before 2025, the industry focused on scaling production and reducing the levelized cost of energy. In Q 1 2026, that success created a new problem: a flood of low-cost panels, exemplified by China’s record 68 GW of solar exports in March, is overwhelming unprepared grids.

- This market imbalance has led financial institutions like Barclays to issue warnings in March 2026 about the rising threat of “stranded assets”, where renewable projects are rendered obsolete because they cannot secure a grid connection.

- The risk is not theoretical. In India, a CRISIL Ratings report from March 2026 estimates that over 35 GW of renewable energy capacity is at risk of grid curtailment by fiscal year 2027 due to slower-than-needed deployment of transmission infrastructure.

- Analysis from the CERAWeek conference in March 2026 confirmed this system-level shift, identifying transmission and grid integration, not generation technology, as the new primary bottlenecks in the energy transition.

Chinese Solar Exports Hit Record 68 GW

This chart directly visualizes the record-breaking 68 GW of solar exports mentioned in the section’s heading, illustrating the supply-side glut that challenges global grid infrastructure.

(Source: Electrek)

$920 M in Financing, Arevon Nighthawk Project Highlights Storage Co-location Need

Investment is flowing not just to solar generation but increasingly towards critical enabling infrastructure like battery storage, a direct market response to grid instability and the need to absorb intermittent renewables. The major financing deals of Q 1 2026 show that securing project viability now requires solving for grid services, not just delivering low-cost electrons.

- In March 2026, large-scale financing shifted decisively toward projects that pair solar with storage. This trend directly addresses the grid’s inability to manage massive influxes of solar power alone.

- Arevon closed $920 million in financing for its 1, 200 MWh Nighthawk Energy Storage Project in California. This large-scale battery is designed specifically to enhance grid reliability in a market saturated with solar.

- Similarly, Octopus reached a $900 million financial close for its Blind Creek project in Australia, a major solar and battery facility that moved forward only after securing a critical offtake agreement.

- The market logic was further confirmed by Clenera, which signed twenty-year offtake agreements with utility Idaho Power for two projects, with the contracts explicitly covering both the solar output and the storage components.

Table: Major Renewable Project Financing with Grid-Enabling Components (March 2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Arevon / Nighthawk Project | Mar 11, 2026 | Closed $920 million in financing for a 1, 200 MWh energy storage project in California, designed to provide grid stability and manage solar intermittency. | Yahoo Finance |

| Octopus / Blind Creek Project | Mar 17, 2026 | Reached financial close on a $900 million solar and battery project in Australia, proceeding to construction after securing an offtake agreement. | Energy Storage News |

| Clenera / Two Idaho Projects | Mar 19, 2026 | Signed 20-year offtake agreements with Idaho Power for both solar output and storage components, signaling utility demand for integrated grid solutions. | Index Box |

| Zelestra | Mar 17, 2026 | Secured 1.5 TWh under Italy’s Energy Release 2.0 program, part of a strategy to build 3 GW of capacity by the end of 2026, requiring grid integration at scale. | Renewable Energy Magazine |

US vs. India, Jinko Solar Exports Expose Divergent Regional Grid Constraints

The global influx of solar panels is revealing starkly different regional bottlenecks, with developed markets like the U.S. facing rising power purchase agreement prices due to project backlogs while developing markets like India face direct grid curtailment.

- In North America, the primary problem is a mismatch between module availability and project viability. A March 2026 analysis from k Wh Analytics shows Power Purchase Agreement (PPA) prices are rising because the supply of financeable, grid-connected projects is outstripped by demand.

- The strain on the U.S. grid is compounded by new, massive sources of electricity demand. AI data centers are projected to consume 1, 000 TWh globally by 2026, placing unprecedented stress on transmission and distribution systems.

- In India, the issue is more direct and immediate. Over 35 GW of renewable capacity is at high risk of having its power generation curtailed by 2027 simply because the transmission lines required to carry the electricity are not being built fast enough.

- In response to energy security concerns, the European Union has adopted protectionist measures, including a 100% tariff on Chinese clean tech, which complicates supply dynamics without solving the underlying infrastructure deficit.

Jinko Solar’s Mature Tech, Cost per Watt Is Solved, Grid Integration Is Not (2026)

Solar PV module technology is commercially mature and hyper-efficient at the production level, but the broader energy system required to support it at scale is lagging. This makes grid integration technology, policy, and financing the new frontiers for innovation and investment.

- Through 2024, the primary technology race was in the factory, focused on improving cell efficiency and lowering the cost per watt. Chinese firms like LONGi Green Energy and Jinko Solar achieved leadership through aggressive R&D and economies of scale.

- In 2026, this upstream maturity has created the downstream crisis. The technology challenge has shifted to grid-forming inverters, advanced energy storage solutions, dynamic line rating, and high-voltage transmission hardware.

- Even as US-based companies like Tesla aim to build domestic manufacturing capacity, the fundamental reliance on established supply chains for equipment and technology underscores the maturity of the upstream sector.

- The market’s focus has expanded from the panel to the entire ecosystem of grid management. The LCOE of a semi-transparent PV system may be as low as €0.095/k Wh, but that cost is irrelevant if the power cannot reach customers.

2027 Outlook: Jinko Solar PPA Prices Hinge on Transmission, Not Panel Cost

For the next 12 to 18 months, solar project viability will be determined less by module cost and more by the speed of interconnection approvals and transmission build-outs. The market has an abundance of cheap solar panels; it is starved of the infrastructure needed to deploy them effectively.

- If grid interconnection queues remain congested at current levels, watch for an increase in project cancellations and a potential slowdown in new utility-scale announcements in late 2026 and early 2027, regardless of module price drops.

- If regulators and utilities in key markets like the U.S. and E.U. successfully implement reforms to fast-track grid modernization and permitting, these could be happening: a stabilization of PPA prices as the backlog of viable projects clears, finally allowing developers to capitalize on low module costs.

- The most critical lead indicator for the solar market’s health is no longer the spot price of polysilicon or modules. Instead, investors and strategists must monitor the quarterly change in interconnection queue times and the volume of new transmission projects receiving financing and permits.

The questions your competitors are already asking

This report covers one angle of the global solar market’s pivot from a manufacturing challenge to a grid integration and financial risk crisis. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the new market for solar grid integration and financial risk mitigation?

- What is the outlook for utility-scale solar deployment and PPA pricing, considering the rising risk of grid curtailment and stranded assets?

- What are the opportunities for grid-enhancing technologies and energy storage in markets facing an oversupply of solar modules?

- Which project developers and financiers are successfully adopting new models to de-risk solar assets against transmission bottlenecks?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.