US Grid Strain 2026: Why Data Center Demand Fuels a Gas & Nuclear Revival Over Offshore Wind

The Great Divide: How Data Center Growth Splits US Energy Strategy in 2026

Explosive electricity demand from data centers is forcing a clear strategic divergence among U.S. utilities, with many, like Southern Company, prioritizing firm, dispatchable power over intermittent renewables such as offshore wind. Instead of investing in offshore wind projects, these utilities are channeling billions into new natural gas generation and nuclear power to guarantee the 24/7 reliability required by hyperscale computing facilities. This marks a significant shift from the 2021-2024 period, where national clean energy goals heavily favored renewable development, to a 2025-2026 reality where grid reliability and speed-to-market for new generation capacity are the dominant drivers.

- In the period from 2021 to 2024, the national conversation focused on achieving the 30 GW by 2030 offshore wind target, with utilities in the Northeast forming major joint ventures to develop multi-gigawatt projects.

- The 2025-2026 period revealed a starkly different reality, as the U.S. offshore wind industry faced over $114 billion in canceled or delayed investments due to supply chain constraints, inflation, and political headwinds.

- In direct contrast, Southern Company responded to a committed load of 10 GW from new data centers by securing a landmark $26.54 billion loan from the U.S. Department of Energy (DOE) in early 2026, explicitly for building 5 GW of new natural gas plants and upgrading 6 GW of nuclear capacity.

- While competitors like Dominion Energy are proceeding with capital-intensive projects like the $10.7 billion Coastal Virginia Offshore Wind (CVOW) farm, Southern Company’s actions demonstrate a deliberate strategic choice to avoid the offshore wind market’s volatility in favor of proven, dispatchable technologies.

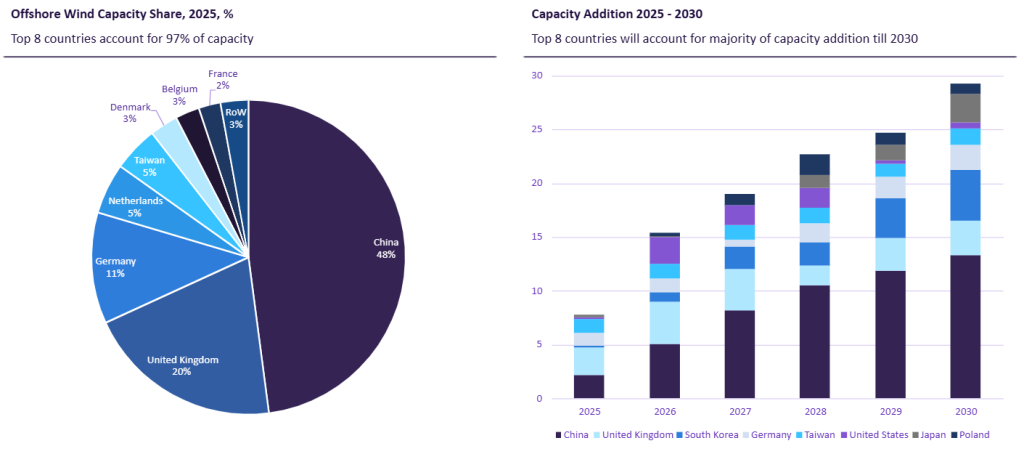

US Lags in Global Offshore Wind

This chart shows the US’s minimal contribution to global offshore wind capacity, contextualizing why some domestic utilities are hesitant to invest in a sector dominated by China and the UK.

(Source: Investment Monitor)

Investment Schism: Capital Flows to Gas and Nuclear as Offshore Wind Falters

Financial commitments in 2025 and 2026 confirm that capital is flowing towards technologies that ensure grid stability rather than intermittent sources. Southern Company’s financial strategy, highlighted by a massive federal loan and an increased five-year capital expenditure plan, is firmly anchored in developing its natural gas and nuclear portfolio. This allocation stands in sharp relief against the financial turmoil and project cancellations plaguing the U.S. offshore wind sector, indicating that investors and utilities with significant near-term demand growth are de-risking their generation strategies.

- Southern Company raised its five-year capital expenditure plan for 2026-2030 to $81 billion, a 7% increase, specifically to accommodate the “watershed” moment of economic development and data center growth in the Southeast.

- The company’s acceptance of the $26.54 billion DOE loan package in 2026 is the single largest indicator of its strategic direction, with funds explicitly designated for non-wind assets that provide firm power.

- This contrasts with the offshore wind sector, which saw major projects like Leading Light Wind in New Jersey get canceled in November 2025, contributing to an estimated $114 billion in stalled or abandoned investments.

- Even as some projects like Empire Wind 1 and Revolution Wind resumed construction in February 2026, the broader market sentiment remains cautious, a risk that utilities like Southern Company are choosing to avoid.

Table: Energy Investment Divergence, 2025-2026

| Company / Sector | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Southern Company | Feb 2026 | Raised five-year (2026-2030) CAPEX plan to $81 billion to fund grid modernization and new generation, primarily gas and nuclear, to meet data center demand. | MSN |

| Southern Company | Feb 2026 | Accepted a $26.54 billion DOE loan to build 5 GW of new gas generation and upgrade 6 GW of nuclear power. | Power Mag |

| U.S. Offshore Wind Industry | Oct 2025 | Suffered $114 billion in canceled or delayed project investments due to economic and political challenges, severely impacting near-term capacity goals. | Yale E 360 |

| Dominion Energy | 2025-2026 | Continued construction of the $10.7 billion, 2.6 GW Coastal Virginia Offshore Wind (CVOW) project, highlighting the high cost of entry that other utilities are avoiding. | Virginia Business |

| Invenergy / energy RE | Nov 2025 | Canceled the Leading Light Wind project off the coast of New Jersey, citing unfavorable market conditions. | Jersey Shore Online |

Partnership Focus: Development JVs vs. Technology Enablers

Partnership structures reveal the different strategic priorities, with offshore wind leaders forming direct joint ventures for project development, while Southern Company engages in collaborations that enhance its existing asset base or provide indirect market visibility. Before 2025, major utilities were aggressively forming JVs to bid on offshore lease areas. Now, while those partnerships persist, companies like Southern Company are focusing on technology-centric alliances, such as using AI for permitting or investing in venture capital, to gain insights without direct capital risk in volatile markets. This contrasts with companies like Shell, which have formed direct JVs for project development.

- In 2025, active offshore wind developers like National Grid and RWE created Community Offshore Wind, a joint venture to develop projects in the New York Bight, continuing a trend of direct development partnerships.

- Similarly, Holcim and BW Ideol formed a strategic partnership in January 2026, with Holcim taking an equity stake to advance floating offshore wind foundation technology.

- Southern Company’s primary partnership remains its role as a founding partner in Energy Impact Partners (EIP), a venture capital fund that gives it broad exposure to emerging technologies without committing to specific large-scale projects.

- The company is also reportedly using AI to streamline permitting for large renewable projects, including CVOW, positioning itself as a technology provider to the industry rather than an equity partner in wind farm construction.

Geography of Power: Southeast Doubles Down on Thermal as Northeast Pursues Wind

A clear geographical fault line has emerged in U.S. energy strategy, with the Southeast, led by utilities like Southern Company, committing to thermal and nuclear generation, while the Northeast continues to be the epicenter of offshore wind development. The massive industrial and data center load growth in states like Georgia and Alabama is the primary driver for Southern Company’s focus on local, reliable power. This regional concentration of demand has led to a generation strategy tailored to the Southeast’s economic boom, distinct from the policy-driven renewable goals of the Atlantic Northeast.

Northeast Emerges as Offshore Wind Hub

This map details a specific offshore wind project plan off the New England coast, illustrating the regional concentration of wind development in the Northeast as described in the text.

(Source: The Vineyard Gazette)

- Between 2021 and 2024, federal lease auctions and state-level procurements established the coasts of New York, New Jersey, and Massachusetts as the core of the U.S. offshore wind industry.

- From 2025 onwards, the focus for Southern Company has been entirely on its Southeastern service territory, where it has already signed contracts for 10 GW of new load, almost all of which will be served by new gas and existing nuclear plants.

- The Georgia Public Service Commission’s approval of Georgia Power’s 2025 Integrated Resource Plan (IRP) solidified this regional strategy, authorizing major investments in coal, gas, and nuclear infrastructure without any provision for offshore wind.

- This contrasts with projects like South Coast Wind (Massachusetts) and Empire Wind (New York), which, despite challenges, remain geographically anchored to the Northeast’s grid and policy environment.

Technology Maturity: Proven and Dispatchable Trumps Intermittent and Volatile

Southern Company’s strategy is a clear vote for technological certainty, prioritizing the mature, dispatchable performance of natural gas and nuclear power over the still-evolving and economically volatile offshore wind sector. While the offshore wind industry makes progress on larger turbines and new foundation types, utilities facing immediate, massive demand from critical infrastructure like data centers are opting for technologies with proven reliability and established supply chains. The period from 2025-2026 has underscored the operational and financial risks of relying on a sector still grappling with scaling challenges.

- Before 2025, the industry anticipated a rapid scale-up of new technologies. The 2025-2026 reality has been one of supply chain bottlenecks and cost inflation that has hampered deployment.

- Southern Company’s focus on combined-cycle gas plants and nuclear license renewals leverages decades of operational expertise and predictable cost structures, minimizing construction and operational risk.

- In contrast, the offshore wind industry is advancing technologies like Vestas’ V 236-15.0 MW turbines and Entrion Wind’s FRP monopiles for deeper waters. While innovative, these are still being deployed at scale for the first time, introducing risk that Southern Company is avoiding.

- The AI-driven permitting acceleration mentioned in Southern Company’s strategy is a low-risk, high-leverage technological play, enhancing existing processes rather than building entirely new, capital-intensive asset classes.

SWOT Analysis: Southern Company’s Strategic Position on Offshore Wind Initiatives

An analysis of Southern Company’s strategy reveals a calculated decision to leverage its strengths in conventional power to capture a historic market opportunity, while consciously avoiding the threats currently destabilizing the offshore wind sector. This SWOT analysis contrasts the company’s position before and after the full impact of data center demand and offshore wind market turmoil became clear in 2025.

Table: SWOT Analysis of Southern Company’s Energy Generation Strategy

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strength | Operational expertise in large-scale nuclear (Vogtle) and gas fleet. A strong, regulated utility business model. | Secured a $26.54 B DOE loan and raised CAPEX to $81 B to build firm power. Deep relationships with large industrial customers. | The company validated that its core competency in large, centralized power projects is its primary strength for meeting massive new demand reliably. |

| Weakness | High capital expenditure on Vogtle nuclear units. Perceived as slower to adopt renewables compared to peers. | Increased carbon footprint with 5 GW of new gas generation. Long-term exposure to natural gas price volatility. | The massive data center demand forced a trade-off, prioritizing reliability over near-term decarbonization goals, reinforcing its carbon-intensive weakness. |

| Opportunity | General economic growth in the Southeast. Potential to expand solar portfolio. | Capturing 10 GW of committed, high-margin load from data centers and manufacturing. Leveraging AI to improve operational efficiency. | The “watershed” economic boom in the Southeast became a concrete, massive opportunity that overshadowed speculative investments in offshore wind. |

| Threat | Rising pressure from ESG investors and federal clean energy mandates to decarbonize faster. | Offshore wind market turmoil ($114 B in delays) and project cancellations (Leading Light Wind) validated a risk-averse strategy. Long-term regulatory risk on carbon emissions remains. | The immediate, systemic risk of the offshore wind market’s collapse validated Southern Company’s conservative stance, turning an external threat for others into a strategic justification. |

Scenario Modelling: The Firm Power Mandate for 2027 and Beyond

The most critical expectation for the year ahead is that utilities with significant data center load, led by Southern Company, will double down on their firm power strategy, accelerating gas and nuclear development while deferring any serious consideration of offshore wind until at least 2030. If the exponential growth in electricity demand from AI and data centers continues, watch for these utilities to actively lobby for streamlined permitting for thermal plants and begin formally evaluating next-generation nuclear, such as small modular reactors (SMRs), as the only viable long-term solution for providing carbon-free, 24/7 power.

North American Offshore Wind Market Forecast

This forecast projects strong long-term growth for the North American offshore wind market through 2033, providing crucial context for the article’s scenario modeling.

(Source: Market Data Forecast)

- Signal to Watch: Monitor the groundbreaking and construction timelines for the 5 GW of new natural gas plants funded by Southern Company’s DOE loan. Any acceleration will confirm the urgency of meeting the 10 GW of committed load.

- Signal to Watch: Track the allocation of Southern Company’s $81 billion CAPEX budget. A heavier-than-expected allocation to generation over transmission would indicate a priority to build power now, even at the expense of longer-term grid upgrades.

- What Could Be Happening: Utilities are likely engaging in private talks with SMR developers to assess commercial readiness post-2030, seeing it as the only technology that satisfies both decarbonization goals and the reliability demands of an AI-driven economy.

- Losing Steam: The narrative that intermittent renewables alone can power the future grid is losing traction among utilities with heavy industrial and data center loads. The focus has shifted from “megawatts” to “megawatt-hours” and reliability metrics, a domain where offshore wind currently struggles to compete with gas and nuclear without massive energy storage investments.

Frequently Asked Questions

Why is Southern Company choosing natural gas and nuclear over offshore wind for data centers?

Southern Company is prioritizing natural gas and nuclear power because data centers require a constant, 24/7 reliable power supply. These ‘firm’ energy sources can guarantee that level of reliability. In contrast, the article highlights that the offshore wind industry is currently volatile, facing over $114 billion in project delays and cancellations, making it a riskier choice for meeting the immediate and massive 10 GW of new demand from data centers in the Southeast.

Does this mean the push for U.S. offshore wind is over?

Not entirely, but it has significantly faltered. The article describes a ‘geographical fault line’ where the Northeast continues to pursue offshore wind projects like Empire Wind 1 and South Coast Wind, driven by state policies. However, the sector has faced major setbacks due to inflation and supply chain issues. Utilities in regions with high, immediate demand, like the Southeast, are avoiding the market’s volatility in favor of more predictable technologies.

What is the significance of the $26.54 billion DOE loan to Southern Company?

The $26.54 billion loan is a landmark event that confirms the strategic shift towards firm power. The funds are explicitly designated to help Southern Company build 5 GW of new natural gas generation and upgrade 6 GW of nuclear capacity. This federal backing validates the strategy of prioritizing grid reliability to support economic growth and shows a willingness to fund thermal and nuclear assets to meet urgent demand.

Is every U.S. utility following Southern Company’s strategy?

No, the article points to a ‘strategic divergence.’ While Southern Company is leading the move towards gas and nuclear in the Southeast, other utilities like Dominion Energy are proceeding with major offshore wind projects, such as the $10.7 billion Coastal Virginia Offshore Wind farm. The choice of strategy appears to be regional, heavily influenced by the specific scale and urgency of new demand, like the data center boom in Southern Company’s territory.

How does this shift impact the U.S. goal of a cleaner energy grid?

It creates a short-term trade-off. By investing in 5 GW of new natural gas, Southern Company is increasing its carbon footprint to guarantee grid reliability. The article suggests that for utilities facing massive, immediate load growth, reliability has temporarily overshadowed decarbonization goals. However, the long-term plan may still involve clean energy, with the article noting that utilities might be looking at next-generation nuclear, like SMRs, as a future solution for carbon-free, 24/7 power.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.