AI PCB Supply Crunch, $27 B Market Faces 45% Cost Hikes Amid Shortages (2025-2027)

AI-Driven Demand Creates a Structural PCB and CCL Supply Deficit

The global electronics supply chain is confronting a structural deficit in high-performance Printed Circuit Boards (PCBs) and Copper Clad Laminates (CCLs), creating a defining constraint on the deployment of AI infrastructure. Before 2025, the PCB market grew in line with general electronics demand. However, the post-2025 explosion in AI server requirements has created a demand shock that existing and planned manufacturing capacity cannot meet. This is not a cyclical inventory issue but a fundamental mismatch between the exponential need for complex, high-layer-count boards and a supply chain with long, linear capital investment cycles.

- The global AI server PCB market is projected to grow from $3.1 billion in 2024 to $27.1 billion by 2027, with growth rates exceeding 113% in 2026. This reflects a massive technical upgrade, not just a volume increase.

- By 2026, AI servers are expected to command over 25% of the total PCB market value, a sharp increase from 15% in 2025. This rapid reallocation of capacity is starving other electronics sectors.

- The technical demands have escalated dramatically; while standard servers in the 2021-2024 period used 10-12 layer boards, AI accelerators in 2026 require boards with 30-40+ layers and superior thermal properties, driving prices up by as much as 75 x on a per-area basis.

- The strain is evident in lead times, which have extended to six months for high-end CCLs as of March 2026, forcing suppliers to implement quota systems to manage overwhelming demand.

AI Hardware Creates Upstream Material Shortages

The section discusses an AI-driven supply deficit for PCBs and CCLs. This chart directly illustrates this by linking AI hardware to upstream material shortages, which is a synonym for a supply deficit.

(Source: semivision – Substack)

$1.1 B Investment from Zhen Ding Technology Highlights a Lagging Supply Response

Major manufacturers are committing significant capital to address the supply deficit, but these investments will not provide relief in the near term. The 18 to 24-month lead time for constructing and commissioning new advanced PCB and CCL facilities means that capacity expansions announced in 2025 will only begin to impact the market in late 2026 or 2027, failing to meet the immediate demand surge. This lag ensures suppliers will retain pricing power and that procurement managers will face a constrained environment for the foreseeable future.

- In August 2025, Zhen Ding Technology announced a major $1.1 billion expansion of its Huai’an Park facility in China to boost production of high-end PCBs, signaling a direct response to the AI-driven demand.

- SYRMA is investing up to $48 million in a new PCB manufacturing facility in India, with the first phase expected to be completed by December 2026. This highlights the global nature of the capacity race.

- The equipment needed to build these factories is itself a bottleneck. As of April 2026, lead times for critical manufacturing equipment like lamination presses stretched to two years, compounding delays in bringing new supply online.

- These capital-intensive projects, often requiring upwards of $50 million per facility, create high barriers to entry and limit the market’s ability to react quickly to demand shocks.

Taiwan Tech Firms Show Massive AI Supply Chain Growth

The section highlights a major investment by a Taiwanese firm (Zhen Ding) as part of a lagging supply response. This chart’s headline about Taiwanese firms’ supply chain growth provides the broader context for this specific investment, linking it to the overall AI-driven expansion in the region.

(Source: Atlas.ML – Substack)

Table: Capital Investments in PCB & CCL Manufacturing Capacity

| Company | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Zhen Ding Technology (Avary Holding) | Aug 2025 | Announced a ~$1.1 Billion (RMB 8 billion) expansion of its Huai’an Park facility in China to increase production of high-end PCBs for AI and other applications. | Printed Circuit Engineering Association Magazine |

| SYRMA | Feb 2026 | Phase 1 of a multi-phase expansion plan for PCB manufacturing in India, with an investment of $43 M – $48 M (Rs 3.6–4.0 bn) expected to be completed by December 2026. | [PDF] PL Capital |

| WIN | Sep 2025 | Announced a ~$60 Million investment for a new copper-clad laminate (CCL) facility in Karnataka, India, to bolster the domestic supply chain. | Printed Circuit Engineering Association Magazine |

GCE, Tripod Lead PCB Supplier Revenue Race

This section is a table about capital investments in manufacturing capacity. A chart showing the competitive revenue landscape (‘revenue race’) of key PCB suppliers provides context for why these capital investments are being made—to gain market share and leadership.

(Source: digitimes)

Taiwan vs. China, Shifting PCB Supply Chains and US Trade Policy

Geopolitical tensions and strategic industrial policies are actively reshaping the global PCB manufacturing map. While mainland China dominated global PCB output in the 2021-2024 period, accounting for over 56% of production, the post-2025 era is defined by a strategic diversification away from this concentration. US tariff policies and a focus on supply chain resilience are accelerating the rise of Taiwan and Southeast Asia as critical hubs for high-end PCB and CCL production.

- By 2025, Taiwan surpassed mainland China as the largest source of PCB imports to the United States, a direct result of tariff-driven supply chain realignment. Taiwanese firms have become the key alternative for US-based companies.

- The US government is actively supporting domestic production through legislation like the Bipartisan PCBs Act and the CHIPS Act’s Advanced Manufacturing Investment Credit, which offers a 25% tax credit for such investments.

- India is also emerging as a contender, approving seven projects worth $625 million under its Electronics Component Manufacturing Scheme (ECMS) to foster a local ecosystem and reduce reliance on imports.

- Despite these diversification efforts, the conflict in the Middle East and ongoing trade disputes continue to disrupt shipping and inflate raw material costs, demonstrating the fragility of the global supply chain.

Geopolitics to Create a Split Semiconductor World

The section focuses on the geopolitical tensions between Taiwan and China and their effect on the PCB supply chain. The chart’s headline is a perfect thematic match, describing the macro trend of a ‘split semiconductor world’ that directly encompasses the specific issue discussed in the section.

(Source: Medium)

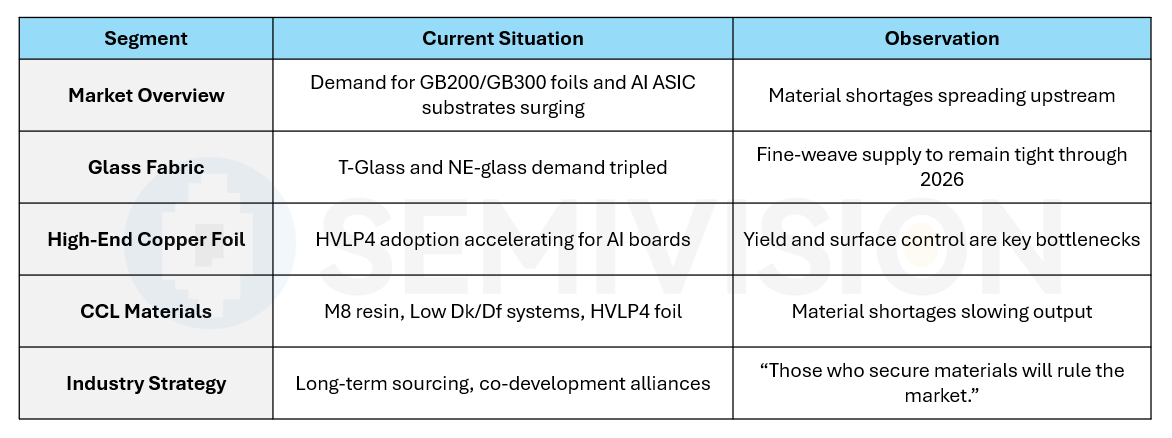

Advanced CCL Materials, M 7-M 10 Grade Shortages Create Production Gaps

The bottleneck in the AI infrastructure supply chain is not in the mature technology of PCB fabrication (TRL 9) but in the availability of the specialized, high-performance materials required. The shift from standard FR-4 grade materials, which were sufficient for most applications before 2025, to ultra-low-loss materials (rated M 7 to M 10) for AI servers has created a critical scarcity. The supply of these advanced materials is highly concentrated and cannot be scaled quickly, forming the core of the 2026 bottleneck.

- High-performance materials like M 7-M 10 grades, essential for next-generation AI accelerators, are experiencing severe lead time pressure of up to six months and are often available only through allocation or at “spot zero” availability.

- Persistent shortages of high-end glass fiber cloth, a key ingredient for these advanced laminates, are expected to cloud the 2026 AI chip outlook, directly limiting CCL production.

- The cost premium for these materials is extreme. Ultra-low loss materials cost 6-20 x more than standard FR-4, with some high-end CCL grades seeing price increases of 20% to 40% alone.

- Manufacturing complexity for high-layer count boards with precise signal integrity also constrains effective supply, with production yield losses for AI server boards expected to remain high at 35-38% through 2026-2027.

Copper Foil Accounts for 42% of CCL Cost

The section details shortages in advanced CCL materials. This chart is highly relevant as it breaks down the cost structure of CCLs, highlighting a major component (copper foil). This cost information is critical when discussing advanced, high-cost materials and potential production gaps.

(Source: TrendForce)

SWOT Analysis, PCB and CCL Market Strengths vs. Supply Risks

The market for high-performance PCBs and CCLs is defined by the tension between unprecedented, technology-driven demand and severe structural constraints on the supply side. Before 2025, the market was characterized by incremental growth and predictable supply dynamics. The AI-driven shift has introduced both immense opportunity for suppliers and systemic risk for the entire hardware ecosystem.

- Strengths: The primary strength is the inelastic, non-discretionary demand from hyperscalers like Amazon, Microsoft, and Google, who are locked into massive capital expenditure cycles for AI data centers.

- Weaknesses: The industry’s fundamental weakness is its slow reaction time, stemming from long capital investment cycles (18-24 months) and chokepoints in the upstream supply of raw materials like specialty glass fiber.

- Opportunities: The supply crunch creates significant opportunities for technological innovation in materials science (e.g., glass core substrates) and for geographic diversification of manufacturing, supported by government incentives in the US, India, and other regions.

- Threats: The greatest threats are geopolitical, including US-China trade restrictions that could sever critical supply lines, and external shocks like regional conflicts that disrupt logistics and inflate raw material costs.

AI Boom Creates Semiconductor Supply Bottlenecks

This section is a SWOT analysis, weighing strengths against risks. The chart’s headline perfectly captures this duality: the ‘AI Boom’ represents an opportunity and strength, while ‘Supply Bottlenecks’ represent a risk and threat.

(Source: Medium)

Table: SWOT Analysis for the High-Performance PCB and CCL Market

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Steady demand from consumer electronics, automotive, and traditional data centers. | Explosive, high-margin demand from AI servers requiring complex, high-value boards. Pricing power shifts to suppliers. | The value proposition shifted from volume to technical capability. AI server demand is validated as a structural, long-term growth driver. |

| Weaknesses | Fragmented market with price competition. Reliance on established supply chains, primarily in China. | Inability to scale capacity quickly due to 18-24 month fab construction times. Severe shortages of advanced materials (glass fiber, low-loss resins). | The weakness of a “just-in-time” global supply chain was validated. Long investment cycles are a structural barrier, not a temporary issue. |

| Opportunities | Incremental improvements in manufacturing efficiency and material performance. Geographic concentration was seen as a cost advantage. | Government incentives (US CHIPS Act, India’s ECMS) promoting reshoring. Development of new technologies like glass core substrates. | Geopolitical risk has become a primary driver of investment, creating opportunities for new manufacturing hubs outside of China. |

| Threats | Cyclical downturns in electronics demand. Raw material price volatility. | Geopolitical conflict (US-China trade war, Middle East disruptions). Export controls on critical manufacturing equipment and materials. | The threat of supply chain weaponization and logistics disruption has been validated as a primary risk to the entire electronics industry. |

Supplier Landscape for Critical PCB Raw Material

This section is a table-based SWOT analysis. A chart illustrating the ‘Supplier Landscape’ for critical raw materials is an ideal data source for such a table, as it informs the analysis of threats (e.g., supplier concentration) and opportunities in the market.

(Source: TrendForce)

6-Month Lead Times Confirm PCB Bottlenecks Will Stall AI Deployment

The most critical forward-looking indicator is that hardware bottlenecks, particularly in foundational components like PCBs, are now expected to persist through 2027-2028. If AI accelerator production continues to scale while PCB and CCL capacity remains constrained, the availability of these boards will become the primary gating factor for AI server deployment. Watch for quarterly earnings reports from hyperscalers for upward revisions to CAPEX, which will further tighten supply, and for pricing announcements from key Asian CCL manufacturers like Kingboard and SYTECH as a real-time barometer of the supply/demand imbalance.

- If this happens: Lead times for high-end CCLs extend beyond the current six months.

- Watch this: Major PCB and CCL suppliers like ITEQ or Nan Ya Plastic may announce further price hikes or move more product lines to an allocation-only basis.

- These could be happening: AI server OEMs and hyperscalers begin signing multi-year, high-volume contracts to secure supply, or announce strategic investments directly into material suppliers to de-risk their build-out plans. This would signal a long-term structural shift in procurement strategy.

The questions your competitors are already asking

This report covers one angle of the AI hardware component supply chain. The questions that matter most depend on your work.

- Which PCB and CCL manufacturers are gaining or losing ground in the high-end AI server market?

- What is the outlook for the AI server PCB supply/demand gap through 2027?

- What is the cost breakdown of a 2026-era AI accelerator board, from raw CCLs to final assembly?

- Who are the key suppliers of high-speed, low-loss CCLs for the AI PCB market?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.