TEPCO CCUS Strategy, $70 B Decarbonization Plan, HPE Partnership, and JERA Project Contrast (2024-2026)

TEPCO’s Phased CCUS Adoption: Digital Foundations Before Physical Assets

Tokyo Electric Power Company (TEPCO) is deliberately deferring large-scale Carbon Capture, Utilization, and Storage (CCUS) project commitments, instead prioritizing digital optimization and market-based mechanisms as preparatory steps for future deployment. This positions the company as a technology evaluator rather than a first-mover, a strategy shaped by high technology costs and a focus on strengthening its financial position before committing to capital-intensive infrastructure.

- The period from 2021 to 2024 was characterized by strategic planning, but by 2025 this evolved into tangible, non-asset-based actions. The October 2024 partnership with Hewlett Packard Enterprise (HPE) to leverage AI for efficiency and the launch of a “Carbon Offset Gas” service in 2025 demonstrate a focus on building commercial and digital capabilities, not physical CCUS plants.

- This cautious approach contrasts sharply with domestic competitor JERA, which in April 2025 formed a joint venture to develop the Blue Point low-carbon ammonia project in the U.S. The project will capture approximately 2.3 million metric tons of CO₂ annually, highlighting a direct investment strategy in physical decarbonization assets.

- TEPCO’s pilot projects are focused on adjacent technologies that build expertise for a future decarbonized grid. Its green hydrogen demonstration project, launched in October 2025, is a key step in developing a non-fossil fuel value chain that will complement, rather than constitute, its eventual CCUS activities.

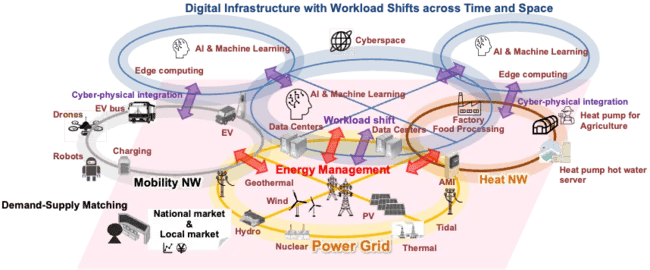

TEPCO Visualizes Digitally Integrated Energy Grid

The section heading emphasizes TEPCO’s strategy of building ‘Digital Foundations Before Physical Assets.’ The chart, which visualizes a digitally integrated energy grid, directly illustrates this digital-first approach, making it a perfect conceptual match for the section’s theme.

(Source: Energy Central)

$70 Billion Investment Plan, TEPCO’s Focus on Renewables Over CCUS

TEPCO’s massive ten-year, ¥11 trillion ($70 billion) investment plan, announced in early 2026, allocates capital primarily toward expanding renewable and other carbon-free generation sources, positioning CCUS as a longer-term solution for residual emissions from its essential thermal power assets.

- The primary objective of the $70 billion investment is to increase TEPCO’s share of carbon-free electricity from approximately 20% in 2024 to over 60% by 2040. This signals a clear strategic preference for deploying capital on proven technologies like renewables and nuclear ahead of large-scale CCUS.

- To fund this transition, TEPCO initiated a major financial restructuring in 2026, including a ¥3.1 trillion ($20 billion) cost-cutting program and a ¥200 billion ($1.3 billion) asset sale. This demonstrates that securing balance sheet health is a prerequisite for executing its long-term decarbonization strategy.

- The absence of specific, large CAPEX allocations for CCUS projects within this initial plan suggests the company is awaiting lower technology costs and stronger regulatory price signals, particularly from Japan’s mandatory Emissions Trading System (ETS) starting in 2026, before making significant commitments.

TEPCO’s Installed PV Capacity Growth Projection

The section highlights TEPCO’s investment focus on renewables over CCUS. This chart provides concrete evidence by showing a specific growth projection for solar (PV) capacity, quantifying the company’s commitment to renewables as mentioned in the heading.

(Source: Energy Central)

Table: TEPCO Strategic Financial Commitments and National Context

| Initiative | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| 10-Year Decarbonization Investment | 2026 – 2035 | TEPCO plans to invest over ¥11 trillion ($70 billion) to increase its carbon-free electricity generation share to over 60% by 2040, focusing on renewables and grid modernization. | Nikkei Asia |

| Cost Reduction Program | 2025 – 2034 | A ¥3.1 trillion ($20 billion) cost-cutting initiative across personnel, equipment, and power supply to streamline operations and fund strategic investments. | Reuters |

| Asset Divestment Program | 2026 – 2028 | Plan to sell approximately ¥200 billion ($1.3 billion) in assets, primarily real estate, to generate funds for Fukushima cleanup and new business initiatives. | The Japan Times |

| Japan National CCUS Funding | 2014 – 2025 | The Japanese government has spent $5.2 billion to support domestic and overseas carbon capture projects, creating a favorable policy environment for future private investment. | Climate Home News |

TEPCO’s Digital-First Alliances with HPE and NTT vs. JERA’s Asset-Building JV (2024-2026)

In 2025-2026, TEPCO’s partnerships with technology firms like HPE and NTT focus on creating data-driven efficiencies and platforms for low-carbon services, a stark contrast to competitor JERA’s asset-focused joint venture to build physical CCUS infrastructure.

- The October 2024 collaboration with HPE uses the Green Lake cloud platform for AI-driven optimization, aiming to reduce the carbon footprint through data analysis and operational efficiency rather than direct capture technology. This focus on data-driven decarbonization is also being pursued by major technology companies like Microsoft, which are securing massive renewable energy deals to power their data centers.

- A joint investment with NTT, disclosed in November 2025, targets the high energy demand of data centers. This move positions TEPCO as a provider of future carbon-neutral energy solutions for the digital economy, a market also being served by firms like Bloom Energy with its fuel cell technology, but it does not involve building capture facilities today.

- This digital enablement strategy contrasts with JERA’s April 2025 joint venture with CF Industries and Mitsui & Co., which represents a direct, multi-party investment in a world-scale low-carbon ammonia plant with integrated CCUS. This mirrors the asset-building approach taken by other global energy giants like Exxon Mobil in the blue hydrogen space.

Table: TEPCO Decarbonization Partnerships vs. Competitor (JERA)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| TEPCO & Hewlett Packard Enterprise | Oct 2024 | Technology collaboration where TEPCO SYSTEMS uses the HPE Green Lake cloud platform to leverage AI and data for advancing a lower-carbon footprint through operational efficiency and new services. | HPE Newsroom |

| TEPCO & NTT Global Data Centers | Nov 2025 (Disclosed) | Joint investment to address the high energy demands of data centers, creating a platform for future carbon-neutral power solutions. | TEPCO Integrated Report |

| JERA (Competitor), CF Industries, & Mitsui & Co. | Apr 2025 | A joint venture to build a world-scale low-carbon ammonia plant in the U.S. designed to capture and sequester 2.3 million metric tons of CO₂ annually. | CF Industries |

Japan-Centric Strategy, TEPCO’s Domestic Focus vs. JERA’s Global Plays

TEPCO’s decarbonization activities for 2025-2026 are almost entirely concentrated within Japan, focusing on national policy drivers and domestic market development, whereas key competitors like JERA are actively pursuing international, large-scale CCUS projects to secure low-carbon energy imports.

- TEPCO’s initiatives, including its green hydrogen demonstration project, the supply of decarbonized electricity to Subaru’s Tokyo office, and its offering of “Carbon Offset Gas” using Japan’s J-Credit market, are all rooted in the domestic Japanese market.

- The company’s strategy is closely aligned with Japanese national policy, including the “GX 2040 Vision” and the Japan Organization for Metals and Energy Security (JOGMEC) selection of nine potential domestic CCS projects, indicating a plan to leverage government support within Japan.

- In contrast, JERA’s flagship CCUS-related project, the Blue Point low-carbon ammonia plant announced in April 2025, is located in Louisiana, USA. This showcases a global strategy to secure low-carbon energy sources, similar to how other international energy companies like Shell and Woodside Energy operate across different geographies to build their energy transition portfolios.

Japan’s Carbon Import Market Shows Diversification

The section contrasts TEPCO’s ‘Domestic Focus’ with JERA’s ‘Global Plays.’ The chart on Japan’s carbon import market illustrates a key international aspect of the energy transition, serving as a backdrop for the ‘Global Plays’ that a competitor like JERA might engage in.

(Source: 6Wresearch)

TEPCO’s CCUS Path: From R&D and Market Services to Future Deployment

For TEPCO, CCUS remains in a preparatory phase focused on research, development, and market services, as the high costs and technical uncertainties of large-scale deployment prevent immediate commercialization and favor investments in more mature technologies.

- Between 2021-2024, TEPCO’s approach was largely strategic planning. By 2025, this evolved into creating commercial products like “Carbon Offset Gas” and providing decarbonized electricity to corporate clients like Subaru, monetizing carbon reduction without deploying capital-intensive capture technology.

- The significant cost of CCUS technologies in 2025, with Direct Air Capture (DAC) ranging from $400 to $1, 500 per tonne and retrofitting power plants costing $86 to $132 per tonne, reinforces TEPCO’s decision to wait for technological maturation and cost reductions.

- National-level initiatives, such as the advanced CO₂ capture system showcased at Expo 2025 Osaka, serve as the primary testbeds for technologies that TEPCO and other Japanese utilities will evaluate, underscoring that the technology is still in a demonstration phase for the Japanese context.

Lifecycle Carbon Impact of Direct Air Capture Technology

The section describes TEPCO’s CCUS path, beginning with R&D. This chart provides a technical deep-dive into Direct Air Capture (a CCUS technology), illustrating the detailed lifecycle analysis that is characteristic of the R&D phase before future deployment.

(Source: ScienceDirect.com)

TEPCO CCUS SWOT Analysis: Financial Discipline vs. Competitive Lag

TEPCO’s CCUS strategy is characterized by the strength of its cautious financial approach and alignment with national policy, but this creates a weakness in its competitive positioning and a threat of falling behind first-movers in securing technology and partnerships.

- Strength: The company’s disciplined approach, underpinned by a massive $70 billion investment plan and a $20 billion cost-cutting initiative, provides a stable foundation for long-term decarbonization.

- Weakness: By prioritizing renewables and financial restructuring, TEPCO is visibly lagging behind competitors like JERA in the deployment of tangible CCUS assets.

- Opportunity: The impending mandatory ETS in 2026 will create a clear price signal, potentially making CCUS projects economically viable and justifying a strategic pivot.

- Threat: While TEPCO waits, competitors are locking in global partnerships and technology access, which could place TEPCO at a long-term disadvantage.

TEPCO’s Daily Power Mix Varies Widely

This section is a SWOT analysis. The chart showing TEPCO’s variable and fossil-fuel-reliant power mix directly illustrates a core ‘Weakness’ or ‘Threat’ driving the need for a CCUS strategy, thereby providing essential context for the SWOT discussion.

(Source: Energy Central)

Table: SWOT Analysis for TEPCO’s CCUS Strategy

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strength | Strategic planning for national decarbonization goals. | A concrete $70 B investment plan and a $20 B cost-cutting program. Strong alignment with Japan’s “GX” strategy. | The shift from abstract planning to a fully articulated and funded financial and strategic restructuring plan. |

| Weakness | Ambiguity on the specific role and timing of CCUS deployment. | No large-scale, physical CCUS projects announced. A clear lag behind competitor JERA’s asset-building strategy. | The competitive gap in tangible CCUS project development became explicit and measurable against JERA’s U.S. project. |

| Opportunity | Emerging government support for decarbonization technologies. | Japan’s mandatory ETS legislated for 2026. JOGMEC selection of 9 potential CCS projects for support. Digital decarbonization partnerships (HPE). | The primary regulatory catalyst (the ETS) is no longer theoretical but is now a legislated, imminent market force. |

| Threat | High cost and technological immaturity of CCUS. | Costs remain high ($400+/tonne for DAC). Competitors like JERA are securing international partnerships (CF Industries), potentially limiting future options. | The risk of being a technology-taker became more pronounced as competitors actively locked in global partnerships and supply chains. |

TEPCO’s 2026 Turning Point: Will the ETS Mandate CCUS Investment?

The single most critical driver for TEPCO’s shift from planning to CCUS deployment will be the economic pressure created by Japan’s mandatory Emissions Trading System (ETS), set to begin in 2026.

- If the ETS establishes a high and stable carbon price, watch for TEPCO to fast-track its participation in one of the JOGMEC-supported projects or announce its first proprietary pilot CCUS plant at a thermal power station.

- If the ETS price is low or initial allowances are generous, these could be happening: TEPCO continues its current strategy, focusing on its renewables build-out, extending the life of its digital and offset-based services, and deferring major CCUS CAPEX past 2026.

- A key signal to watch will be the specific allocation of its $70 billion investment fund in post-2026 financial reports. The appearance of a multi-billion dollar line item for “Carbon Capture Projects” would validate a definitive strategic pivot.

Japan Launches Carbon Market, Reforms Wind Auctions

The section questions whether a future Emissions Trading Scheme (ETS) will mandate CCUS investment. The chart’s headline, ‘Japan Launches Carbon Market,’ directly refers to the establishment of an ETS, making it the most relevant visual to support the section’s core topic.

(Source: LinkedIn)

The questions your competitors are already asking

This report covers one angle of TEPCO’s strategy for CCUS and large-scale decarbonization. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in Japan’s utility decarbonization market: TEPCO or JERA?

- TEPCO investments and funding. Is its $70 billion decarbonization plan on track to meet its 2030 targets?

- TEPCO activities in digital decarbonization. Is the HPE partnership for AI optimization progressing from pilot to wider deployment?

- What is the outlook for large-scale CCUS deployment by Japanese utilities by 2030?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.