Baker Hughes CCUS for Data Centers, 270 MW Frontier Deal, 1.3 GW Mobile Fleet, and 9 Agreements (2021 to 2025)

Baker Hughes 1.3 GW Gas Turbine Orders Confirm Shift to Data Center Power (2021 to 2025)

In 2025, Baker Hughes executed a decisive pivot from its traditional oilfield services identity to become a critical technology provider for power generation and grid stability. This strategic repositioning is a direct response to the surging electricity demand from industrial electrification and the proliferation of AI-powered data centers, which has created severe bottlenecks in the gas turbine supply chain. Rather than competing directly in the crowded battery manufacturing market, the company is now a primary enabler of the infrastructure required to support the energy storage ecosystem.

- Before 2025, the company’s new energy initiatives were part of a broader, more gradual transition. The strategic shift in 2025 was marked by aggressive, large-scale commercial agreements targeting the source of the new energy demand: power generation for data centers and grid firming.

- A landmark deal with Frontier Infrastructure, announced in May 2025, validated this strategy. Baker Hughes will supply 16 natural gas turbines to provide 270 MW of power for data center projects in Wyoming and Texas, directly addressing the power deficit created by the AI boom.

- Further cementing this position, Baker Hughes secured a significant order from Dynamis Power Solutions in November 2025 for 25 aeroderivative gas turbines. This equipment will create a mobile power generation fleet of approximately 1.3 GW, designed to provide flexible, on-demand power to stabilize the grid.

- This strategic focus is reflected in the company’s financial performance. The Industrial & Energy Technology (IET) segment, which includes this equipment, achieved a record backlog of $32.1 billion in Q 3 2025, driven by these new energy and power generation orders.

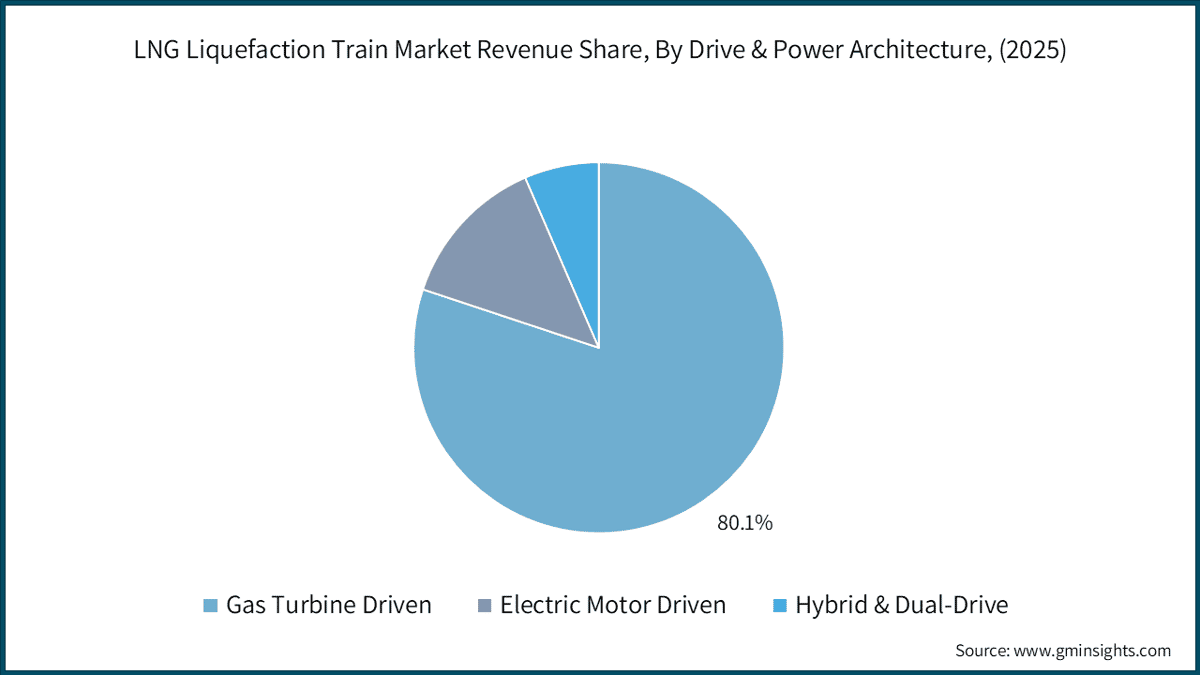

Gas Turbines Dominate LNG Liquefaction Market

While the chart focuses on the LNG market, it establishes the dominance of gas turbine technology. This supports the section’s premise that Baker Hughes can leverage its leadership in this core technology to pivot to new applications like powering data centers.

(Source: Global Market Insights)

$13.6 B Acquisition, Baker Hughes Cements Leadership in Hydrogen and LNG

The company’s 2025 investment strategy was defined by a transformational move to secure leadership across the entire decarbonized energy value chain, extending far beyond simple power generation. This strategy is centered on acquiring and integrating critical technologies for long-duration energy storage and the transport of low-carbon fuels, positioning Baker Hughes as an indispensable architect of future energy systems.

- The cornerstone of this strategy is the landmark $13.6 billion all-cash acquisition of Chart Industries, announced in July 2025. This move integrates critical cryogenic technologies for LNG, hydrogen, and Carbon Capture, Utilization, and Storage (CCUS), all of which are intrinsically linked to large-scale, long-duration energy storage.

- The market’s demand for these solutions is confirmed by the company’s projection to secure over $1.6 billion in new energy technology orders during 2025 alone, a strong signal of commercial traction for its diversified portfolio.

- Underpinning these large-scale investments is a disciplined financial strategy, evidenced by portfolio optimization actions announced in Q 2 2025 that are expected to generate approximately $1 billion in net proceeds. This capital recycling allows the company to fund its strategic pivot while maintaining financial health.

Baker Hughes Acquires Chart Industries for $13.6B

The chart headline is a direct and explicit match for the section’s topic, confirming the specific $13.6B acquisition mentioned in the heading to bolster its LNG and hydrogen portfolio.

(Source: Energy Central)

Table: Baker Hughes Strategic Investments in 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Acquisition of Chart Industries | Jul 2025 | $13.6 billion all-cash agreement to acquire a leader in cryogenic technology. The deal accelerates the company’s strategy in LNG, hydrogen, and CCUS, positioning it across the full energy value chain. | Energy Central |

| Portfolio Optimization | Jul 2025 | Announced portfolio actions expected to generate about $1 billion in net proceeds. This move signals a strategic reallocation of capital towards higher-growth energy technology sectors. | Baker Hughes |

| Louisiana LNG Project (Technology Provider) | Apr 2025 | Serving as a key technology provider for Woodside’s $15.9 billion Louisiana LNG project, highlighting the company’s role in enabling large-scale energy infrastructure. | Woodside |

| New Energy Technology Orders | Jan 2025 | The company projected securing over $1.6 billion in new energy technology orders in 2025, reflecting strong demand for its decarbonization and energy transition solutions. | Upstream |

Synchronous Condenser Market Growth Forecast

The chart highlights a specific, high-growth niche market for synchronous condensers, which are critical for grid stability. This forecast identifies a promising area for a strategic investment by an energy technology company like Baker Hughes.

(Source: MarketsandMarkets)

CCUS Partnerships, Baker Hughes Targets Data Center Decarbonization

In 2025, Baker Hughes established a strategic partnership ecosystem designed to integrate its core power generation technologies with decarbonization solutions. These alliances are not speculative; they are targeted commercial agreements focused on solving the immediate challenge of powering high-growth sectors like data centers while providing a clear pathway to reduce their carbon footprint.

- The most critical alliance is the partnership with Frontier Infrastructure, formalized in March 2025. This collaboration moves beyond a simple equipment supply relationship to the joint development of large-scale Carbon Capture and Storage (CCS) and power generation projects specifically for data centers in the U.S.

- Demonstrating global reach, Baker Hughes entered a collaboration with Kaz Munay Gas and Chevron in September 2025 to explore a pilot CCUS facility in Kazakhstan. This project provides a critical entry point into the developing Eurasian carbon management market.

- The company also reinforced its core market position through a framework agreement with Hunt Oil Company in December 2025. This partnership focuses on applying Baker Hughes‘ advanced technology portfolio to redevelop mature oil and gas fields, creating opportunities to integrate CCUS at the source.

Ranking of Key Energy Transition Technologies

This chart provides strategic context for the section’s topic by showing where CCUS ranks among key energy transition technologies. A high ranking justifies the formation of strategic partnerships to capitalize on this important decarbonization trend.

(Source: ACORE)

Table: Baker Hughes Strategic Partnerships in 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Hunt Oil Company | Dec 2025 | Joint framework agreement to redevelop mature oil and gas fields. This leverages Baker Hughes‘ technology to enhance production while creating opportunities for integrated decarbonization. | Baker Hughes |

| Kaz Munay Gas and Chevron | Sep 2025 | Collaboration to evaluate a pilot Carbon Capture, Utilization, and Storage (CCUS) facility in Kazakhstan, expanding the company’s carbon management footprint internationally. | Pw C |

| Frontier Infrastructure | Mar 2025 | Partnership to accelerate the development of integrated CCUS and power generation solutions specifically for the high-growth, energy-intensive data center industry in the U.S. | Baker Hughes |

Pipeline Integrity Market to Reach $8B

The chart shows the market size for pipeline integrity, a critical enabling service for Baker Hughes’ core growth areas of natural gas, hydrogen, and CCUS. This makes it a logical field for forming strategic partnerships, as discussed in the section.

(Source: Market.us)

US vs. International, Baker Hughes Geographic Focus on Power and CCUS

While Baker Hughes maintains a global operational footprint, its most decisive strategic initiatives in 2025 were heavily concentrated in North America, specifically targeting the region’s acute power demand and advanced energy infrastructure. This geographic focus is complemented by targeted expansion in international markets with strong policy support for decarbonization, demonstrating a dual-pronged growth strategy.

- The United States was the epicenter of activity, driven by the AI-fueled data center boom. Key agreements with Frontier Infrastructure for data center power in Wyoming and Texas, and with Dynamis Power Solutions for a North America-focused mobile power fleet, confirm the U.S. as the primary growth market.

- The company’s role as a technology provider for the $15.9 billion Louisiana LNG project and equipment supplier for Fervo Energy’s geothermal project in Utah further solidifies its deep integration into the U.S. energy infrastructure build-out.

- Internationally, the strategy is more targeted. The CCUS pilot collaboration with Kaz Munay Gas and Chevron in Kazakhstan represents a strategic entry into a region with significant hydrocarbon resources and a growing imperative to decarbonize.

- In South America, the multi-year contract with Petrobras to deploy offshore stimulation vessels in Brazil shows a continued commitment to leveraging advanced technology in established oil and gas producing regions, which may offer future CCUS opportunities.

Baker Hughes Deploys Commercial-Ready CCUS and Gas Turbine Technology

In 2025, Baker Hughes’ technology strategy centered on deploying commercially proven, high-readiness-level solutions to meet immediate market demand, particularly in power generation and carbon capture. This focus on bankable technology (TRL 9) provides a strong revenue foundation while the company simultaneously develops next-generation solutions like ammonia-based power to address future decarbonization requirements.

- The company is capitalizing on its commercially available (TRL 9) carbon capture portfolio. This includes being the sole active commercializer of the Chilled Ammonia Process (CAP) for post-combustion CO₂ capture and offering integrated offshore CO₂ injection systems based on its mature subsea technology.

- The major gas turbine orders from Frontier Infrastructure and Dynamis Power Solutions involve the deployment of highly reliable, well-established turbine models like the Nova LT™ and aeroderivative LM series, ensuring performance and bankability for customers.

- In parallel, Baker Hughes is advancing future technologies. Its PSM business is developing an ammonia combustor for retrofitting existing small-frame gas turbines, creating a pathway for asset owners to transition to low-carbon fuels without replacing entire units. This shows a clear strategy to bridge current technology with future market needs.

Industrial Electrification Market to Exceed $95B by 2034

The chart illustrates the significant growth in the industrial electrification market. This trend creates a substantial demand for the commercial-ready gas turbines (to provide power) and CCUS (to abate emissions) that the section states Baker Hughes is deploying.

(Source: Precedence Research)

SWOT Analysis, Baker Hughes Strategic Pivot to Energy Technology

The strategic actions undertaken by Baker Hughes in 2025 have fundamentally altered its market position, capitalizing on its industrial strengths to seize opportunities in the energy transition while exposing it to new risks associated with policy and complex supply chains.

- Strengths: The company’s diversified technology portfolio and robust IET backlog provide a strong foundation for growth.

- Weaknesses: The high cost of acquisitions and a lingering identity tied to legacy oil and gas markets present internal challenges.

- Opportunities: The insatiable demand for data center power and supportive policies for hydrogen and CCUS create significant market openings.

- Threats: U.S. policy instability and persistent supply chain bottlenecks for key components pose the most significant external risks to executing its strategy.

Energy Sector Prioritizes Efficiency, M&A, and Emissions Tech

This chart outlines the high-level strategic priorities of the energy sector. These priorities represent the opportunities and threats that would be central to a SWOT analysis of Baker Hughes’ strategic pivot to energy technology.

(Source: Turbomachinery Magazine)

Table: SWOT Analysis for Baker Hughes Energy Storage and Battery Initiatives

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong engineering capabilities and an existing portfolio of industrial and energy technology (IET). A growing but unproven new energy order book. | Record IET backlog of $32.1 billion. Proven ability to win large-scale power generation and LNG technology contracts. Diversified portfolio now includes leading cryogenic tech via Chart Industries. | The 2025 performance validated that the company’s core IET strengths are highly transferable and in-demand for energy transition infrastructure, converting potential into a record backlog. |

| Weaknesses | Perception as a traditional oilfield services (OFSE) company. Dependence on cyclical oil and gas capital expenditures. | Significant capital outlay ($13.6 billion) for the Chart Industries acquisition creates integration risk and high debt load. Continued, though declining, exposure to the volatile OFSE segment. | The pivot away from OFSE was confirmed, but it introduced new financial risks associated with large-scale M&A integration, shifting the nature of the company’s internal challenges. |

| Opportunities | Emerging demand for LNG, hydrogen, and CCUS. Early signs of increased power demand from digitalization. | Explosive, non-negotiable power demand from AI data centers. Favorable policies for CCUS and hydrogen are largely preserved despite broader clean energy credit changes. | The data center power crisis emerged as the single largest commercial opportunity, validating the strategic pivot to gas turbines as a critical grid-enabling technology. |

| Threats | General policy uncertainty around the energy transition. Standard supply chain disruptions post-COVID. | Specific policy risk from the One Big Beautiful Bill Act (OBBBA), creating uncertainty around IRA tax credits. Severe, systemic supply chain bottlenecks for gas turbines. Permitting delays for major projects. | Risks became more specific and acute. The OBBBA introduced a tangible policy threat, while the data center boom turned a general supply chain issue into a critical bottleneck for a core product line. |

Battery Storage Market to Hit $161B by 2034

This chart quantifies the significant market opportunity in battery storage, which directly informs the ‘Opportunities’ component of a SWOT analysis for Baker Hughes’ specific battery initiatives.

(Source: Fortune Business Insights)

$32.1 B Backlog, Baker Hughes Execution Risk in 2026

Looking ahead, the central challenge for Baker Hughes is execution. The success of its 2025 strategy hinges on its ability to smoothly integrate the massive Chart Industries acquisition and translate its record $32.1 billion Industrial & Energy Technology backlog into profitable revenue, all while navigating significant supply chain and policy headwinds.

- If this happens: The successful integration of Chart Industries will be the primary focus for 2026. Watch this: Progress reports on achieving cost synergies, consolidating supply chains, and winning joint contracts that leverage both companies’ technologies. These could be happening: Delays in integration could signal culture clashes or unforeseen technical hurdles, impacting the projected returns of the $13.6 billion deal.

- If this happens: The company’s ability to scale manufacturing will be tested by the immense demand for gas turbines. Watch this: Announcements regarding the expansion of manufacturing capacity in Italy and its impact on reducing lead times for turbine orders. These could be happening: Failure to scale production could lead to lost market share as customers turn to competitors or alternative power solutions.

- If this happens: The full impact of the OBBBA legislation will become clear as projects seek financing. Watch this: The pace of final investment decisions (FIDs) for major CCUS and hydrogen projects in the U.S. These could be happening: A slowdown in FIDs could indicate that the altered tax credit landscape is hampering project economics, potentially slowing the growth of a key market for Baker Hughes.

Economic Conditions, Volatility, Decarbonization Shape Energy Industry

The chart’s focus on ‘Economic Conditions’ and ‘Volatility’ directly addresses the external factors that create the ‘execution risk’ for a large backlog, as mentioned in the section heading.

(Source: Turbomachinery Magazine)

The questions your competitors are already asking

This report covers one angle of Baker Hughes’s strategic pivot into the data center power generation market. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the gas turbine market for data center power?

- What is the outlook for gas turbine and CCUS deployment in the data center sector by 2030?

- Baker Hughes’s activities in CCUS for data centers. Are these initiatives progressing from pilot to commercial-scale deployment?

- Which data center operators are adopting on-site gas turbines for primary power?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.