BESS Supply Chain Risks, GM’s LMR & Sodium-Ion Strategy, 370 GWh Chinese Capacity, and $20 B Investment (2021 to 2026)

BESS Supply Chain Risk, GM LMR and Sodium-Ion Adoption

The extreme concentration of the lithium-ion battery supply chain within China created a critical geopolitical risk, forcing Western automakers like General Motors (GM) to accelerate development of alternative chemistries like Sodium-Ion (Na-ion) and Lithium Manganese-Rich (LMR) to secure future production.

- Between 2021 and 2024, China solidified its market position, producing three-quarters of all lithium-ion batteries and controlling 70% of production capacity for cathodes and 85% for anodes. During this period, GM‘s primary battery strategy was to build a domestic, lithium-ion supply chain centered on its Ultium platform, with a target of 160 GWh of cell capacity.

- By 2025-2026, this supply chain risk materialized into strategic action. GM confirmed it was developing proprietary LMR and Na-ion prototypes as a direct response to projections that China would control over 95% of the global sodium-ion manufacturing capacity by 2030, effectively creating a new dependency.

- This strategic pivot is now two-pronged: GM is targeting its Na-ion prototypes for grid-scale storage, where low cost and cycle life are paramount, while positioning its LMR technology as a direct, US-built competitor to the Chinese-dominated Lithium Iron Phosphate (LFP) batteries used in affordable EVs.

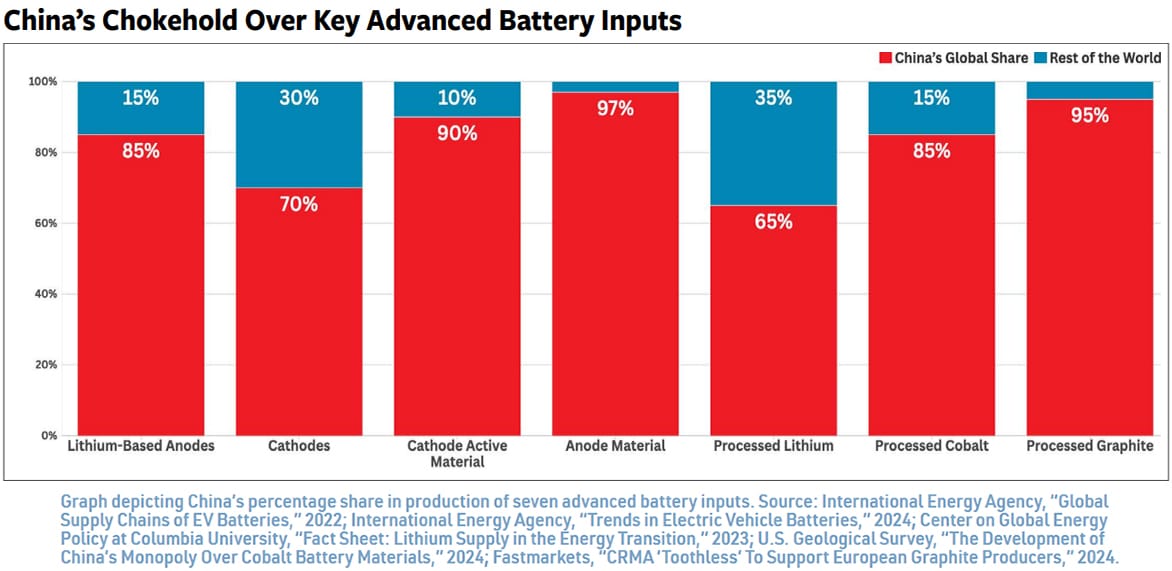

China Dominates Key Advanced Battery Inputs

The section discusses supply chain risk as a motivation for adopting sodium-ion. This chart directly illustrates that risk by showing China’s dominance over the processing of key battery materials, highlighting the vulnerability that alternative chemistries aim to mitigate.

(Source: Battery Technology)

$20 B in Global Investment, Sodium-Ion Capacity Expansion

Over $20 billion in announced global investment has poured into the sodium-ion sector, yet this capital is overwhelmingly concentrated in China, creating a formidable first-mover advantage and a high barrier to entry for Western firms.

- Before 2025, significant capital injections were signaled by deals like Reliance Industries‘ acquisition of UK-based technology leader Faradion for £100 million in late 2021, highlighting industrial interest in securing sodium-ion intellectual property.

- By 2026, the scale of investment had resulted in a tracked global production capacity pipeline of 370 GWh for sodium-ion cells, with nearly all of it located in China, demonstrating an established and rapidly scaling manufacturing ecosystem.

- This contrasts sharply with the US market, where battery project announcements saw $11 billion in cancellations during 2025, reflecting market volatility and the difficulty Western companies face in securing long-term capital for new battery chemistries amid shifting government policies.

Sodium-Ion Battery Market Projects 18% CAGR

This section covers global investment and capacity expansion in sodium-ion technology. A chart projecting a strong Compound Annual Growth Rate (CAGR) for the sodium-ion market directly supports the thesis of growing investment and planned expansion.

(Source: MarketsandMarkets)

Table: Strategic Investments in Battery Technology

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Global Sodium-Ion Sector | 2025 – 2026 | Over $20 billion in announced global investments and a tracked production capacity of 370 GWh have been established, primarily driven by Chinese firms. This investment cements China’s dominance before Western firms can establish a foothold. | Battery-Tech.net |

| US Battery Projects | 2025 | Announcements for new US battery projects saw $11 billion in cancellations. This highlights the volatile investment climate and policy uncertainty facing companies like GM as they attempt to build out domestic supply chains. | CSIS |

| Reliance New Energy Solar / Faradion | Dec 2021 | Reliance acquired UK-based sodium-ion IP leader Faradion for £100 million. This early strategic move by an industrial major validated the commercial potential of sodium-ion technology. | Faradion |

GM 0 Sodium-Ion Partnerships vs Chinese JVs (2021 to 2026)

While Chinese firms like BYD and CATL aggressively formed joint ventures to build a dominant sodium-ion market, GM‘s partnerships through 2026 remained focused on securing its existing lithium-ion supply chain, highlighting its late-mover status in sodium-ion collaborations.

- In November 2023, BYD announced a major joint venture with Huaihai Holding Group with the explicit goal of becoming a world leader in the production of sodium-ion batteries, signaling a strategic push to build an ecosystem around the technology.

- In contrast, GM’s key collaborative agreement during this period was a June 2023 supply deal with Element 25. The partnership was designed to secure manganese sulfate for its lithium-ion Ultium battery cathodes, not for developing alternative chemistries.

- This divergence demonstrates two different strategies. Chinese players used partnerships to rapidly build and control a new manufacturing ecosystem, whereas GM‘s efforts in alternative chemistries appear to be primarily internal R&D, lacking the external alliances needed for rapid scaling.

Table: Comparative Battery Technology Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| BYD / Huaihai Holding Group | Nov 2023 | Formation of a joint venture to establish a world-leading production base for sodium-ion batteries. This strategic alliance is designed to accelerate mass commercialization and secure market leadership in China. | Yahoo News |

| General Motors / Element 25 | Jun 2023 | GM agreed to help finance a new manganese sulfate facility in Louisiana to secure supply for its lithium-ion Ultium batteries. The partnership shores up its existing supply chain rather than building a new one for alternative chemistries. | General Motors |

China vs US, GM Sodium-Ion Geographic Focus

China established itself as the undisputed global hub for sodium-ion manufacturing and capacity between 2021 and 2026, while the United States’ efforts, including GM‘s development, are positioned as a strategic, domestic countermeasure rather than a play for global market share.

- Between 2021 and 2024, China’s dominance in the lithium-ion supply chain was solidified, with the country controlling critical processing steps, including 95% of graphite and 85% of processed cobalt.

- From 2025 to 2026, this pattern was replicated in the sodium-ion sector. Projections showed China would command a 95.9% share of the 122.9 GWh of global sodium-ion battery capacity by the end of 2025.

- The US response remains geographically defensive. GM’s R&D is concentrated in its US labs, and its partnerships aim to build a US-based supply chain, such as the manganese facility in Louisiana, to insulate its North American production from geopolitical shocks.

- The US holds a significant long-term geographical advantage with its large domestic sodium reserves, which account for 45% of the top five global reserves, but this is only valuable if a domestic manufacturing base can be successfully established.

China’s Dominance in Battery Manufacturing to Continue

The section discusses GM’s geographic focus, comparing the US and China. This chart explains the strategic importance of China by visualizing its continued dominance in battery manufacturing capacity, a critical factor influencing a global company’s strategic focus.

(Source: Elements by Visual Capitalist)

Sodium-Ion Commercial Scale, GM Prototypes vs CATL 175 Wh/kg

Sodium-ion technology rapidly matured from lab-scale validation to commercial mass production between 2023 and 2026, but this progress was led entirely by Chinese firms, leaving Western counterparts like GM in a state of developmental catch-up.

- From 2021-2023, sodium-ion technology was largely at a Technology Readiness Level (TRL) of 5-6. During this time, CATL announced its first-generation cells with an energy density of 160 Wh/kg and laid out a roadmap for mass production.

- By 2026, Chinese manufacturers had achieved full commercial scale. CATL began mass production of sodium-ion batteries for EVs and energy storage with cell energy densities reaching 175 Wh/kg, making them competitive with LFP chemistry. Simultaneously, cell costs fell by 24% year-over-year to approximately $57/k Wh.

- In stark contrast, GM‘s sodium-ion efforts in 2026 remain in the prototype stage. Its initial application is targeted at grid storage, indicating the company is several years behind its Chinese competitors in bringing a commercially viable, automotive-grade product to market.

Sodium-Ion vs. Lithium-Ion Battery Characteristics Compared

The section compares specific performance metrics (Wh/kg) of sodium-ion prototypes. This chart provides a foundational comparison of the general characteristics of sodium-ion and lithium-ion, giving the reader context for the detailed technical discussion.

(Source: ScienceDirect.com)

SWOT Analysis, GM Sodium-Ion Strategy Execution Risks

GM‘s strategy to develop alternative battery chemistries is a necessary defensive move to mitigate supply chain risk, but a SWOT analysis reveals significant weaknesses in execution speed and scale when compared to the entrenched strengths and rapid progress of its Chinese competitors.

- Strengths like access to abundant raw materials are offset by profound Weaknesses, including a late-mover status and a lack of manufacturing scale.

- While the Opportunity to create a resilient, low-cost domestic supply chain is significant, it is overshadowed by the Threat of China’s overwhelming market dominance and cost leadership.

Analysis of Sodium-Ion Battery Market Factors

This section presents a SWOT analysis for GM’s strategy. A chart analyzing the broader sodium-ion market factors provides the external context for this analysis, corresponding directly to the ‘Opportunities’ and ‘Threats’ facing GM.

(Source: Coherent Market Insights)

Table: SWOT Analysis for GM’s Alternative Battery Strategy

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Focus on a proven Li-ion platform (Ultium) with a clear domestic manufacturing roadmap (160 GWh target). | Strategy leverages abundant and low-cost raw materials (sodium, manganese), directly addressing the core cost and geopolitical risks of lithium and cobalt. The US also holds large sodium reserves. | The strategic rationale for non-lithium chemistries was validated. The focus shifted from optimizing Li-ion to de-risking the entire supply chain. |

| Weaknesses | No public commercial activity or partnerships in sodium-ion technology. Strategy was fully dependent on the Li-ion supply chain. | GM is in the prototype stage for Na-ion, while Chinese firms like CATL are in mass production. GM lacks the partnerships and scale needed to compete on cost or volume in the near term. | The technology gap widened significantly. What was a research topic became a mass-market reality for Chinese firms, leaving GM several years behind. |

| Opportunities | IRA incentives (e.g., 45 X tax credit) created a favorable environment for domesticating the battery supply chain. | Develop and scale LMR and Na-ion to create a truly resilient, non-Chinese supply chain for affordable EVs and grid storage, insulating production from geopolitical shocks. | The opportunity became more urgent and specific. It is no longer just about onshoring Li-ion but about leapfrogging to alternative chemistries to escape Chinese control. |

| Threats | Growing awareness of China’s dominance in Li-ion mineral processing (70-85% control of key components). | China’s first-mover advantage and scale in sodium-ion (370 GWh capacity, $20 B+ investment) creates a formidable barrier. Chinese Na-ion cells at $57/k Wh set a difficult cost target to match. | The threat fully materialized. China not only controls the current Li-ion supply chain but has also moved to dominate the most viable alternative, creating a new and even more entrenched dependency. |

GM 2028 LMR Commercialization and Na-ion Pilots

For GM to successfully de-risk its supply chain, it must translate its LMR and sodium-ion R&D into commercial products by 2028; failure to achieve this will cede the entire low-cost battery segment to Chinese manufacturers indefinitely.

- If this happens: GM announces a firm timeline and capital investment for a giga-scale LMR battery plant in the US before 2027. This would be the strongest signal that it intends to compete directly with Chinese LFP batteries in the mass market.

- Watch this: The deployment of GM‘s first grid-scale energy storage projects using its proprietary sodium-ion technology. The performance and cost data from these pilots will be the first real-world validation of its technology against established Chinese products.

- These could be happening: GM forms a joint venture with a non-Chinese chemical or mining company to create a vertically integrated sodium-ion supply chain. Such a move would signal a serious acceleration of its strategy, mimicking the ecosystem-building approach of its rivals like BYD.

Sodium-Ion vs. LFP Battery Cost Breakdown

The section focuses on the commercialization and piloting of new battery chemistries. This chart is highly relevant as it breaks down the cost of sodium-ion versus LFP, the incumbent low-cost battery. This cost comparison is central to evaluating the commercial viability of GM’s pilots.

(Source: ScienceDirect.com)

The questions your competitors are already asking

This report covers one angle of GM’s strategic pivot to sodium-ion batteries in response to China’s supply chain dominance. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the race to commercialize sodium-ion batteries?

- What is the outlook for sodium-ion deployment in US grid-scale storage by 2030?

- How does GM’s LMR technology compare to Chinese-made LFP for the affordable EV market?

- GM’s activities in alternative chemistries. Is its sodium-ion initiative progressing from prototype to deployment?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.