Hydrogen Project Collapse: Why Mega-Scale Ambitions Stalled in 2026

Project Cancellations Reveal A Sector-Wide Reality Check

The commercial model for developing mega-scale green and blue hydrogen projects fractured in 2025, triggering a strategic retreat from capital-intensive “moonshot” ventures. Analysis of BP‘s project pipeline reveals a definitive pivot away from the large-scale hydrogen hub strategy that defined the 2021-2024 period. The company is now aggressively dismantling its portfolio of multi-gigawatt ambitions in favor of smaller, de-risked projects that are directly tied to existing industrial demand and supportive regional policies.

- Between 2021 and 2024, the strategy was to establish global leadership by securing massive project stakes, such as acquiring a 40.5% share in the 26 GW Australian Renewable Energy Hub (AREH) and anchoring the 1 GW H 2 Teesside blue hydrogen project in the UK. This approach assumed that scale and first-mover status would overcome market uncertainties.

- The strategy reversed in 2025. BP exited AREH, cancelled H 2 Teesside, and paused or exited major projects in Australia, Oman, and the United States. This cull of over 27 GW of planned projects signals that the economics for large-scale developments, absent guaranteed government subsidies and firm offtake agreements, are unworkable.

- The new model is defined by smaller, focused initiatives like the 100 MW Lingen Green Hydrogen project in Germany and a 25 MW plant in Spain. These projects survive because they are scoped to serve specific, identifiable industrial customers in markets with clear regulatory support, representing a shift from building supply for a speculative market to meeting existing demand.

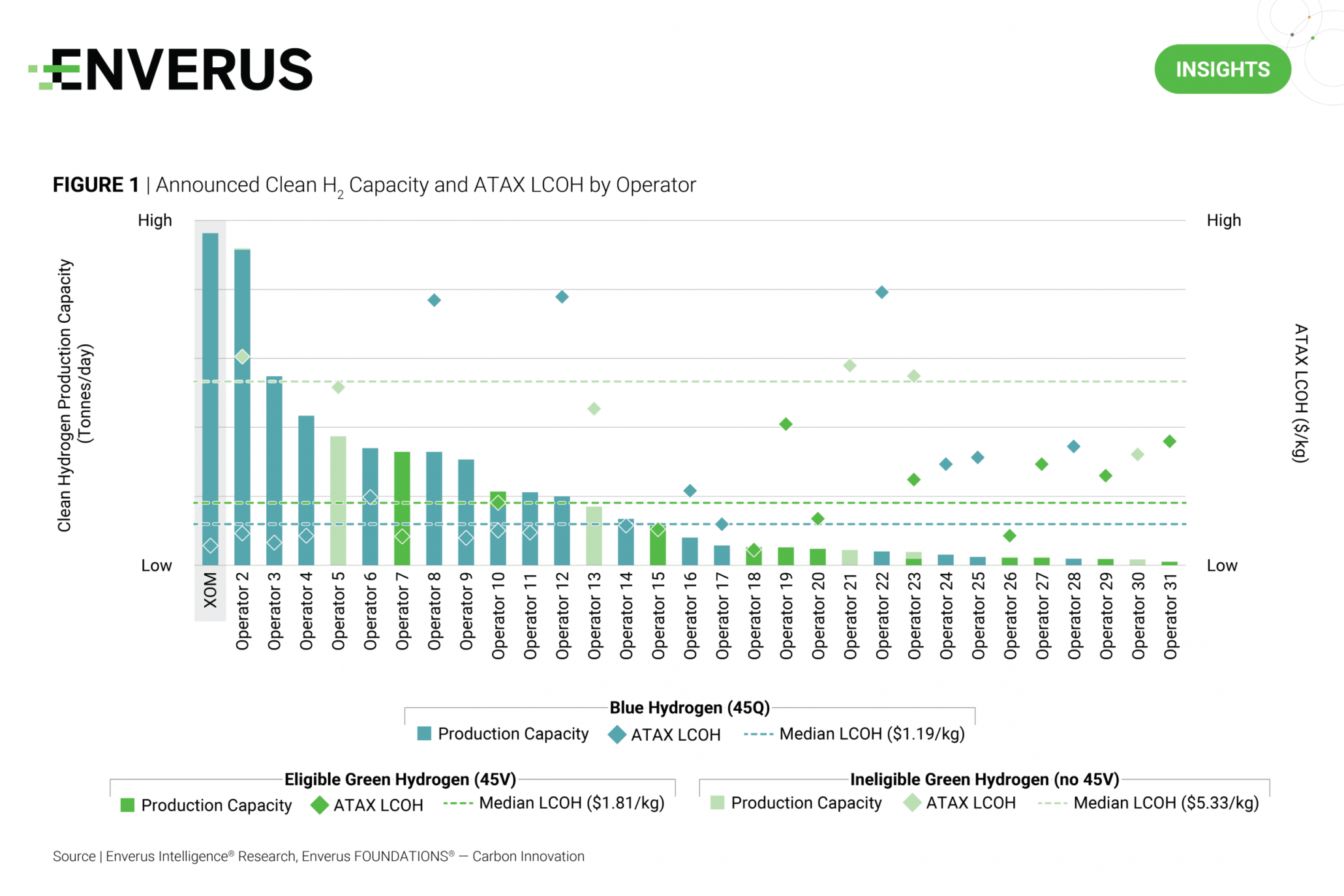

Hydrogen Projects Face Cost and Scale Reality Check

This chart’s comparison of project scale and cost directly illustrates the ‘sector-wide reality check’ described in the text. It visualizes why capital-intensive ‘moonshot’ ventures became commercially unviable.

(Source: Enverus)

Investment Pivot: A Retreat from Green Ambition to Oil and Gas Certainty

A wave of high-profile project cancellations throughout 2025, culminating in a multi-billion-dollar financial writedown, confirms a broad-based withdrawal from the hydrogen sector’s most ambitious ventures. This is not a nuanced adjustment but a full-scale capital reallocation back toward legacy fossil fuel operations, driven by a reassessment of future cash flows from low-carbon energy.

- The most direct signal of this strategic failure is the $4 billion to $5 billion non-cash impairment charge announced for Q 4 2025 results. This writedown on the gas and low-carbon portfolio, which includes hydrogen and carbon capture projects, is a formal admission that their expected future profitability has been drastically reduced.

- This financial adjustment was paired with a strategic decision to increase annual spending on oil and gas to $10 billion. This move directly redirects capital away from renewables and toward the company’s core business, prioritizing short-term shareholder returns over long-term, high-risk energy transition leadership.

- The contrast is stark: while billions are written off the low-carbon portfolio, the only new hydrogen investment moving forward is a modest $72.2 million for the 25 MW green hydrogen plant in Spain, underscoring the shift to small, manageable capital outlays.

Table: Key BP Hydrogen and Low-Carbon Project Cancellations & Pauses (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Duqm Green Hydrogen Project | December 2025 | BP exited the green hydrogen consortium in Oman, another major developer withdrawal testing the viability of Gulf state hydrogen strategies. | Energy News.biz |

| H 2 Teesside (Blue Hydrogen) | December 2025 | BP officially scrapped its flagship 1.2 GW blue hydrogen project in the UK. The site is being repurposed for an AI data center, marking a definitive failure of its UK blue hydrogen strategy. | Insider Media |

| Whiting Refinery H 2 Project | October 2025 | The planned blue hydrogen and carbon capture project at the Indiana, USA refinery was paused indefinitely, removing a key decarbonization project from its US portfolio. | The Future is Electric |

| Australian Renewable Energy Hub (AREH) | July 2025 | BP exited the massive 26 GW green hydrogen project in Western Australia, with a senior executive admitting, “We went too quickly, ” conceding the project’s scale was unmanageable. | PV Tech |

| H 2 Kwinana & Kwinana Renewable Fuels | February 2025 | The planned $1 billion green hydrogen and biofuel projects in Perth were put on indefinite hold due to policy and demand uncertainty. | Advanced Biofuels USA |

BP’s Hydrogen Partnerships: A Shift From Grand Alliances to Focused Ventures

BP’s partnership strategy has mirrored its project portfolio collapse, pivoting from forming broad consortiums for continent-spanning mega-projects to engaging in targeted collaborations on smaller, de-risked ventures with a clear commercial line of sight.

The ‘Grand Alliance’ Model BP Left Behind

This diagram of an integrated hydrogen economy represents the complex, multi-sector consortium model that BP is now abandoning. It visually defines the ‘before’ picture of BP’s old partnership strategy.

(Source: Sandia National Laboratories)

Visualizing BP’s Cancelled Blue Hydrogen Ambition

This diagram of the blue hydrogen process provides direct visual context for the cancelled H2 Teesside project mentioned in the table. It effectively illustrates the specific ambition that has now failed.

(Source: POWER Magazine)

- The previous strategy, exemplified by joining the 71-member Midwest Alliance for Clean Hydrogen (MACHH 2) in 2023 and taking operatorship of the AREH consortium in 2022, was about distributing risk across vast, government-backed alliances to enable massive scale.

- By 2025, this model had failed. The exit from the AREH consortium showed that even a shared-risk model could not overcome the economic hurdles of a 26 GW project. The MACHH 2 project remains active, but its future depends entirely on the materialization of up to $1 billion in U.S. government funding.

- The current partnership model is demonstrated by the joint project with Iberdrola, which began construction in February 2025. This collaboration is for a single, 25 MW plant with a joint investment of $72.2 million, aimed squarely at supplying green hydrogen to BP‘s adjacent refinery and the local ceramic industry, representing a tangible, demand-driven business case.

Table: Evolution of BP’s Strategic Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Corteva (Etlas JV) | January 2026 | A 50:50 joint venture focused on producing oil from crops for biofuel feedstock. This shows a pivot to adjacent, more mature low-carbon markets. | Indian Chemical News |

| Iberdrola España | February 2025 | Began construction of a 25 MW green hydrogen plant in Castellón, Spain, with a $72.2 million joint investment to serve the local refinery and industrial clients. This exemplifies the new, smaller-scale strategy. | Power Technology |

| Midwest Alliance for Clean Hydrogen (MACHH 2) | October 2023 | BP joined a 71-partner consortium selected for up to $1 billion in US government funding. This represents the old, large-scale consortium model that is now under scrutiny. | Hydrogen Insight |

BP’s Hydrogen Ambitions: Geographic Contraction from Global to European Hubs

BP‘s geographic footprint for hydrogen development has contracted dramatically, shifting from a global strategy targeting hubs in Australia, the US, and the UK to a highly concentrated focus on specific industrial zones in Germany and Spain. This geographic consolidation is a direct consequence of the company’s strategic retreat to markets with the most favorable and certain policy and demand signals.

Australian Hydrogen Pipeline Remains Largely Unbuilt

This chart shows that most Australian hydrogen capacity is still in the planning stage, validating BP’s strategic retreat from the region. It provides clear evidence for the geographic contraction described in the section.

(Source: Energy Connects)

- Between 2021 and 2024, BP pursued a global presence. It targeted Australia for green hydrogen exports (AREH, Kwinana), the UK as a premier blue hydrogen market (H 2 Teesside), and the US for industrial decarbonization (MACHH 2, Whiting).

- The year 2025 saw a near-total collapse of this global map. The company withdrew from its flagship projects in Australia (AREH, Kwinana), the UK (H 2 Teesside), and Oman (Duqm), and paused its Indiana, US project. This effectively erases its strategic presence in those regions’ large-scale hydrogen development plans.

- The surviving hydrogen strategy is now almost exclusively European. The active projects, Lingen (Germany) and Castellón (Spain), are located in established industrial regions with heavy manufacturing, existing infrastructure, and strong government support, including clear demand from BP‘s own refining operations.

Hydrogen’s Commercial Maturity: Scaling Model, Not Technology, Is the Hurdle

The widespread cancellation of BP‘s hydrogen projects is not an indictment of the underlying technology but a clear verdict on the failed commercial model for deploying it at a mega-scale. The events of 2025 demonstrate that a profound gap remains between technical readiness and the economic and policy frameworks required to support multi-billion-dollar hydrogen investments.

Core Challenges Hindering Hydrogen’s Commercial Scale-Up

This chart’s focus on policy, cost, and infrastructure hurdles perfectly aligns with the section’s argument that the commercial model, not the technology, is the key problem. It details the ‘profound gap’ between technical readiness and economic reality.

(Source: Springer Nature)

- The strategy from 2021-2024 was built on the assumption that technical feasibility for both blue and green hydrogen production was sufficient to justify enormous capital commitments. Projects like AREH and H 2 Teesside were advanced with the belief that markets and policy would materialize in time.

- In 2025, this assumption proved incorrect. The combination of high capital expenditure, uncertain long-term offtake contracts, and insufficient or slow-moving government support mechanisms made these mega-projects unbankable, forcing their cancellation.

- The surviving projects at Lingen and Castellón represent a different, more mature commercial model. By focusing on smaller, sub-100 MW electrolyzers co-located with refineries and industrial customers, BP is pursuing a strategy where offtake is certain and projects can be funded without depending on transformative policy shifts or speculative export markets.

SWOT Analysis of BP’s Hydrogen Strategy

BP‘s strategic pivot has fundamentally altered its position, exposing significant weaknesses from its failed hydrogen ambitions while creating opportunities to focus on more profitable, de-risked energy sectors. The company has traded its leadership role in the energy transition for short-term financial stability.

- Strengths have shifted from portfolio scale to operational discipline.

- Weaknesses have materialized from potential CAPEX exposure to realized financial losses.

- Opportunities have narrowed from global market creation to capturing value in smaller, proven markets.

- Threats related to policy and economic uncertainty have been validated, resulting in a loss of market position to competitors.

Table: SWOT Analysis for BP Hydrogen Initiatives

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Ambitious global portfolio of large-scale hydrogen projects (AREH, H 2 Teesside). Perceived first-mover advantage in key markets. | Operational expertise in conventional energy. Financial discipline to cut losses and reallocate capital. A few focused, viable green hydrogen projects remain (Lingen, Castellón). | The company demonstrated its ability to make difficult financial decisions, pivoting from ambition to a focus on profitability and de-risking its portfolio. |

| Weaknesses | High capital expenditure exposure on long-timeline projects with uncertain returns. Dependence on future policy and subsidy mechanisms. | Massive $4-5 billion portfolio writedown, signaling asset value destruction. Damaged credibility as an energy transition leader. A depleted project pipeline. | The financial risks inherent in the previous strategy were realized as concrete losses, forcing a public and costly strategic retreat. |

| Opportunities | To lead the development of a global hydrogen economy and capture significant market share in the UK, Australia, and the US. | Reallocate capital to more profitable and predictable oil and gas and biofuel operations. Develop a smaller, more profitable hydrogen business focused on industrial niches. | The opportunity shifted from market creation to market participation. BP is now positioned as a follower, not a leader, in the hydrogen sector, prioritizing safer returns over scale. |

| Threats | Execution risk on mega-projects. Policy and regulatory uncertainty. Competition from other energy majors and pure-play hydrogen developers. | Policy uncertainty and unfavorable economics were validated as project-killing factors. Competitors may push ahead and capture market share while BP retreats. Reputational risk from abandoning climate goals. | The primary threats materialized, forcing project cancellations. The company is now ceding ground in the race to build a global hydrogen business. |

Scenario Modelling: 2026 Hinges on a Smaller, Demand-Led Model

The viability of BP‘s downsized hydrogen strategy now rests entirely on its ability to prove a smaller, demand-led project model, with the Lingen project serving as the critical test case for 2026. If the company fails to secure firm buyers for its German facility, a further retreat from the sector is likely.

BP’s Scenarios Contrast Net Zero Ambition With Reality

This chart’s comparison of BP’s own energy scenarios directly matches the ‘Scenario Modelling’ heading. It visualizes the tension between the company’s past ambition and a more conservative trajectory, highlighting the critical choices for 2026.

(Source: Resources for the Future)

- The primary signal to watch is the outcome of the Expression of Interest process for the 100 MW Lingen Green Hydrogen project. Success in securing offtake agreements for the targeted 10, 000-12, 000 tonnes per year will validate the new strategy. Failure will signal that even this smaller model is not commercially viable.

- Monitor for further portfolio rationalization. The $4-5 billion writedown suggests a deep reassessment of all low-carbon assets. Early-stage projects that are less advanced than Lingen or the Iberdrola venture may be quietly shelved or cancelled.

- The timeline for deploying hydrogen fueling at the newly acquired Travel Centers of America network will be a key indicator of BP‘s commitment to hydrogen in transport. The company stated hydrogen would come “later, ” and any significant delays would confirm it is a low-priority, optionality play.

Frequently Asked Questions

Why did BP cancel its large-scale hydrogen projects in 2025?

BP cancelled its mega-scale projects, such as the 26 GW Australian Renewable Energy Hub (AREH) and H2 Teesside, because their commercial model was unworkable. The article states the economics for these large developments fractured due to a lack of guaranteed government subsidies and firm offtake agreements, making them unbankable.

What is BP’s new hydrogen strategy after these cancellations?

BP’s new strategy pivots from ‘moonshot’ ventures to smaller, de-risked projects directly tied to existing demand. This is exemplified by initiatives like the 100 MW Lingen Green Hydrogen project in Germany and a 25 MW plant in Spain, which are scoped to serve specific, identifiable industrial customers in markets with clear regulatory support.

How did this strategic shift impact BP financially?

The failure of its large-scale hydrogen strategy resulted in a major financial writedown. BP announced a $4 billion to $5 billion non-cash impairment charge on its gas and low-carbon portfolio for Q4 2025. This was paired with a decision to increase annual spending on oil and gas, redirecting capital away from its low-carbon ventures.

Does this mean hydrogen technology itself has failed?

No, the article argues that the project cancellations are not an indictment of hydrogen technology but a verdict on the failed commercial model for deploying it at a mega-scale. The surviving smaller projects demonstrate the technology’s readiness, but the key hurdle was the gap between technical feasibility and the economic and policy frameworks required for multi-billion-dollar investments.

Where is BP now focusing its hydrogen efforts geographically?

BP’s geographic footprint for hydrogen has contracted dramatically from a global strategy targeting Australia, the US, and the UK to a concentrated focus on specific European industrial zones. The company’s surviving active projects, Lingen and Castellón, are located in Germany and Spain, respectively, chosen for their heavy manufacturing, existing infrastructure, and strong government support.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.