Hydrogen FID Freeze 2026: Why Majors Like Woodside Are De-Risking Giga-Projects

Hydrogen Project Adoption Shifts from Ambition to Pragmatism

The hydrogen industry’s transition from ambitious project announcements to a cautious, pragmatic execution phase is marked by a significant slowdown in Final Investment Decisions (FIDs), as energy majors reassess capital-intensive projects amid economic and policy headwinds. This strategic recalibration prioritizes financial discipline and de-risking over rapid, speculative expansion.

- Between 2021 and 2024, the market was characterized by large-scale project proposals, such as Woodside Energy’s ambitious plans for the dual-pathway H 2 Perth and green hydrogen H 2 TAS projects in Australia.

- The market shifted in 2025, with Woodside canceling its capital-intensive H 2 OK liquid hydrogen project in Oklahoma in July 2025. This move mirrors a broader industry trend, including Exxon Mobil’s decision to pause its major blue hydrogen project in Baytown, Texas.

- This reflects a “definitive slowdown” in FIDs for green hydrogen projects globally, driven by cost inflation and persistent policy uncertainty, forcing companies to pivot from international expansion to developing lower-risk domestic ecosystems.

- The current strategy is not an abandonment of hydrogen but a pivot to leverage profitable core businesses, such as LNG, to fund a more measured and long-term exploration of new energy ventures, validating the need for a staged approach to the energy transition.

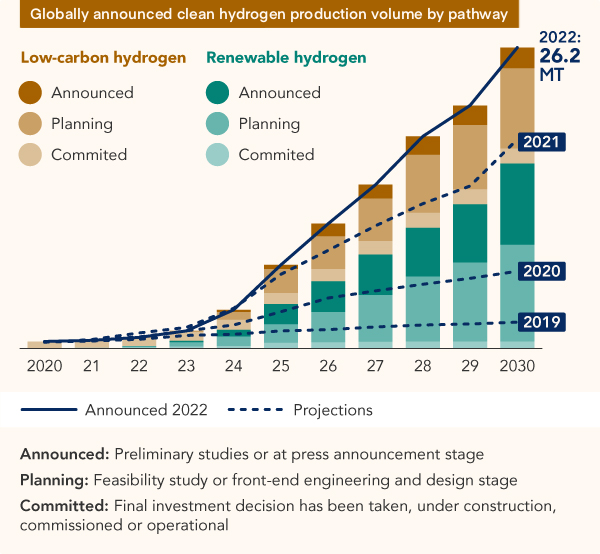

Gap Widens Between Hydrogen Ambition, Reality

This chart perfectly illustrates the section’s theme by showing a large and growing gap between announced hydrogen projects (ambition) and the small fraction that have a committed Final Investment Decision (pragmatism).

(Source: GNS Science)

Hydrogen Investment Realigns as Majors Prioritize Core Assets

In 2025, capital allocation by energy majors pivoted sharply away from speculative hydrogen projects towards fortifying core oil and gas assets, with project cancellations and pauses serving as the most significant financial signals in the new energy sector. This financial realignment underscores a return to proven, cash-generative operations to navigate market uncertainty.

Majors Double Down on Core Assets

This infographic details Woodside’s strong performance in its core LNG and oil assets, directly supporting the section’s point that majors are fortifying proven, cash-generative operations over speculative projects.

(Source: Seeking Alpha)

- The most significant financial move in the hydrogen space was a divestment action, with Woodside’s exit from the H 2 OK project in July 2025 to cut costs and de-risk its new energy portfolio.

- This contrasts sharply with concurrent investments in traditional energy, such as Woodside’s approval of the Kipper 1 B and Turrum Phase 3 gas projects in the first half of 2025 and a major LNG supply agreement with Turkey’s BOTAŞ.

- Financial performance reinforces this priority, with Woodside’s $1, 316 million net profit in H 1 2025 driven entirely by its traditional oil and gas segments, not its nascent hydrogen business.

- This trend is not isolated. In June 2025, peer Meridian Energy cancelled its large-scale green hydrogen project, citing unfavorable economics and a lack of government underwriting, further highlighting the challenging investment climate.

Table: Key Hydrogen Project Cancellations and Pauses (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Woodside Energy / H 2 OK Project | July 2025 | Exited the planned liquid hydrogen production facility in Oklahoma, USA, as part of a strategic pivot to cut costs and halt major capital expenditure on US-based hydrogen. | Discovery Alert |

| Meridian Energy / Southern Green Hydrogen | June 2025 | Cancelled its grand green hydrogen project in New Zealand due to unfavorable economics and the lack of sufficient government financial support, highlighting market-wide challenges. | Newsroom.co.nz |

| Exxon Mobil / Baytown Blue Hydrogen Project | February 2025 (Paused) | Paused its planned 1 Bcf/d blue hydrogen project in Texas, reflecting the difficult economic and regulatory landscape for large-scale, low-carbon hydrogen initiatives. | S&P Global |

Partnership Strategy Pivots to Foundational, Long-Term Exploration

Strategic partnerships in the hydrogen sector are shifting from aggressive development joint ventures to more cautious, exploratory agreements focused on de-risking future supply chains and cultivating local demand ecosystems. This change reflects the market’s pivot from rapid expansion to methodical foundation-building.

- The ambitious partnerships of the early 2020 s, such as Woodside’s January 2024 collaboration with SK E&S to explore offtake and equity participation, have been superseded by more conservative models.

- By September 2025, the focus shifted to foundational studies, evidenced by Woodside’s Memorandum of Understanding (MOU) with Japanese counterparts to assess the long-term viability of a low-carbon hydrogen supply chain.

- In parallel, partnerships are being localized to stimulate demand. Woodside’s collaboration with vehicle operators in Western Australia, reported in October 2025, aims to support the early adoption of hydrogen vehicles and create a stable domestic customer base for future production from projects like H 2 Perth.

- Collaboration on enabling technologies remains critical, with the April 2024 partnership between Woodside and Yara Pilbara to explore large-scale Carbon Capture and Storage (CCS) continuing as an essential step for future blue hydrogen viability.

Table: Evolution of Woodside’s Hydrogen-Related Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Multiple WA Vehicle Operators | October 2025 | Collaboration to support the adoption of hydrogen vehicles, creating a local demand ecosystem for future domestic production. | Govt. of Western Australia |

| Japanese Companies | September 2025 | MOU to study and demonstrate the viability of a large-scale, low-carbon hydrogen supply chain, positioning for future export markets without immediate capital commitment. | Petroleum Australia |

| Yara Pilbara | April 2024 | Collaboration to explore a large-scale CCS project, a critical enabler for decarbonizing existing assets and future blue hydrogen production. | Carbon Credits |

| SK E&S | January 2024 | Partnership to investigate long-term offtake agreements and potential equity participation for hydrogen and ammonia supply to the Korean market. | Chem Analyst |

Hydrogen Geography Contracts from Global Expansion to Domestic Strongholds

The geographic focus for major energy players in hydrogen has contracted from ambitious global expansion in the early 2020 s to a strategic consolidation within domestic markets where companies hold existing operational advantages and can influence policy. This retreat to home turf is a direct response to heightened risks in undeveloped international markets.

- The 2021-2024 period saw companies like Woodside pursue a global footprint, with planned projects in the United States (H 2 OK) and potential developments in New Zealand (Southern Green Hydrogen project).

- In 2025, this strategy was reversed. The cancellation of the Oklahoma-based H 2 OK project marked a definitive retreat from capital-intensive US hydrogen production.

- The company’s focus has now consolidated in Australia, where it is advancing projects like H 2 Perth in Western Australia and H 2 TAS in Tasmania, leveraging its deep operational history and existing infrastructure in the region.

- Future international activity is now framed through low-risk, long-term exploratory partnerships, such as the MOU with Japanese firms, rather than direct foreign investment in new production assets.

Hydrogen Technology Waits for Commercial Viability as Majors Re-evaluate Pathways

Despite technological readiness, the commercial maturity of both green and blue hydrogen production is being challenged by unfavorable economics, leading companies to maintain a technologically agnostic stance while waiting for cost curves and policy support to align. The current bottleneck is not the technology itself but its economic viability at industrial scale.

High Costs Impede Hydrogen Commercialization

This chart identifies ‘High capital costs’ as a significant market restraint, directly visualizing the unfavorable economics and commercial viability challenges discussed in the section.

(Source: Coherent Market Insights)

- The period between 2021 and 2024 was driven by an assumption that scaling production via projects like H 2 Perth (SMR with CCS and electrolysis) would drive down costs, backed by an investment target of $5 billion in new energy by 2030.

- The reality of 2025 demonstrated that persistent inflation and uncertain government subsidies made the economics of large-scale projects, particularly in new markets, untenable, leading directly to the H 2 OK cancellation.

- Woodside’s strategy now reflects this reality by keeping multiple technology pathways open without committing to a final investment decision. It continues to advance both blue hydrogen (H 2 Perth) and green hydrogen (H 2 TAS) concepts.

- This dual-pathway approach is enabled by foundational investments in cross-cutting technologies like CCS via the planned Angel CCS project, which de-risks the blue hydrogen option but remains a long-term venture dependent on its own set of commercialization hurdles similar to the DAC market in 2026.

SWOT Analysis: Woodside’s Hydrogen Pivot in a Challenging Market

A SWOT analysis reveals that while Woodside has strong foundational strengths in gas processing and project management, its hydrogen strategy has been forced to adapt to external market weaknesses and threats, shifting its opportunities from rapid international growth to more measured domestic development.

- Strengths in LNG expertise and cash flow were repurposed from funding aggressive expansion to underwriting a more cautious, de-risked approach.

- Weaknesses related to high project CAPEX and dependency on policy support were validated by market conditions, forcing the cancellation of at-risk projects.

- Opportunities have shifted from capturing first-mover advantage in global markets to building foundational domestic demand and securing long-term, low-risk export partnerships.

- Threats from cost inflation and policy uncertainty intensified significantly in 2025, becoming the dominant drivers of strategic change across the industry.

Table: SWOT Analysis for Woodside’s Hydrogen Strategy Evolution

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | LNG operational expertise and strong cash flow to fund a $5 B new energy investment target. | Core LNG business profitability ($1.3 B H 1 profit) used to stabilize the company during a new energy pivot. | The core business was validated as a critical financial anchor, enabling a strategic retreat rather than a forced exit from new energy. |

| Weaknesses | High CAPEX requirements for greenfield hydrogen projects (e.g., H 2 TAS at $90.3 M). Dependency on CCS for blue hydrogen. | Realized inability of projects like H 2 OK to proceed without clear policy support and subsidies. | The theoretical weakness of subsidy dependence was confirmed as a hard financial constraint, forcing project cancellations. |

| Opportunities | Pursue global first-mover advantage in export markets like the US (H 2 OK) and South Korea (SK E&S partnership). | Develop domestic demand (WA mobility) and secure long-term, exploratory supply chain partnerships (Japan MOU). | The opportunity shifted from rapid market capture to methodical, lower-risk market creation and long-term positioning. |

| Threats | Competition from other energy majors and challenging project economics. | A global slowdown in hydrogen FIDs, severe cost inflation, and widespread policy uncertainty become the dominant threats. | External market threats intensified from being a planning consideration to the primary driver of strategic retreat and de-risking. |

2026 Hydrogen Outlook: Watch for Domestic FIDs and Policy Triggers

The critical indicator for a thaw in the hydrogen FID freeze in 2026 will be the alignment of supportive domestic policy with tangible offtake agreements, which could trigger investment decisions for long-stalled projects. Without these two elements, large-scale project development will remain stalled.

Hydrogen CAPEX Awaits Policy Triggers

This chart shows clean hydrogen as a tiny fraction of total energy CAPEX, visually representing the investment stall that the 2026 outlook hopes to resolve through policy triggers and offtake agreements.

(Source: Issuu)

- If this happens: The Australian government announces a bankable, long-term incentive framework for clean hydrogen production, similar in structure to the US Inflation Reduction Act.

- Watch this: Woodside moving either its H 2 Perth or H 2 TAS project to a Final Investment Decision. Such a move would be a powerful signal of renewed confidence in the Australian market and could catalyze further investment across the sector.

- These could be happening: The exploratory MOU with Japanese partners matures into a binding commercial offtake agreement, providing the revenue certainty needed to underwrite project financing for a major export facility. Additionally, the direction set by Woodside’s new CEO following the December 2025 leadership change will be critical in determining the pace of its new energy ambitions.

Frequently Asked Questions

Why are major energy companies like Woodside canceling their big hydrogen projects?

Major energy companies are canceling or pausing large hydrogen projects due to a combination of high cost inflation, persistent policy uncertainty, and unfavorable economics. This has made these capital-intensive projects too risky in the current climate. As a result, they are pivoting to a more cautious strategy that prioritizes financial discipline and de-risking over rapid expansion.

Does this mean energy companies are abandoning hydrogen altogether?

No, it’s a strategic pivot, not an abandonment. Companies are shifting from ambitious global projects to a more measured, long-term approach. They are using profits from their core businesses, like LNG, to fund foundational activities such as building domestic demand, de-risking technology, and forming exploratory partnerships, waiting for better market conditions before making major investments.

What is the significance of Woodside canceling its H2OK project?

Woodside’s cancellation of the H2OK liquid hydrogen project in Oklahoma in July 2025 is significant because it reflects a broader industry trend of retreating from speculative, capital-intensive projects. It marked a definitive pivot for Woodside away from US-based hydrogen production to cut costs and consolidate its focus on its domestic Australian projects where it has existing operational advantages.

What needs to happen for these major hydrogen projects to get a green light (FID) in 2026?

According to the outlook, two key things need to happen. First, governments must implement bankable, long-term policy incentives, similar to the US Inflation Reduction Act, to make the projects economically viable. Second, developers need to secure binding commercial offtake agreements with customers, which provide the revenue certainty required to finance construction.

How have partnerships in the hydrogen sector changed?

Partnerships have shifted from aggressive joint ventures focused on rapid development and offtake (like Woodside’s 2024 talks with SK E&S) to more cautious, exploratory agreements. The current focus, as seen in Woodside’s 2025 MOU with Japanese companies, is on foundational studies to de-risk future supply chains and collaborations to build local demand, rather than immediate capital commitment.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.