BHP CCUS Hubs, $400 M Fund, 5 Sites with JSW Steel, and 6 Key Agreements (2021 to 2026)

CCUS Hub Adoption, BHP’s 6 Steelmaker Partnerships Signal Industry Shift

The adoption of Carbon Capture, Utilisation, and Storage (CCUS) in the Asian steel sector is moving from isolated, single-company studies to a consortium-led, shared infrastructure model, driven by major resource producers like BHP to de-risk their own value chains. This strategic shift addresses the prohibitive costs of standalone CCUS projects and aims to create a viable decarbonization pathway for an industry reliant on blast furnace technology. By orchestrating this ecosystem, BHP is working to secure long-term demand for its iron ore in a carbon-constrained world.

- Between 2021 and 2024, BHP’s strategy focused on bilateral R&D partnerships to explore decarbonization, including agreements with China Baowu and a $15 million commitment to JFE Steel. This approach laid the groundwork for understanding the technological needs of its key customers.

- A significant acceleration occurred in August 2025 with the launch of a global consortium, led by BHP, that includes major steelmakers Arcelor Mittal Nippon Steel India, JSW Steel, and Hyundai Steel, alongside energy major Chevron. This move marked a pivot from individual research to collective infrastructure development.

- The consortium’s focus quickly became tangible. By April 2026, after assessing over 3, 000 locations, it identified five promising sites for large-scale CO 2 storage hubs in India, Indonesia, Malaysia, and Australia, demonstrating a clear and structured execution plan.

- Underscoring this strategic shift, BHP announced a $400 million fund in April 2025 to invest in low-emissions technologies. The consortium also expanded in April 2026, adding logistics partner “K” LINE to address the critical challenge of CO 2 transportation.

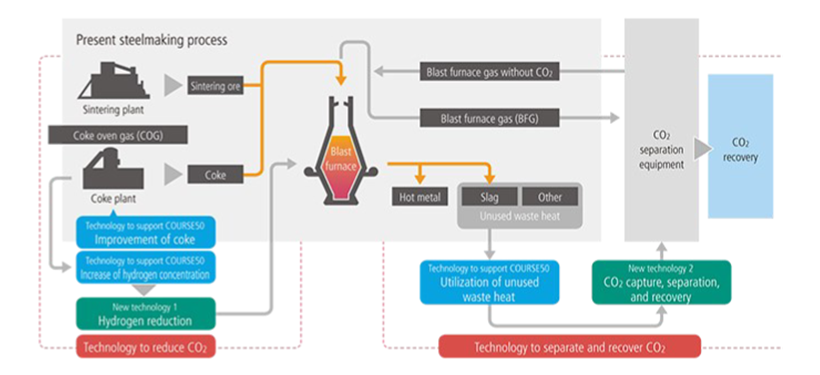

Visualizing Decarbonization for Blast Furnaces

The section discusses CCUS for the existing blast furnace industry, and this chart shows how CO2 capture technology integrates into that traditional process.

(Source: Ignacio Ibarrondo – Iron and Steelmaking)

$400 M Fund, BHP Investment in CCUS Hubs and Low-Carbon Tech

BHP‘s investment strategy for decarbonization has evolved from targeted R&D funding for individual partners to a broader, strategic capital allocation designed to build the foundational infrastructure for an entire industry. This approach reflects a recognition that solving the steel industry’s emissions problem requires system-level investment beyond the capabilities of any single operator, similar to efforts seen in the cement industry from companies like Holcim.

- In April 2025, BHP announced a commitment to invest $400 million over five years into a dedicated fund for low-emissions technologies. This capital is intended to support initiatives like CCUS, hydrogen, and other innovations across its value chain.

- This large-scale fund represents a significant evolution from its earlier approach, such as the June 2021 partnership with JFE Steel, which included a more targeted investment of up to $15 million for collaborative research.

- The potential scale of investment required for the CCUS hubs is substantial. For context, Petronas’s Kasawari CCS project in Malaysia, a region also targeted by the BHP consortium, has an estimated cost of $1.07 billion, providing a financial benchmark for future capital deployment.

- BHP‘s demonstrated capacity to execute mega-projects, such as its over $10 billion investment in the Jansen potash project, signals its capability and willingness to deploy the significant capital that will be necessary to build out commercial-scale carbon infrastructure.

Table: BHP Strategic Decarbonization Investments

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Strategic Decarbonization Fund | Apr 2025 | A $400 million, five-year fund for developing low-emissions technologies, including CCUS and hydrogen, to support value chain decarbonization. | Asia Fund Managers |

| Partnership with JFE Steel | Jun 2021 | Up to $15 million over five years to fund joint R&D into decarbonization technologies, including CCUS, for the integrated steelmaking process. | White & Case LLP |

BHP 6 Key Alliances, JSW Steel to Chevron (2021 to 2026)

BHP has strategically constructed a multi-layered partnership ecosystem, progressing from bilateral R&D agreements with steelmakers to a broad, cross-industry consortium that now includes energy majors, technology providers, and logistics firms. This collaborative model is essential for tackling the complexities of cross-border carbon management.

BHP’s Vision for an Asian CCUS Network

This section describes the formation of a partnership ecosystem, and this chart illustrates the end-goal of that ecosystem—a network of CCUS hubs across Asia.

(Source: Discovery Alert)

JFE Steel’s Path to Carbon Neutrality

As the section’s table lists BHP’s R&D partnership with JFE Steel, this chart provides direct context on JFE’s own multi-faceted decarbonization strategy.

(Source: Ignacio Ibarrondo – Iron and Steelmaking)

- The initial phase of partnerships from 2021 to 2024 focused on foundational R&D with individual steelmakers, including agreements with Japan’s JFE Steel, China’s Baowu, and India’s JSW Steel to explore a range of technology options.

- In August 2025, the strategy pivoted to collective action with the formation of the Asian CCUS Hub consortium. This brought together competitors Arcelor Mittal Nippon Steel India, JSW Steel, and Hyundai Steel with energy partner Chevron.

- Signaling a move toward implementation, the consortium expanded in April 2026 by adding Japanese shipping company “K” LINE. This addresses the crucial logistics of transporting captured CO 2 from industrial sites to permanent storage hubs.

- In parallel, BHP maintains partnerships focused on alternative long-term technologies. An October 2025 agreement with POSCO targets hydrogen-based iron production, while the Neo Smelt joint venture with Rio Tinto and others explores a new DRI-based process.

Table: BHP Key Decarbonization Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| “K” LINE | Apr 2026 | Addition of the shipping company to the Asian CCUS Hub consortium to provide expertise on CO 2 transportation logistics. | Maritime Fairtrade |

| POSCO | Oct 2025 | Technology development agreement to jointly advance ‘near zero’ emissions iron production using hydrogen-based technologies. | Reuters |

| Arcelor Mittal, JSW, Hyundai, Chevron | Aug 2025 | Formation of a consortium to launch a pre-feasibility study for shared, large-scale CCUS hubs across Asia for hard-to-abate industries. | BHP |

| China Baowu | Apr 2022 | Five-year R&D partnership to investigate greenhouse gas reduction, including the deployment of CCUS in the steel value chain. | ARC Group |

| JFE Steel | Jun 2021 | Five-year, up to $15 million funding agreement for collaborative research into steel decarbonization technologies, including CCUS. | White & Case LLP |

Asia-Pacific Focus, BHP CCUS Hubs Target India, Malaysia, Australia

BHP’s decarbonization infrastructure efforts are geographically concentrated in the Asia-Pacific region, strategically aligning with its primary iron ore customer base and moving from general agreements to identifying specific countries for large-scale CCUS infrastructure development. This targeted approach increases the likelihood of tangible project development by focusing on areas with both high emissions and favorable geology.

Conceptualizing the Asian CCUS Hub

This section’s focus on an Asia-Pacific hub, including India, directly aligns with the chart’s conceptual depiction which includes Japanese and Indian flags.

(Source: Discovery Alert)

POSCO’s Hydrogen-Based Steelmaking Process

The section’s table explicitly notes a partnership with POSCO on hydrogen technology, and this chart perfectly illustrates that specific process.

(Source: Ignacio Ibarrondo – Iron and Steelmaking)

- Between 2021 and 2024, BHP‘s activities were centered on partnerships with companies in major Asian steelmaking nations, including Japan (JFE Steel), China (Baowu), and India (JSW Steel), without defining specific infrastructure locations.

- A critical development occurred by April 2026, when the consortium’s pre-feasibility study identified five specific, promising locations for developing CCUS hubs. This shortlisted two sites in India, and one each in Indonesia, Malaysia, and Australia.

- This geographic focus demonstrates a pragmatic strategy, targeting countries with significant industrial emissions from sectors like steel and cement, combined with potential for geological CO 2 storage.

- The inclusion of Australia as a potential hub location connects BHP’s domestic operational footprint and resource base to its broader regional decarbonization strategy, potentially creating an export market for carbon storage services.

CCUS Commercialization, BHP Prioritizes Hubs Over Green Steel R&D

While long-term “green steel” technologies like hydrogen-based ironmaking remain in development, BHP‘s strategy prioritizes the near-term commercial deployment of CCUS as a bridging solution for the existing blast furnace infrastructure that dominates Asian steel production. This pragmatic approach acknowledges that replacing the entire existing asset base is not feasible in the short-to-medium term.

- From 2021 to 2024, BHP’s focus was on exploring a wide range of decarbonization technologies through its partnerships. This included research into CCUS as one of several potential pathways.

- The launch of the multi-stakeholder CCUS hub consortium in August 2025 marked a decisive strategic pivot towards deploying CCUS at a commercial scale. This implicitly recognizes CCUS as the most viable option for achieving significant emissions reductions from existing infrastructure this decade.

- The consortium is evaluating specific, commercially ready technologies. A feasibility study with JSW Steel is assessing Carbon Clean’s modular Cyclone CC system, a technology aimed at reducing the cost and physical footprint of carbon capture plants.

- This near-term focus on CCUS is pursued in parallel with longer-term technology bets. The Neo Smelt joint venture, with a Final Investment Decision (FID) anticipated in 2026, and the hydrogen-iron partnership with POSCO represent hedges on future technological breakthroughs.

SWOT Analysis, BHP’s CCUS Strategy Strengths and Market Risks

BHP‘s strength lies in its ability to leverage its market position and financial capacity to orchestrate a complex, multi-stakeholder solution to a system-level problem. However, the strategy faces external threats from the high costs of CCUS and the potential for disruptive green steel technologies to mature faster than expected.

Table: SWOT Analysis for BHP’s Shared CCUS Infrastructure Strategy

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated / Poses Risk |

|---|---|---|---|

| Strengths | Strong balance sheet; deep relationships with key steelmakers (JFE, Baowu, JSW) through bilateral R&D partnerships. | Demonstrated ability to lead a complex, multi-company consortium; commitment of significant capital ($400 M fund). | Validated its position as an indispensable orchestrator in the value chain, not just a supplier. |

| Weaknesses | High exposure to steel industry’s Scope 3 emissions; strategy dependent on partner buy-in and technology that was not yet proven at scale. | Execution now depends on managing a complex web of partners with potentially competing interests across different countries. | The complexity of managing a multi-national, multi-company consortium introduces significant project management risk. |

| Opportunities | Potential to secure long-term iron ore demand by helping customers decarbonize; nascent concept of shared infrastructure. | Rising carbon prices (projected $20-55/tonne) improve project economics; identification of 5 hub sites creates a tangible roadmap. | The business case for shared CCUS infrastructure is becoming stronger due to market and regulatory drivers. |

| Threats | High cost of CCUS was a major barrier; uncertainty over which decarbonization technology (CCUS vs. hydrogen) would prevail. | CCUS costs remain high ($141-$287/ton); logistical challenges (CO 2 shipping) become a primary focus; alternative tech (Neo Smelt) advances in parallel. | The core economic and technological competition risks remain, and logistical complexity is now a primary, rather than secondary, hurdle. |

2026 FID, BHP’s Neo Smelt Decision and CCUS Hub Progress

The critical event to watch in 2026 is the conclusion of the CCUS hub pre-feasibility study, which will determine if the consortium commits capital to a Front-End Engineering and Design (FEED) stage for one of the five identified sites. This decision will be a key validation point for the shared infrastructure model for industrial decarbonization in Asia.

- If the pre-feasibility study, scheduled to conclude by the end of 2026, produces a strong business case, watch for an announcement launching Phase 2. This would likely involve a detailed FEED study for the most promising hub location and the formation of a formal joint venture to develop the project.

- A parallel signal to monitor is the 2026 Final Investment Decision (FID) for the Neo Smelt project. A positive decision would validate a key alternative technological pathway, whereas a delay or cancellation would further underscore the immediate importance of CCUS for existing blast furnaces.

- Progress in building out the value chain will also be critical. Observe whether the consortium can secure agreements with additional emitters, such as cement producers, which would strengthen the economic case for shared infrastructure and reduce per-ton abatement costs.

The questions your competitors are already asking

This report covers one angle of building cross-industry carbon infrastructure for the steel sector. The questions that matter most depend on your work.

- BHP’s activities in CCUS hubs. Is the global steelmaker consortium progressing from site selection to deployment?

- What is the outlook for shared CCUS hub deployment in the Asian steel sector by 2030?

- Which steelmakers are adopting the consortium-led CCUS hub model?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.