Microsoft Nuclear 2026, 6 GW Shortfall, X-energy Deal

PJM Data Center Power Crisis, 24 GW Shortfall, $329/MW-day Prices, and Emergency Curtailment Orders (2021 to 2026)

The PJM Interconnection, the largest U.S. grid operator, is facing a systemic power crisis driven by explosive data center demand, creating a potential 24 GW capacity shortfall by 2030 and forcing regulators to authorize emergency curtailment orders. This supply-demand imbalance has caused capacity prices to skyrocket and is catalyzing a fundamental shift in grid management, forcing data centers to abandon their role as passive consumers and invest in on-site generation and grid-interactive capabilities to ensure survival. The era of reliable, cheap grid power for data centers in the PJM region has ended, replaced by a new market reality where energy resilience is a primary determinant of operational viability.

Data Center Expansion Risks, PJM Faces 24 GW Shortfall by 2030

The risk profile for data center operations in the PJM territory has shifted from a manageable concern to an acute crisis, as grid capacity fails to keep pace with exponential load growth. Before 2025, the challenge was primarily theoretical and addressed through standard demand response programs; now, it has materialized as recurring emergency orders and market-altering policy proposals.

- Between 2022 and 2024, PJM’s projected 10-year annual summer peak load growth forecast quadrupled from 0.4% to 1.7%, a revision driven almost entirely by new data center developments. While PJM’s Manual 13 for emergency operations existed, its most severe measures were considered a distant last resort.

- Starting in 2025, the crisis became tangible. PJM’s 2027 capacity auction revealed a historic 6 GW shortfall, and price spikes during a June 2025 heatwave saw Locational Marginal Prices (LMPs) exceed $2, 100/MWh.

- In response, the Department of Energy (DOE) invoked Section 202(c) of the Federal Power Act, issuing emergency orders authorizing PJM to curtail power to large loads. An order on May 19, 2026, was a direct repeat of a similar order that expired in January 2026, establishing curtailment as a recurring, seasonal grid management tool.

- To address the root cause, PJM proposed radical market reforms in January 2026, including a “Bring-Your-Own-Generation” (BYOG) model. This policy would require new data centers to finance their own dedicated power sources, fundamentally shifting infrastructure risk from the public to the private sector.

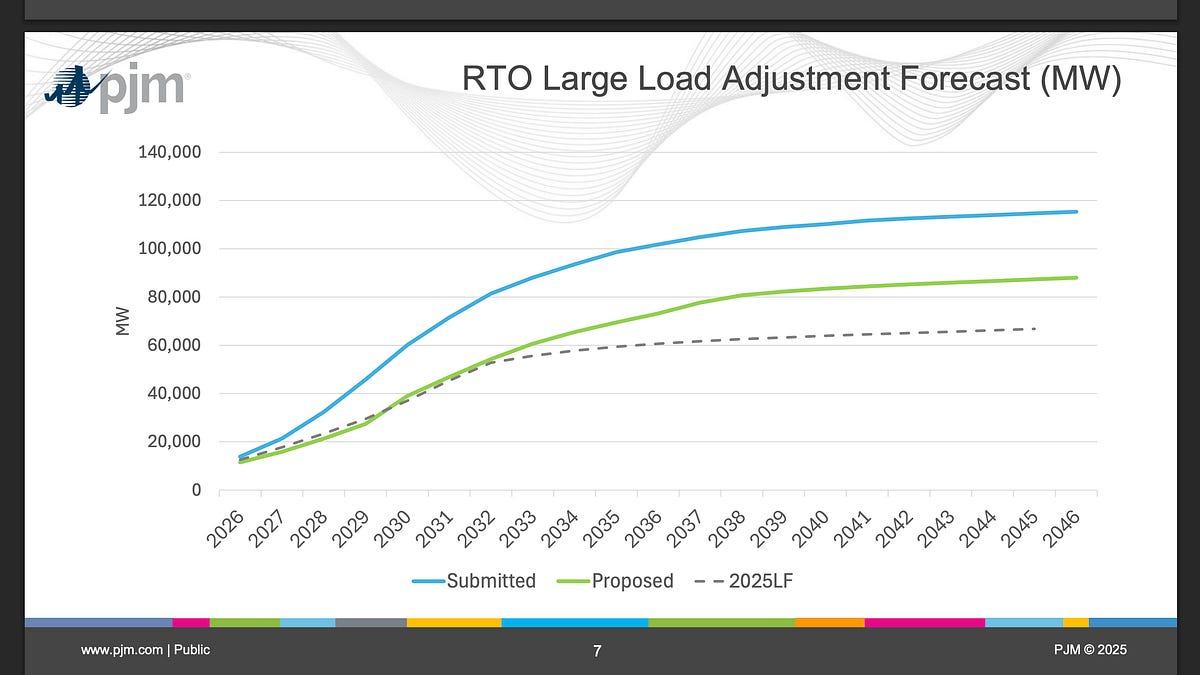

PJM Forecasts Massive Surge in Power Demand

This chart’s forecast of a massive demand surge directly explains the ’24 GW Shortfall’ projected for the PJM grid, which is the central risk outlined in the section heading.

(Source: Miner Weekly)

$173 B in PJM Capacity Costs, Dominion and Com Ed Face Biggest Investments

The grid instability is creating massive financial liabilities for utilities and their customers, with an estimated $173.5 billion in capacity costs projected through 2033 to manage the data center-driven load. This enormous capital expenditure requirement is a primary driver behind the extreme price volatility in PJM’s capacity markets and increases the financial incentive for utilities to support emergency curtailment measures.

- The financial burden is not evenly distributed, concentrating in utility zones with the highest density of data center development. The Dominion Energy territory in Northern Virginia faces the largest share of these costs, estimated at $27 billion.

- Other major utilities in the PJM footprint are also facing significant costs, including Com Ed ($21.4 billion) and AEP ($15 billion), indicating that the data center load problem is becoming a region-wide issue.

- These projected costs are reflected in PJM’s capacity auctions. The 2026/2027 auction cleared at a record $329.17/MW-day in constrained zones, a more than tenfold increase from the ~$30/MW-day prices seen in the 2023/24 delivery year.

- This cost pressure is forcing data centers to pursue on-site power solutions. The global data center generator market is now projected to reach $13.8 billion by 2030, while the market for battery energy storage is forecast to hit $3.5 billion by 2033, representing a direct transfer of capital from grid reliance to on-site resilience.

PJM Capacity Prices Surge 11-fold in Four Years

This chart quantifies the dramatic increase in capacity prices, which is the direct driver of the ‘$173 B in PJM Capacity Costs’ and massive utility investments discussed in this section.

(Source: Energy Industry Insights from Avanza Energy – Substack)

Table: PJM Policy Proposals and Regulatory Actions

| Policy / Order | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Emergency Curtailment Order (Sec. 202(c)) | May 2026 | DOE authorizes PJM to direct data centers with backup generation to curtail load during grid emergencies to prevent rolling blackouts. This followed a similar order that expired in January 2026. | Utility Dive |

| Proposed ‘Bring Your Own New Generation’ (BYONG) | Mar 2026 | PJM proposes requiring new data centers to procure their own new generation resources, shifting the cost and performance risk away from existing utility customers and onto the load creator. | [PDF] GPAEE |

| Proposed ‘Connect and Manage’ Framework | Jan 2026 | PJM proposes allowing new data centers to connect to the grid faster without funding immediate, extensive grid upgrades, but subjecting them to more frequent curtailment during stress events. | Jackson Walker LLP |

| FERC Directive on Co-located Resources | Dec 2025 | FERC directs PJM to create transparent rules to facilitate the interconnection of AI data centers that are co-located with their own power generation, encouraging private infrastructure solutions. | FERC |

Solar & Storage Dominate US Grid Interconnection Queues

The trend of solar and storage in interconnection queues is a direct consequence of energy policies and a key topic in regulatory actions, making it a relevant illustration for this policy-focused section table.

(Source: Reuters)

PJM Region at Epicenter, Virginia Data Centers Trigger Grid Strain

The data center power crisis is geographically concentrated within the 13 states and the District of Columbia that constitute the PJM Interconnection, with Northern Virginia emerging as the global epicenter of the problem. The sheer density of data center development in this single area is creating localized grid constraints that have regional and national implications for energy policy and reliability.

- Prior to 2024, data center growth was a point of economic pride for states like Virginia. After 2025, it has become a primary source of grid instability, with PJM’s load forecasts showing that nearly all projected demand growth through 2046 is attributable to data centers.

- The Dominion Energy service territory in Northern Virginia is the focal point. The concentration of hyperscale facilities has overwhelmed the local transmission system, creating a bottleneck that requires billions in upgrades and makes the area highly susceptible to curtailment orders.

- The problem is now spilling over into adjacent utility zones. PJM’s 2026 forecast shows that the demand surge is expanding beyond Northern Virginia, affecting utilities in Pennsylvania, Maryland, and Illinois, indicating the problem is spreading.

- In response, large tech companies are exploring solutions that bypass local constraints. Amazon is developing private power grids, while Microsoft is pursuing deals for nuclear power from small modular reactors (SMRs) to secure clean, reliable baseload power independent of grid-level volatility.

AI Data Center Power Demand to Skyrocket

This chart identifies the exponential power demand from AI as the specific ‘trigger’ for the grid strain centered in the PJM region, as described in the section heading.

(Source: Deloitte)

Grid Curtailment as Policy, DOE’s Section 202(c) Becomes a Recurring Tool

The use of emergency government orders to force data centers offline marks a significant maturation of the grid crisis, shifting mandatory curtailment from a theoretical risk to a standard operational planning assumption. The repeated issuance of Section 202(c) orders by the DOE demonstrates that regulators now view this as a necessary, recurring tool to manage seasonal grid stress, fundamentally altering the risk calculus for data center operators in the PJM region.

- Before 2025, emergency operations under PJM Manual 13 were viewed as an extreme measure for black swan events like major storms or widespread generation failures. Participation in demand response programs was largely a voluntary, revenue-generating activity.

- The DOE order in May 2026, which followed a similar winter order, validates that curtailment is now part of the standard operating procedure for managing predictable, weather-driven peak demand. The trigger is no longer an unexpected failure but the forecast of a hot summer or cold winter.

- This institutionalizes risk for data centers. The core value proposition of 100% uptime is now directly challenged by federal policy, forcing operators to invest heavily in on-site power infrastructure like gas turbines, solid-oxide fuel cells (SOFCs) from providers like Bloom Energy, and battery storage to avoid service interruptions.

- The policy also creates a new market dynamic. By targeting facilities with on-site backup, the order effectively commandeers private assets for public grid stability. This incentivizes data centers not just to own backup power but to design it for more frequent and prolonged use, increasing CAPEX and OPEX.

PJM Capacity Auction Prices Skyrocket

Skyrocketing auction prices signal extreme grid stress and supply-demand imbalance, which are the conditions that necessitate the use of emergency policy tools like curtailment, the subject of this section.

(Source: SemiAnalysis)

SWOT Analysis, PJM’s Market and Risks for Data Center Operators

The escalating power crisis in the PJM market has created a complex environment for data center operators, defined by significant financial risks counterbalanced by new opportunities for revenue generation and strategic differentiation. The period from 2025 onward represents a clear inflection point where passive energy consumption became an untenable strategy.

Data Centers Can Earn $200k/MW/yr From Grid Support

This chart highlights a significant financial ‘Opportunity’ for data centers to provide grid support, directly corresponding to the ‘O’ in the section’s SWOT analysis framework.

(Source: Energy Industry Insights from Avanza Energy – Substack)

Table: SWOT Analysis for Data Centers in the PJM Market

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Access to dense fiber networks and a large customer base in the Mid-Atlantic. Relatively stable and low-cost grid power. | Ability to monetize flexibility through demand response, earning up to $1, 000/MWh. Operators with on-site power gain a competitive advantage in reliability. | The crisis validated that data centers with sophisticated energy strategies (e.g., on-site generation, BESS) can turn a grid liability into a revenue stream and a key market differentiator. |

| Weaknesses | High concentration in a single geographic area (Northern Virginia). Growing but manageable reliance on grid power. | Extreme exposure to grid instability and curtailment orders. Massive CAPEX required for on-site power to ensure uptime, lowering IRR on new builds. | The weakness of total grid dependency was exposed. The “build it and the power will come” model was invalidated, replaced by a need for energy-first development strategies. |

| Opportunities | Participate in PJM’s capacity and ancillary service markets for supplemental revenue. Sign long-term PPAs for clean energy. | Become a grid-interactive asset, providing essential reliability services. Lead development of new energy models like “Bring-Your-Own-Generation” and direct nuclear PPAs. | The opportunity set expanded from passive participation in existing markets to actively shaping new energy infrastructure through direct investment and innovative partnerships with power producers. |

| Threats | Increasingly backlogged interconnection queues for new power generation. Rising capacity prices forecasted for future years. | Recurring emergency curtailment orders from the DOE. Extreme price volatility (LMPs >$2, 000/MWh, capacity >$329/MW-day). Loss of anchor tenants due to SLA failures. | The threat moved from a future financial risk (higher prices) to a present operational reality (forced shutdowns), making energy a primary constraint on growth and profitability. |

Data Centers Face Up to 7-Year Wait for Power

The extensive wait time for power is a critical ‘Threat’ or ‘Weakness’ for data center operators, making this chart a perfect data point to illustrate a key finding within the SWOT analysis table.

(Source: Energy Industry Insights from Avanza Energy – Substack)

2026-2027 Scenarios, PJM Curtailment Events and Data Center Response

The most critical strategic expectation for data center operators in the PJM region through 2027 is that emergency curtailment events will become more frequent, forcing an acceleration of investment into grid-independent power solutions. The market is now bifurcating between operators who can guarantee uptime through on-site assets and those who remain exposed to grid volatility.

- If this happens: PJM’s proposed “Bring-Your-Own-Generation” (BYOG) policy is approved by FERC and implemented for new interconnection requests.

- Watch this: An increase in the number and scale of direct partnerships between data center operators (e.g., Microsoft, Amazon) and power generation developers (e.g., Constellation, X-energy). We would also expect to see data center developers acquiring or co-developing power plant sites.

- These could be happening: This would validate the shift of infrastructure investment risk from the public to the private sector. It would create a new asset class of data center-anchored microgrids and accelerate the commercialization of technologies like SMRs and advanced geothermal, as data centers seek firm, 24/7 power.

- If this happens: The DOE continues to issue seasonal Section 202(c) curtailment orders for PJM ahead of summer 2026 and winter 2027.

- Watch this: A surge in orders for on-site power solutions, including natural gas turbines, battery energy storage systems (BESS), and SOFCs. Look for announcements from companies like Ceres Power and Hitachi Energy on new products or large-scale orders specifically targeting data center resilience.

- These could be happening: This signals that regulators have accepted curtailment as a long-term bridge solution. Data center SLAs will begin to include specific language and pricing tiers related to grid reliability and the use of on-site power, making energy resilience a formal part of the service offering.

The questions your competitors are already asking

This report covers one angle of data center survival strategies amidst the PJM power crisis. The questions that matter most depend on your work.

- What is actually happening with PJM’s emergency curtailment orders? Are they becoming a standard operating procedure for data centers?

- What is the outlook for on-site power generation deployment in PJM data centers by 2030?

- Which data center operators in the PJM region are adopting on-site generation and grid-interactive capabilities to ensure operational viability?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.