PJM Grid Interconnection Failure, 220 GW New Apps vs. 3 GW Connected, a 60 GW Shortfall, and 51 Fast-Tracked Projects (2021 to 2026)

PJM Interconnection Risks: 298 GW Queue Creates Systemic Failure

The PJM Interconnection queue has ceased to be a reliable indicator of future power generation and is now a primary risk to grid stability, transforming from a project pipeline into a systemic dam. An overwhelming volume of proposed generation, which grew from 259 GW in 2021 to nearly 300 GW by mid-2023, is effectively blocked from reaching the grid by procedural and physical bottlenecks. The staggering gap between the 220 GW of new applications received in a single 2026 cycle and the mere 3.045 GW of capacity that successfully came online in all of 2025 illustrates a system failing its core function, creating false market signals and jeopardizing the region’s ability to meet demand.

- Before 2025, the queue swelled under a “first-come, first-served” model that encouraged speculative entries, resulting in a backlog of over 2, 700 projects and wait times averaging four years. This historic backlog was dominated by solar, wind, and storage projects, which comprised over 90% of the queued capacity.

- The reformed “cluster study” process, intended to streamline connections, was immediately overwhelmed in April 2026 with 811 new projects representing 220 GW. This influx demonstrates immense pent-up developer interest but also proves the new process is not a panacea for the underlying constraints.

- The most telling metric of failure is the connection rate. The new applications in the first 2026 cycle represent more than 72 times the total capacity PJM managed to interconnect in the entire previous year, confirming the queue is a logjam, not a functioning pipeline.

- High project attrition further distorts the queue’s value as a planning tool. In 2025 alone, developers cancelled 38 GW of projects, a clear signal that the majority of queued capacity is not commercially viable under current interconnection rules and cost structures.

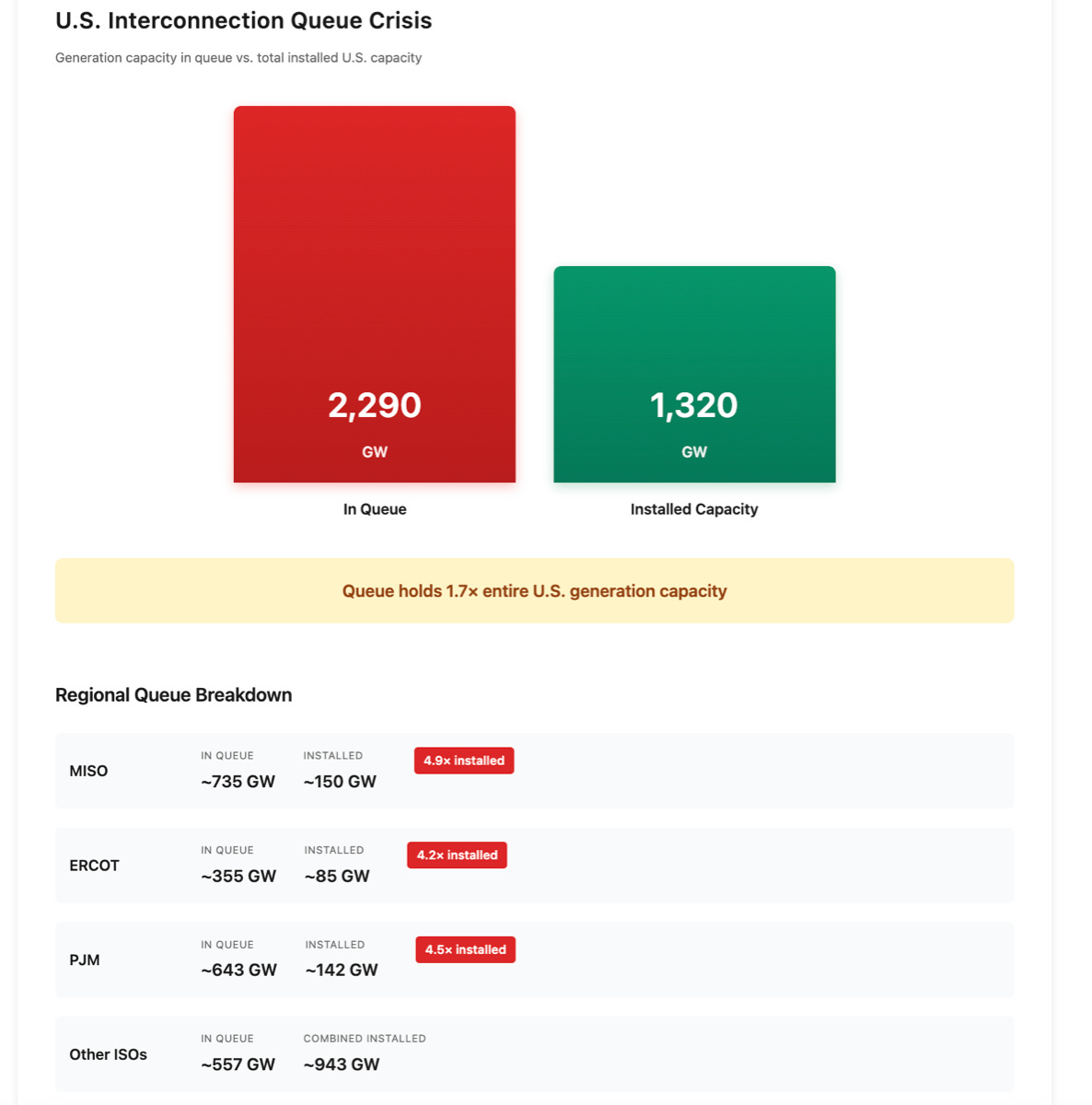

PJM Queue Hits 643 GW, 4.5x Installed Capacity

The chart visualizes the scale of the PJM interconnection queue, directly supporting the section’s focus on the systemic risk created by its massive size.

(Source: Energy Industry Insights from Avanza Energy – Substack)

38 GW in Cancellations, PJM Project Withdrawals Spike (2021 to 2026)

Massive project cancellations within PJM are not an anomaly but a predictable outcome of a broken system where prohibitive and uncertain interconnection costs make most queued projects economically unviable. The withdrawal of 38 GW in 2025, largely triggered by a deadline for developers to post full security deposits, exposed the speculative nature of the queue. This high attrition rate, where nationally only about one in four projects reach commercial operation, is a primary driver of the disconnect between PJM’s hundreds of gigawatts of queued projects and its looming capacity shortfall.

- The primary driver for withdrawals is the high and unpredictable cost of network upgrades assigned to developers late in the study process. These costs can turn an otherwise profitable project into a financial liability, forcing its cancellation.

- PJM’s reforms, which began to take effect in 2025, aim to reduce speculation by imposing higher deposits and stricter readiness milestones. The mass cancellation event on October 21, 2025, demonstrated this is working to weed out non-serious projects, but it also starkly revealed how much of the queue was phantom capacity.

- Between 2021 and 2024, the slow, serial study process allowed non-viable projects to linger for years, clogging the system for more mature projects behind them. The new cluster study approach is designed to identify these upgrade costs earlier.

- The scale of withdrawals is so large that it negates much of the potential new supply. The 38 GW cancelled in 2025 is more than ten times the amount of new generation that successfully connected in the same year, highlighting the immense waste and inefficiency of the process.

Table: PJM Project Cancellations and Market Signals

| Event or Signal | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Project Cancellations | 2025 | A total of 38 GW of generation projects were cancelled in PJM’s queue. A significant portion of these withdrawals was triggered by an October 21, 2025, deadline for posting full security deposits, forcing speculative projects out. | Cleanview |

| Capacity Price Spike | 2025/2026 Delivery Year | The PJM capacity auction cleared at a record $329.17/MW-day. The total market cost reached $16.1 billion, with data center demand accounting for a $9.3 billion increase, reflecting a market pricing in the lack of new supply. | Electricity Rates.com |

| First-Ever Capacity Shortfall | 2027 Delivery Year | The 2027 capacity auction resulted in a 6 GW shortfall, the first time in PJM’s history it failed to procure enough resources to meet reliability targets. This is a direct consequence of the interconnection bottleneck. | Introl |

| Interconnection Queue Pause | 2022 – 2024 | In early 2022, PJM was forced to implement a two-year pause on reviewing most new project applications to work through its massive backlog, effectively freezing new market entry. | pv-magazine-usa |

PJM’s Special Reforms, 9.3 GW Fast-Tracked via RRI Initiative

The proliferation of special, expedited interconnection tracks within PJM is the clearest admission that its standard process is fundamentally broken and incapable of meeting urgent grid reliability needs. These workarounds, such as the one-time Reliability Resource Initiative (RRI) that fast-tracked 9.3 GW of “shovel-ready” projects in May 2025, are necessary acts of triage. However, they underscore the failure of the primary queue to perform its core function, creating a confusing, multi-tiered system instead of fixing the underlying problem.

- The Reliability Resource Initiative (RRI) was a special, one-time process created to bypass the standard queue for projects deemed critical for near-term reliability. PJM selected 51 projects out of 94 applications, fast-tracking over 9.3 GW of capacity.

- The Expedited Interconnection Track (EIT), proposed in March 2026, is another workaround designed specifically to serve large new loads like data centers. It would allow up to 10 generation projects per year to bypass the queue to directly supply these new customers.

- In February 2026, FERC approved a streamlined process for new generation to replace retiring units, allowing them to use existing grid connection rights and avoid the main queue entirely.

- While PJM’s primary reform was the shift to a cluster study model in 2025, the fact that it required these additional ad-hoc measures almost immediately proves the cluster approach alone is insufficient to address the speed and scale of the crisis.

Table: PJM Interconnection Reform Initiatives

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Reformed Queue Process (Cluster Study) | Apr 2026 | Shifted from “first-come, first-served” to “first-ready, first-served” cluster studies. The first cycle immediately attracted 220 GW of applications, indicating it may still be overwhelmed. | PJM Inside Lines |

| Reliability Resource Initiative (RRI) | May 2025 | A one-time, fast-track process for shovel-ready projects to address near-term reliability. It advanced 51 projects totaling 9.3 GW. | PA Environment Daily |

| Expedited Interconnection Track (EIT) | Mar 2026 | A proposed new process to allow generators to bypass the main queue to serve large new loads like data centers, limited to 10 requests per year. | White & Case |

| Replacement Generation Process | Feb 2026 | A FERC-approved streamlined process allowing new generation to replace retiring units by using their existing grid connection rights, bypassing the main queue. | Public Power |

PJM Territory, Data Center Demand Drives Reliability Crisis

The PJM region, particularly states with significant data center growth like Virginia, has become the epicenter of a collision between soaring electricity demand and an inadequate grid supply pipeline. The rapid, concentrated load growth from the hyperscaler and AI industries is exposing the frailty of the interconnection process, turning a procedural delay into an imminent reliability crisis. PJM’s own forecasts predict a potential 60 GW power shortfall within a decade, driven almost entirely by this new demand colliding with a grid that cannot add new resources fast enough.

- PJM projects that by 2030, regional electricity demand will climb by 32 GW, with a staggering 30 GW of that increase originating from data centers alone. This has reversed a long-term trend of flat demand in the region.

- The strain is most acute in Northern Virginia, home to the world’s largest concentration of data centers. The challenges faced by the regional utility, Dominion Energy, in serving this load have become a focal point for the entire PJM system and a key driver of the need for improved grid infrastructure.

- The market is already pricing in this crisis. The 2027 capacity auction resulted in a 6 GW shortfall, the first in PJM history. This failure to procure sufficient capacity is a direct result of retiring thermal plants not being replaced quickly enough due to the interconnection logjam.

- In February 2026, PJM officials issued a severe warning of a potential 60 GW supply deficit over the next decade if the current trends of demand growth, generation retirements, and slow interconnection persist.

Data Center Power Delays Reach 7 Years

This chart provides a specific, quantifiable example of the reliability crisis driven by data center demand, showing the extreme power-on-line delays that result.

(Source: Energy Industry Insights from Avanza Energy – Substack)

Grid Planning Maturity: PJM’s Reactive Model Fails Commercial Scale

The PJM interconnection crisis stems from a fundamental immaturity in its planning process, which remains reactive and unable to cope with the scale and speed of the modern energy transition. The system, designed for an era of a few large, centralized power plants, has collapsed under the weight of thousands of smaller, geographically dispersed renewable and storage projects. The constant need for ad-hoc reforms and emergency workarounds is definitive proof that PJM’s core process is not mature enough to manage a commercially-driven, large-scale grid modernization.

- Between 2021 and 2024, PJM’s “first-come, first-served” serial process became a critical bottleneck. It was poorly suited for the influx of renewable projects, which often have different study needs and are more sensitive to interconnection cost uncertainty than traditional thermal plants.

- The transition to a “first-ready, first-served” cluster model in 2025 was a step toward maturity, but its immediate overload with 220 GW of new requests shows it is still a reactive mechanism, studying what developers propose rather than proactively planning for what the grid needs.

- A stark signal of this immaturity is the shift in queue composition in the first reformed cycle. The queue was dominated by natural gas (105.8 GW) and storage (67.5 GW), with renewables plummeting. This indicates the current system, with its high costs and long waits, is now selecting for dispatchable, high-capital projects, not necessarily the lowest-cost or cleanest energy.

- True process maturity would involve proactive, long-range transmission planning that anticipates load growth and generation pockets, building out the grid ahead of interconnection requests. PJM’s current model places the entire burden of grid expansion on individual generator projects, a model that has clearly failed.

SWOT Analysis, PJM’s Reliability Mandate vs. Interconnection Failure

PJM’s primary strength as the nation’s largest grid operator with a mandate to ensure reliability is being directly threatened by the systemic weakness of its interconnection process. This has created an opportunity for new, dispatchable generation to command high prices, but it poses a severe threat to long-term reliability and affordability for the 65 million people PJM serves.

- Strengths: Established capacity market designed to ensure resource adequacy, central role in the U.S. energy system, and demonstrated willingness to reform its processes.

- Weaknesses: An unmanageable interconnection queue, extremely low project completion rates, and a reactive planning model that cannot keep pace with market and demand shifts.

- Opportunities: Record-high capacity prices create a powerful incentive for investment in new firm resources, including gas, storage, and potentially advanced nuclear, while FERC Order No. 2023 provides regulatory backing for further reform.

- Threats: An imminent and officially recognized capacity shortfall, soaring electricity costs passed on to consumers, and the risk of a full-blown reliability crisis if demand growth continues to outpace new generation connections.

Table: SWOT Analysis for PJM Grid Interconnection

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Managed a large, complex grid with a functioning capacity market. | Initiated major interconnection reforms (cluster studies) and special initiatives (RRI). FERC Order No. 2023 provided federal support. | The system’s strength is its ability to recognize a crisis and initiate reforms, though their effectiveness is still in question. The capacity market is functioning as designed by sending extreme price signals. |

| Weaknesses | Queue backlog grew to unmanageable levels (approaching 300 GW) under a slow, serial process. Wait times stretched to 4+ years. | The first reformed cycle was immediately flooded with 220 GW of new requests. The first-ever capacity shortfall (6 GW) occurred for the 2027 delivery year. | The weakness was validated: changing the study process did not fix the underlying mismatch between generation interest, transmission availability, and demand growth. The problem is physical, not just procedural. |

| Opportunities | A massive influx of renewable and storage projects signaled strong developer interest in decarbonization. | Record capacity prices ($329.17/MW-day) create a powerful business case for new, firm generation. New rules (EIT) create direct paths for generators to serve data centers. | The opportunity shifted from a theoretical “green transition” to a practical, high-priced market for any resource that can get online quickly and guarantee reliability, especially dispatchable power. |

| Threats | A growing, but largely theoretical, risk of future reliability issues due to retiring thermal plants and slow renewable interconnection. | The threat became acute and immediate, with PJM officially forecasting a potential 60 GW shortfall and data center load growth becoming a primary driver of grid instability. | The threat was validated and accelerated. The theoretical risk of a “reliability gap” became a certainty, with PJM now managing a declared crisis. |

PJM 2026 Outlook: Capacity Price Spikes Signal Need for Firm Power

The most critical forward-looking signal is that PJM’s capacity market will continue to send extreme price signals until the physical bottleneck of interconnection is resolved, creating a powerful incentive for dispatchable resources that can guarantee reliability. The market has fundamentally shifted from rewarding the lowest-cost proposed megawatt to rewarding the first available and most reliable megawatt, a trend that will define investment and development in the PJM region for the foreseeable future.

- If this happens: If PJM cannot significantly accelerate the connection of the 63 GW of projects that already have signed or offered interconnection agreements, the capacity shortfalls will worsen.

- Watch this: The results of the next PJM capacity auction will be the most important near-term signal. Watch for continued price volatility and which resource types (e.g., gas, storage, demand response) successfully clear, as this will indicate what the market believes can actually be built.

- This could be happening: A bifurcation of the development market is likely. Developers with dispatchable projects (natural gas, long-duration storage) or those using queue-skipping mechanisms (like the replacement generation rule) will find a clear path to market. Meanwhile, standalone renewable projects without a clear, near-term interconnection path will face a “valley of death, ” unable to secure financing amid years of uncertainty.

Data Centers Moving Off-Grid with BTM Power

The chart illustrates a market response to the lack of reliable grid power, showing how the “need for firm power” is driving major consumers like data centers to seek alternative, off-grid solutions.

(Source: Energy Industry Insights from Avanza Energy – Substack)

The questions your competitors are already asking

This report covers one angle of the PJM Interconnection’s grid stability risks. The questions that matter most depend on your work.

- What is actually happening with PJM’s reformed ‘cluster study’ process since its April 2026 launch?

- What is the outlook for solar, wind, and storage deployment in the PJM territory by 2030, given the current interconnection backlog?

- Which of the 2,700 projects in PJM’s historic backlog are at the highest risk of withdrawal, and which have a viable path to interconnection?

- What are the opportunities for transmission upgrades and grid-enhancing technologies (GETs) to alleviate PJM’s interconnection bottlenecks?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.