European Airlines Carbon Costs, €1.5 B+ Exposure for Lufthansa, 15 CEO Opposition, and EU ETS Expansion (2025 to 2026)

Carbon Cost Exposure, European Airlines Face €1.5 B+ Risk from ETS Expansion

The European aviation sector is confronting a structural change in its cost base as carbon emissions shift from a peripheral compliance item to a core financial liability. This is driven by the legislated phase-out of free carbon allowances by 2026 under the EU Emissions Trading System (EU ETS) and a concurrent proposal to expand the system’s scope to all flights departing the European Union. This dual regulatory pressure is set to create substantial financial risk, fundamentally altering the competitive dynamics for all European carriers.

- Prior to 2025, the impact of the EU ETS was partly mitigated by a system of free allowances and a limited scope covering only intra-European flights. This framework effectively subsidized a large portion of the industry’s carbon costs, particularly for legacy carriers with extensive long-haul networks whose emissions fell largely outside the system’s reach.

- The market inflection point arrives in 2026, when the phase-out of free allowances becomes absolute, requiring airlines to purchase 100% of their required carbon allowances at market prices. This move alone directly exposes airline balance sheets to the full volatility of the carbon market.

- The most significant financial threat stems from the European Commission’s proposal to extend the EU ETS to cover all outbound international flights. Analysis from May 2026 shows this would expose each of the three largest legacy groups, Lufthansa, International Airlines Group (IAG), and Air France-KLM, to over €1.5 billion in additional annual costs.

- In response, chief executives from 15 of Europe’s largest airlines have collectively warned that the plan will penalize European passengers and create a competitive disadvantage, forcing a strategic re-evaluation of network planning, fleet acquisition, and long-term capital allocation.

ETS Expansion to Triple Airline Carbon Costs

This chart directly quantifies the ‘Carbon Cost Exposure’ and ‘€1.5 B+ Risk’ mentioned in the section heading. It explains the magnitude of the financial risk by showing that costs are expected to triple due to the ETS expansion.

(Source: Transport & Environment)

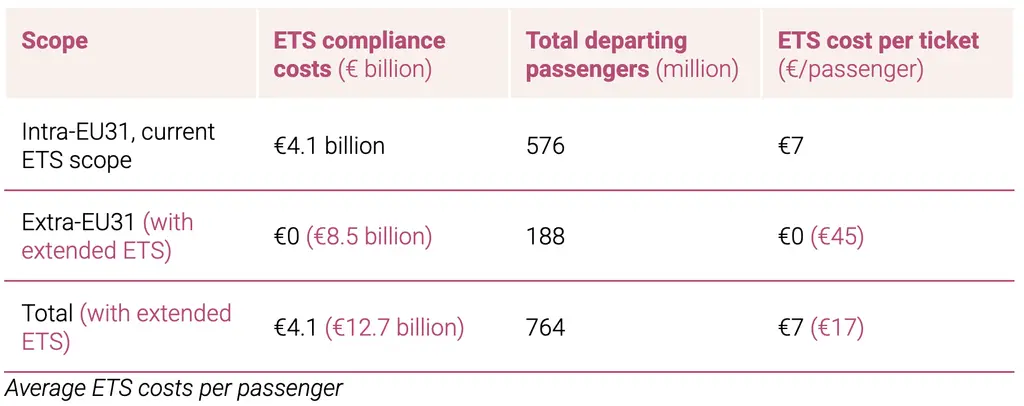

€8.5 B in Unpaid Emissions, European Airlines Brace for Rising Carbon Prices

Projected compliance costs are set to escalate as the EU tightens its regulatory framework, driven by rising carbon allowance prices and the closure of historical loopholes. The financial gap between emissions generated and costs paid is now closing, with the burden expected to be passed directly to consumers through higher ticket prices, fundamentally altering the economics of air travel.

- In 2025, European airlines left an estimated €8.5 billion in emissions costs unpaid due to the combined effect of free allowances and the limited scope of the ETS, which covered only 32% of emissions from departing flights.

- The effective carbon price paid by the industry in 2025 was just €23 per tonne, a stark contrast to the average EU ETS market price of €73 per tonne paid by other sectors, highlighting the scale of the previous subsidy.

- With the phase-out of free allowances from 2026, this price gap will disappear. Analyst forecasts project EU Allowance (EUA) prices will average €92.65 per metric ton in 2026, with consensus forecasts projecting a rise to €126/t CO₂ or even €145/t CO₂ by 2030.

- This cost increase is expected to add an average of €45 to long-haul ticket prices if the ETS expansion is approved, generating significant revenue for climate initiatives but also creating major headwinds for airline profitability and passenger demand.

Airlines Left €8.5B in Emissions Costs Unpaid

The chart’s headline directly corresponds to the section’s heading, ‘€8.5 B in Unpaid Emissions’. It provides the core financial figure that this section is built around, making it a perfect match.

(Source: Transport & Environment)

Table: EU Carbon Allowance (EUA) Price Forecasts (€/t CO₂)

| Forecast Provider | 2026 Forecast (€/t) | 2027 Forecast (€/t) | 2030 Forecast (€/t) | Source |

|---|---|---|---|---|

| Reuters Survey | €92.65 | €107.29 | N/A | Reuters |

| GMK Center | €85 | €100 | €126 | GMK Center |

| Bloomberg NEF | N/A | N/A | €122 | Bloomberg NEF |

| ABN AMRO | N/A | N/A | €145 | ABN AMRO |

| Enerdata | N/A | N/A | €70 | Enerdata |

EU vs Global Carriers, The Competitive Risk of EU ETS Expansion for Airlines

The European Commission’s proposal to unilaterally expand its carbon market creates a critical geopolitical and competitive friction point, pitting the EU’s regional climate ambitions against the established global framework for aviation emissions. This divergence risks creating an uneven playing field that could disadvantage EU-based carriers and lead to a rerouting of global air traffic to circumvent Europe’s carbon pricing zone.

- The current EU ETS framework applies only to flights within the European Economic Area, creating a relatively balanced competitive environment for carriers operating on those routes.

- Expanding the system to cover all flights departing the EU would establish a “carbon border, ” imposing significant costs on EU carriers that their international competitors operating from nearby non-EU hubs would not face on the same intercontinental routes.

- Industry bodies, led by the International Air Transport Association (IATA), warn this could trigger “carbon leakage, ” where passengers and cargo are rerouted through hubs in the UK, Turkey, or the Middle East to avoid the EU charges, shifting emissions without reducing them globally.

- Airlines are instead advocating for the global Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) to be the sole measure for international flights, but EU policymakers view its offsetting mechanisms as insufficient to drive the deep decarbonization required by the ‘Fit for 55’ package.

European Aviation Emissions Grew Faster Than Other Major Markets

This chart directly supports the ‘EU vs Global Carriers’ theme of the section. By comparing the emissions growth of Europe to other markets, it establishes the premise for the ‘Competitive Risk’ that the EU-specific ETS creates.

(Source: Transport & Environment)

European Airlines and SAF Mandates, The Only Escape from EU ETS Costs (2025 to 2026)

The EU ETS for aviation is rapidly maturing from a subsidized signaling mechanism into a powerful, full-cost carbon pricing tool, forcing airlines to shift focus from lobbying to operational mitigation. With rising compliance costs becoming unavoidable, fleet efficiency and the adoption of Sustainable Aviation Fuel (SAF) have emerged as the primary strategic battlegrounds for competitive survival and leadership.

- Between 2021 and 2024, the system’s impact was limited, with free allowances and a narrow scope failing to drive significant operational changes beyond what was already planned for fleet modernization.

- The period from 2025 to today is defined by a sharp increase in financial pressure as the 2026 deadline for the complete removal of free allowances approaches. The vocal opposition from airline CEOs validates the policy’s newfound financial severity.

- This forces a strategic pivot toward tangible decarbonization. Fleet efficiency is now a critical differentiator, giving carriers like Ryanair and Wizz Air, which operate younger, more fuel-efficient aircraft, a structural cost advantage.

- Ultimately, SAF remains the only viable near-term path to mitigate these escalating costs. However, with global SAF production expected to meet less than 1% of jet fuel demand in 2026, securing supply is a critical challenge and a key focus for airlines seeking to manage their future carbon exposure. These new fuel pathways are analogous to the growth of Renewable Natural Gas in ground transport.

Cleaner Aircraft Could Save Airlines €800 Billion

The section discusses SAF as an ‘Escape from EU ETS Costs’. This chart complements that topic by introducing another major capital-intensive solution—fleet modernization (‘Cleaner Aircraft’)—thus broadening the discussion on long-term cost mitigation strategies.

(Source: Transport & Environment)

SWOT Analysis, European Airlines’ €1.5 B Carbon Cost Exposure

European airlines possess strengths in their global network reach and brand recognition, but these are directly challenged by the weaknesses of aging fleet segments and the significant financial threat posed by the EU’s climate regulations. The opportunity for efficiency leaders to gain market share is clear, while the threat of margin compression and competitive displacement is a major risk for the entire sector.

EU Carbon Price Surged After 2017 Lows

A ‘SWOT Analysis’ section requires context on external threats. This chart’s depiction of a surging carbon price is a primary example of such a threat, providing a critical data point for the strategic analysis of carbon cost exposure.

(Source: Carbon Tax Center)

Table: SWOT Analysis for European Airline Carbon Cost Exposure

| SWOT Category | Strengths | Weaknesses | Opportunities | Threats |

|---|---|---|---|---|

| Legacy Carriers (Lufthansa, IAG, Air France-KLM) | Extensive global networks and premium brand recognition. Established hub-and-spoke models. | Higher reliance on older, less fuel-efficient wide-body aircraft for long-haul routes. High exposure to proposed ETS expansion. | Leverage scale to secure large, long-term SAF offtake agreements. Consolidate market share if smaller competitors falter. | Over €1.5 billion in additional annual costs per group from ETS expansion. Loss of competitiveness to non-EU carriers on long-haul routes. |

| Low-Cost Carriers (Ryanair, Wizz Air, easy Jet) | Young, highly fuel-efficient fleets with low emissions per passenger. Lean operational models. | Network focused on intra-European routes, which are already fully exposed to the EU ETS. Price-sensitive customer base limits ability to pass on costs. | Capitalize on structural cost advantage as carbon prices rise. Gain market share from less efficient competitors. | Full exposure to rising carbon allowance prices after 2026. Inability to hedge via long-haul routes outside the ETS. |

| Industry-Wide | Acts as a critical enabler of economic activity and connectivity for the EU. | Limited near-term alternatives to liquid jet fuel. SAF production is nascent and expensive (up to 5 x conventional jet fuel). | Accelerate fleet renewal to improve efficiency. Drive innovation in alternative fuels like Hydrogen and new technologies. | “Carbon leakage” to non-EU hubs. Rising ticket prices impacting passenger demand. Conflicting regulatory pressures (EU ETS vs. CORSIA). |

Aviation Emissions Largely Escape EU Carbon Pricing

This chart perfectly visualizes a central point for the ‘Table: SWOT Analysis’. The fact that emissions have historically escaped pricing is a key weakness and threat that would be detailed in the SWOT table, as this exemption is now ending.

(Source: Transport & Environment)

Scenario Modelling, European Airlines’ Response to the 2026 EU ETS Review

The single most critical variable for the European aviation industry is the outcome of the European Commission’s 2026 review of the ETS scope. An aggressive expansion will force radical network and pricing adjustments, whereas a compromise aligning more closely with global standards would allow for a more managed transition. The industry’s strategic response will be dictated entirely by this decision.

- If the EU proceeds with a full expansion to all outbound flights: Watch for legacy carriers to announce route adjustments or cancellations on marginally profitable long-haul services to mitigate cost exposure. Expect a surge in public announcements of large-scale SAF offtake agreements as airlines attempt to secure supply and hedge against future carbon price volatility. This also increases the business case for technologies like carbon capture to produce e-fuels.

- If the EU opts for a compromise or delay: Watch for a renewed and intensified lobbying effort to harmonize the EU’s approach with the global CORSIA framework. Airlines will likely still accelerate fleet modernization, but the urgency to make drastic network cuts would diminish, leading to more gradual and predictable increases in ticket prices.

- These signals could be happening now: The unified and vocal opposition from 15 airline CEOs serves as a clear leading indicator of the perceived severity of the financial risk. Behind the scenes, airlines are undoubtedly running advanced network models to map out route profitability under different carbon price scenarios and preparing contingency plans for a worst-case regulatory outcome.

EU ETS Expansion to Dramatically Increase Covered Emissions

‘Scenario Modelling’ requires clear inputs about changing market conditions. This chart visualizes the most critical input for the airlines’ response models: the significant increase in the volume of emissions that will fall under the ETS.

(Source: Transport & Environment)

The questions your competitors are already asking

This report covers one angle of the financial exposure of European airlines to the EU’s carbon market reforms. The questions that matter most depend on your work.

- Which European airlines are gaining or losing ground in managing their exposure to the EU ETS expansion?

- Are Lufthansa, IAG, and Air France-KLM good investments given their €1.5 billion-plus exposure to EU ETS carbon costs?

- What is the status of the CEO opposition to the EU ETS expansion for all outbound international flights?

- Which European airlines are leading the adoption of Sustainable Aviation Fuel (SAF) to mitigate their EU ETS compliance costs?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.