Top 10 On-Site Power Pivots for AI: INNIO’s 2.3 GW Deal, Bloom Energy’s 1 GW Pact, and More (2024-2025)

The explosive growth of artificial intelligence is creating an unprecedented energy demand, forcing companies to adopt a “power-first” strategy for data center development. A clear pattern shows a strategic pivot away from relying on constrained electrical grids and toward deploying dedicated, on-site power generation. Key deals, such as INNIO’s landmark 2.3 GW order with Volta Grid and Bloom Energy’s agreement to supply up to 1 GW of fuel cell capacity, underscore a fundamental market shift. The dominant theme for 2025 is that securing reliable, scalable, and rapidly deployable power is now the primary enabler and bottleneck for AI expansion, creating a new class of specialized energy infrastructure providers and driving innovation in on-site solutions.

1. Hut 8

Company: Hut 8

Installation Capacity: $7 billion Google-backed deal

Applications: Leveraging existing data center assets and energy infrastructure, originally for Bitcoin mining, to power AI workloads.

Source: Hut 8 Pivots From Bitcoin to AI With $7 B Google-Backed Deal to …

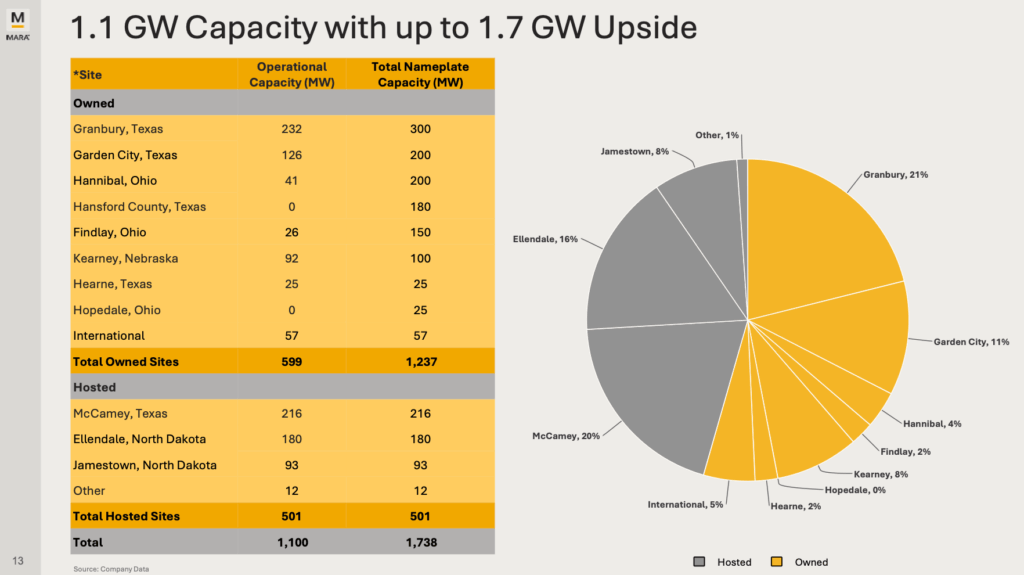

Bitcoin Miner Details 1.1 GW Power Capacity

This section on the specific miner Hut 8 is the ideal location for a chart detailing its specific power capacity available for AI workloads.

(Source: YIAZOU – Substack)

2. IREN (Iris Energy)

Company: IREN

Installation Capacity: Not Specified

Applications: Repurposing energy procurement and data center infrastructure from Bitcoin mining to AI cloud hosting.

Source: Bitcoin miners’ power edge makes them key AI infrastructure players …

Bitcoin Miners Pivot to AI for Revenue

The chart illustrates the strategic trend of miners diversifying into AI, for which IREN serves as a prime example discussed in this section.

(Source: Global X ETFs)

3. Applied Digital

Company: Applied Digital

Installation Capacity: 250 MW

Applications: High-performance computing (HPC) data center lease for AI cloud company Core Weave.

Source: Applied Digital Announces 250 MW AI Data Center Lease With …

HPC Hosting Capacity Projected to Exceed 1,150 MW

As a key player in the high-performance computing (HPC) space, Applied Digital’s strategy is contextualized by this chart projecting massive growth in its target market.

(Source: YIAZOU – Substack)

4. INNIO & Volta Grid

Company: INNIO & Volta Grid

Installation Capacity: 2.3 GW

Applications: Supplying 92 gas power packs for a major data center, providing a scalable on-site power solution.

Source: INNIO Secures Largest Order in Company History with Volta Grid …

Power Is Top Factor for Data Center Siting

This chart highlights the primary challenge in data center development, which the on-site power solutions from INNIO and Volta Grid are specifically designed to solve.

(Source: The Block)

5. Bloom Energy

Company: Bloom Energy

Installation Capacity: Up to 1 GW

Applications: Grid-independent power for AI data centers using solid oxide fuel cells through an agreement with American Electric Power (AEP).

Source: AI’s Achilles’ Heel Just Became a $50 Billion Opportunity

6. x AI

Company: x AI

Installation Capacity: Not Specified

Applications: Integrating on-site gas turbines to power its “Colossus 1 and 2” data centers in Memphis, Tennessee.

Source: AI Data Centers, Desperate for Electricity, Are Building Their Own …

7. Homer City Redevelopment

Company: Homer City Redevelopment

Installation Capacity: Up to 4.4 GW

Applications: Redeveloping a former coal plant site to deliver power to support AI-driven hyperscale data centers.

Source: Project Overview – Homer City Redevelopment

Bitcoin Miners’ Power Assets Compared for AI

The Homer City redevelopment represents one of the largest power assets being repurposed for AI, and this chart provides context by comparing its scale to other miners’ assets.

(Source: Medium)

8. Brookfield

Company: Brookfield

Installation Capacity: $10 billion investment commitment

Applications: Capital allocation toward building the energy and digital backbone required by the AI economy.

Source: [PDF] building the backbone of AI. – Brookfield

Chart Maps AI Giants’ Infrastructure Investments

This chart illustrates the competitive landscape of large-scale AI infrastructure investments, providing the backdrop for the section’s discussion of investment firm Brookfield’s strategy.

(Source: The Business Engineer)

9. Microsoft

Company: Microsoft

Installation Capacity: 900 MW

Applications: Building a new AI data center facility requiring direct involvement in power infrastructure development.

Source: Detailed explanation of the U.S. data center frenzy: 45 GW, $2.5 …

NVIDIA Data Center Revenue Explodes in Q2’25

Microsoft is a primary customer and driver of NVIDIA’s staggering data center revenue growth, making this chart essential for understanding Microsoft’s AI build-out and supply chain.

(Source: Compounding Your Wealth – Substack)

10. Williams Companies

Company: Williams Companies

Installation Capacity: Not Specified

Applications: Pivoting natural gas infrastructure assets to provide reliable power to data centers through long-term power purchase agreements.

Source: 3 Stocks Powering the $25 Trillion AI Energy Boom | Investing.com

Table: Top Company Pivots to AI Energy Infrastructure (2024-2025)

| Company | Market Segment | Key Project / Deal | Announced Capacity (GW) | Investment Value ($B) |

|---|---|---|---|---|

| Homer City Redevelopment | Infrastructure Redevelopment | Redevelopment of former coal plant site for AI data centers | 4.4 | Not Specified |

| INNIO & Volta Grid | On-Site Power Generation | Supply of 92 gas power packs for a major data center | 2.3 | Not Specified |

| Bloom Energy | On-Site Power Generation | Agreement with AEP to supply solid oxide fuel cells | 1 | Not Specified |

| Microsoft | Hyperscaler / Self-Build | Construction of a new AI data center facility in Wisconsin | 0.9 | Not Specified |

| Applied Digital | Digital Infrastructure | AI data center lease agreement with Core Weave | 0.25 | Not Specified |

| Brookfield | Investment & Asset Management | Strategic investment to support AI infrastructure development | Not Specified | 10 |

| Hut 8 | Crypto-to-AI Pivot | Google-backed deal to power AI data centers | Not Specified | 7 |

| x AI | Hyperscaler / Self-Build | Building data centers with on-site gas turbines | Not Specified | Not Specified |

| IREN | Crypto-to-AI Pivot | Aggressive pivot of data center assets to AI cloud hosting | Not Specified | Not Specified |

| Williams Companies | Traditional Energy | Signing long-term PPAs to supply power to data centers | Not Specified | Not Specified |

On-Site Power Adoption, INNIO’s 2.3 GW Order Signals Grid Bypass

The trend toward on-site power is attracting a diverse set of companies, signaling that it is now a core strategic imperative, not a niche solution. The players range from hyperscalers like Microsoft and x AI building their own power infrastructure to traditional energy firms like Williams Companies pivoting to serve data centers directly. Furthermore, former crypto miners such as Hut 8 and IREN are repurposing their expertise in high-density energy procurement for the more lucrative AI market. This widespread adoption across the value chain, from tech giants to asset managers like Brookfield, which has committed $10 billion, confirms that bypassing grid limitations is critical for competitive AI development.

AI Energy Demand Projected to Near 1,000 TWh

The chart’s projection of massive AI energy demand provides the crucial ‘why’ behind the strategic shift towards on-site power and grid bypass detailed in this section.

(Source: GasTurbineHub)

North America Leads, Microsoft’s 900 MW Wisconsin Project

Geographically, North America, and particularly the United States, is the clear epicenter of this AI energy infrastructure buildout. The projects are strategically located across the country, from Microsoft’s 900 MW development in Wisconsin to x AI’s new data centers in Memphis, Tennessee, and the massive 4.4 GW Homer City Redevelopment in Pennsylvania. This concentration is driven by the colocation of major technology firms, the availability of land suitable for large-scale energy and data campuses, and access to natural gas infrastructure, which is a key fuel source for many of these on-site power solutions. The scale of these US-based projects establishes the region as the primary market for AI-related energy investment through 2025.

$10 B Investment, Brookfield Validates AI Infrastructure

Recent deployments reveal that on-site power technologies like gas turbines and fuel cells are commercially mature, but they are now being implemented at an unprecedented scale. The innovation lies not in the core technology itself but in the business models and financial commitments backing these projects. INNIO’s 2.3 GW order, the largest in its history, and Bloom Energy’s 1 GW pact with AEP are not demonstration projects; they are large-scale commercial deployments intended to solve immediate, gigawatt-scale power deficits. The involvement of major financial players, highlighted by Brookfield’s $10 billion investment strategy and the $7 billion deal backing Hut 8, signifies that the market for dedicated AI power infrastructure has moved firmly into a phase of rapid, large-scale commercialization.

Bloom Energy 1 GW Pact Signals Future SMR Integration (2025-2030)

The critical path for AI energy infrastructure will involve a strategic diversification of on-site generation technologies, moving beyond current natural gas solutions toward carbon-free, firm power sources to meet both ESG goals and extreme reliability requirements. If the current trajectory of multi-gigawatt projects continues, the strain on natural gas supply chains will intensify, making alternative baseload power increasingly necessary. Watch for hyperscalers and their energy partners to formalize plans for next-generation power sources, particularly Small Modular Reactors (SMRs). The following signals indicate this shift is already underway:

- The sheer scale of projects like the 4.4 GW Homer City redevelopment establishes a new benchmark for power demand at a single site, a scale that aligns with the output of future SMR deployments.

- Strategic pivots by companies like Bloom Energy with its fuel cells provide a bridge technology, but the long-term need for 24/7, zero-carbon power points directly toward nuclear.

- Deepening partnerships between tech companies and energy specialists, such as the Google-backed deal for Hut 8, will likely evolve to include nuclear technology developers as SMRs advance toward commercial viability.

- Expect major hyperscalers to announce formal SMR evaluation studies or strategic partnerships by late 2025, as they plan for data center power needs extending into the next decade.

The questions your competitors are already asking

This report covers one angle of the market shift toward on-site power generation for AI data centers. The questions that matter most depend on your work.

- What is the status of landmark deals like INNIO’s 2.3 GW order with Volta Grid and Bloom Energy’s 1 GW pact? Are they progressing from announcement to deployment?

- How are former Bitcoin miners like Hut 8 and IREN successfully repurposing their energy infrastructure to capture the AI power demand?

- How do gas engine solutions, like those from INNIO, compare to fuel cells from Bloom Energy for powering AI data centers?

- Which data center operators and hyperscalers are most aggressively adopting on-site power generation over grid reliance?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.