Offshore Hydrogen 2026: Why Legacy Giants Prioritize Consolidation Over Green CAPEX

Commercial Hydrogen Projects 2026: A Market of Pilots and Pragmatism

The transition from 2024 to 2025 reveals a strategic split, with offshore drilling incumbents like Transocean prioritizing core business consolidation over direct, large-scale green hydrogen production, while other energy majors advance tangible, albeit regionally concentrated, projects.

- Prior to 2025, Transocean‘s engagement was limited to exploring operational decarbonization, such as using hydrogen injection for its rig engines. In 2025, its strategy shifted to investigating the repurposing of offshore platforms for green hydrogen, a conceptual plan that remains secondary to the execution of its massive $5.8 billion merger with Valaris announced in early 2026.

- This contrasts with competitors like Repsol, which in September 2025 moved from planning to execution by approving a €300 million-plus investment in a 100 MW green hydrogen facility in Spain, a concrete capital commitment far beyond Transocean‘s current scope.

- The investment climate for hydrogen became more cautious in 2025 after the IEA revised its 2030 low-emissions hydrogen production forecast downward, from 49 million to 37 million tonnes per year. This adjustment supports a more pragmatic approach that favors incremental steps over speculative capital outlays.

- Market signals are mixed, creating further uncertainty. While Exxon Mobil paused its US blue hydrogen project in late 2025 due to weak market demand, the discovery of natural hydrogen in Canada in early 2026 opens a new, albeit nascent, technological pathway for the industry.

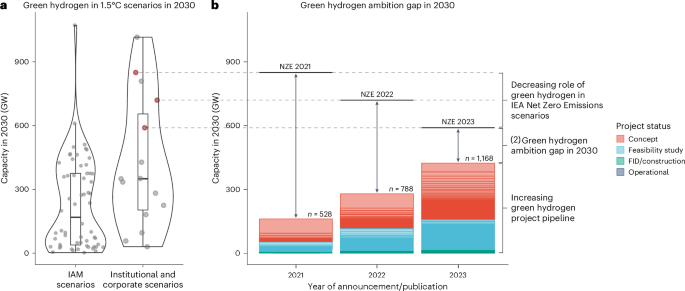

Hydrogen Project Pipeline Lags 2030 Ambition

This chart supports the section’s theme of “pilots and pragmatism” by showing the vast majority of green hydrogen projects remain in early ‘Concept’ or ‘Feasibility’ stages, not yet under construction.

(Source: Nature)

Hydrogen Investment Analysis: Strategic Capital Favors Core Business and Proven Tech

In 2025, capital allocation in the energy sector demonstrated a clear preference for strengthening core operations and funding proven, adjacent energy transition projects, rather than committing to speculative offshore hydrogen ventures.

New Hydrogen Projects Target Existing Demand

This chart perfectly illustrates the section’s argument that capital favors proven applications, showing that new hydrogen capacity is committed to decarbonizing existing industrial demand in refining and ammonia.

(Source: Strategic Energy Europe)

- Transocean‘s major financial move in September 2025 was an upsized public offering, not a direct hydrogen project investment. This capital was designated for strengthening its balance sheet ahead of the Valaris merger and for general corporate purposes, underscoring a priority on consolidation.

- In sharp contrast, Repsol’s Final Investment Decision (FID) in September 2025 for its Cartagena green hydrogen project involved a direct commitment of over $320 million to a specific green energy asset, highlighting a different strategic priority.

- Market caution was further validated by Exxon Mobil‘s decision in November 2025 to halt development of its large-scale blue hydrogen facility in Baytown, Texas. The company cited weak market demand as the primary driver, providing a significant counterpoint to the green hydrogen investment narrative.

Table: Comparative Capital Allocation in the Energy Sector (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Exxon Mobil / Blue Hydrogen Facility | Nov 2025 | Development of a large-scale blue hydrogen production facility in Baytown, Texas, was paused. The decision was attributed to weak market demand, signaling a cautious approach to new hydrogen investments. | The Energy Year |

| Repsol / Cartagena Green Hydrogen Project | Sep 2025 | Approved construction of a 100 MW green hydrogen plant with an investment over $320 million. The project aims to produce 15, 000 tonnes per annum, targeting decarbonization of its refinery. | Upstream |

| Transocean / Public Offering | Sep 2025 | Executed an upsized public share offering to strengthen its capital structure for operations and strategic initiatives. This move shores up its finances ahead of the Valaris merger, rather than funding a specific hydrogen project. | Vinson & Elkins |

Hydrogen Partnerships: Vague Agreements Lag Behind Concrete Supply Chain Alliances

Partnership activity in 2025-2026 reveals a gap between foundational, non-specific agreements by companies like Transocean and the concrete, supply-chain-focused collaborations formed by more advanced players.

Mapping the Complete Hydrogen Value Chain

This diagram provides visual context for the section’s point, illustrating the complex ecosystem that “concrete, supply-chain-focused collaborations” must address, in contrast to the vague partnerships mentioned.

(Source: Sandia National Laboratories)

- Transocean‘s sole hydrogen-related partnership noted in May 2025 is a foundational agreement to designate an “Official or Technology or Hydrogen Partner, ” with specific terms yet to be agreed upon. This signals an early, exploratory stage with no committed resources or defined project scope.

- Conversely, the Mo U between En BW and Acwa in February 2026 establishes a specific goal: creating a hydrogen corridor to import ammonia from Saudi Arabia to Germany. This represents a mature, strategic alliance aimed at building a tangible international supply chain.

- Even Transocean‘s most significant diversification partnership, a 2023 joint venture with Eneti (now part of DEME Group), is explicitly focused on offshore wind installation. Although partner DEME is active in hydrogen, the JV’s scope does not extend there, highlighting a deliberate focus on a more mature adjacent market.

Table: Analysis of Hydrogen-Related Partnerships (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| En BW / Acwa | Feb 2026 | Signed an Mo U to establish a hydrogen corridor between Saudi Arabia and Germany. The partnership aims to build a supply chain for green hydrogen and its derivatives like ammonia. | The Energy Year |

| Transocean / Unnamed Partner | May 2025 | A foundational partnership agreement was put in place where an unnamed entity would be referred to as Transocean‘s technology or hydrogen partner. The agreement lacks specific project details or commitments. | [PDF] Government of Jersey |

Global Hydrogen Hotspots: Investment Divergence Between West and Emerging Hubs

The period from 2025 to today highlights a clear geographical divergence in hydrogen project momentum, with emerging economies showing high potential for giga-scale investment decisions while established Western markets demonstrate a more cautious, project-by-project approach.

Middle East Green Hydrogen Market Surges

This forecast provides a direct example for the section’s thesis, showing strong investment growth in an “emerging hub” (the Middle East) and validating the point about geographical divergence.

(Source: Grand View Research)

- While hydrogen project announcements were widespread before 2025, analysis from that year shows a low probability of giga-scale Final Investment Decisions (FIDs) in North America and Western Europe. This indicates potential delays or a scaling-back of ambitions in these regions.

- In contrast, Brazil, the Middle East, India, and parts of Asia are identified as high-potential zones for major FIDs in 2025. This is exemplified by Saudi Arabia’s NEOM Green Hydrogen Complex, which is moving forward with a 2 GW electrolyzer, positioning the region as a future production powerhouse.

- Transocean’s new drilling contracts in 2025-2026 are in its traditional hotspots of Brazil, Norway, and Mexico. This ties its capital generation to established oil and gas regions, not the emerging hydrogen centers, while its own hydrogen strategy remains geographically undefined.

- European activity, such as Repsol‘s project in Spain, demonstrates continued progress on a large scale (100 MW) supported by government grants. This indicates a regional growth model that differs from the massive, state-backed projects seen elsewhere.

Hydrogen Technology Maturity: From Onboard Decarbonization to Offshore Production Concepts

The technological focus for offshore operators has shifted from near-term, operational solutions like hydrogen injection (pre-2025) to more ambitious, long-term concepts like repurposing entire platforms for green hydrogen production (2025-onward), though the latter remains in the earliest stages of investigation.

Defining Hydrogen by its Production Source

This infographic is essential for understanding the technological shift to “green hydrogen production” discussed in the section, clarifying for the reader how it differs from other production methods.

- Prior to 2025, Transocean‘s hydrogen interest centered on its use as a fuel supplement for diesel engines. This technology represented an incremental, risk-averse application aimed at reducing emissions from existing assets.

- In 2025, Transocean‘s stated strategy evolved to include investigating the repurposing of its offshore platforms for green hydrogen production. This marks a conceptual leap from using hydrogen as a fuel additive to becoming a producer, but it remains a strategic plan, not a funded project.

- The maturity gap is evident when compared to projects like the NEOM Green Hydrogen Complex or Repsol‘s 100 MW facility. These ventures are deploying commercially available electrolyzer technology at scale, while Transocean is still evaluating the feasibility of applying it offshore.

- The discovery of natural hydrogen concentrations in Canada in early 2026 introduces a new technological pathway. This technology is at an early R&D stage but could eventually leverage the drilling and subsea expertise of companies like Transocean if it becomes commercially viable.

SWOT Analysis: Transocean’s Hydrogen Strategy Amidst Market Consolidation

Transocean‘s SWOT profile for hydrogen is dominated by the immense operational and financial strength of its core business, which simultaneously provides the means for future diversification while also acting as a major constraint on its immediate appetite for risk in nascent markets.

Green Hydrogen Market Faces Explosive Growth

This chart quantifies the “Opportunity” aspect of the SWOT analysis, showing the massive market growth potential that motivates a company like Transocean to explore diversification into green hydrogen.

(Source: Insightace Analytic)

- The company’s primary strength is its unparalleled offshore expertise and massive asset base, which are core to its “repurposing” strategy, alongside strong cash flow from its drilling contracts.

- A key weakness is the lack of any demonstrated hydrogen project experience and the overwhelming management focus required for the complex $5.8 billion Valaris merger.

- The opportunity lies in leveraging its assets for a first-mover advantage in offshore hydrogen production, should the market mature and require such specialized infrastructure.

- The main threat is being outpaced by more committed competitors who are already building projects and supply chains, alongside the broader market risk of slower-than-expected hydrogen demand, as indicated by the IEA’s revised forecast.

Table: SWOT Analysis for Transocean’s Hydrogen Position

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Deep offshore drilling expertise. Large fleet of high-specification rigs. Experience in adjacent sectors like CCS (Northern Lights project). | Dominant market position reinforced by $17 B Valaris merger. Strong backlog (over $257 M in new deals in late ’25/early ’26) providing financial stability for diversification. | The Valaris merger validates a strategy of consolidation and scale in the core business, creating a financial powerhouse that could, in theory, fund future energy transition ventures. |

| Weaknesses | No direct experience in hydrogen production or commercialization. Focus on operational decarbonization (hydrogen injection) rather than new business models. | Management bandwidth and capital likely consumed by massive Valaris integration. Hydrogen strategy remains conceptual (“investigating repurposing”) with no concrete projects or investment. | The 2025-2026 period confirmed that hydrogen is a low-priority, exploratory initiative, not a core strategic pillar, as corporate resources are diverted to the merger. |

| Opportunities | Leverage offshore engineering expertise for new energy sectors. Potential to enter offshore wind installation via JV with Eneti/DEME. | Capitalize on a capital-efficient entry into hydrogen by repurposing existing offshore platforms. Secure a first-mover advantage in offshore hydrogen production infrastructure if market demand accelerates. | The “repurposing” strategy, articulated in 2025, presents a logical, low-CAPEX entry point, but it remains an unvalidated opportunity without a pilot project. |

| Threats | Competition from other energy majors with more aggressive hydrogen strategies. Volatility in the oil and gas market affecting capital for new ventures. | Slower-than-expected hydrogen market growth (IEA forecast revision). Competitors like Repsol are moving to FID on large-scale projects, capturing market share and experience. Risk of stranded assets if the pivot is too slow. | The 2025-2026 data validates the threat of being outpaced. While Transocean strategizes, others are building, and market headwinds like Exxon Mobil‘s project pause show the risks are real. |

2026 Outlook: Watch for Pilot Project FID to Validate Offshore Hydrogen Strategy

The critical determinant for Transocean‘s hydrogen ambitions in the year ahead is whether its “investigation” into platform repurposing translates into a funded pilot project; without this milestone, the strategy remains a paper exercise overshadowed by the realities of the Valaris merger and a booming oil and gas market.

Green Hydrogen’s Market Share to Triple

This chart underscores the strategic importance of the 2026 outlook by showing the projected dominance of green hydrogen, explaining why a pilot project FID is a critical validation milestone.

(Source: ScienceDirect.com)

- If Transocean announces a specific pilot project with a defined budget, timeline, and partner in 2026, it would signal a genuine strategic commitment. Watch for the allocation of capital from its recent offering towards this initiative, rather than exclusively to rig upgrades or debt service.

- Continued high-value contract awards for its drilling fleet, like the over $257 million in new backlog secured in late 2025 and early 2026, could reinforce the status quo. This would prioritize reinvestment in the profitable core business and delay any significant hydrogen capital expenditures.

- The success of the Valaris integration is the primary near-term focus. Any stumbles or higher-than-expected integration costs will likely starve nascent ventures like hydrogen of both capital and management attention. The creation of the $17 billion entity is the dominant event.

- Monitor the progress of competitor projects and end-use markets, such as the development of the Top Green Ammonia Projects 2025: Unveiling the Global Top 10 and trends in Methanol Bunkering 2026: An Uphill Battle Against LNG, as these will shape the demand that offshore production aims to serve.

Frequently Asked Questions

Why is Transocean prioritizing a merger over investing in green hydrogen?

According to the analysis, Transocean is prioritizing the consolidation of its core offshore drilling business through its $5.8 billion merger with Valaris. This strategy focuses on strengthening its market position and balance sheet in a proven sector, viewing large-scale green hydrogen CAPEX as a secondary, conceptual plan that is more speculative in the current cautious investment climate.

What is the main difference between Transocean’s and Repsol’s approach to hydrogen?

The primary difference is the level of concrete investment. In September 2025, Repsol approved a direct investment of over €300 million for a 100 MW green hydrogen plant in Spain. In contrast, Transocean’s major financial move in the same period was a public offering to support its merger, while its hydrogen strategy remains at an exploratory stage of ‘investigating’ the repurposing of platforms, with no specific project or capital committed.

Is the overall market for hydrogen slowing down?

The article suggests the investment climate became more cautious in 2025. This is supported by two key events: the IEA revising its 2030 low-emissions hydrogen production forecast downward by nearly 25% (from 49 to 37 million tonnes), and Exxon Mobil pausing its large-scale blue hydrogen project in late 2025 due to weak market demand.

What does the SWOT analysis say is Transocean’s biggest weakness regarding hydrogen?

The SWOT analysis identifies Transocean’s primary weakness as the overwhelming management bandwidth and capital that will likely be consumed by the massive Valaris merger and integration. This leaves its hydrogen strategy as a conceptual, low-priority initiative with no concrete projects or dedicated investment, while competitors gain practical experience.

What is the key indicator to watch for in Transocean’s hydrogen strategy in 2026?

The 2026 outlook states that the critical determinant for Transocean’s hydrogen ambitions is whether its ‘investigation’ into repurposing platforms translates into a funded pilot project. An announcement of a pilot with a defined budget, timeline, and partner would signal a genuine strategic commitment. Without it, the strategy remains a ‘paper exercise’.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.