Baker Hughes Data Center Power, 1.21 GW Boom Supersonic Deal, $3 B Target, and 3 Major Contracts (2021 to 2026)

Industry Pivot to Data Center Power Projects Accelerates

Oilfield services (OFS) giants have decisively shifted from exploratory clean energy initiatives to securing large-scale commercial contracts for data center power, a strategic pivot validated by a surge in multi-megawatt deals since 2025. This transition marks the commercial validation of repurposing core competencies in complex project management and power systems engineering to solve the acute energy-for-AI bottleneck.

- Between 2021 and 2024, OFS companies focused on foundational partnerships and technology adaptation. SLB collaborated with NVIDIA and Microsoft to build digital platforms, while Halliburton incubated startups through its Labs program. Baker Hughes focused on making its Nova LT turbines hydrogen-ready. These actions built capability but did not yet represent a significant revenue shift.

- From January 2025, the strategy materialized into substantial commercial wins. Baker Hughes secured orders for its gas turbines from Frontier Infrastructure (270 MW) and Twenty 20 Energy, and a massive 1.21 Gigawatt generator order for a Boom Supersonic AI data center project.

- SLB’s Data Center Solutions business revenue doubled to $331 million in the first nine months of 2025, and the company became the official modular design partner for NVIDIA’s DSX AI data centers, moving from a technology collaborator to a critical infrastructure delivery partner.

- Halliburton solidified its market entry by taking a 20% stake in Volta Grid and securing manufacturing for 400 MW of modular power capacity, demonstrating a capital-efficient partnership model to capture immediate demand.

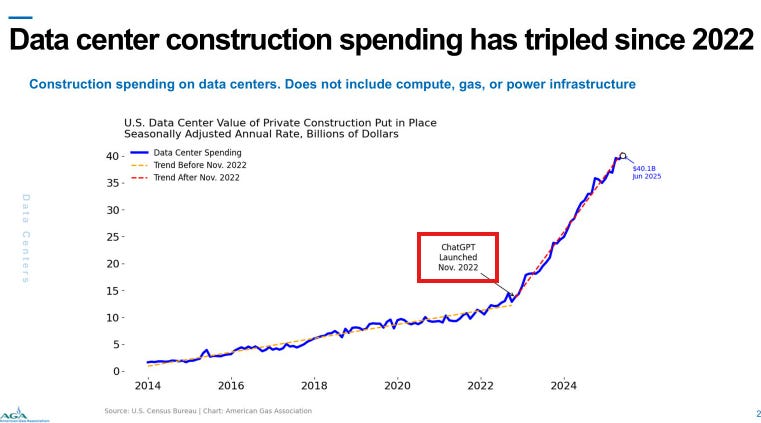

AI Boom Fuels Data Center Construction

This chart shows the massive surge in data center construction spending, which is the primary market demand driving the oilfield services pivot described in this section.

(Source: The Merchant’s News – Substack)

$3.3 B in Capital Commitments, OFS Companies Target Data Center Market

Capital deployment has shifted from internal R&D and minority stakes to direct investments in manufacturing capacity and large-scale project targets, signaling strong confidence in the data center power market as a primary growth vector. This strategic allocation of funds is designed to scale production and secure a dominant position in the power infrastructure supply chain for AI.

- Baker Hughes has been the most aggressive, doubling its data center equipment order target to $3 billion for the 2025-2027 period. This financial goal is supported by a robust and visible pipeline of large-scale turbine and generator orders.

- SLB is investing $30 million to expand its Shreveport, Louisiana, manufacturing facility. This investment will double the plant’s capacity for modular data center components and support its growing partnership with NVIDIA.

- Halliburton‘s approach is a 20% ownership stake in its key partner, Volta Grid. This move aligns interests and provides Halliburton with a dedicated vehicle for deploying distributed power solutions without the overhead of building the technology in-house.

Table: Strategic Investments by OFS Companies in Data Center Power (2025-2026)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Baker Hughes Order Target | Jan 2026 | Doubled its equipment order target for the data center market to $3 billion for the 2025-2027 period, reflecting a surge in demand and a strong project pipeline. | TT News |

| SLB Facility Expansion | Dec 2025 | Announced a $30 million investment to expand its Shreveport, Louisiana, facility to double manufacturing capacity for modular data center infrastructure. | Next MSC |

| Halliburton Stake in Volta Grid | Oct 2025 | Revealed a 20% ownership stake in distributed power specialist Volta Grid to jointly provide turnkey power solutions for data centers. | Fortune |

Data Center Supply Agreements, OFS Companies Partner with Tech and Infra Firms

Partnerships have matured from technology co-development to concrete supply and deployment agreements, reflecting a market shift towards execution. Where early alliances focused on building digital tools, recent collaborations are centered on delivering physical infrastructure and power capacity at an accelerated pace.

- The landmark collaboration is SLB becoming the modular design and deployment partner for NVIDIA‘s next-generation DSX AI data centers in March 2026. This moves SLB from being a software partner to a core part of NVIDIA‘s physical infrastructure strategy.

- Baker Hughes has established a strong partner ecosystem for hardware deployment. Key agreements include supplying 16 Nova LT™ turbines to Frontier Infrastructure and 10 Frame 5 turbines to Twenty 20 Energy, both for U.S. data center projects.

- In a significant move to integrate energy and digital technology, Baker Hughes partnered with Google Cloud in March 2026. The alliance aims to develop AI-enabled solutions for optimizing power and sustainability at data centers, combining hardware expertise with advanced software.

- Halliburton‘s primary partnership with Volta Grid resulted in a tangible commitment to secure manufacturing for 400 MW of power generation for data centers, moving the alliance from a strategic agreement to a project-focused delivery mechanism.

Table: Key Data Center Partnerships and Alliances (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| SLB & NVIDIA | Mar 2026 | SLB became the modular design partner for NVIDIA‘s DSX AI data centers, using off-site construction to accelerate deployment. | Wall Street Journal |

| Baker Hughes & Google Cloud | Mar 2026 | Partnership to develop AI-enabled power optimization and sustainability solutions for data centers, leveraging Google‘s AI and Baker Hughes‘ energy technology. | Baker Hughes |

| Baker Hughes & Boom Supersonic | Feb 2026 | Secured an order for 25 BRUSH generators as part of a 1.21 Gigawatt power solution for a major AI data center project. | Baker Hughes |

| Baker Hughes & CTR | Sep 2025 | Agreement to advance 500 MW of U.S. geothermal power projects specifically to serve the data center and AI sector, diversifying beyond gas turbines. | CTR |

US Market Focus, Baker Hughes and SLB Concentrate on Domestic Projects

The strategic pivot by oilfield services companies is overwhelmingly concentrated in the United States, targeting regions with heavy data center development and significant grid interconnection challenges. While some initiatives are aimed globally, the bulk of announced contracts, investments, and partnerships are for domestic projects, highlighting the U.S. as the primary battleground for this new market.

US Dominates Global Data Center Count

This chart quantifies why OFS companies are concentrating on domestic projects, as the US market for data centers is significantly larger than all other major countries combined.

(Source: The Merchant’s News – Substack)

- Between 2021-2024, partnerships like the one between SLB and Total Energies had a broader international focus on digital solutions. The geographic strategy was less defined and more about global capability building.

- The period from 2025 onward shows a clear geographical concentration. Baker Hughes‘ major turbine orders with Frontier Infrastructure are for data center projects located in Wyoming and Texas. Its generator order with Boom Supersonic and turbine deal with Twenty 20 Energy also target U.S. infrastructure.

- SLB‘s $30 million manufacturing expansion in Shreveport, Louisiana, is explicitly intended to serve the growing demand for digital infrastructure within the United States.

- The main exception is Halliburton and Volta Grid‘s initial 400 MW manufacturing commitment, which targets data centers in the Eastern Hemisphere. This suggests a two-pronged strategy, but the most visible, large-scale contracts remain U.S.-centric.

Gas Turbine Technology Maturity and Commercial Scale for Data Centers

The underlying power generation technology, natural gas turbines, is highly mature, but its specific application for data centers has rapidly advanced from concept to commercial scale since 2025. OFS firms are successfully marketing these systems not just as power sources but as integrated solutions offering a clear path to decarbonization through hydrogen fuel flexibility and carbon capture integration.

- In the 2021-2024 period, the focus was on adapting and proving the technology. Baker Hughes worked on validating its Nova LT turbines for 100% hydrogen operation, a crucial R&D step for future-proofing the solution. The dialogue was about potential applications.

- Starting in 2025, the technology is being sold at commercial scale. Baker Hughes is no longer just discussing hydrogen-readiness; it is selling Nova LT and Frame 5 turbines in large volumes for immediate natural gas operation, with hydrogen conversion as a contracted future option.

- The concept of Combined Heat and Power (CHP) has also matured. Instead of a theoretical efficiency gain, it is now a key selling point, with systems designed to capture waste heat from data centers to power cooling, boosting total efficiency toward 90%.

- Diversification into other mature technologies is also accelerating. Baker Hughes‘ partnership with CTR to advance 500 MW of geothermal power demonstrates a strategic move to offer firm, clean baseload power, repurposing decades of subsurface engineering expertise. Similarly, Chevron has pursued geothermal pilots to leverage its own drilling experience.

SWOT Analysis of OFS Pivot to Data Center Power

The strategic shift into data center power leverages the core engineering and project management strengths of oilfield services companies, presenting a significant revenue opportunity. However, it also exposes them to new competitive dynamics and operational challenges in scaling for a completely different industry.

Baker Hughes Demonstrates Improving Efficiency

Illustrating a key ‘Strength’ for the SWOT analysis, this chart shows Baker Hughes’s improving operational efficiency, a core competency being leveraged in its market pivot.

Table: SWOT Analysis for the OFS Pivot to Data Centers

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Core expertise in large-scale energy project management, global supply chains, and power systems engineering. | Demonstrated ability to convert expertise into multi-hundred MW and GW-scale commercial contracts (e.g., Baker Hughes deals). Proven success of modular construction (SLB). | The strength was commercially validated. The theoretical capability to execute complex projects translated into a tangible, multi-billion-dollar order book in a new industry. |

| Weaknesses | High exposure to cyclical oil and gas markets. Public perception as purely fossil fuel companies, creating potential ESG headwinds. | Need to rapidly scale manufacturing for a new sector (e.g., SLB‘s $30 M investment). Potential talent gap in data center-specific domains like high-density cooling. | The primary weakness shifted from market perception and cyclicality to the operational challenge of executing a rapid scale-up in a non-core market. |

| Opportunities | Emerging AI-driven energy demand was identified as a potential growth area. Grid constraints were a known but less acute problem. | Data center power demand is surging, and grid interconnection queues now span multiple years, creating massive, immediate demand for behind-the-meter distributed power. | The market opportunity evolved from a future trend into an urgent, present-day crisis for data center developers, dramatically increasing the value proposition of OFS solutions. |

| Threats | General competition from established Independent Power Producers (IPPs) and renewable energy developers. | Direct competition from other industrial giants like Caterpillar entering the CHP market. Emergence of specialized distributed power players (e.g., Crusoe). | The competitive field became more defined and direct. OFS companies are now competing head-to-head with other specialists aiming at the same data center power niche. |

Scenario: From Hardware Sales to Integrated Energy Providers

The critical factor for 2026 and beyond will be the successful execution of the current project backlog, converting massive orders into operational assets and recurring revenue. This will determine if the pivot is a temporary boom or a permanent transformation into integrated energy and technology infrastructure companies.

Investor Confidence in AI Infrastructure Surges

This chart reflects strong investor belief in the future success of ‘picks and shovels’ AI companies, validating the long-term transformation scenario described in this section.

- If this happens: OFS companies successfully bring their contracted gigawatts of power online for data centers on time and on budget.

- Watch this: An increase in M&A activity. As they prove their capability in power generation, watch for Baker Hughes, SLB, or Halliburton to acquire smaller technology firms specializing in battery energy storage systems (BESS), advanced cooling, or data center energy management software to offer a more vertically integrated solution.

- This could be happening: The business model shifts from one-time equipment sales to long-term Energy as a Service (Eaa S) contracts. Instead of just selling a turbine, they will sell guaranteed power and uptime for a 20-year term, creating a stable, high-margin recurring revenue stream that further decouples them from oil price volatility. The initial deals for geothermal development (Baker Hughes/CTR) are early signals of this trend.

The questions your competitors are already asking

This report covers one angle of the oilfield services pivot to data center power. The questions that matter most depend on your work.

- Which oilfield services companies are gaining or losing ground in the data center power market?

- What is the outlook for gas turbine and CHP deployment in AI data centers by 2030?

- How do gas turbines like the Baker Hughes Nova LT compare to fuel cells for powering AI data centers?

- Which hyperscalers and colocation operators are adopting on-site power from oilfield services companies?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.