BESS Fire Risk Escalation, $12.8 B Safety Market, 28% Defect Rate, and 3 State Regulations (2024-2026)

Industrial Risk, BESS Deployment Growth Multiplies Fire Incidents

The rapid, large-scale deployment of Battery Energy Storage Systems (BESS) is amplifying fire risk from a manageable technical issue into a systemic industrial hazard, as the sheer density of stored energy increases the consequences of a single cell failure. The velocity of BESS commercialization has outpaced the maturation of universal safety protocols, creating a critical window of vulnerability for developers, financiers, and grid operators. This shift demands that BESS safety be treated with the same rigor as established industrial facilities like chemical plants or refineries.

- Between 2021 and 2024, BESS deployments grew steadily, with fire incidents often treated as isolated technical failures that could be addressed at the cell or module level. The primary industry focus remained on reducing costs and improving performance metrics to compete with traditional grid assets.

- From 2025 to today, the scale has fundamentally changed the risk profile. US BESS capacity is now projected to exceed 600 GWh by 2030, with major developers like Spearmint Energy adding tens of gigawatts to interconnection queues. This concentration means a single manufacturing defect, which accounts for an estimated 28% of lithium-ion fires, can now trigger a catastrophic, cascading thermal runaway event.

- The financial exposure has grown in parallel. With installed BESS costs ranging from $250 to $580 per k Wh in 2026, a fire at a typical 100 MWh facility now represents a direct asset loss of over $25 million, excluding business interruption, regulatory fines, and site remediation costs. This escalating financial risk is forcing the industry to re-evaluate its safety-cost trade-off.

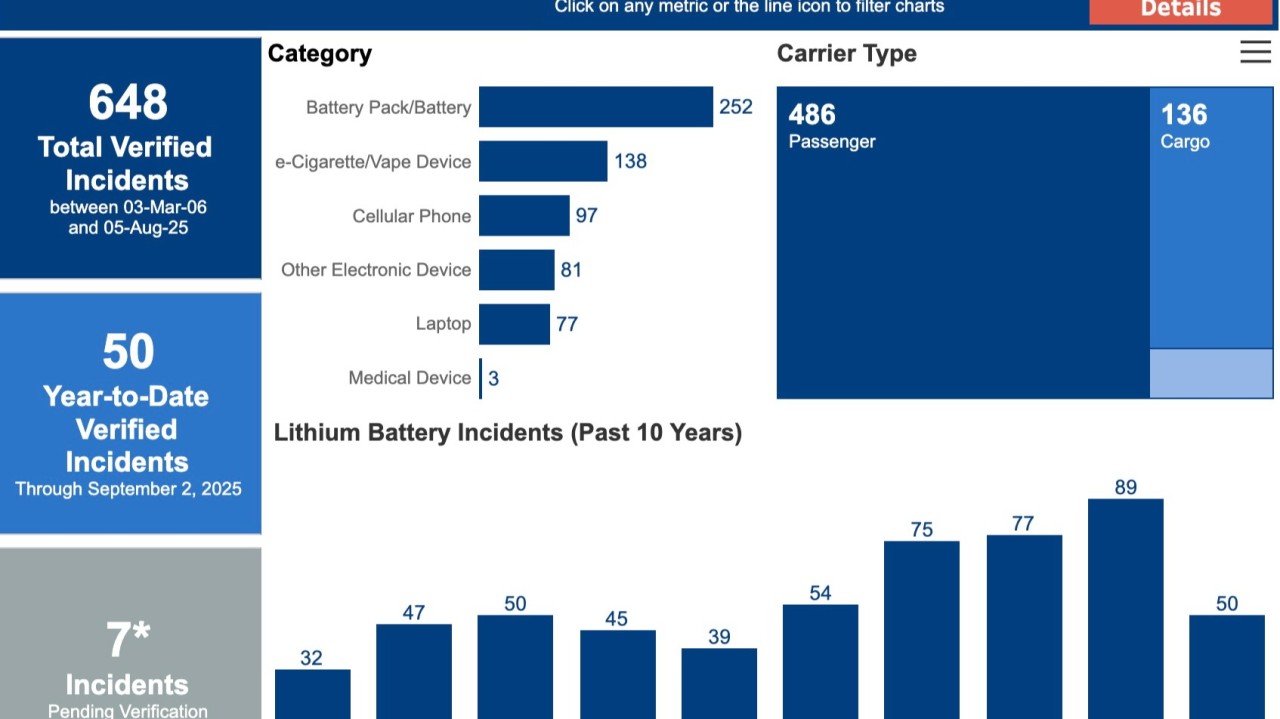

Data Shows Rising Trend of Lithium Battery Incidents

The chart’s depiction of a rising trend in incidents visually supports the section’s argument that BESS deployment growth is multiplying fire events.

(Source: LinkedIn)

US vs. EU Regulations, BESS Fire Safety Compliance Patchwork

A fragmented and evolving regulatory landscape is emerging, with key regions like the United States and European Union developing distinct and often stricter safety standards that create complex compliance challenges for BESS developers. While federal standards provide a baseline, a patchwork of state and local rules is now the primary driver of safety requirements, forcing a shift from a one-size-fits-all compliance strategy to a location-specific risk mitigation approach.

- In the US, federal standards such as NFPA 855 have historically set the benchmark. However, from 2025 onward, states have begun imposing more stringent rules. California enacted new laws (SB 283, SB 38) and CPUC general order modifications mandating the highest available safety standards, while Texas is proposing its own state-level permits with detailed emergency response plans.

- This state-led action is a direct response to public safety concerns and high-profile incidents, leading to project friction. In regions like New York and Massachusetts, local opposition and proposed moratoriums on new BESS projects have created significant development hurdles for asset owners like Recharge Power and Repono Energy.

- The European Union is pursuing a more centralized strategy with its EU Battery Regulation, which becomes fully applicable by August 2025. It imposes comprehensive safety, performance, and labeling requirements on all batteries sold in the EU, creating a uniform but demanding compliance environment for global manufacturers and operators such as Rolls-Royce.

Class L Fire Standard, BESS Hazard Recognition Reaches Maturity

The technical understanding of lithium-ion fire risk has matured to the point of formal recognition with a new fire classification, even as the industry’s preferred long-term solution, inherently safer battery chemistries, remains years from commercial scale. This formalization signals a critical shift from treating battery fires as conventional events to acknowledging their unique electrochemical hazards, demanding specialized suppression and response protocols.

- A significant milestone is the introduction of Class L in the upcoming ISO 3941:2026 update, a new fire classification specifically for fires involving electrochemical devices. This officially separates lithium-ion battery incidents from traditional fires, codifying their unique behavior, including thermal runaway, the release of flammable and toxic gases, and the high potential for re-ignition.

- Before 2024, mitigation efforts were primarily focused on cell-level chemistry and manufacturing quality. The current focus has shifted to system-level prevention and containment, with advanced Battery Management Systems (BMS), early off-gas detection, and sophisticated thermal management, including immersion cooling, becoming essential for preventing propagation in large-scale deployments.

- While safer long-duration technologies like Form Energy’s iron-air chemistry and advanced lithium-sulfur batteries from developers like Lyten offer a future path, they are not yet at the scale of lithium-ion. The dominant incumbent technology, supplied by giants like Sungrow, will define grid-scale storage risk for at least the next decade, making management of its fire hazard a top industry priority.

ISO Introduces New ‘Class L’ for Battery Fires

The chart’s headline announces the new ‘Class L’ fire standard, which is the central topic of this section about maturing hazard recognition.

(Source: LinkedIn)

SWOT Analysis, BESS Industrial Risk and Mitigation Strategies

The BESS market’s primary strength lies in its indispensable role in the global energy transition, but this is directly threatened by the inherent fire risk of lithium-ion chemistry and an increasingly complex regulatory environment. This tension creates significant opportunities for specialized safety technology providers and new business models, while posing a systemic threat to developers and investors who fail to adapt.

BESS Fire Safety Technologies Categorized

The chart categorizes fire safety technologies, directly supporting the ‘Mitigation Strategies’ component of the SWOT analysis discussed in this section.

(Source: IDTechEx)

Table: SWOT Analysis for BESS Fire Safety Risk

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Deployment growth driven by falling battery pack costs and renewable integration mandates. BESS begins to establish grid-support value. | Exponential deployment growth projected to exceed 600 GWh in the US by 2030. LCOS for 4-hour systems falls below $100/MWh, reaching economic tipping points over gas peakers. | The economic and strategic indispensability of BESS for grid stability and decarbonization is now validated at scale, making it a permanent fixture of energy infrastructure. |

| Weaknesses | Fire incidents were often viewed as isolated technical failures or “black swan” events. The primary weakness was seen as cost and duration limitations. | Thermal runaway is now understood as a systemic, predictable risk. Manufacturing defects (28% of fires) are a known trigger, and propagation in dense systems is a primary concern. | The risk is no longer seen as a random bug but an inherent chemical property of the technology at scale, shifting the focus from prevention alone to holistic risk management. |

| Opportunities | General industrial fire safety companies offered adapted solutions. The opportunity was in selling standard equipment to a new market. | A dedicated BESS fire suppression market emerges, valued at $4.2 billion in 2025 and forecast to hit $12.8 billion by 2034, with specialized tech like Full Circle Lithium’s FCL-X™GEL. | A specialized, high-growth BESS safety and risk mitigation market has been created, attracting investment and spurring innovation in detection and suppression. |

| Threats | Project-specific “Not In My Backyard” (NIMBY) opposition based on general safety concerns. Insurance was available with standard underwriting. | Widespread, organized community opposition and proposed government moratoriums (e.g., Massachusetts). Rising insurance premiums and stricter underwriting threaten project bankability. | The threat has scaled from localized project delays to a systemic market risk that can impact regional deployment targets and the overall cost of capital for the entire sector. |

BESS Fire Safety 2026, Insurance Premiums and NFPA 855 Compliance

For 2026, the primary signal to watch is the insurance market’s reaction to BESS fire risk; rising premiums and stricter underwriting tied to compliance with NFPA 855 and large-scale fire testing (UL 9540 A) will become a key determinant of project viability. Financiers and insurers will increasingly mandate advanced safety features not just as a best practice, but as a non-negotiable condition for investment.

- If a major, highly publicized BESS fire occurs near a population center in 2026, watch for an immediate and sharp increase in insurance costs across the board, coupled with the potential for a federal-level regulatory inquiry that moves beyond the current state-by-state approach.

- This could be happening as insurers are already actively repricing risk and tightening policy terms for BESS projects. This trend will accelerate, compelling developers like Infinite Grid Capital to adopt more expensive, robust suppression and detection systems as a baseline requirement to secure financing and coverage.

- If adoption of advanced diagnostics like off-gas detection and safer designs becomes standard practice for new deployments from manufacturers like LONGi, watch for the emergence of a two-tiered asset market. Older, less-safe facilities may become difficult to insure or sell, potentially becoming stranded assets.

- This could be happening as the dedicated market for BESS fire protection is forecast to grow at a strong 13.2% CAGR, signaling powerful demand for these advanced safety features, driven by both regulation and market pressure. This is a global trend, impacting ambitious national programs like India’s push for expanded energy storage.

Lithium Battery Fire Costs Reach $1.2B in US/Canada

This chart provides the financial context for the discussion on insurance premiums by quantifying the significant monetary cost of battery fires.

(Source: Large Battery)

The questions your competitors are already asking

This report covers one angle of the industrial-scale fire risk associated with Battery Energy Storage Systems (BESS). The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the $12.8B BESS fire safety market?

- What is the true financial exposure from a BESS fire, including direct asset loss, business interruption, and regulatory fines?

- How do different fire suppression technologies compare for mitigating cascading thermal runaway in utility-scale BESS?

- Which utility-scale developers are adopting advanced fire safety and monitoring solutions for their BESS portfolios?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.