Berkshire Hathaway’s Hydrogen Strategy 2026: Why Cautious Evaluation Beats Market Hype

Berkshire Hathaway’s Low-Risk Hydrogen Projects Signal a Shift from Planning to Piloting

Berkshire Hathaway’s engagement in the hydrogen sector is defined by a strategic transition from long-term planning to tangible, low-risk operational testing. Instead of making large capital-intensive investments in standalone hydrogen production, the company is leveraging its subsidiaries to evaluate specific applications, using its vast industrial footprint as a controlled laboratory. This approach minimizes exposure to market volatility while building critical, firsthand operational knowledge.

- Between 2021 and 2024, Berkshire’s hydrogen interest was primarily visible through its energy utility subsidiaries, like Pacifi Corp, which modeled hydrogen combustion turbines and storage in its Integrated Resource Plans (IRPs) for post-2030 deployment. This represented a long-term, theoretical exploration phase.

- Starting in 2025, the strategy materialized into concrete action. Berkshire Hathaway’s 2025 Annual Report, released in February 2026, explicitly states that hydrogen locomotives are being “evaluated and field-tested” within the company, a clear reference to its BNSF Railway subsidiary.

- This shift from paper studies to physical pilots demonstrates a methodical de-risking process. By testing hydrogen in a high-impact application like rail, Berkshire Hathaway can directly assess technical viability, infrastructure needs, and operating costs without committing to a broader, more speculative market entry.

Investment Analysis: A $9.7 Billion Petrochemical Play, Not a Hydrogen Bet

Berkshire Hathaway’s most significant recent transaction in the energy materials sector, the acquisition of Oxy Chem, is fundamentally an opportunistic investment in petrochemicals, not a strategic pivot to hydrogen. The company’s capital allocation continues to prioritize assets with established cash flows and clear value propositions over speculative ventures in emerging clean energy technologies, reinforcing its cautious stance.

OxyChem Capex Underpins Acquisition Logic

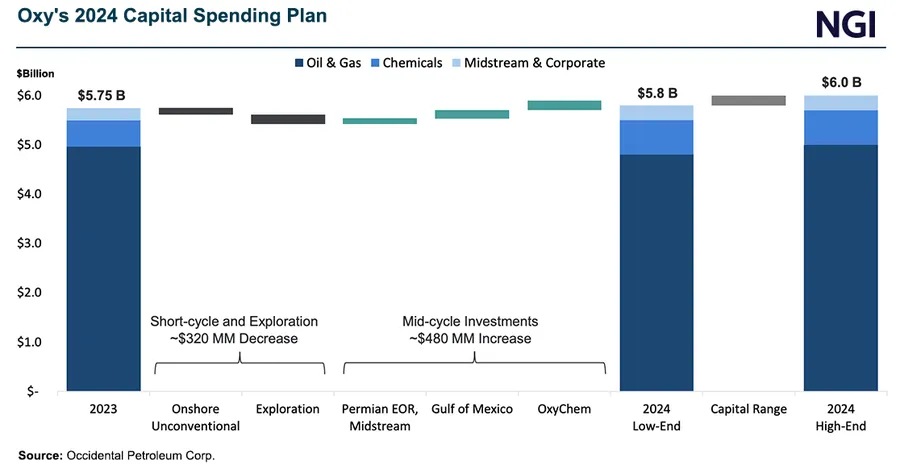

This chart details Occidental’s capital plan for OxyChem, reinforcing the section’s point that Berkshire’s acquisition was a strategic petrochemical investment, not a speculative hydrogen play.

(Source: Natural Gas Intelligence)

- The cornerstone transaction was the $9.7 billion all-cash acquisition of Occidental Petroleum’s chemical division, Oxy Chem, finalized in January 2026. Public statements framed the deal as a move to acquire a “low-cost resource runway” during a cyclical downturn in the petrochemicals market.

- While Oxy Chem’s assets could offer future synergies for hydrogen production (e.g., as a chemical feedstock or for carbon capture), this potential was not the stated driver of the investment. This contrasts sharply with the broader market’s fervor, where the green hydrogen sector was projected to be worth up to $12.85 billion in 2025.

- Other major investments, such as the $3.3 billion acquisition of a majority stake in the Cove Point LNG facility in 2023, underscore a focus on controlling existing energy infrastructure. These assets provide strategic optionality for future fuels but are not direct hydrogen plays.

Table: Berkshire Hathaway Strategic Capital Allocation (2023-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Acquisition of Oxy Chem | Jan 2026 | Acquired Occidental Petroleum’s chemical unit for $9.7 billion. The primary driver was gaining a low-cost production asset in a cyclical petrochemicals slump, not direct entry into hydrogen. | Indian Chemical News |

| Acquisition of remaining BHE Stake | Oct 2024 | Paid $2.4 billion to acquire the remaining 8% of Berkshire Hathaway Energy (BHE), consolidating control over the subsidiary central to its energy strategy. | Windpower Monthly |

| Acquisition of Cove Point LNG Stake | Sep 2023 | BHE acquired Dominion Energy’s 50% stake in the Maryland LNG terminal for $3.3 billion, increasing its ownership to 75% and strengthening its control of key gas infrastructure. | Pipeline & Gas Journal |

Partnership Strategy: Risk Mitigation Through Joint Ventures and Hub Participation

Berkshire Hathaway utilizes partnerships to gain exposure to the hydrogen value chain and adjacent clean technologies without bearing the full financial and technological risk. By collaborating with technology leaders and participating in regional ecosystems, the company secures strategic positioning and practical knowledge while limiting direct capital expenditure.

Geothermal Growth Validates BHE Partnership

The projected growth in the geothermal market, where BHE is a key player, highlights the strategic value of the assets being leveraged in its new joint venture, as detailed in this section.

(Source: Research Nester)

- In June 2024, BHE Renewables formed a joint venture with Occidental Petroleum to pilot Terra Lithia’s Direct Lithium Extraction (DLE) technology at BHE’s geothermal facilities in California. This partnership allows BHE to explore a critical clean energy supply chain (lithium) while creating a potential platform for co-located green hydrogen production powered by firm geothermal energy.

- Through its BNSF Railway subsidiary, Berkshire Hathaway became a partner in the Heartland Hydrogen Hub in North Dakota in January 2023. BNSF’s role is to provide rail transport logistics, positioning it as a critical infrastructure enabler for the regional hydrogen economy rather than a producer.

- These partnerships reflect a clear pattern: Berkshire Hathaway provides the operational scale, existing assets, and offtake stability, while its partners bring specialized technology. This symbiotic structure is a low-risk method for entering complex new markets.

Table: Key Berkshire Hathaway Hydrogen-Related Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Occidental Petroleum (Joint Venture) | Jun 2024 | BHE Renewables and Occidental formed a JV to pilot DLE technology at BHE’s California geothermal sites. This de-risks entry into lithium extraction and creates a potential nexus for clean hydrogen production. | Carbon Credits |

| Heartland Hydrogen Hub (Collaboration) | Jan 2023 | BNSF Railway partnered with Bakken Energy and Mitsubishi Power to provide rail logistics for the North Dakota hub, securing a role in hydrogen transport infrastructure. | Natural Gas Intelligence |

Geography: A North American Focus on Existing Operational Footprints

Berkshire Hathaway’s hydrogen activities are geographically concentrated in North America, specifically in regions where its subsidiaries already have significant infrastructure and operational control. This strategy leverages existing assets to minimize new logistical challenges and focuses efforts where regulatory and physical infrastructure advantages can be maximized.

Electricity Demand Drives Infrastructure Strategy

Projected growth in electricity demand provides the strategic rationale for Berkshire’s focus on its North American utility footprints, which serve as the foundation for new energy projects.

(Source: ClearPath)

- Between 2021 and 2024, the primary geographic focus was on planning activities within the service territories of its utilities. Pacifi Corp’s IRPs, for example, modeled hydrogen projects across its Western U.S. territory.

- From 2025 onwards, the focus has become more specific and project-based. Key locations include California’s Imperial Valley, where BHE Renewables is piloting DLE technology with its geothermal assets, and North Dakota, where BNSF is supporting the Heartland Hydrogen Hub.

- The field-testing of hydrogen locomotives is happening across BNSF’s extensive rail network, providing real-world data from diverse operating conditions across the continent.

- While direct activity is North American, Berkshire Hathaway’s investment in Japanese trading houses like Itochu Corp., which is active in global hydrogen projects, provides indirect exposure to international market developments without direct operational involvement.

Technology Maturity: Engaging at the Pilot and Evaluation Stage, Not Commercial Scale

Berkshire Hathaway is deliberately engaging with hydrogen technology at a pilot and evaluative stage, focusing on validating specific use cases rather than investing in commercial-scale production. This approach contrasts with pure-play hydrogen companies and indicates that Berkshire Hathaway does not yet view the technology as mature enough for large-scale, low-risk deployment.

Fossil Fuels Dominate Hydrogen Production

This chart illustrates the immaturity of the clean hydrogen sector, supporting the analysis that Berkshire is engaging cautiously at the pilot stage due to the technology’s current development level.

(Source: Energy and Policy Institute)

- The period from 2021 to 2024 was characterized by exploration of commercially available technologies within planning documents. For instance, Pacifi Corp’s IRPs considered hydrogen-capable combustion turbines and storage systems, which are technologies being developed by major OEMs.

- The shift in 2025-2026 is marked by the move to in-house “field-testing” of hydrogen locomotives. This is a crucial step up from planning, as it involves integrating a complex hydrogen application into an active industrial operation (BNSF), testing everything from fueling logistics to performance and reliability.

- The company is also focused on enabling technologies like DLE. The successful demonstration of DLE at BHE’s geothermal sites validates a technology that is adjacent but critical to the clean energy transition, providing a pathway to creating the firm renewable power needed for cost-effective green hydrogen. The power demands from emerging AI and data centers make such firm power sources increasingly valuable.

SWOT Analysis: Berkshire Hathaway’s Calculated Hydrogen Position for 2026

Berkshire Hathaway’s hydrogen strategy is built on its core strengths of immense capital and existing infrastructure, yet its risk-averse nature presents both opportunities for methodical entry and threats of being outpaced by more agile competitors. The changes between the earlier planning phase and the current pilot phase highlight a validation of its cautious, asset-led approach.

Power Market Scale Defines BHE’s Strength

The multi-trillion dollar scale of the power generation market provides context for the SWOT analysis, underscoring why ownership of BHE’s infrastructure is a core strategic strength for Berkshire Hathaway.

(Source: The Business Research Company)

- Strengths: The company’s unparalleled access to capital and ownership of critical infrastructure like BNSF and extensive energy grids provide a powerful platform for deployment once the technology is proven.

- Weaknesses: A conservative investment philosophy may cause it to miss out on first-mover advantages and the high-growth potential of the early-stage hydrogen market.

- Opportunities: The potential to vertically integrate by using Oxy Chem assets for feedstock, BNSF for transport, and BHE for power and offtake is a significant long-term advantage.

- Threats: The rapidly evolving hydrogen technology landscape and uncertain regulatory frameworks for incentives like the 45 V tax credit pose risks to long-term investment decisions.

Table: SWOT Analysis for Berkshire Hathaway Hydrogen Initiatives

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Vast capital resources and ownership of utility (BHE) and rail (BNSF) infrastructure. | Leveraging BNSF for locomotive pilots and BHE geothermal assets for DLE joint venture. Consolidation of BHE control. | The strategy of using existing operating companies as testbeds for new technology was validated, moving from theory to practice. |

| Weaknesses | Lack of direct hydrogen production experience. A culture that avoids speculative technology investments. | Continued absence of large-scale, direct investment in hydrogen production, even as competitors like Plug Power rally. | The company’s risk-averse nature was confirmed by the opportunistic petrochemical acquisition of Oxy Chem instead of a direct hydrogen play. |

| Opportunities | Potential to use natural gas pipelines for hydrogen blending. Use utility IRPs to plan for hydrogen integration. | Field-testing hydrogen locomotives for rail decarbonization. Exploring lithium extraction, a key enabler for the energy transition. | The opportunity to use its industrial assets (rail) for tangible pilots has been seized, providing a clear path to gain operational data. |

| Threats | Regulatory uncertainty around hydrogen tax credits (IRA). Competition from aggressive pure-play hydrogen companies. | Competitors like Bloom Energy gain traction in high-growth markets like data center power. BHE faces challenges in supplying enough power for existing data center customers. | The threat of falling behind agile competitors is materializing, as market demand for clean power from sectors like AI is surging now. |

Scenario Modelling: Locomotive Test Results Will Dictate Next Investment Cycle

The single most critical factor determining Berkshire Hathaway’s next move in hydrogen is the outcome of the hydrogen locomotive field tests. If these tests prove economically and operationally viable, watch for a significant, focused investment in rail decarbonization; if they fail, expect the company to remain in an observational mode, awaiting further market and technology maturation.

- If this happens: The hydrogen locomotive pilots at BNSF demonstrate favorable performance, reliability, and a clear path to cost-competitiveness against diesel.

- Watch this: Look for any public statements from BNSF or Berkshire Hathaway on the test results, announcements of expanded pilot programs, or initial RFPs for hydrogen fueling infrastructure along key rail corridors.

- This could be happening: A successful pilot would trigger a multi-billion dollar investment cycle focused on acquiring a fleet of hydrogen locomotives and building the necessary production and distribution infrastructure, potentially leveraging partners from the Heartland Hydrogen Hub. This would represent Berkshire Hathaway’s first large-scale, direct entry into the hydrogen economy, focused on an application where it has dominant market control.

Frequently Asked Questions

Is Berkshire Hathaway making a large investment in green hydrogen production?

No. The article emphasizes that Berkshire Hathaway is taking a cautious, evaluative approach. Its largest recent energy-related acquisition, the $9.7 billion purchase of Oxy Chem, was a strategic investment in petrochemicals, not a direct bet on hydrogen. The company is currently focused on low-risk pilot projects rather than large-scale, capital-intensive hydrogen production.

What is the most significant hydrogen-related project Berkshire Hathaway is currently working on?

The most significant project is the field-testing of hydrogen locomotives within its BNSF Railway subsidiary. This represents a shift from theoretical planning to tangible, operational testing of hydrogen in a high-impact application, allowing the company to gather real-world data on technical viability and operating costs.

How is Berkshire Hathaway participating in the hydrogen economy without being a direct producer?

Berkshire Hathaway is using partnerships and its existing assets to engage with the hydrogen ecosystem. For example, its BNSF Railway is a partner in the Heartland Hydrogen Hub, providing rail logistics and transportation support. This allows it to be a critical infrastructure enabler for the regional hydrogen economy without taking on the risks of production.

Why was the acquisition of a majority stake in the Cove Point LNG facility significant for Berkshire’s strategy?

The $3.3 billion acquisition of a controlling stake in the Cove Point LNG terminal underscores Berkshire Hathaway’s strategy of focusing on controlling existing, cash-flowing energy infrastructure. While such assets provide strategic optionality for future fuels like hydrogen, the primary goal is control over key infrastructure, not a direct investment in hydrogen technology itself.

What is the key factor that will determine Berkshire Hathaway’s next major move in the hydrogen sector?

According to the analysis, the outcome of the hydrogen locomotive field tests at BNSF is the single most critical factor. A successful pilot demonstrating economic and operational viability would likely trigger a significant investment cycle focused on rail decarbonization. An unsuccessful pilot would likely lead the company to continue its cautious, observational stance.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.