Top 10 Data Center Regulations: Virginia’s New Rules, 10 Regions Face Grid Strain (2024-2025)

An analysis of regulatory actions in 2024 and 2025 reveals the end of the “build-anywhere” era for data centers. The explosive energy demand from AI workloads is the primary catalyst, forcing governments to shift from offering incentives to implementing significant restrictions. The dominant theme for 2025 is the transition to an energy-constrained market, where grid availability, not just land or fiber, has become the principal gating factor for development. Key markets like Virginia, which hosts 13% of global capacity, are moving away from streamlined approvals, as seen with the March 18, 2025, vote in Loudoun County to eliminate “by-right” development. This pivot towards stricter regulations, financial penalties, and outright moratoriums is now a defining feature of the data center landscape.

1. Virginia, USA: End of “By-Right” Development

Location: Virginia, USA

Regulatory Action: The Loudoun County Board of Supervisors eliminated “by-right” development for data centers, subjecting new projects to heightened public and regulatory scrutiny.

Key Drivers: Severe strain on the power grid managed by Dominion Energy and organized opposition from 42 local groups concerned about noise, land use, and environmental impact.

Source: Loudoun County, Virginia, Eliminates By-Right Data Center …

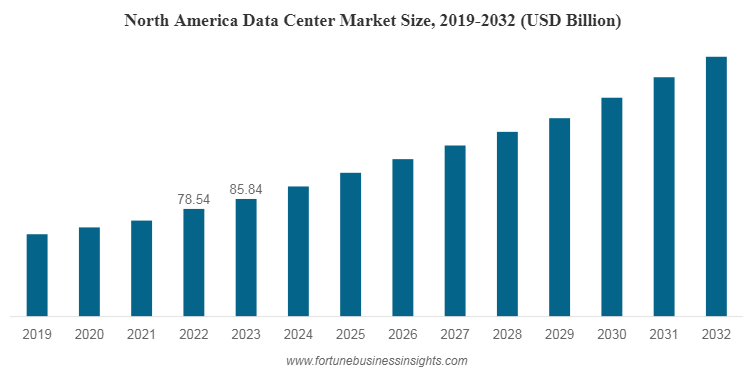

North America Data Center Market Shows Strong Growth

This chart illustrates the strong market growth in North America, which is the direct cause of the regulatory pressure in Virginia, the continent’s largest data center market, leading to the end of “by-right” development.

(Source: Fortune Business Insights)

2. Ireland: De Facto Moratorium on Grid Connections

Location: Ireland

Regulatory Action: State-owned grid operator Eir Grid implemented a de facto moratorium on new data center grid connections, especially in the saturated Dublin market.

Key Drivers: Extreme grid constraints and the risk that unchecked data center growth posed to the stability of the national electricity network.

Source: Unlocking the Data Center opportunity in KSA – Roland Berger

3. Singapore: Highly Selective Permitting

Location: Singapore

Regulatory Action: A government moratorium on new data center construction has evolved into a highly selective process, prioritizing projects with top-tier efficiency and sustainability metrics.

Key Drivers: Scarcity of land and limited domestic energy generation capacity, aligning new development with long-term climate goals.

Source: an overview of use and impact of data centres – UNECE

Data Center Industry Shifts to New Technologies

The section describes Singapore’s highly selective permitting process. A chart showing the industry’s shift to new, more efficient technologies (e.g., advanced cooling) illustrates the type of innovation that would be favored by such a selective process in a resource-constrained environment.

(Source: MarketsandMarkets)

4. Texas, USA: New Rules for Large Loads

Location: Texas, USA

Regulatory Action: The state passed Senate Bill 6 (SB-6) in May 2025 to regulate cost allocation for large loads. A subsequent law in June 2025 empowers grid operator ERCOT to disconnect large consumers during grid emergencies.

Key Drivers: Protecting the independent power grid from instability and preventing residential ratepayers from subsidizing grid upgrades for new data centers.

Source: Important Texas Regulatory Updates for Data Centers – Mayer Brown

Hyperscaler Capex to Approach $1 Trillion

The chart shows the massive capital expenditure by hyperscalers, which are the entities building the largest data centers. This directly relates to the section on Texas creating new rules for “large loads,” as hyperscaler investments are the primary source of these new, large demands on the grid.

(Source: Fortune)

5. Netherlands: Formal Growth Regulations

Location: Netherlands

Regulatory Action: The Amsterdam region, a major European hub, has enacted official regulations to manage data center growth and alleviate pressure on the local power grid.

Key Drivers: Local grid capacity limits and sustainability concerns, mirroring issues in other saturated European markets.

Source: Advancing Cloud and Data Infrastructure Markets – The World Bank

6. Illinois, USA: Legislative and Location Restrictions

Location: Illinois, USA

Regulatory Action: Lawmakers are pursuing new rules to manage grid impact and have passed laws restricting where new facilities can be built. This includes Senate Bill 94, the “Data Center Construction by Foreign Adversaries Act.”

Key Drivers: Concerns over grid stability, national security, and protecting consumers from rate hikes tied to grid expansion.

Source: Lawmakers seek ways to prevent data centers from straining Illinois …

7. Ohio, USA: Financial Pre-Payment for Upgrades

Location: Ohio, USA

Regulatory Action: A novel financial regulation requires data center developers to pre-pay 85% of the projected costs for necessary energy infrastructure upgrades.

Key Drivers: Shifting the significant financial risk of infrastructure expansion from the utility and its ratepayers directly onto the developer creating the demand.

Source: Inside Site Selection: Tackling the Barriers Slowing AI Data Center …

8. Arizona, USA: Development Suspensions

Location: Arizona, USA

Regulatory Action: State and local officials have passed laws to suspend new data center development or impose stricter location-based restrictions.

Key Drivers: Primary concerns over water consumption in an arid region, compounded by the electrical grid strain from large-scale projects.

Source: As internet data centers multiply, efforts to control them are growing

9. Georgia, USA: Proposed Cost-Bearing Legislation

Location: Georgia, USA

Regulatory Action: The state is actively considering legislation that would require data center developers to bear the full costs of new energy infrastructure their facilities require.

Key Drivers: Protecting residential and commercial ratepayers from subsidizing the massive grid buildout needed to support the state’s growing data center industry.

Source: States push new rules as data centers strain electric grids – EHN

US Data Center Market Shows Strong Growth

The chart depicting strong growth in the overall US data center market provides the context for why individual states like Georgia are now considering legislation to shift infrastructure costs to developers to manage this rapid expansion.

(Source: Global Market Insights)

10. United Kingdom: Grid Connection Stalemate

Location: United Kingdom

Regulatory Action: A de facto halt on new large-scale projects in the “Data Centre Alley” west of London due to a stalemate over grid connections, with multi-hundred-megawatt projects stalled.

Key Drivers: Severe grid congestion, where existing infrastructure is insufficient to support the power demands of new hyperscale data centers, leading to multi-year delays.

Source: Green Grid, Red Tape: How Regulation Holds Back (and Can …

Data Center Electricity Use to Double by 2030

The projection that data center electricity use will double provides a clear rationale for the “Grid Connection Stalemate” in the United Kingdom, as the grid struggles to accommodate such a significant increase in future demand.

(Source: Bessemer Venture Partners)

Table: Data Center Regulatory Actions (2024-2025)

| Location | Type of Action | Key Drivers | Status / Timeline |

|---|---|---|---|

| Virginia, USA | Zoning Ordinance Change | Grid Strain, Community Opposition | Enacted Mar 2025 |

| Ireland | De Facto Moratorium | Grid Capacity & Stability | Ongoing since 2024 |

| Singapore | Moratorium / Strict Permitting | Grid Capacity, Land Scarcity | Ongoing since before 2024 |

| Texas, USA | State Legislation (SB-6) | Grid Stability, Cost Allocation | Passed May/June 2025 |

| Netherlands (Amsterdam) | Official Regulations | Grid Strain, Sustainability | Implemented by 2025 |

| Illinois, USA | Proposed Legislation / Restrictions | Grid Strain, National Security | Active in 2025 |

| Ohio, USA | Financial Regulation (Pre-payment) | Cost Allocation, Infrastructure Risk | Implemented by 2025 |

| Arizona, USA | State Legislation (Suspension/Restriction) | Water Scarcity, Grid Strain | Enacted by 2024 |

| Georgia, USA | Proposed Legislation | Cost Allocation, Ratepayer Protection | Active in 2025 |

| United Kingdom | De Facto Moratorium (Grid Stalemate) | Grid Congestion & Bottlenecks | Ongoing in 2025 |

Data Center Market to Exceed $422B by 2032

This chart, showing the immense and growing financial scale of the data center market, provides the overarching context for a summary table of regulatory actions. A market of this size inevitably attracts significant regulatory attention globally.

(Source: Mordor Intelligence)

Data Center Regulation, States Shift Infrastructure Costs to Developers

A clear pattern emerging across the United States is the adoption of policies that shift the financial burden of grid expansion directly onto data center developers. This marks a strategic move away from socializing these costs across all ratepayers. Ohio is pioneering this with a requirement for developers to pre-pay 85% of infrastructure upgrade costs. Similarly, Texas passed SB-6 to create a new framework for cost allocation, ensuring that the massive loads from data centers do not destabilize the market or unfairly burden existing consumers. Georgia is now considering similar legislation. This trend indicates a maturing understanding among policymakers that while data centers can bring economic benefits, their unique infrastructure demands require a dedicated financial model to ensure equitable and sustainable growth.

11 US States Consider Data Center Restrictions

This chart is a perfect match for the section, as both focus on the widespread trend of US states implementing regulations and restrictions on data centers, often to manage infrastructure costs.

(Source: Visual Capitalist)

10 Global Hubs, Data Center Growth Cools in Saturated Markets

The geographic landscape for data center development is bifurcating. Primary, saturated markets are applying the brakes, while new regions are sought for their energy potential. The world’s largest market, Northern Virginia, is now a leader in regulatory friction. Major European hubs like Dublin and the Amsterdam region face de facto or official moratoriums driven by grid limitations. In Asia, Singapore‘s highly restrictive policies serve as a global benchmark for resource-constrained jurisdictions. This cooling in traditional hotspots, including the grid connection stalemate in the UK‘s “Data Centre Alley, ” is forcing a strategic migration of investment toward secondary and tertiary markets where power is more readily available, even if it means contending with less-developed fiber and labor pools.

Forecasts Show Surging Data Center Energy Use

This chart on surging energy use explains the core reason why growth is “cooling” in saturated markets, as mentioned in the section heading. These hubs are reaching their power capacity limits, forcing a slowdown.

(Source: Information Technology and Innovation Foundation (ITIF))

Virginia’s Regulatory Shift, 42 Groups Signal Policy Maturation

The regulatory tools being deployed are evolving from blunt instruments to more sophisticated policies. Early actions, like the moratoriums in Ireland and Singapore, were emergency measures to halt unsustainable growth. Now, jurisdictions are developing more nuanced approaches. The vote in Loudoun County, Virginia, to end “by-right” development is a prime example, replacing a rubber stamp with a detailed review process that incorporates community input—a process now heavily influenced by 42 organized local opposition groups. Texas is not just restricting but creating frameworks for data centers to act as flexible, controllable loads. This maturation shows that governments are moving beyond simply saying “no” and are instead building the long-term governance structures needed to manage the data center industry as a permanent and power-intensive part of their infrastructure.

US Map Shows Hotspots of Data Center Opposition

The regulatory shift in Virginia, a major data center hotspot, is often driven by local opposition and land/resource use concerns. This map visually represents these “hotspots of opposition,” providing geographical context for the policy maturation described in the section.

(Source: Data Center Watch)

Grid Integration as the New Competitive Edge in Data Center Siting

The single most critical strategic action for data center developers in the coming year is to reframe utility engagement from a transactional procurement to a strategic partnership. Developers who fail to proactively co-invest in grid solutions and instead treat power as a simple commodity will face multi-year delays and project cancellations. Success will be defined by the ability to secure power through proactive grid integration, not just land acquisition.

- The March 2025 vote in Loudoun County to end “by-right” development is a definitive signal that even the most established markets will prioritize grid and community stability over rapid, unchecked approvals.

- Texas’s SB-6 legislation, passed in May 2025, formalizes a new reality where data centers must function as participants in grid reliability, creating a regulatory model for large loads to be both a resource and a responsibility.

- Ohio‘s pre-payment rule, implemented by 2025, is a leading financial indicator of a nationwide trend to de-risk public utilities by placing the capital burden for expansion directly on the entities creating the demand.

- The indefinite project stalls for multi-hundred-megawatt facilities in the UK and Ireland serve as a stark, real-world warning that land without a clear, available power connection is a stranded asset.

The questions your competitors are already asking

This report covers one angle of data center site selection and development strategy. The questions that matter most depend on your work.

- Which data center developers are gaining or losing ground in an energy-constrained market?

- What is the outlook for data center investment in regions like Virginia and Ireland with grid connection moratoriums?

- What is actually happening with development pipelines in Loudoun County since the March 2025 elimination of ‘by-right’ approvals?

- What are the opportunities for new data center development in secondary markets without grid constraints?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.