SLB BESS Strategy, $1 B New Energy Target, Microsoft Carbon Deal, and Northern Endurance Partnership (2025)

BESS Market Risks, SLB Navigates 79 GW Cancellations

SLB’s 2025 strategy deliberately avoids direct exposure to the volatile battery manufacturing and deployment market, which saw significant project cancellations, by focusing instead on critical upstream and enabling technologies. While the period between 2021 and 2024 was characterized by broad market expansion, 2025 introduced significant turbulence, creating a difficult environment for companies directly involved in battery production and utility-scale project development. SLB has instead leveraged its core competencies to build a defensible position in adjacent, high-margin sectors.

- The broader clean energy market faced significant headwinds in 2025, with an estimated $22 billion in clean energy projects cancelled, closed, or scaled back in the first half of the year alone.

- The US energy storage sector was particularly hard-hit, with a reported 21 GWh of planned US ESS cell manufacturing capacity for 2028 cancelled in early 2025 due to new tariffs, duties, and market pressures that eroded margins.

- In response, SLB has focused its New Energy division not on battery manufacturing but on enabling the supply chain. This includes accelerating its Direct Lithium Extraction (DLE) technology to produce a key material for EV batteries.

- The company is also concentrating on enabling infrastructure, such as its modular data center solutions and large-scale Carbon Capture, Utilization, and Sequestration (CCS) projects, which leverage its legacy expertise in subsurface characterization.

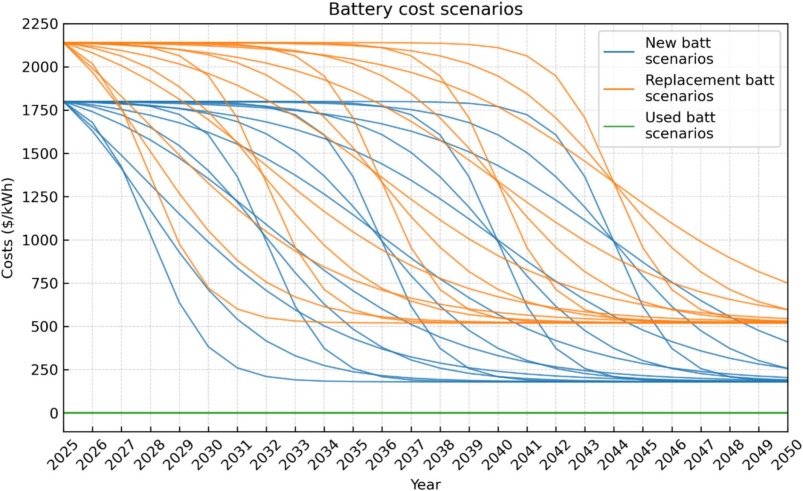

Battery Cost Projections Show High Uncertainty

The chart highlights a fundamental market risk—high uncertainty in future battery costs. This uncertainty is a primary driver for the large-scale project cancellations mentioned in the section heading.

(Source: ScienceDirect.com)

$1 B New Energy Revenue, SLB A$31 M Ray Gen Investment

SLB is funding its strategic pivot into New Energy through targeted investments and is on track to achieve significant revenue milestones, contrasting with the capital-intensive outlays required for direct battery manufacturing. The company’s financial discipline allows it to selectively invest in technology providers and grow its service-oriented New Energy segments without exposing itself to the commodity-like competition and price volatility seen in the battery cell market.

- SLB’s New Energy division, which includes CCS, geothermal, critical minerals, and data center solutions, is on pace to generate combined revenue exceeding $1 billion in 2025, marking a major financial milestone for the company’s diversification efforts.

- On April 9, 2025, SLB led a Series D investment round in Australian solar-plus-storage firm Ray Gen, providing a follow-on investment of A$31 million (~$20.5 M USD) to advance its solar and thermal storage technology.

- This “picks and shovels” approach, focused on providing technology and services, stands in contrast to the massive capital expenditures of battery manufacturers and project developers, thereby mitigating direct exposure to project cancellations and manufacturing overcapacity.

Table: SLB New Energy Investments and Financials

| Company / Division | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| SLB New Energy | 2025 | The division is projected to exceed $1 billion in revenue from its CCS, geothermal, critical minerals, and data center segments, validating its strategic pivot. | Natural Gas Intel |

| Ray Gen | April 2025 | SLB led a Series D round with an A$31 million investment to support the deployment of Ray Gen’s concentrated solar and thermal storage technology. | Ray Gen |

SLB 3 Key CCS Partnerships with Microsoft and JPMorgan Chase (2025)

SLB solidified its position in the decarbonization sector through high-profile partnerships in 2025, leveraging its SLB Capturi joint venture to secure commercial agreements with major corporate and financial institutions. These collaborations serve as crucial validation for SLB’s carbon capture technology and its ability to execute complex, large-scale projects, establishing a new and material revenue stream.

- In July 2025, SLB was awarded a contract by the Northern Endurance Partnership (NEP) in the UK to design and evaluate the CO 2 injection and storage system, applying its subsurface modeling and technology.

- The SLB Capturi joint venture was selected in May 2025 as the technology supplier for a carbon removal project involving CO 280 and JPMorgan Chase, where JPMorgan Chase signed an offtake agreement for the carbon credits.

- A significant agreement was announced in April 2025 where SLB Capturi will provide the technology for a project removing 3.7 million tons of CO 2 from a U.S. pulp and paper mill, with Microsoft purchasing the resulting carbon removal credits.

Table: SLB Strategic Decarbonization Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Northern Endurance Partnership (NEP) | July 2025 | SLB was awarded a contract to provide comprehensive carbon storage solutions, including injection system design and subsurface modeling, for the pioneering UK CCS project. | SLB |

| CO 280 & JPMorgan Chase | May 2025 | SLB Capturi will supply its carbon capture technology for a project where CO 280 captures and stores CO 2, with JPMorgan Chase acting as the offtake partner for the credits. | PR Newswire |

| Microsoft | April 2025 | As technology supplier, SLB Capturi’s technology will be used to remove 3.7 million tons of CO 2 from a US mill, with Microsoft purchasing the carbon removal credits. | ESG Today |

US vs Europe, SLB CCS and BESS Supply Chain Focus

While SLB’s carbon capture activities showed strong commercial traction in both Europe and the US in 2025, its critical minerals strategy is positioned to address supply chain needs globally, particularly for a North American market facing significant policy-driven volatility. The company’s geographic strategy appears designed to diversify risk by securing cornerstone projects in mature regulatory environments like the UK while simultaneously providing enabling technology to capitalize on growth markets like the US.

- In the period from 2021 to 2024, SLB’s New Energy division was primarily in a development and early partnership phase, building the foundation for the commercial agreements seen in 2025.

- In 2025, SLB’s CCS business secured a major contract in the UK (Northern Endurance Partnership) and deployed modular plants in Europe (Twence facility), demonstrating a strong foothold in the European market.

- Simultaneously, high-profile carbon removal offtake agreements with US-based entities like Microsoft and JPMorgan Chase confirm the commercial viability of its technology in North America.

- The US market represents a key target for SLB’s DLE technology, aiming to supply the domestic EV battery supply chain, but its technology-provider model insulates it from the direct impact of project cancellations that plagued US developers in 2025.

US Battery Capacity Grew Rapidly Through 2024

The chart provides essential data on the rapid growth of the US battery market, which directly supports the ‘US… BESS Supply Chain Focus’ aspect of the section’s comparative analysis between the US and Europe.

(Source: Reuters)

DLE and CCS Commercialization, SLB Technology Validation

In 2025, SLB advanced its key New Energy technologies from pilot stages toward commercial validation, with its modular CCS solutions securing major contracts and its Direct Lithium Extraction technology moving into active project acceleration. This progression marks a critical shift from R&D investment to revenue generation, proving the commercial applicability of technologies developed over the 2021-2024 period.

- From 2021-2024, SLB invested in developing and piloting its New Energy technologies, including DLE and advanced CCS, largely within partnerships and internal development programs.

- By 2025, its CCS technology achieved commercial scale and bankability, evidenced by the multi-million-ton carbon removal agreement with Microsoft and the technology supply contract for the JPMorgan Chase-backed project.

- SLB’s sustainable lithium production technology, widely understood to be DLE, moved from a conceptual stage to active acceleration in 2025, with the company focused on commercial adoption to address bottlenecks in the battery supply chain.

- The launch of Data Center Infrastructure Solutions in July 2025 represents the commercial debut of a new service offering, moving a strategic concept to a market-ready product designed to meet the energy demands of AI and cloud computing.

SWOT Analysis, SLB Strategic Pivot Risks and Opportunities

SLB’s strategic pivot leverages its formidable subsurface expertise and financial strength to enter high-growth energy transition markets, but it faces challenges in scaling these new ventures to a size that can materially offset potential declines in its legacy business. The market volatility of 2025 highlighted both the risks of direct competition and the opportunities available to a differentiated technology and services provider.

- Strengths: World-class subsurface expertise, a strong balance sheet, and an established global operational footprint provide a durable competitive advantage.

- Weaknesses: The New Energy division, despite its growth, remains a small fraction of SLB’s total revenue, and the company remains heavily dependent on its legacy oil and gas business.

- Opportunities: The explosive growth forecast for the BESS, CCS, and AI-driven data center markets provides massive addressable markets for SLB’s new technology and service offerings.

- Threats: Continued volatility and policy uncertainty in clean energy markets, demonstrated by the $22 billion in US project cancellations in 2025, could slow demand, while competition from specialized technology firms remains intense.

Table: SWOT Analysis for SLB’s New Energy Strategy

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Core subsurface expertise from oil and gas was a theoretical advantage for New Energy. | Awarded major CCS contracts (Northern Endurance Partnership) and accelerated DLE technology, directly applying subsurface expertise. | The competitive advantage of subsurface knowledge was validated through commercial contracts in CCS and critical minerals. |

| Weaknesses | New Energy division was in an early, pre-revenue or low-revenue stage, representing a cost center. | New Energy is on track to exceed $1 billion in revenue but remains small relative to the core business. | The division shifted from a conceptual bet to a tangible, growing business, though the challenge of scale remains. |

| Opportunities | The energy transition represented a large, theoretical future market for SLB’s technologies. | Major offtake deals (Microsoft, JPMorgan Chase) and a new data center solutions offering proved tangible demand. | The opportunity moved from abstract market growth to concrete, bankable projects and new product-market fit. |

| Threats | Policy and market risks were potential future headwinds for clean energy adoption. | $22 billion in US project cancellations and 21 GWh of shelved battery factory capacity materialized as direct market shocks. | Abstract risks became real market events, validating SLB’s risk-averse strategy of avoiding direct manufacturing. |

SLB Scenario: DLE Commercialization and Data Center Wins

The primary indicator of SLB’s continued success in 2026 will be the commercialization of its Direct Lithium Extraction technology through a major offtake or licensing agreement and its ability to secure a significant contract for its new data center infrastructure solutions. Success on these fronts would validate its strategy of building high-margin, technology-driven adjacencies, while a lack of progress could signal a stalled transition.

- If SLB announces its first commercial-scale DLE project, watch this: The company’s valuation may be re-rated by the market to reflect its new position as a critical materials technology provider for the EV supply chain, moving it beyond a traditional energy services classification.

- The key signal to watch is a contract with a hyperscaler or large data center operator. This could be happening because: The explosive energy demand from AI is creating an urgent need for the modular, decarbonized power and infrastructure solutions SLB now offers, and a marquee customer win would confirm product-market fit.

- If commercial momentum in DLE and data centers stalls, watch this: The company may face increased pressure to demonstrate growth in its New Energy division, especially if its legacy upstream business faces the spending declines it warned of in mid-2025.

The questions your competitors are already asking

This report covers one angle of SLB’s New Energy strategy amid market turbulence. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the energy storage market by focusing on upstream technologies versus direct BESS deployment?

- SLB’s New Energy investments. Is the division on track for its $1B revenue target?

- SLB activities in Direct Lithium Extraction (DLE). Is the technology progressing from pilot to commercial deployment?

- What is the status of SLB’s Northern Endurance Partnership and its carbon capture deal with Microsoft?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.