Hydrogen Infrastructure 2026: Why Baker Hughes’ Technology Enabler Strategy is Winning

Commercial Projects Confirm the Shift to Large-Scale Deployment

By 2025, the hydrogen equipment market transitioned from pilot-scale validation to supporting multi-billion-dollar commercial projects, confirming the viability of a technology-enabling strategy. Baker Hughes has capitalized on this shift by positioning itself as a critical supplier of high-margin turbomachinery and compression technology rather than a direct hydrogen producer. This “picks and shovels” approach minimizes capital risk while capturing value across green, blue, and low-carbon hydrogen value chains.

- Between 2021 and 2024, the focus was on validating technology through pilot projects. A key example was the December 2022 trial with Snam, which successfully tested a Nova LT™12 turbine on a 10% hydrogen blend in a live gas network, proving the concept of retrofitting existing infrastructure.

- In 2025, the strategy pivoted to securing roles in globally significant commercial undertakings. Baker Hughes became a pivotal technology provider for Saudi Arabia’s NEOM Green Hydrogen Project, the world’s largest, and secured a contract in June 2025 to supply its advanced CO₂ compressor technology for Eni’s Liverpool Bay carbon capture project.

- The company’s role expanded beyond hydrogen-specific projects to include major energy infrastructure with a decarbonization component. In November 2025, it signed an agreement to supply main refrigerant compressors and power generation equipment for the Alaska LNG mega-project, demonstrating its ability to serve a wide array of energy transition initiatives.

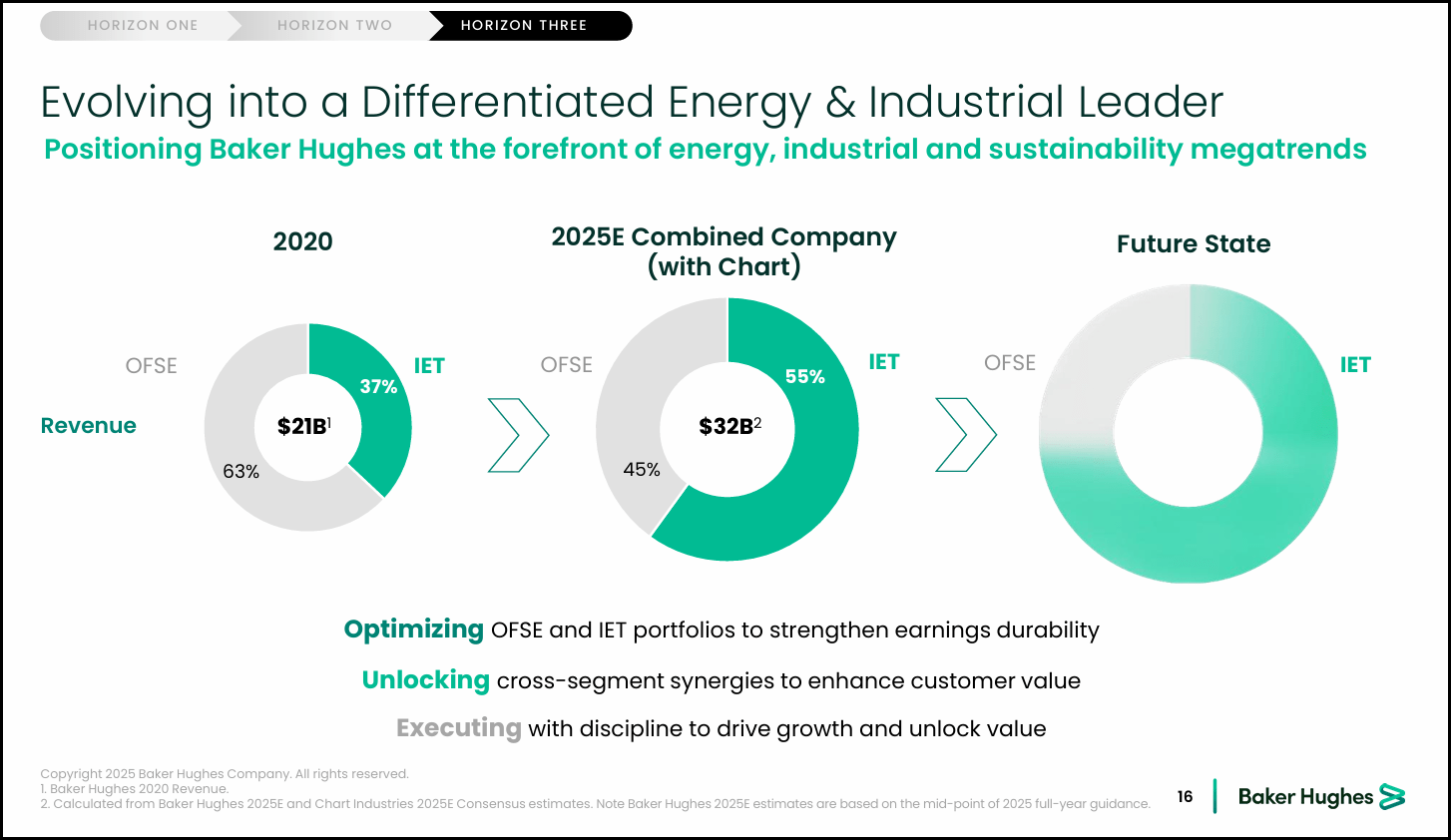

Baker Hughes’ Revenue Shifts Toward Technology

This chart shows the strategic revenue shift to the Industrial & Energy Technology (IET) segment, directly quantifying the section’s point about capitalizing on the market shift by becoming a key technology supplier.

(Source: Seeking Alpha)

Investment Strategy Favors Ecosystem Growth Over Direct Production

Baker Hughes‘s financial strategy de-risks its entry into the hydrogen market by investing in ecosystem-building funds and targeted technology companies, rather than committing massive capital to direct asset ownership. This approach creates a downstream pull for its own equipment and services. The company’s investments validate emerging pathways like turquoise hydrogen while its participation in infrastructure funds provides a pipeline of future commercial orders.

Acquisition Expands Non-O&G Revenue and Capabilities

This chart illustrates a major acquisition, a prime example of the section’s described strategy of investing in targeted technology companies to build an ecosystem rather than committing capital to direct asset ownership.

(Source: Gas Compression Magazine)

- A foundational move was becoming a technology partner and investor in Hy 24, a joint venture managing a €2 billion clean hydrogen infrastructure fund. This June 2023 investment gives Baker Hughes direct insight and access to a portfolio of large-scale projects seeking technology partners.

- The company has also made targeted investments in emerging production technologies. In 2022, it invested in Ekona Power, a developer of methane pyrolysis technology for turquoise hydrogen, diversifying its exposure beyond established green and blue hydrogen methods.

- In March 2025, Baker Hughes‘s involvement in the Clean Hydrogen Partnership was confirmed, which is backing eight hydrogen combustion projects with a total investment of €33.15 million to accelerate industrial adoption. This move supports the development of a key end-market for its hydrogen-ready turbines.

Table: Key Strategic Investments in Hydrogen and Adjacent Technologies

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Alaska LNG Project | Nov 2025 | Investment and equipment supply agreement. Secures a role in a major U.S. energy project, supplying compressors and power generation equipment. | World Oil |

| Clean Hydrogen Partnership | Mar 2025 | Participation in a €33.15 million funding initiative across 8 projects to advance hydrogen combustion technologies for industrial use. | Clean Hydrogen Partnership |

| Hy 24 Clean Hydrogen Fund | Jun 2023 | Became a technology partner and investor in the €2 billion fund, creating a project pipeline for its hydrogen technologies. | Hy 24 |

| Ekona Power | Feb 2022 | Strategic investment to gain access to methane pyrolysis technology for low-cost, low-emission turquoise hydrogen production. | [PDF] Baker Hughes Holdings LLC |

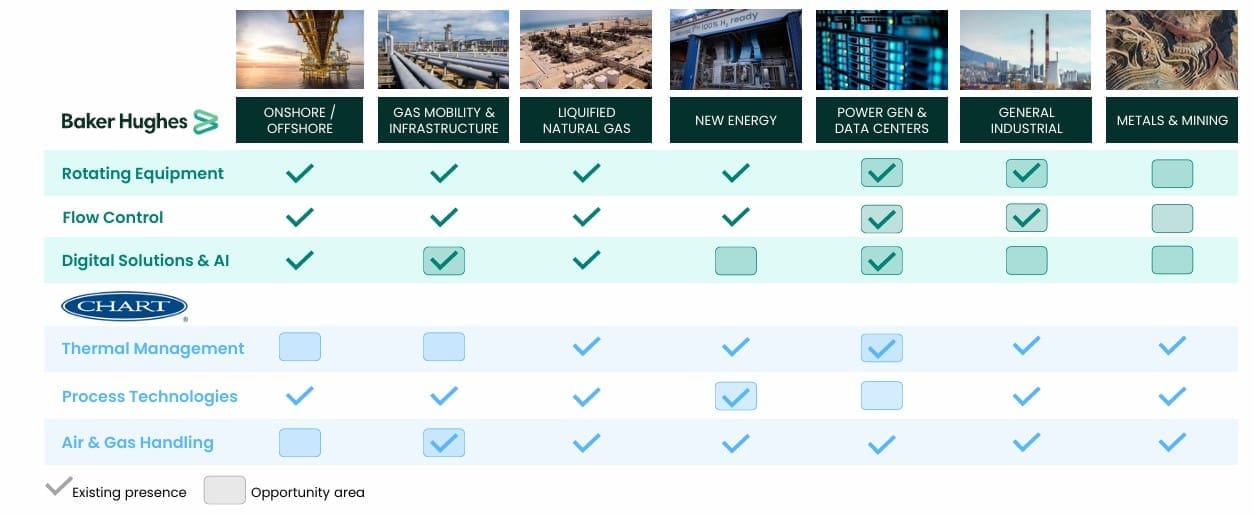

Partnerships Secure Access to New Markets and Industrial Verticals

Strategic partnerships are the central mechanism for Baker Hughes to embed its technology across the energy and industrial spectrum. These collaborations combine its hardware expertise with the project development and operational capabilities of its partners. This model accelerates market penetration into carbon capture, industrial clusters, and hard-to-abate sectors like steel manufacturing.

Partnership Expands Market Reach and Capabilities

The matrix chart visually demonstrates how a major partnership combines capabilities, directly supporting the section’s theme of using strategic collaborations to penetrate new markets and industrial verticals.

(Source: Gas Compression Magazine)

- The March 2025 partnership with Frontier Infrastructure is designed to accelerate large-scale carbon capture, storage (CCS), and power generation projects in the U.S., including for data center power. This combines Baker Hughes‘s technology with Frontier’s development expertise.

- Also in March 2025, the company’s participation in the SYRIUS project alongside Elcogen demonstrated a push into heavy industry. The project aims to integrate hydrogen production directly into the steelmaking process, opening a new vertical for its technology.

- Earlier collaborations, such as with industrial cluster partners Iberdrola and Petronor/Repsol announced in January 2025, focus on aligning infrastructure priorities to speed up regional decarbonization efforts.

Table: Baker Hughes’ 2025 Hydrogen and CCUS Partnership Network

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| SYRIUS Project (with Elcogen) | Mar 2025 | Technology partner for a project focused on decarbonizing the steel industry by integrating on-site hydrogen production. | Elcogen |

| Frontier Infrastructure | Mar 2025 | Strategic partnership to develop large-scale CCS and power generation projects in the U.S. by combining technology with project management. | ESG News |

| Industrial Clusters (with Iberdrola, Repsol) | Jan 2025 | Collaboration within industrial clusters to streamline the development of shared decarbonization infrastructure, including H 2 and CCUS. | [PDF] World Economic Forum |

| Avports | Aug 2023 | Agreement to develop and implement green hydrogen, SAF, and micro-grid solutions to decarbonize airport operations. | CSRwire |

Geographic Focus Expands from Europe to Global Mega-Projects

The geographic focus of Baker Hughes‘s hydrogen activities has expanded from European technology trials to major commercial commitments in North America and the Middle East. This progression reflects the global maturation of the hydrogen market and the company’s ability to serve diverse regional energy strategies, from green hydrogen export hubs to domestic industrial decarbonization.

- From 2021 to 2024, Europe was the primary ground for technology validation. The successful turbine trial with Snam in Italy in 2022 and investment in Germany-based Electrochaea were key activities.

- The year 2025 marked a definitive global expansion. The company secured its role as a key technology provider for the NEOM Green Hydrogen Project in Saudi Arabia, a cornerstone of the Middle East’s energy export ambitions.

- In North America, Baker Hughes cemented its position in large-scale energy infrastructure. Its selection for Air Products’ net-zero hydrogen complex in Canada (November 2022) was followed by the major supply and investment agreement for the Alaska LNG project in November 2025.

- In the UK, the agreement to supply CO₂ compressors for Eni’s Liverpool Bay CCS project in June 2025 reinforces its strong position in the growing European carbon management market.

Technology Maturity Moves from Pilot to Commercially Proven

Baker Hughes‘s hydrogen and CCUS technology portfolio has advanced from the pilot stage to commercial deployment, validated by significant orders for large-scale projects. The company’s core offerings, particularly hydrogen-ready gas turbines and specialized compressors, are now proven and bankable solutions for the energy transition, underpinning its goal of capturing a 25% market share in hydrogen compression by 2027.

Strategy Targets Billions in New Energy Orders

This chart outlines the company’s multi-horizon strategy for commercialization, which aligns with the section’s theme of technology moving from pilot stage to commercially proven and securing large orders.

(Source: Constellation Research)

- Between 2021 and 2024, the focus was on demonstrating capability. The Snam project successfully operated a Nova LT™12 turbine with a hydrogen blend, establishing technical readiness. Investments in early-stage tech like Ekona Power’s turquoise hydrogen process were made to build a future pipeline.

- The period from 2025 onward is defined by commercial validation. The selection of Nova LT™ technology for Air Products’ blue hydrogen facility and equipment supply for NEOM’s green hydrogen plant confirms the commercial maturity of its production-related hardware.

- Its CCUS technology achieved a similar milestone. The June 2025 contract to supply CO₂ compressors for the Liverpool Bay CCS project provides a tangible, commercial-scale reference point for its carbon management solutions, moving it from a theoretical offering to a deployed technology.

SWOT Analysis: Baker Hughes’ Hydrogen and CCUS Strategy

The strategic shift towards being a technology enabler has fortified Baker Hughes‘s market position, but it also creates dependencies on partner execution and exposes it to competition from other diversified energy technology firms. The company’s success hinges on converting its strong project pipeline and technology leadership into sustained market share growth.

Table: SWOT Analysis of Baker Hughes’ Hydrogen & CCUS Initiatives

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Established expertise in turbomachinery; successful pilot projects like the Snam turbine trial. | Secured pivotal technology provider roles in mega-projects (NEOM, Alaska LNG); broad portfolio for green, blue, and low-carbon applications. | The company successfully translated its legacy O&G expertise into confirmed, large-scale new energy contracts, validating its technology leadership. |

| Weakness | Reliance on partnerships to access projects; emerging portfolio with limited large-scale commercial references. | Strategy is dependent on the execution and financial investment decisions (FID) of partners like Frontier Infrastructure. | While partnerships provide access, they also introduce external risks related to project delays or cancellations outside of Baker Hughes‘s control. |

| Opportunity | Growing market for hydrogen turbines and compressors; early-stage investments in new tech like turquoise hydrogen (Ekona Power). | Aggressively pursuing a 25% market share in H 2 compression by 2027; expanding into hard-to-abate sectors (e.g., steel with SYRIUS project). | The market has matured enough for the company to set concrete, ambitious market share targets, moving from exploration to a clear growth strategy. |

| Threat | Competition from other industrial giants and integrated energy companies entering the hydrogen equipment space. | Competitors like Exxon Mobil and BP are also investing heavily in new energy technologies, including using AI for operational efficiency. | The competitive field is solidifying. Maintaining a technological edge in core areas like compression and combustion is now critical for differentiation. |

Scenario Modelling: Progress Toward 25% Market Share is the Key Signal

The most critical factor determining the success of Baker Hughes‘s strategy is its ability to convert its strong project pipeline into a dominant market share for hydrogen compression. The company’s performance in 2026 will be defined by its execution on existing mega-projects and its capacity to win new, large-scale equipment orders, particularly through its strategic partnerships.

EBITDA Growth Signals Commercial Execution

As the section discusses the key signals of success, this chart provides a core financial indicator—projected EBITDA growth and margin expansion—that validates the commercial execution described.

(Source: Seeking Alpha)

- If this happens: Baker Hughes announces several more major compression and turbomachinery contracts for hydrogen or green ammonia projects in 2026, especially through its Hy 24 and Frontier Infrastructure partnerships.

- Watch this: The company’s quarterly earnings reports for specific order intake figures within its Climate Technology Solutions segment. Progress on the NEOM and Alaska LNG projects without significant delays will also be a positive indicator.

- This could be happening: The technology-enabler strategy is successfully gaining traction, allowing the company to outpace competitors focused on riskier, capital-intensive production models. Its “picks and shovels” approach is proving to be the more scalable and financially prudent path to growth in the hydrogen economy.

Frequently Asked Questions

What is Baker Hughes’ main strategy in the hydrogen market?

Baker Hughes’ strategy is to be a ‘technology enabler’ or a ‘picks and shovels’ supplier. Instead of producing hydrogen directly, it focuses on supplying critical, high-margin equipment like turbomachinery and compression technology to hydrogen projects, minimizing capital risk while capturing value across the entire hydrogen value chain.

Has Baker Hughes’ technology been proven in real-world applications?

Yes, the technology has moved from pilot tests to large-scale commercial deployment. A key validation was the December 2022 trial with Snam, which successfully ran a Nova LT™12 turbine on a hydrogen blend. This was followed by major commercial contracts, such as supplying technology to the NEOM Green Hydrogen Project and Air Products’ net-zero hydrogen complex.

Why does Baker Hughes invest in funds like Hy24 instead of building its own hydrogen plants?

This is part of a de-risking strategy to build a project pipeline. By investing in the €2 billion Hy24 clean hydrogen infrastructure fund, Baker Hughes gains direct access to a portfolio of large-scale projects that will need its equipment. This creates a downstream demand for its technology without the massive capital expenditure and risk of owning and operating production assets directly.

What are some of the major projects Baker Hughes is involved in as of 2025?

As of 2025, Baker Hughes is a pivotal technology provider for Saudi Arabia’s NEOM Green Hydrogen Project, the world’s largest. It also secured a contract to supply CO₂ compressor technology for Eni’s Liverpool Bay carbon capture project and an agreement to supply compressors and power generation for the Alaska LNG mega-project.

What is the biggest risk to Baker Hughes’ hydrogen strategy?

The primary risk is its dependence on the execution and final investment decisions (FID) of its partners. Because Baker Hughes supplies technology to projects developed by others (like Frontier Infrastructure), its success is vulnerable to external factors such as project delays or cancellations that are outside of its direct control.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.