SLB’s Hydrogen Pivot 2026: Why Building the Supply Chain Beats Owning the Molecule

Hydrogen Project Adoption: SLB’s Shift from R&D to Industrial-Scale Pilots

SLB has transitioned its hydrogen strategy from forming foundational technology ventures between 2021 and 2024 to focusing on the tangible application and supporting infrastructure for those technologies in 2025, signaling a move from R&D toward commercial readiness.

- Between 2021 and 2024, the strategy was defined by the formation of the Genvia joint venture with the French Alternative Energies and Atomic Energy Commission (CEA) to develop high-efficiency solid oxide electrolyzer (SOE) technology, followed by pilot agreements with industrial giants Arcelor Mittal (steel) and Vicat (cement).

- This foundational period also saw SLB forge a critical partnership in June 2024 with John Cockerill Hydrogen to scale mature alkaline electrolyzer technology and a landmark agreement in December 2024 with Aramco and Linde to develop a blue hydrogen-enabling carbon capture and sequestration (CCS) hub.

- In 2025, the focus shifted to enabling infrastructure, highlighted by the $30 million investment to expand its Shreveport, Louisiana manufacturing hub to produce components for its New Energy portfolio, including for data centers.

- The acquisition of Champion X Corporation for $4.9 billion in Q 3 2025 further validated this shift, broadening SLB‘s offerings for industrial decarbonization beyond pure hydrogen technology to a more integrated suite of production and recovery services.

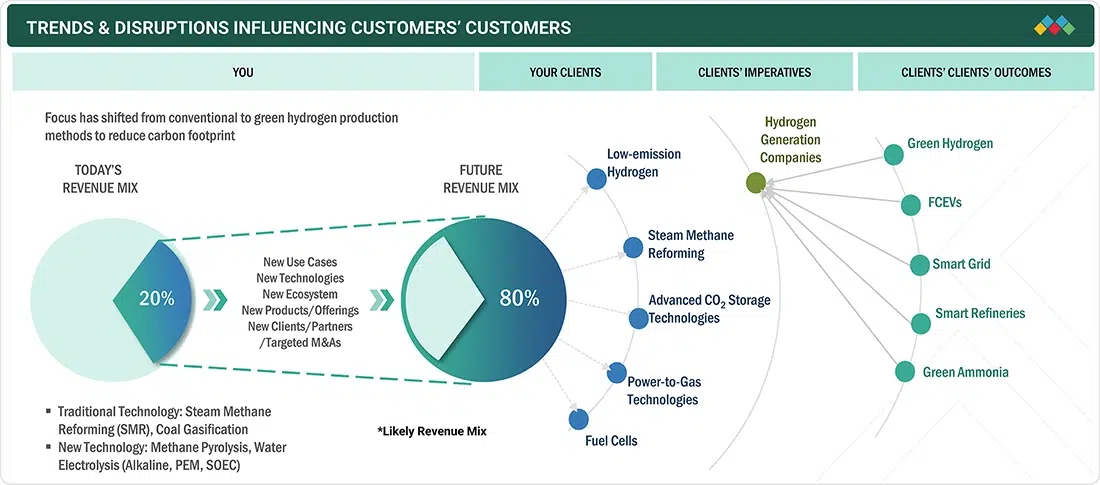

SLB’s Strategic Shift to Hydrogen Tech

This diagram illustrates the strategic pivot from legacy services to new hydrogen technologies, mirroring the section’s focus on SLB’s move from R&D to commercial applications.

(Source: MarketsandMarkets)

Strategic Capital Allocation: SLB’s Billion-Dollar Bets on Decarbonization

SLB‘s investment strategy is defined by a clear financial ambition for its New Energy division, supported by targeted, multi-billion dollar acquisitions and infrastructure enhancements rather than direct capital expenditure on large-scale hydrogen production assets.

- By early 2024, SLB established a target of achieving $3 billion in annual revenue from its New Energy portfolio by 2030, building on the more than $1 billion in revenue already generated by its “Transition Technologies” portfolio.

- The company executed a significant strategic move in 2025 with the acquisition of Champion X Corporation in a $4.9 billion all-stock transaction to create an integrated production and recovery portfolio aimed at industrial clients.

- A tangible infrastructure investment of $30 million was committed in December 2025 to expand its Shreveport, Louisiana manufacturing hub, a move that directly supports the operational and supply chain needs of its growing New Energy business.

Table: SLB Strategic Investments in New Energy and Decarbonization (2025)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Shreveport Manufacturing Hub Expansion | 2025-12-11 | $30 Million investment to expand operations for producing data-center and AI-enabling components that support the New Energy portfolio. This builds internal supply chain capacity. | POLITICO Pro |

| Acquisition of Champion X | Q 3 2025 | $4.9 Billion all-stock acquisition of a leader in chemistry solutions and artificial lift to create an integrated production and recovery portfolio, enhancing offerings for industrial decarbonization. | Market Screener |

Partnership Ecosystem: SLB’s Strategy for Scaling Hydrogen Technology in 2026

SLB‘s hydrogen strategy is constructed upon a network of strategic partnerships that provide access to best-in-class technology and market scale, effectively covering both the green and blue hydrogen value chains without bearing the full development risk.

Explaining the ‘Colors’ of Hydrogen

This infographic defines the ‘green’ and ‘blue’ hydrogen mentioned in the section, providing essential context for understanding SLB’s dual-pronged partnership strategy across the value chain.

(Source: IDTechEx)

- The foundation was laid with the Genvia joint venture formed in January 2021 with France’s CEA, targeting the development and industrialization of a high-performance solid oxide electrolyzer (SOE) technology.

- This was complemented in June 2024 by a collaboration with John Cockerill Hydrogen, a leader in alkaline electrolyzers, to accelerate the manufacturing of systems including 5 MW stacks and complete 30 MW units.

- To address the blue hydrogen pathway, SLB joined industry giants Aramco and Linde in a shareholder agreement signed in December 2024 to develop a mega-scale CCS hub in Saudi Arabia, leveraging its core subsurface characterization expertise.

Table: Key SLB Hydrogen and CCS Partnerships (2021-2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| John Cockerill Hydrogen | 2025-03-04 (ongoing) | Collaboration to develop and scale low-carbon hydrogen production solutions. Leverages John Cockerill‘s leadership in alkaline electrolyzer technology. | SLB |

| Aramco, Linde | 2024-12-05 | Shareholder agreement to develop a major carbon capture and sequestration (CCS) hub in Saudi Arabia. This is critical enabling infrastructure for large-scale blue hydrogen production. | Enterprise AM |

| Genvia (JV) | 2021-01-11 (ongoing) | A clean hydrogen technology venture with CEA and other partners to develop and industrialize high-performance solid oxide electrolyzer technology, aiming for a 30% efficiency gain. | SLB |

Global Footprint for Hydrogen: From European Tech Hubs to Middle East Mega-Projects

SLB‘s geographic focus for hydrogen has strategically expanded from European technology development hubs between 2021 and 2024 to include large-scale infrastructure projects in the Middle East and manufacturing expansion in North America through 2025.

Middle East Commits to Renewable Expansion

This chart quantifies the renewable energy ambitions in the Middle East, substantiating the region’s emergence as a key market for the mega-projects central to SLB’s geographic expansion.

(Source: Deloitte)

- From 2021 to 2024, initial efforts were centered in Europe, particularly France, with the establishment of the Genvia joint venture, its pilot projects with Arcelor Mittal and Vicat, and its manufacturing plant in Béziers.

- In 2024, the strategy broadened significantly to the Middle East with the landmark shareholder agreement with Aramco and Linde to develop a CCS hub in Saudi Arabia, positioning SLB as a key enabler for the region’s blue hydrogen ambitions.

- North America gained strategic importance in late 2025 with the $30 million investment to expand manufacturing capabilities in Shreveport, Louisiana, creating a key supply chain node for its New Energy portfolio.

- Looking ahead, SLB has identified Africa as a region with significant potential for integrated energy development, including hydrogen export routes, signaling a potential next frontier for geographic expansion.

Hydrogen Technology Maturity: From SOE Innovation to Commercial Component Supply

SLB‘s technology portfolio has matured from a primary focus on innovative, next-generation electrolyzer research and development between 2021 and 2024 to include the commercial supply of essential components and enabling infrastructure technologies in 2025.

Green Hydrogen’s High Cost Challenge

This chart highlights the high production cost of green hydrogen, directly illustrating the market problem that SLB’s high-efficiency SOE technology, as described in the section, aims to solve.

(Source: SLB)

- The 2021-2024 period was defined by the Genvia JV’s work on high-performance solid oxide electrolyzer (SOE) technology, which targets a 30% improvement in electricity conversion efficiency, directly addressing the high cost of green hydrogen.

- This was complemented by the commercial launch of a portfolio of hydrogen-ready valves in 2023 and the 2024 partnership with John Cockerill to scale existing pressurized alkaline electrolyzer technology, a more mature solution.

- By 2025, the focus broadened to the supporting ecosystem. This includes manufacturing AI-enabling components in its Louisiana facility, essential for managing complex energy projects similar to Shell’s AI initiatives, and leveraging its subsurface expertise to explore nascent fields like natural hydrogen.

SWOT Analysis: SLB’s Hydrogen Strategy Evolution for 2026

The strategic evolution from 2021 to 2025 shows SLB successfully leveraging its core strengths to build a de-risked position in hydrogen, though it now faces the challenge of commercializing these ventures and integrating large-scale acquisitions.

SLB’s Five Pillars of Decarbonization

This image visualizes the broad ‘industrial decarbonization platform’ that the SWOT analysis identifies as a key strategic strength for SLB’s hydrogen ventures.

(Source: SLB)

- Strengths have evolved from a narrow focus on subsurface expertise to a broader industrial decarbonization platform, validated by the Champion X acquisition.

- Weaknesses remain in the New Energy division’s small contribution to overall revenue and a strategic reliance on partners like Genvia for core electrolyzer innovation.

- Opportunities have expanded significantly with the move into integrated industrial services and the exploration of new energy sources like natural hydrogen.

- Threats have become more tangible, including macroeconomic pressures impacting capital projects and intensifying competition from peers like Baker Hughes.

Table: SWOT Analysis for SLB’s Hydrogen Initiatives

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Core subsurface expertise; global oilfield services reach and project management capabilities. | Capital-light, partnership-driven model (Genvia, John Cockerill); diversified portfolio across green and blue hydrogen enablers (electrolyzers, CCS). | Successfully leveraged legacy strengths to enter the hydrogen market without high-CAPEX production risk, building an enabling-tech portfolio. |

| Weaknesses | Limited track record in new energy; revenue heavily dependent on traditional oil and gas. | New Energy division is a small part of total revenue (Q 1 2025 revenue was $8.5 B). Reliance on partners for core electrolyzer technology creates integration risk. | While strategic progress is clear, the financial impact remains nascent. The model outsources key technology risk but also potential upside. |

| Opportunities | Nascent but large addressable markets for hydrogen and CCS; growing industrial demand for decarbonization. | Acquisition of Champion X ($4.9 B) opens integrated industrial services market. Exploration of natural hydrogen. $30 M manufacturing expansion in Louisiana builds supply chain capacity. | The strategy has expanded from pure hydrogen technology to the broader, more immediate market of industrial decarbonization services and component manufacturing. |

| Threats | Uncertainty in hydrogen-related policy and subsidies; high cost of green hydrogen production. | Slowing global economy impacting capital projects (reflected in SLB‘s 3% Yo Y revenue decline in Q 1). Increased competition from peers like Baker Hughes, which reported a 45% jump in new energy orders. | Macroeconomic headwinds and intensifying competition are now tangible threats to the growth trajectory of the New Energy division. |

2026 Outlook: Commercialization is the New Frontier for SLB’s Hydrogen Ventures

If SLB‘s technology partnerships begin yielding commercial-scale orders in 2026, watch for a significant acceleration in the New Energy division’s revenue growth, which would validate its capital-light, enabling-tech strategy.

Hydrogen Market Poised for Major Growth

This forecast shows the significant growth potential of the global hydrogen market through 2030, providing the macro-economic context for SLB’s commercialization outlook and future revenue ambitions.

(Source: MarketsandMarkets)

- The most critical signal to monitor will be the operational results from the Genvia pilot projects with Arcelor Mittal and Vicat. Any announcements of full-scale deployments would confirm the technology’s commercial viability and de-risk future investments.

- Another key indicator is tangible progress on the Saudi Arabia CCS hub with Aramco and Linde. A Final Investment Decision (FID) on this project would trigger significant engineering and construction activity, solidifying SLB‘s role in the global blue hydrogen ecosystem.

- Finally, scrutinize SLB‘s quarterly financial reports for the New Energy segment’s performance. Consistent growth toward the $3 billion revenue target for 2030 will be the ultimate proof that the strategy is delivering financial returns beyond just strategic positioning.

Frequently Asked Questions

Why is SLB focusing on building the hydrogen supply chain instead of producing hydrogen itself?

SLB’s strategy is to be a “capital-light” enabler of the hydrogen economy. By focusing on providing critical technologies (like electrolyzers via Genvia and John Cockerill), enabling infrastructure (like CCS with Aramco and Linde), and manufacturing key components, SLB avoids the high capital expenditure and commodity risk of owning large-scale hydrogen production assets. This approach leverages its core expertise in technology, project management, and subsurface characterization to serve the entire market of hydrogen producers.

What is the significance of SLB’s $4.9 billion acquisition of Champion X?

The acquisition of Champion X is a pivotal move that broadens SLB’s strategy from a pure hydrogen technology provider to an integrated industrial decarbonization partner. Champion X adds a portfolio of chemistry solutions and artificial lift technologies, allowing SLB to offer a more comprehensive suite of production and recovery services to industrial clients looking to reduce their carbon footprint, a market much larger and more immediate than just hydrogen production.

How do SLB’s partnerships with Genvia, John Cockerill, and Aramco/Linde work together?

These partnerships strategically cover both green and blue hydrogen pathways. The Genvia joint venture focuses on developing next-generation, high-efficiency solid oxide electrolyzers for green hydrogen. The collaboration with John Cockerill aims to scale up mature, commercially available alkaline electrolyzer technology, also for green hydrogen. The agreement with Aramco and Linde is for developing a massive Carbon Capture and Sequestration (CCS) hub, which is the critical enabling infrastructure for large-scale blue hydrogen production.

What are the key technologies SLB is focused on in its hydrogen portfolio?

SLB’s technology focus has matured from R&D to commercial supply. It includes co-developing high-performance solid oxide electrolyzer (SOE) technology through Genvia to improve efficiency, scaling mature alkaline electrolyzer technology with John Cockerill, and providing its core subsurface expertise for Carbon Capture and Sequestration (CCS) projects. Additionally, it is now manufacturing supporting hardware, like AI-enabling components at its Louisiana facility, and specific products like hydrogen-ready valves.

What are the main indicators to watch for in 2026 to gauge the success of SLB’s hydrogen strategy?

There are three critical indicators to monitor. First, the commercialization of its Genvia technology, specifically whether pilot projects with Arcelor Mittal and Vicat result in full-scale deployment orders. Second, progress on enabling infrastructure, such as a Final Investment Decision (FID) on the Saudi Arabia CCS hub with Aramco and Linde. Finally, the ultimate proof will be in financial results—specifically, consistent quarterly revenue growth in the New Energy division toward its $3 billion by 2030 target.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.