BESS Policy Risk, $35 B in US Project Cancellations, 10.4 GW in New Auctions, and FEOC Restrictions (2024 to 2026)

BESS Supply Chain Risks, FEOC Rules, and $35 B in Canceled Projects

Despite dramatic cost reductions making Battery Energy Storage Systems (BESS) economically compelling, escalating policy and trade risks create significant uncertainty that threatens project pipelines. The global average price for a turnkey BESS fell to approximately $117/k Wh in early 2026, a fraction of its cost just three years prior. However, this powerful economic tailwind is meeting a formidable headwind from geopolitical tensions, particularly in the U.S. market, where reliance on Chinese-made components exposes the industry to volatile trade policies.

- Between 2021 and 2024, the BESS market was primarily defined by rapid growth fueled by the U.S. Inflation Reduction Act (IRA), which introduced a 30% investment tax credit for standalone storage. This spurred massive investment and deployment plans.

- The landscape shifted sharply in 2025. The enactment of new legislation and the reversal of prior clean energy policies led to the abandonment of nearly $35 billion in private clean energy investments in the U.S., impacting BESS projects directly and injecting severe uncertainty into the market.

- A critical future risk is the enforcement of Foreign Entity of Concern (FEOC) restrictions, set to take effect in 2027. These rules will likely disqualify most current BESS projects, which rely on Chinese cells and components, from receiving the full IRA tax credits, forcing a costly and complex realignment of the entire supply chain.

- Operational risks also persist, highlighted by a fire at the 300 MW Moss Landing facility in January 2025. Such incidents intensify regulatory scrutiny and increase insurance costs, adding another layer of commercial risk for developers and investors.

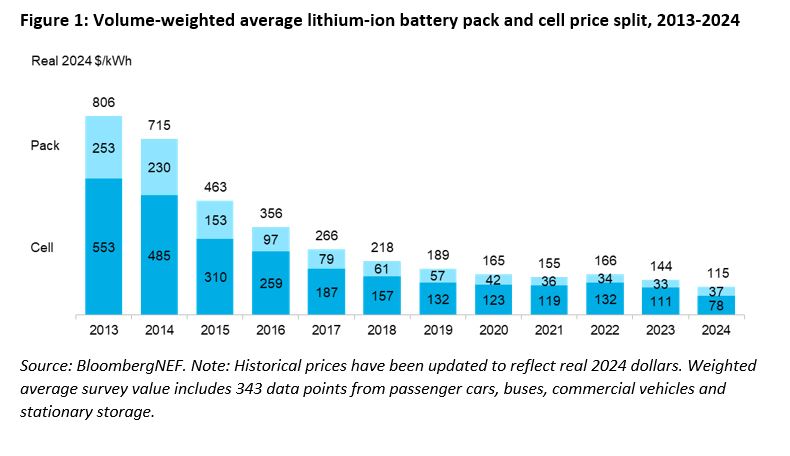

Li-Ion Battery Pack Prices Drop to $115/kWh

This chart illustrates the declining cost of the core component in BESS projects. It provides essential context for the section’s discussion on supply chain risks and FEOC rules, which directly threaten the cost and availability of these battery packs.

(Source: BloombergNEF)

BESS Project Cancellations and $35 B in US Clean Energy Reversals (2025 to 2026)

Recent policy shifts and trade uncertainty in 2025 directly triggered the cancellation or delay of substantial clean energy investments, demonstrating the market’s acute sensitivity to regulatory stability. While BESS costs have plummeted, the financial models underpinning these projects are fragile and cannot easily absorb sudden changes in tariff structures or the loss of expected tax incentives.

- The primary driver of market disruption was the reversal of key Biden-era policies in 2025, which Pexapark reported led to the halt of nearly $35 billion in planned private sector investments across the U.S. clean energy sector.

- Tariffs, including those enacted under IEEPA and antidumping/countervailing duties (AD/CVD), directly caused some BESS project deals to fail in 2025. This underscores how trade disputes can immediately derail projects that were otherwise economically viable.

- Reflecting this instability, the first quarter of 2025 saw a notable increase in manufacturing project cancellations, signaling eroding investor confidence in the previously robust domestic supply chain build-out.

NA BESS Market to Exceed $19B by 2030

The chart quantifies the significant value of the North American BESS market. This frames the discussion of ‘$35 B in US Clean Energy Reversals’ by showing the scale of the market opportunity being affected by project cancellations.

(Source: MarketsandMarkets)

Table: BESS Market Headwinds and Project Disruptions (2025 to 2026)

| Event / Risk Factor | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Clean Energy Investment Pullback | 2025 | A reversal of federal policies led to the abandonment of nearly $35 billion in private investments, disrupting project pipelines for BESS and other clean technologies. | Pexapark |

| BESS Project Fires | Jan 2025 | A fire at the 300 MW Moss Landing Energy Storage Facility in California triggered heightened regulatory scrutiny and increased focus on mitigating commercial risks related to battery safety. | Orrick |

| U.S. Tariffs on BESS Components | 2025 | Tariffs on Chinese components directly impacted BESS project economics, causing some deals to fall through and creating uncertainty for developers reliant on imported hardware. | Energy-Storage.News |

| Manufacturing Project Cancellations | Q 1 2025 | A rise in manufacturing project cancellations was reported, reflecting the impact of shifting trade policies and supply chain concerns on investor sentiment for domestic production. | ABHA Foundation |

BESS Offtake Agreements: Securing Revenue Amidst Market Volatility

In response to financing challenges and revenue volatility, developers are increasingly pursuing long-term offtake agreements to de-risk projects and ensure bankability. This trend is a direct reaction to the difficulties of financing merchant projects that rely on unpredictable revenue from ancillary services and energy arbitrage, a problem exacerbated by market fluctuations seen in 2025.

- The value of stable, contracted revenue was highlighted in 2025 as merchant BESS revenues declined in markets like ERCOT (Texas) compared to prior years. This made projects without offtake agreements significantly harder to finance.

- The market is adapting with more sophisticated contract structures. Offtake models such as virtual tolls, capacity sharing arrangements, and long-term optimization agreements are becoming more common and bankable.

- Recent deals validate this trend. In June 2025, the Hirohara BESS project in Japan secured financing based on a 20-year offtake agreement with Tokyo Gas. In February 2026, GEN-I and R.Power signed a long-term agreement for a major BESS project in Romania.

Wholesale Power and Gas Prices Show Volatility in 2025

This chart directly visualizes the ‘Market Volatility’ mentioned in the section heading, establishing the core problem that offtake agreements are designed to solve by securing predictable revenue streams for BESS projects.

(Source: LinkedIn)

Table: Recent BESS Commercial and Offtake Agreements

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Scornicesti BESS (Romania) | Feb 2026 | GEN-I and R.Power signed a long-term optimisation agreement for one of Romania’s largest utility-scale BESS projects, securing revenue streams. | GEN-I |

| Australian BESS Market | Sep 2025 | Market confidence improved significantly due to the increasing availability of long-term contracts, making it easier for developers to secure project financing from commercial banks. | Dentons |

| Red Sands BESS (South Africa) | Jun 2025 | Scatec signed project agreements for a major BESS project, marking a key milestone for energy storage deployment in the region. | Fractal Energy Storage Consultants |

| Hirohara BESS Project (Japan) | Jun 2025 | A 20-year offtake agreement with Tokyo Gas was critical in enabling the project to secure financing, demonstrating the importance of long-term revenue certainty. | Infrastructure Investor |

| UK BESS Project | Apr 2025 | Revenues for a project backed by AXA IM Alts were secured through a 10-year offtake agreement and two long-term Capacity Market contracts. | AXA IM Alts |

US vs. Global Markets: BESS Deployment and Policy Divergence

While the United States remains a primary growth market for BESS, its vulnerability to policy reversals and trade disputes contrasts with expanding activity in Europe and the Asia-Pacific region. The dramatic fall in BESS equipment prices is a global phenomenon, but its translation into deployed projects is heavily mediated by local policy, market structure, and supply chain access.

- The U.S. market, projected to exceed 170 GW of BESS capacity by 2030, saw strong growth between 2021 and 2024 under the IRA. However, the policy instability that emerged in 2025 created significant headwinds not felt as acutely in other regions.

- Europe and the UK have enacted their own landmark legislation to support energy storage. This provides a more stable, albeit different, incentive structure that is driving investment in grid stability and renewable integration projects.

- The Asia-Pacific region is a center of both demand and supply. China’s manufacturing dominance, led by firms like CATL and BYD, underpins the global cost decline. Meanwhile, countries like Australia and Japan are developing sophisticated financing and offtake markets to accelerate deployment.

European BESS Market Forecasts Strong Growth

To facilitate the ‘US vs. Global Markets’ comparison, this chart provides a concrete example of a major international market’s growth trajectory, allowing for a discussion on policy and deployment divergence between regions.

(Source: MarketsandMarkets)

TRL 9 BESS Maturity vs. 300 MW Moss Landing Fire and Operational Risks

Although lithium-ion BESS has achieved full commercial maturity (TRL 9), significant operational risks, including fire safety and battery degradation, persist as primary concerns for investors, insurers, and regulators. The technology is proven and bankable, but high-profile failures can have an outsized impact on project economics and public perception, tempering the enthusiasm from falling equipment costs.

- From 2021 to 2024, the industry focused on scaling production and driving down costs, with a notable pivot to Lithium Iron Phosphate (LFP) chemistry to improve safety and reduce reliance on cobalt. This pivot was a key enabler of the sub-$150/k Wh system prices seen today.

- The January 2025 fire at the 300 MW Moss Landing facility served as a stark reminder of residual technological risk. This event prompted decisive regulatory shifts in California and increased insurer scrutiny on safety protocols and system design globally.

- Battery degradation remains a critical commercial challenge. Structuring long-term performance guarantees and accurately modeling capacity loss over a project’s life are complex issues that are central to negotiating bankable offtake and warranty agreements.

BESS Failure Rate Drops as Deployment Soars

This chart perfectly illustrates the section’s theme by showing a declining failure rate, a key indicator of technological maturity (TRL 9). It visually contrasts this progress with the ongoing reality of operational risks as deployment increases.

(Source: EPRI Storage Wiki)

BESS SWOT Analysis, Cost Declines, and Geopolitical Supply Risks

The BESS market’s primary strength is its rapidly falling cost curve, which has made it competitive with conventional power assets for many grid services. However, this is directly challenged by the market’s greatest weakness: a heavy reliance on a geographically concentrated supply chain that is vulnerable to geopolitical tensions and trade disputes.

- The market’s core opportunity is to address new sources of demand, particularly from energy-intensive AI data centers, while its greatest threat remains policy instability that can erase project returns overnight.

Battery Costs Plummeted as Installations Surged

The chart’s depiction of plummeting costs represents a primary ‘Strength’ and ‘Opportunity’ within a BESS SWOT analysis. The corresponding surge in installations provides a broad market context for the analysis.

(Source: Energy-Storage.News)

Table: SWOT Analysis for BESS Market Dynamics

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Falling costs and improving technology (LFP adoption). The IRA created powerful demand-pull in the U.S. | Turnkey system prices fell below $150/k Wh, with pack prices reaching $70/k Wh. BESS achieved economic parity with gas peakers for many applications. | The cost-down thesis was validated, proving BESS as a mature (TRL 9), cost-competitive technology. |

| Weaknesses | High concentration of battery manufacturing in China. Project financing was difficult without subsidies. | Revenue volatility in merchant markets (e.g., ERCOT) became apparent. Safety incidents like the Moss Landing fire highlighted operational risks. | The fragility of merchant revenue models was confirmed, increasing the importance of offtake agreements. Supply chain concentration became an acute geopolitical risk. |

| Opportunities | Co-location with renewables to provide grid services. Growing EV market created manufacturing scale. | AI-driven data centers emerged as a massive new source of demand. V 2 G technology showed potential to add significant distributed capacity. | The Total Addressable Market expanded beyond renewables integration to include critical infrastructure support for the digital economy. |

| Threats | Potential for raw material price spikes (lithium, cobalt). Grid interconnection queues were a known bottleneck. | Policy reversal in the U.S. led to $35 billion in canceled investments. FEOC rules and tariffs created direct threats to the dominant supply chain. | Political risk was validated as a primary threat capable of overriding strong economic fundamentals. Geopolitical tensions moved from a theoretical risk to a direct cause of project failure. |

BESS 2026 Outlook: FEOC Rules and the Race for Supply Chain Diversification

The critical path for BESS growth in 2026 and beyond hinges on the industry’s ability to navigate FEOC restrictions by accelerating the onshoring of manufacturing and securing non-Chinese supply chains. The progress of this industrial shift will be the leading indicator of the market’s long-term health and its ability to absorb the powerful tailwind of falling costs from manufacturers like Sungrow.

- If this happens: The final FEOC rules are strictly enforced on schedule in 2027, making most currently planned BESS projects ineligible for the full IRA tax credits.

- Watch this: The pace of new domestic battery factory announcements and commissioning in North America and Europe. The speed of this localization, driven by incentives like the §45 X manufacturing credit, is the primary countermeasure to FEOC risk.

- These could be happening: A price premium emerges for FEOC-compliant systems, developers race to stockpile non-compliant inventory before the deadline, and investment accelerates into alternative technologies like sodium-ion batteries and long-duration storage from companies like Form Energy.

Global BESS Market Poised for Major Growth

This forward-looking forecast aligns with the ‘2026 Outlook’ theme. The projection of major global growth highlights the high stakes and provides the motivation for the ‘Race for Supply Chain Diversification’ mentioned in the heading.

(Source: ESS News)

The questions your competitors are already asking

This report covers one angle of the BESS market’s collision between falling costs and rising policy risk. The questions that matter most depend on your work.

- What is the outlook for U.S. BESS deployment through 2027, considering low equipment costs but high policy and trade risk?

- Which BESS suppliers are gaining or losing ground as the industry realigns its supply chain away from China ahead of the 2027 FEOC restrictions?

- What is the cost breakdown of a $117/kWh utility-scale BESS, and where do the biggest risks to that price point lie?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.