BESS Supply Chain Under Pressure: 150 GWh of Chinese Exports, a 30% CATL Surge, and Western Gigafactory Risk (2021 to 2026)

BESS Adoption Risks: Chinese Overcapacity, Price Wars, and Western Project Cancellations

The competitive landscape for battery manufacturing has inverted, shifting from a period of ambitious Western expansion between 2021 and 2024 to one of strategic retreat and consolidation from 2025 onward. This change is a direct result of China’s state-backed industrial strategy, which has created massive domestic overcapacity and is now flooding global markets with low-cost batteries, rendering many planned Western gigafactories economically unviable.

- Between 2021 and 2024, Western automakers announced a series of high-profile joint ventures to build a domestic supply chain, including Ford’s partnership with CATL and GM’s alliance with Samsung SDI. However, starting in 2025, this momentum reversed, with over $32 billion in U.S. clean energy projects, including battery factories like KORE Power’s Arizona plant, being shelved due to deteriorating market conditions and policy uncertainty.

- China’s battery production vastly outpaced its domestic needs, creating a structural imperative to export. In early 2026, China produced 309.7 GWh of batteries but installed only 68.3 GWh (22%) in local vehicles, leaving a staggering surplus. This follows a year in which its total production reached 1, 755.6 GWh in 2025.

- The primary weapon is cost. In 2025, battery pack prices in China averaged $108/k Wh, which was 30-35% lower than in the United States and Europe. This price chasm, driven by China’s dominant and highly integrated Lithium Iron Phosphate (LFP) supply chain, makes it nearly impossible for Western firms to compete on mature technologies without significant protectionist measures.

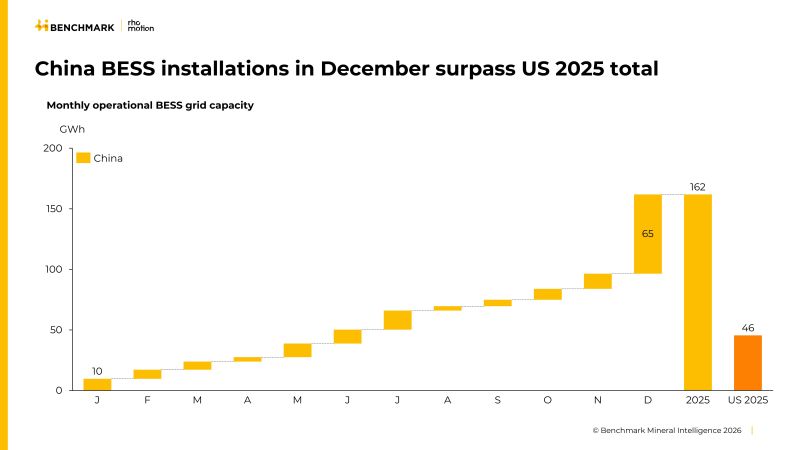

China’s 2025 BESS Installations Dwarf US Market

The section discusses risks from Chinese overcapacity in the BESS market. This chart directly visualizes the scale of China’s market compared to the U.S., illustrating the competitive dominance that creates these risks for Western adoption.

(Source: LinkedIn)

$32 B in Cancellations: U.S. Gigafactory Rollbacks Amid Policy and Market Headwinds

The investment climate for Western battery manufacturing deteriorated sharply in 2025, as the combination of overwhelming Chinese price competition and the rollback of key U.S. government incentives triggered a wave of high-profile project cancellations and delays. The initial optimism fueled by the Inflation Reduction Act (IRA) gave way to financial reality, undermining the economic case for building a domestic supply chain to compete with established, low-cost Chinese imports.

- A significant policy shift in 2025 saw the curtailment and repeal of critical IRA provisions, including production tax credits and consumer incentives. This directly contributed to the cancellation of more battery manufacturing projects in Q 1 2025 than in the previous two years combined.

- By the end of 2025, over $32 billion in U.S. clean energy projects had been canceled or significantly downsized. This figure includes major battery manufacturing facilities, such as the planned KORE Power factory in Arizona and projects by Borg Warner.

- The trend extends beyond the U.S. In February 2026, Honda announced a two-year pause on a $15.4 billion set of projects in Ontario, Canada, which included a new battery plant. Similarly, in Europe, a slowdown in EV sales has forced multiple companies to cancel or postpone planned battery investments.

Lithium-Ion Battery Prices Rise After Long Decline

The section discusses gigafactory cancellations due to ‘Market Headwinds.’ A rise in battery prices is a significant market headwind that increases project costs and risks, providing a direct rationale for the rollbacks.

(Source: Benchmark Source)

Table: Major Western Battery and Clean Energy Project Cancellations (2025-2026)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Honda Ontario Projects | Feb 2026 | A $15.4 billion investment package, including a new EV and battery plant, was put on a two-year pause, signaling a broader reassessment of North American EV manufacturing plans. | Green Transition |

| Various U.S. Clean Energy Projects | Dec 2025 | More than $32 billion in U.S. projects were canceled or downsized throughout 2025, directly linked to policy reversals and changing market dynamics that favored imports. | Fast Company |

| Kore Power & Borg Warner | May 2025 | $14 billion in projects were canceled in the first half of 2025, including Kore Power’s major battery factory in Arizona, citing an unstable policy environment. | BNN Bloomberg |

| Various U.S. Projects | Apr 2025 | Nearly $8 billion in projects were canceled in Q 1 2025 alone, as companies reacted to the rollback of IRA incentives, halting plans for domestic manufacturing. | Utility Dive |

Western OEM Partnerships with CATL, LG, and Samsung for LFP and NMC Supply (2021 to 2026)

Faced with an insurmountable cost and scale gap, Western automakers have pivoted their battery strategies away from full vertical integration and toward forming joint ventures and licensing agreements with dominant Asian manufacturers. This pragmatic shift acknowledges that competing directly with Chinese producers on mature LFP technology is currently unfeasible, forcing automakers to trade long-term industrial independence for near-term supply security and cost-competitiveness.

- The most prominent example is Ford’s decision to build a battery plant in Michigan using technology licensed directly from CATL. This move serves as a clear admission that developing a competitive LFP technology stack in-house would be too slow and costly.

- Other major automakers have followed a similar path of reliance on Asian expertise. General Motors has entered into joint ventures with Samsung SDI, while Stellantis has partnered with LG Energy Solution for its North American battery production.

- These partnerships, while securing the necessary volume of batteries to meet EV production targets, also guarantee a significant and stable export market for Chinese and South Korean technology leaders, further cementing their central role in the global supply chain.

EV Battery Market to Surpass $200B by 2034

This chart shows the immense projected growth of the EV battery market. This provides the strategic context for why ‘Western OEMs’ are forming critical ‘Partnerships’ to secure supply, as discussed in the section.

(Source: Market.us)

Table: Key Western OEM Battery Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Ford and CATL | 2023–2026 | Ford is constructing a plant in Michigan that will operate using licensed LFP battery technology from CATL. This strategy allows Ford to access low-cost, mature battery tech while attempting to qualify for domestic production incentives. | Lexology |

| General Motors and Samsung SDI | 2023–2026 | A $3.5 billion joint venture to build a battery cell manufacturing plant in Indiana. The facility will produce high-nickel prismatic and cylindrical cells, aiming for a capacity of over 30 GWh. | Industrial Info Resources |

| Stellantis and LG Energy Solution | 2022–2025 | The Next Star Energy JV began production in Ontario, Canada, in October 2025. It represents a $3.7 billion investment to supply batteries for a significant portion of Stellantis’s North American EV production. | Yahoo Finance |

China vs. The West: A Geographic Split in Battery Production and Cost Structure

The global battery manufacturing map is now starkly divided into two spheres: China, the undisputed high-volume, low-cost production hub, and the West (North America and Europe), a high-cost region struggling to establish a viable industrial base. China’s control extends across the entire value chain, from mineral processing to cell and pack manufacturing, creating a structural advantage that geographic diversification efforts in the West have so far been unable to overcome. The expansion of Chinese firms like Sungrow Energy Storage and LONGi Energy Storage into Western markets further highlights this trend.

- China’s market dominance is nearly absolute, commanding 75-90% of the midstream cathode and anode material manufacturing. In 2025, Chinese firms controlled 68.9% of the global EV battery market, solidifying the nation’s role as the world’s battery factory.

- The cost disparity is a primary barrier for Western competitiveness. In 2025, battery packs made in China were 30% cheaper than those from the U.S. and 35% cheaper than those from Europe. This gap makes direct competition on price exceedingly difficult for Western manufacturers.

- Efforts to build a self-sufficient Western supply chain are faltering. In Europe, over 30% of planned Li-ion battery projects are hampered by financial, operational, and regulatory issues. In the U.S., a combination of policy uncertainty and market pressures has led to widespread project cancellations, even as developers like Spearmint Energy advance large project queues.

- Other regions are also grappling with this dynamic. For example, India Energy Storage initiatives are targeting significant capacity growth but remain heavily dependent on the Chinese supply chain for key components and materials.

Technology Maturity: LFP Dominance, Chinese Scale, and the Western Pivot to Next-Gen

China’s export strategy is built on its complete mastery of commercially mature (TRL 9) Lithium Iron Phosphate (LFP) technology, which has become the global standard for mass-market EVs due to its low cost and safety. This has forced Western firms into a difficult strategic position: either license this commoditized technology from Chinese leaders or attempt to leapfrog it by accelerating the development of less mature, next-generation chemistries where China’s scale advantage is not yet fully established.

- Between 2021 and 2024, LFP technology, long popular in China, began to gain traction globally as automakers prioritized cost reduction. By 2025, LFP accounted for over 80% of Chinese automotive battery installations and had become a mainstream choice for standard-range EVs worldwide.

- China’s technological maturity is reinforced by its near-total control of the midstream supply chain, where it commands approximately 85–90% of global manufacturing capacity for both cathode and anode active materials. This integration makes its LFP cost structure nearly impossible to replicate elsewhere.

- In response, Western R&D and investment are increasingly focused on next-generation technologies. This includes solid-state batteries (SSBs), which promise higher energy density, and sodium-ion batteries (SIBs), a lower-cost alternative that avoids lithium dependence. Companies like Form Energy are also developing alternative long-duration storage chemistries like iron-air.

- This pivot represents a significant opportunity but also carries risk. SSBs and SIBs are at a lower Technology Readiness Level (TRL) and face significant scaling challenges, leaving a multi-year window where Chinese LFP batteries will continue to dominate the market.

Sodium-Ion Battery Pipeline to Reach 150 GWh

This chart quantifies the development of a specific ‘Next-Gen’ technology (Sodium-Ion). It directly supports the section’s theme of a ‘Western Pivot to Next-Gen’ by showing a tangible pipeline for alternatives to LFP.

(Source: Benchmark Source)

SWOT Analysis: Western Battery Manufacturing Amid Chinese Export Pressure

A strategic analysis of the Western battery industry reveals a core tension: while it possesses strong innovation capabilities and initial policy support, it is exposed to overwhelming threats from China’s scale, cost structure, and integrated supply chain. The reversal of key policy incentives in 2025 has significantly weakened its position, exacerbating internal weaknesses like high costs and financing difficulties.

Table: SWOT Analysis for Western Battery Manufacturing (2021-2025)

| SWOT Category | 2021 – 2024 | 2025 – Present | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong R&D in next-gen tech (SSB, SIB). Access to capital markets. Established automotive OEMs driving demand. | Continued innovation in next-gen chemistries. Growing expertise in battery recycling and management software. | The West’s core strength remains in innovation and high-value software, not in competing with China on mature commodity hardware. |

| Weaknesses | Higher labor and energy costs. Fragmented supply chain with dependence on Chinese-processed minerals. Slower to scale manufacturing. | Cost gap with China widens to 30-35%. Project financing becomes difficult amid policy uncertainty and high interest rates. Lack of domestic LFP expertise. | The fundamental weakness—a higher cost structure—was validated. Without subsidies, Western production is not cost-competitive with Chinese imports. |

| Opportunities | IRA and other policy incentives to build a domestic supply chain. Leapfrog LFP with next-gen tech. Form strategic alliances with non-Chinese mineral suppliers. | Lobby for significant protectionist tariffs. Pivot to high-margin niche applications. Develop circular economy through battery recycling to secure materials. | The primary opportunity has shifted from direct competition to a combination of protectionism, technology leapfrogging, and specialization in adjacent high-value sectors. |

| Threats | Growing Chinese production capacity. Dependence on Chinese supply chain for critical materials and components. Potential for price dumping. | Massive Chinese overcapacity ignites fierce price war. Rollback of IRA incentives removes key support. Project cancellations hollow out nascent industry. China imposes export controls on advanced tech. | The threat of Chinese overcapacity, once theoretical, became a harsh reality in 2025, fundamentally altering the economics of Western battery manufacturing. |

Scenario Modeling: Tariffs, JVs, and the 2026 Outlook for Western Battery Makers

Looking ahead to 2026, the viability of the Western battery manufacturing industry hinges on a more aggressive and sustained policy response to counter China’s overwhelming competitive advantages. Without stronger protectionist measures, the default path points toward increased reliance on Chinese technology through direct imports and licensing agreements, effectively ceding the mass-market battery segment to foreign-controlled supply chains.

- If this happens: The U.S. and EU expand tariffs beyond finished EVs to target Chinese battery cells, packs, and key components with duties significant enough to close the 30-35% price gap.

- Watch this: The sourcing decisions of major Western automakers like GM, Ford, and VW will be the most critical bellwether. A collective pivot toward offtake agreements with nascent Western suppliers, even at a premium, would signal a strategic commitment to supply chain resilience over short-term cost savings.

- These could be happening: A wave of consolidation or bankruptcies among Western battery startups that fail to secure offtake agreements or cannot compete on price. Simultaneously, venture capital may accelerate funding for next-generation technologies (SSB, SIB) that offer a path to circumvent China’s dominance in LFP, creating a bifurcated market focused on long-term innovation alongside short-term survival.

China to Reduce Battery Export Rebates

This chart introduces a specific policy variable—a change in export rebates—that is a critical input for the ‘Scenario Modeling’ of tariffs and outlooks for Western battery makers mentioned in the section heading.

The questions your competitors are already asking

This report covers one angle of the strategic risk to Western gigafactories from Chinese battery overcapacity. The questions that matter most depend on your work.

- Which battery manufacturers are gaining or losing ground in the Western market as Chinese exports surge?

- Are high-profile Western battery JVs like Ford-CATL and GM-Samsung SDI on track, or are they at risk of joining the $32B in shelved projects?

- What is the cost breakdown of a Chinese battery pack, and how does it achieve a 30-35% price advantage over US and European packs?

- What is the realistic outlook for Western gigafactory commissioning through 2026 amid Chinese price pressure?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.