BESS Market Economics, CATL €4.1 B Stellantis JV, 10 GWh Schroders Deal, and 50 GWh Sieyuan Agreement (2021 to 2026)

BESS Adoption, CATL and BYD 50 GWh Deals and Sodium-Ion Commercialization

Chinese battery manufacturers, led by CATL and BYD, are shifting from being component suppliers to full system integrators, accelerating BESS adoption in Europe and the Middle East by offering advanced, lower-cost solutions at a scale that Western competitors struggle to match. This strategic pivot is fundamentally altering grid storage economics, making large-scale renewable integration more financially viable.

- Between 2021 and 2024, the strategy was focused on market entry and establishing industrial credibility. This was demonstrated by CATL initiating production at its €1.8 billion German gigafactory in late 2022 and securing major supply agreements with European automotive giants like the BMW Group. BYD expanded its footprint by promoting its proprietary Blade Battery technology and achieving milestones with its residential Battery-Box systems in Europe.

- From 2025 onward, the approach has become far more aggressive and integrated. In early 2026, CATL announced a landmark memorandum of understanding with asset manager Schroders to develop up to 10 GWh of BESS projects, moving beyond supply to co-development. This was accompanied by a colossal 50 GWh framework supply agreement with Sieyuan, cementing its volume leadership.

- During this same period, BYD executed large-scale infrastructure projects, such as the 500 MWh BESS facility in Bulgaria inaugurated in January 2026, one of the largest in Eastern Europe. This demonstrates a clear transition from selling products to delivering and operating critical grid assets, a far more embedded role in the European energy system.

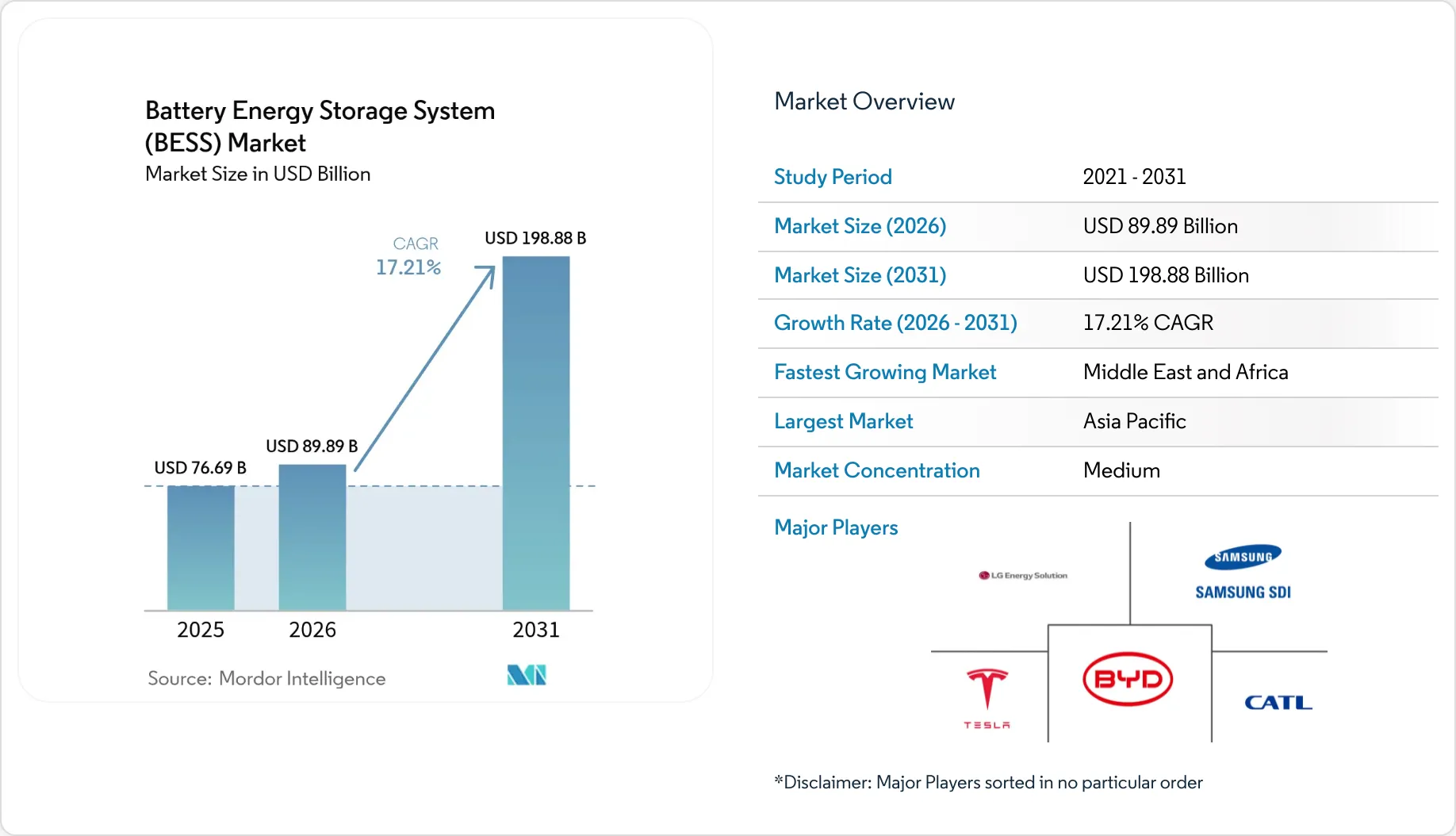

BESS Market to Exceed $198B by 2031

This chart quantifies the rapid BESS market expansion that is being accelerated by the cost-effective, large-scale solutions offered by CATL and BYD.

(Source: Mordor Intelligence)

€4.1 B Stellantis JV, CATL Expands European BESS Manufacturing Capacity

CATL is executing a capital-intensive strategy to embed its manufacturing and supply chains within Europe, moving from a primarily export-led model to localized production to capture market share and mitigate geopolitical risk. This investment is backed by a surging market valuation and is mirrored by BYD’s parallel investments in regional production hubs.

- The foundational investment phase between 2021 and 2024 was marked by CATL’s €1.8 billion commitment to its Arnstadt, Germany gigafactory, which began cell production in December 2022 with an initial capacity of 14 GWh. This move established a critical production beachhead inside the EU single market to serve key clients.

- In late 2024, CATL announced a far deeper industrial partnership: a joint venture with Stellantis worth up to €4.1 billion to construct a large-scale LFP battery plant in Spain. This signifies a move from being a foreign supplier to an integrated local partner for major European industrial players.

- The market recognized this strategic positioning in March 2026, when geopolitical tensions spurred a “paradigm shift” in energy security, adding over $70 billion to the collective market capitalization of CATL, BYD, and peer Sungrow. This financial uplift provides substantial capital for further global expansion and reinforces their ability to out-invest competitors.

- BYD is pursuing a similar localization strategy, exemplified by its investment in a greenfield EV plant in Hungary. While focused on vehicles, this builds a logistical and supply chain foundation that can be directly leveraged for BESS production and assembly within the EU.

Table: Strategic Investments by CATL and BYD in Europe

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Stellantis Joint Venture | 2024 | Investment up to €4.1 billion for a large-scale LFP battery plant in Spain. Secures a major European automaker as a long-term offtaker and deepens industrial integration. | Stellantis Corporate |

| German Gigafactory (G 2) | 2022 | €1.8 billion investment in Arnstadt, Germany, for a plant with 14 GWh initial capacity. Establishes a manufacturing footprint inside the EU to directly supply European clients. | Energetica India |

| Hungarian EV Plant | 2026 (Ongoing) | BYD is building a high-capacity EV plant in Hungary. While not a direct BESS investment, it creates a crucial logistical and supply chain hub within the EU for future energy storage expansion. | Investment Monitor |

CATL 10 GWh Schroders Deal and BYD’s 500 MWh Contour Global Project (2022 to 2026)

CATL and BYD have evolved their partnership strategy from standard supply agreements to sophisticated, multi-GWh collaborations with financial and energy majors, effectively locking in long-term demand and market access in Europe and the Middle East. This progression is a key factor in the overall Battery Storage Market Analysis: Growth, Confidence, and Market Reality(2023-2025).

Utility-Scale Projects Dominate $15.4B BESS Market

This chart provides the market context for the multi-GWh collaborations discussed, showing the current market size and the dominance of the utility-scale segment.

(Source: Market.us)

- Between 2022 and 2024, partnerships were characterized by large-volume supply contracts that established market credibility. Key examples include CATL’s multi-year deal to supply cylindrical cells to the BMW Group (2022), its agreement to supply its TENER product to Rolls-Royce (2024), and its 4 GWh supply deal with Israeli integrator BLEnergy (2024).

- Starting in 2025, the nature of these agreements shifted toward deeper strategic integration. The Mo U signed in February 2026 between CATL, Schroders, and Lochpine to create a 10 GWh European BESS investment platform is not merely a supply contract but a framework for joint development and capital deployment.

- Similarly, BYD’s role in the 500 MWh project with Contour Global in Bulgaria, inaugurated in January 2026, shows its technology being deployed in large, publicly-funded European infrastructure projects. This contrasts with earlier, smaller-scale C&I or residential partnerships and demonstrates a new level of market trust and penetration.

- These firms also secure massive global supply chains that feed into their European and Middle Eastern strategies. In January 2026, CATL inked a 50 GWh framework agreement with Sieyuan, while BYD secured a 2.6 GWh battery sale to Grenergy in March 2026 for projects in Chile, showcasing their global scale.

Table: Key Partnerships and Commercial Agreements (2024-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Schroders & Lochpine | 2026 | Mo U to launch a joint investment platform to develop up to 10 GWh of BESS projects across Europe, with CATL as the primary technology supplier. | IPE Real Assets |

| Contour Global | 2026 | Inauguration of a 500 MWh BESS project in Bulgaria using BYD technology. It is one of the largest in Eastern Europe and BYD‘s largest in the region. | Contour Global |

| Sieyuan | 2026 | CATL signed a monumental 50 GWh multi-year framework supply agreement, locking in a major customer for its advanced LFP battery cells. | ESS-News |

| BLEnergy (Israel) | 2024 | CATL secured a long-term agreement to supply 4 GWh of battery storage products, marking a significant entry into the growing Middle Eastern market. | ESS-News |

| Rolls-Royce Power Systems | 2024 | Partnership to integrate CATL‘s TENER product line into Rolls-Royce‘s mtu Energy Pack QG solution for the large-scale BESS market in Europe. | Turbomachinery Magazine |

Europe vs. Middle East, CATL and BYD BESS Deployment Strategy

While both CATL and BYD are aggressively targeting Europe with large-scale manufacturing and financial partnerships, the Middle East is emerging as a strategic growth frontier where they are establishing initial market presence through key distribution deals and initial supply agreements, positioning for future expansion. This two-pronged geographic approach differs from the domestic focus seen in discussions around US Battery Storage 2026: Can Factories Meet Demand?.

Middle East BESS Market to Hit $6.86B

This chart quantifies the growth potential in the Middle East, directly supporting the section’s focus on this region as a strategic growth frontier for CATL and BYD.

(Source: Mordor Intelligence)

- In Europe, the strategy is one of deep industrial integration. Activity is concentrated in key countries that serve the entire continent. CATL‘s factories in Germany and Hungary, along with BYD’s planned Hungarian plant, serve as central production hubs. Deployments are also becoming widespread, with major projects in Bulgaria (BYD‘s 500 MWh project) and the UK (CATL‘s planned 1 GWh+ project with Quinbrook).

- The Middle East strategy is currently in a more nascent, market-seeding phase. Rather than building factories, the focus is on securing footholds. CATL‘s 4 GWh supply deal with BLEnergy in Israel in 2024 was a significant first move. This was followed by reports in March 2026 of Qatar actively positioning itself to attract battery market investment.

- BYD has used its electric vehicle division as a Trojan horse for its energy solutions in the region. By launching its EV models and opening showrooms in the UAE (2023) and Jordan (2023), it establishes brand presence and a distribution network that can later be used to introduce its BESS products. This positions the company to capitalize on the region’s anticipated rapid growth.

BESS Technology at Scale, CATL Zero Degradation and BYD Sodium-Ion Breakthroughs

CATL and BYD are pushing BESS technology beyond incremental improvements, launching mass-producible systems with zero-degradation claims and commercializing alternative chemistries like sodium-ion, directly addressing the core operator concerns of longevity and cost. This rapid innovation cycle is setting new performance and economic benchmarks for the grid storage industry.

Lithium-Ion to Dominate BESS Market Through 2030

This chart highlights the current dominance of Lithium-ion technology, providing a backdrop for the technological breakthroughs in LFP and Sodium-ion discussed in the section.

(Source: MarketsandMarkets)

- The period between 2021 and 2024 was about refining and scaling Lithium Iron Phosphate (LFP) chemistry for stationary storage. Innovations like BYD’s Blade Battery and CATL’s Qilin Battery (2023) focused on improving energy density and safety through advanced cell-to-pack designs, solidifying LFP’s dominance over other chemistries for grid applications.

- A technological leap occurred from 2025 onward. In April 2024, CATL launched TENER, the first mass-producible BESS claiming zero degradation in its first five years. In March 2026, BYD followed with its second-generation Blade Battery, featuring a lifespan exceeding 5, 000 cycles and ultra-fast charging capabilities.

- Most significantly, both companies have made major strides in commercializing sodium-ion batteries, a lower-cost, lithium-free alternative. In February 2026, BYD announced it had developed sodium-ion batteries with a cycle life of up to 10, 000 cycles. Two months later, at the ESIE expo in Beijing, CATL showcased its own commercially ready sodium-ion BESS cells, signaling the technology’s readiness for market deployment.

SWOT Analysis, CATL & BYD BESS Strategy Strengths and Regulatory Threats

The primary strength of CATL and BYD lies in their unparalleled manufacturing scale and deep vertical integration, which allows them to lead on cost and technology. However, this externally-focused dominance creates a significant vulnerability to geopolitical and regulatory headwinds in Europe, their key expansion market.

- Strengths in manufacturing scale and cost leadership have become solidified, moving from a potential advantage in 2021 to a proven market-shaping force by 2026, evidenced by multi-GWh supply deals.

- Weaknesses, such as a historical reliance on the domestic Chinese market, have been actively mitigated through strategic investments in European factories and deep partnerships with local industrial giants like Stellantis and BMW.

- Opportunities presented by the European and Middle Eastern energy transitions have been validated, with massive market growth forecasts materializing into concrete, large-scale project announcements and a new technology frontier opening with sodium-ion.

- Threats from protectionist policies have become more concrete. Vague geopolitical tensions in 2022 have evolved into specific legislative proposals like the EU’s Industrial Accelerator Act by 2026, which poses a direct challenge to their market access model.

Table: SWOT Analysis for CATL and BYD in European & Middle Eastern BESS Markets

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Emerging scale and cost advantages from the Chinese domestic market. Vertically integrated supply chain for raw materials. Proven LFP technology. | Dominant manufacturing capacity (approaching 60% global share). Demonstrated technological leadership (Blade 2.0, TENER). Cost advantage of 15-20% over Western OEMs. | Scale and cost advantages transitioned from theoretical to a tangible, market-shaping force, validated by massive GWh deals and clear price leadership. |

| Weaknesses | Limited brand recognition in Europe outside of B 2 B. Production capacity heavily concentrated in China, posing supply chain risks. | Geopolitical liability as Chinese-owned entities. Still building out European service and O&M networks to support large-scale deployments. | The weakness shifted from logistical (supply chain) to geopolitical (origin). Direct European investments (German, Hungarian factories) are actively mitigating this. |

| Opportunities | Nascent but growing EU and MEA demand for BESS to support renewable integration and grid stability. | Explosive market growth (Europe projected at $24.2 B in 2026). Emergence of sodium-ion as a lower-cost alternative. Demand for integrated EV charging/BESS solutions. | The opportunity was validated and its scale vastly exceeded initial projections. The development of sodium-ion created a new, non-lithium-dependent growth vector. |

| Threats | General geopolitical tensions between the West and China. Potential for future tariffs or trade barriers. Competition from other Asian and Western players. | Concrete EU regulations like the Industrial Accelerator Act with “Made in EU” requirements. Scrutiny over data security and critical infrastructure control. | The threat evolved from a vague risk of tariffs to specific, targeted industrial policies designed to limit dependency on Chinese technology suppliers. |

EU Regulatory Push vs. Market Reality, CATL’s Next Move

The most critical dynamic to watch in the coming year is the collision between the EU’s push for a domestic supply chain via policies like the Industrial Accelerator Act and the market’s dependence on the cost-effective, high-performance BESS solutions offered by CATL and BYD. This tension will determine the investment climate, making the topic of Battery Storage 2026: The #1 Energy Investment Choice a complex one for regional stakeholders.

- If the EU strictly enforces “Made in EU” local content requirements, watch for CATL and BYD to accelerate announcements for European recycling plants and component factories to comply. Their recent inquiries into European recycling operations in late 2024 are an early signal of this anticipatory strategy.

- If project economics and the lowest Levelized Cost of Storage (LCOS) remain the primary drivers for developers, watch for the market share of Chinese suppliers to expand further. The success of the CATL-Schroders 10 GWh platform and the commercial rollout of even cheaper sodium-ion batteries will be key indicators of this trajectory.

- This could be happening now: A two-tiered market is likely emerging. One tier will consist of premium, EU-compliant projects, possibly smaller in scale or higher in cost, that meet strict domestic sourcing rules. The other, larger tier will continue to prioritize the superior economics offered by CATL and BYD, forcing a potential policy compromise to avoid slowing down the energy transition. The rollout of BYD‘s planned 2, 000 integrated fast charger/BESS stations across Europe will be a major test case for this dynamic.

The questions your competitors are already asking

This report covers one angle of CATL and BYD’s BESS commercial strategy in Europe and the Middle East. The questions that matter most depend on your work.

- Which Western BESS integrators are losing ground to CATL and BYD in the European grid storage market?

- What is the status of the 50 GWh BESS framework supply agreement between CATL and Sieyuan?

- What is the outlook for the commercialization of Sodium-Ion BESS for European grid applications by 2026?

- Which European utilities and asset managers are co-developing large-scale BESS projects with CATL or BYD?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.