China’s Hydrogen Strategy 2026: Why Petro China’s Infrastructure-First Model Will Dominate

Hydrogen Adoption Shifts: Petro China’s Industrial Focus vs. Sinopec’s Retail Network

China’s hydrogen economy is bifurcating into two distinct strategic models, with Petro China’s infrastructure-led, industrial-supply approach gaining significant momentum over the retail-focused strategy of its competitors. While rivals prioritized building out consumer-facing refueling networks between 2021 and 2024, Petro China has spent 2025 consolidating its position as a foundational producer and transporter of hydrogen, positioning it to dominate the more lucrative industrial decarbonization market.

- In the 2021-2024 period, competitor Sinopec announced an aggressive plan to build 1, 000 hydrogen refueling stations by 2025, targeting the transportation sector. In contrast, Petro China focused on large-scale production, culminating in its first major green hydrogen facility at the Yumen Oilfield becoming operational in March 2024 with a capacity of 2, 100 tons per year.

- The strategic pivot intensified in 2025, with Petro China winning a bid in June 2025 to construct a 190-kilometer dedicated hydrogen pipeline. This move into critical midstream infrastructure signaled a clear focus on supplying industrial clusters, a departure from the retail-centric approach.

- Petro China’s strategy is anchored in leveraging its colossal existing asset base. In 2023, the company successfully completed tests for blending hydrogen into its natural gas pipelines, a technological validation that promises to drastically lower transportation costs and accelerate industrial adoption.

- Further reinforcing its industrial integration model, Petro China is developing circular economy projects, such as the Dushanzi plan announced in December 2025. This facility will use by-product hydrogen from ethylene units to produce urea, embedding hydrogen use directly within its large-scale petrochemical operations.

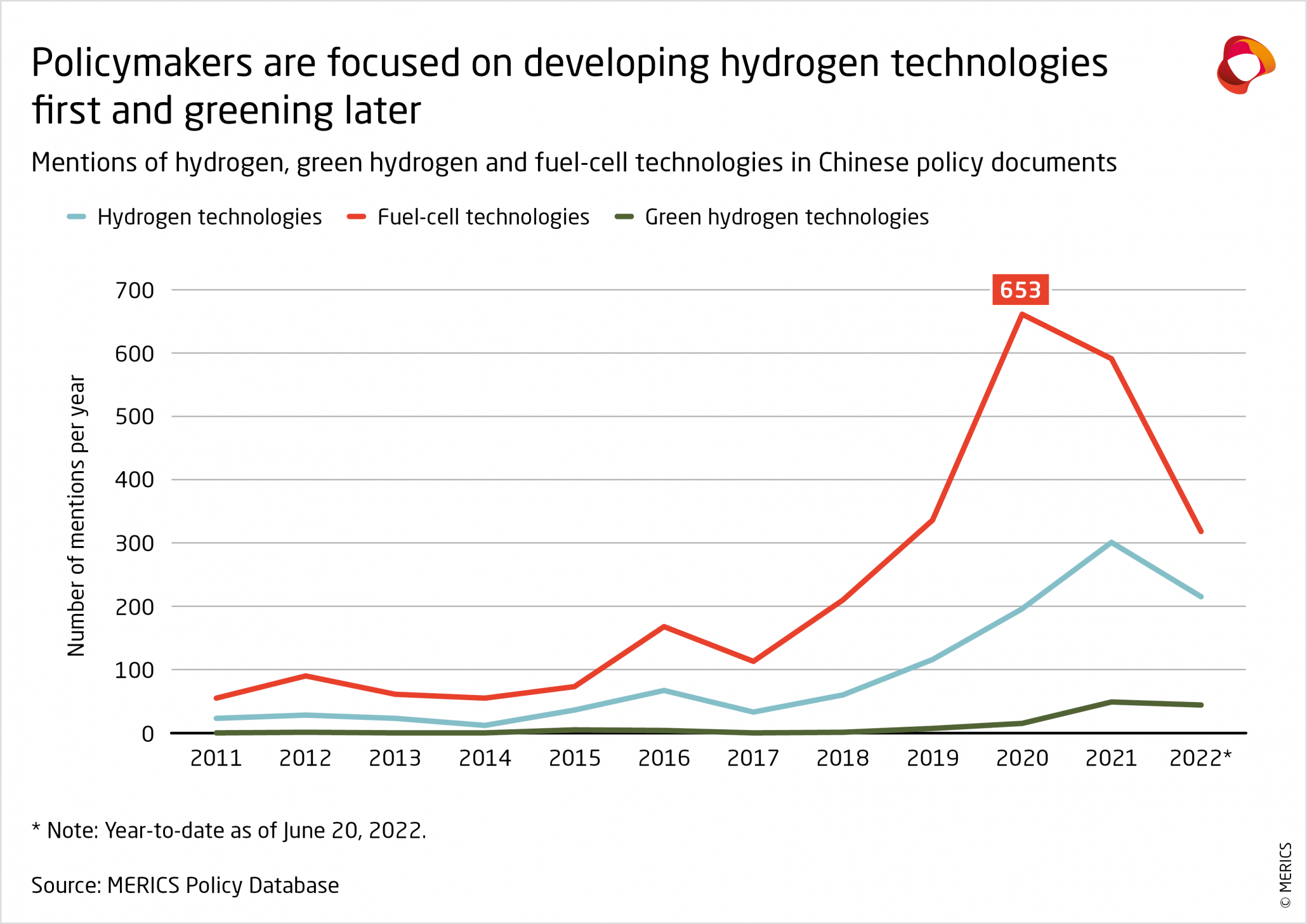

Policy Data Reveals China’s Hydrogen Strategy Split

This chart shows how a historical policy focus on fuel-cell vehicles created the retail-focused strategy that Petro China is now diverging from. It provides essential context for the market’s strategic bifurcation.

Petro China’s Strategic Investments: Funding an Infrastructure-Led Hydrogen Future

Despite allocating only 1% to 2% of its total capital expenditure to new energies, Petro China’s investments are highly targeted, prioritizing foundational assets for large-scale production and integration over a wide distribution of smaller projects. This disciplined spending focuses on acquiring green power capabilities and embedding hydrogen within its industrial complexes, revealing a long-term strategy to control the value chain from production to industrial use.

- A pivotal move was the US$839 million acquisition of its parent company’s electric unit, CNPC Electric Energy, in August 2024. This transaction secures integrated green power assets, a critical prerequisite for producing price-competitive green hydrogen at scale.

- While the $1.5 billion clean energy fund established in April 2021 supports broad renewable development, recent large-scale investments are aimed at creating captive hydrogen demand. The $4.7 billion Jilin Olefin Complex, announced in July 2025, will produce hydrogen as a by-product for integrated use within the facility.

- The investment in a $3.33 billion ethane-to-ethylene project in Hohhot, which will incorporate Carbon Capture, Utilization, and Storage (CCUS), further demonstrates a focus on creating infrastructure for low-carbon hydrogen (blue hydrogen) in addition to its green hydrogen initiatives.

Table: Petro China Strategic Hydrogen-Related Investments (2021-2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Jilin Olefin Complex | Jul 2025 | A $4.7 billion investment in a petrochemical complex that produces hydrogen as a by-product, creating a source of integrated industrial feedstock. | C&EN |

| Acquisition of CNPC Electric Energy | Aug 2024 | A US$839 million (5.979 billion yuan) acquisition to integrate green power generation assets, essential for scaling green hydrogen production. | SCMP |

| Hohhot Ethane Cracker with CCUS | Oct 2023 | A $3.33 billion investment in a petrochemical plant that will incorporate CCUS, enabling future blue hydrogen production. | Industrial Info |

| Clean Energy Investment Fund | Apr 2021 | A $1.5 billion (10 billion yuan) fund established to invest in solar, wind, and hydrogen projects to accelerate its low-carbon transition. | Nikkei Asia |

Strategic Alliances: How Petro China Leverages Partnerships for Hydrogen Technology and Market Access

Petro China is systematically building an ecosystem of partnerships to de-risk its entry into the hydrogen market, sourcing proven technology from specialized suppliers and collaborating with international energy majors to gain operational experience. This “buy-and-deploy” approach allows the company to focus on its core strengths in large-scale project execution and infrastructure management while accelerating its learning curve.

Visualizing PetroChina’s High-Tech Hydrogen Infrastructure Goal

This conceptual image visually represents the technology-forward, infrastructure-led hydrogen future that Petro China aims to build through its strategic partnerships and technology acquisition.

(Source: EnkiAI)

- The partnership with technology supplier ALLY, highlighted in February 2026, provides Petro China with access to one-stop, integrated solutions for hydrogen production and refueling stations. This indicates a strategy of procuring mature technology to speed up deployment.

- Collaboration with Shell on projects like the recently started 20 MW green hydrogen electrolyzer in China provides Petro China with direct experience in constructing and operating large-scale green hydrogen facilities alongside a global expert.

- The company is also pursuing international expansion through partnerships. A June 2023 Memorandum of Understanding with Oracle Energy aims to explore commercial avenues for a large-scale green hydrogen project in Pakistan, signaling an ambition to become a global player.

- The strategy extends to creating new markets, as seen in the collaboration with Dubai, which targets developing integrated LNG & Hydrogen Hubs by 2026. This move leverages its expertise in natural gas to build future hydrogen demand centers.

Table: Key Petro China Hydrogen Partnerships and Collaborations (2023-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| ALLY | Feb 2026 (Announced) | Technology supplier partnership for integrated hydrogen production and refueling station solutions, accelerating deployment with proven technology. | Freep.com |

| Dubai | Target by 2026 | Strategic collaboration to develop integrated LNG & Hydrogen Hubs, leveraging existing infrastructure and creating future demand. | Farmonaut |

| Shell | Ongoing (Project Start-up Announced) | Project collaboration on a 20 MW green hydrogen electrolyzer, providing hands-on experience with large-scale green hydrogen production. | Oil and Gas Advancement |

| Oracle Energy | Jun 2023 | Mo U to explore offtake and commercialization for a green hydrogen project in Pakistan, signaling international market expansion. | re News |

China’s Hydrogen Geography: Petro China Anchors Production in Resource-Rich Regions

Petro China’s hydrogen strategy is geographically concentrated, leveraging China’s vast renewable energy resources in the northern and northwestern provinces to power large-scale green hydrogen production. This approach contrasts with a distributed retail model and instead focuses on creating massive production hubs connected to industrial demand centers via dedicated and repurposed pipeline infrastructure.

Data Confirms Green Hydrogen’s Geographic Concentration

This chart validates the section’s geographic focus, showing that 89% of China’s green hydrogen production capacity is concentrated in the North and Northwest regions. This data supports Petro China’s strategy of building large production hubs there.

(Source: Takshashila Institution)

- National data shows that green hydrogen project planning is heavily skewed towards North China (45%) and Northwest China (44%), regions rich in solar and wind resources. Petro China is aligning its strategy directly with this geographic advantage.

- The company’s flagship projects are located in these key regions. The operational Yumen Oilfield project is in Gansu province (Northwest), and the planned 1 GW green hydrogen facility is in Qinghai province (Northwest).

- The crucial missing piece, transportation, is being addressed through infrastructure projects like the planned hydrogen pipeline connecting Wuhai and Hohhot in Inner Mongolia (North China), designed to move hydrogen from production zones to industrial users.

Technology Deployment: Petro China Focuses on Commercial Scale Production and Transport

Petro China is executing a pragmatic technology strategy focused on deploying mature, commercial-scale solutions for production and transport rather than engaging in high-risk, early-stage research. The period from 2024 to 2025 marks a clear transition from planning and testing to the operational deployment of key technologies that underpin its infrastructure-led model.

China’s Hydrogen Projects Shift From Planning to Operational

This forecast illustrates the market-wide shift from planning to execution discussed in the text. It shows a growing number of projects becoming operational, providing context for Petro China’s move to commercial-scale deployment.

(Source: PV Magazine)

- The commissioning of the Yumen Oilfield green hydrogen project in March 2024 represents a shift from pilot to commercial-scale production. This facility now produces 2, 100 tons of high-purity (99.99%) green hydrogen annually.

- A critical technological milestone was achieved in 2023 with the successful testing of long-distance hydrogen transport through existing natural gas pipelines. This validated a core tenet of its strategy: leveraging existing assets to create a low-cost hydrogen delivery network.

- The company’s exploration of large-scale Underground Hydrogen Storage (UHS), leveraging its extensive geological expertise from oil and gas operations, shows it is preparing to solve the future challenge of seasonal energy storage needed for a stable hydrogen supply chain.

SWOT Analysis: Assessing Petro China’s Hydrogen Strategy for 2026

Petro China’s hydrogen strategy effectively leverages its legacy strengths in infrastructure and capital to build a defensible position in the industrial hydrogen market. However, its cautious investment pace and reliance on partners for technology present weaknesses, while the immense opportunity in industrial decarbonization is threatened by agile competitors and the company’s continued focus on its core fossil fuel business.

Industrial Sector Represents Top Hydrogen Opportunity

This chart quantifies the primary ‘Opportunity’ in the SWOT analysis by showing industrial applications already form the majority of hydrogen demand. This validates Petro China’s strategic focus on industrial decarbonization.

(Source: Center on Global Energy Policy – Columbia University)

Table: SWOT Analysis for Petro China’s Hydrogen Initiatives

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Possession of vast natural gas pipeline network; significant capital reserves from core business; deep expertise in reservoir management. | Successful pipeline blending tests; acquisition of green power assets (CNPC Electric Energy); integration with petchem assets (Dushanzi, Jilin). | The strategy of leveraging existing infrastructure was validated by the successful pipeline blending tests, turning a theoretical strength into a practical one. |

| Weaknesses | Low stated CAPEX for new energies; lack of in-house, cutting-edge electrolyzer technology; slow mover in the hydrogen refueling market. | New energy CAPEX remains low at 1-2%; continued reliance on partners like Shell and ALLY for key technology and operational know-how. | The weakness of low relative investment was confirmed, indicating a deliberate, cautious strategy rather than an all-in transformation, which could cede ground to faster movers. |

| Opportunities | Potential to dominate China’s industrial hydrogen market; ability to use existing pipelines to lower transport costs; align with national decarbonization goals. | Won bid for 190 km hydrogen pipeline; launched 1 GW Qinghai project plan; secured international partnerships (Dubai, Pakistan). | The opportunity to become a midstream leader was validated by winning the major pipeline bid, moving from a strategic goal to a concrete project. |

| Threats | Aggressive retail-focused competition from Sinopec; risk of stranded fossil fuel assets; potential for renewable energy costs to remain high. | Sinopec continues its aggressive rollout of refueling stations; Petro China continues massive investments in oil (e.g., West Qurna-1). | The threat from a divergent competitive strategy was validated, as Sinopec and Petro China are now clearly targeting different segments of the hydrogen market. |

2026 Outlook: Why Pipeline Blending Success is Petro China’s Critical Hydrogen Milestone

The single most critical factor determining Petro China’s market leadership in 2026 is the successful commercial-scale deployment of hydrogen blending across its natural gas pipeline network. This technology is the key that unlocks a decisive cost advantage in supplying hydrogen to industrial users, making it the most important signal to watch.

PetroChina Expands Key Gas Infrastructure Assets

This chart shows PetroChina’s investment in its gas infrastructure, the core asset underpinning its critical hydrogen pipeline blending strategy. The expanding capacity highlights the company’s commitment to this foundational network.

(Source: Panda Perspectives – Substack)

- If Petro China announces specific pipeline segments and blending ratios for commercial operation, watch for a subsequent wave of large-scale industrial hydrogen supply agreements that undercut competitors reliant on trucking.

- The progress of the 1 GW Qinghai green hydrogen project is directly tied to this. Its economic viability hinges on cheap, high-volume transport to distant industrial zones, which only pipelines can provide.

- An increase in the 1-2% CAPEX allocation for new energies would serve as a powerful confirmation that the board is ready to accelerate the strategy, likely after seeing positive results from pipeline blending and initial production projects.

- The primary risk is that technical or regulatory hurdles delay the widespread rollout of pipeline blending. This would force Petro China to rely on more expensive transport methods, eroding its planned competitive advantage and making its remote production hubs less economical.

Frequently Asked Questions

What is the main difference between Petro China’s and Sinopec’s hydrogen strategies?

The primary difference is their target market and approach. Petro China is pursuing an infrastructure-led, industrial-supply model, focusing on large-scale production and pipeline transport to serve industrial decarbonization. In contrast, its competitor Sinopec has focused on a retail model, aiming to build 1,000 hydrogen refueling stations by 2025 to serve the transportation sector.

How is Petro China planning to transport the hydrogen it produces?

Petro China is developing a two-pronged transport strategy. First, it is building new dedicated infrastructure, such as the 190-kilometer hydrogen pipeline it won a bid for in June 2025. Second, and more critically, it plans to leverage its vast existing natural gas pipeline network by blending hydrogen into it, a method successfully tested in 2023 to drastically lower transportation costs.

Why is Petro China’s acquisition of an electric company significant for its hydrogen goals?

Petro China’s US$839 million acquisition of CNPC Electric Energy in August 2024 is a pivotal move because it secures integrated green power assets. Access to large-scale, price-competitive renewable electricity is a critical prerequisite for producing green hydrogen economically, underpinning its strategy to become a foundational producer.

Is Petro China developing its own hydrogen technology or buying it from others?

Petro China is primarily following a ‘buy-and-deploy’ approach. It is forming strategic partnerships to source proven technology from specialized suppliers, such as its collaboration with ALLY for integrated production solutions, and working with global experts like Shell to gain operational experience on large-scale projects. This allows Petro China to focus on its core strengths in project execution and infrastructure management.

What is the most important milestone to watch for in Petro China’s hydrogen strategy by 2026?

According to the analysis, the single most critical milestone is the successful commercial-scale deployment of hydrogen blending across its natural gas pipeline network. This technology is the key that unlocks a decisive cost advantage in supplying hydrogen to industrial users. Its successful rollout would likely trigger a wave of large-scale industrial supply agreements and validate the company’s entire infrastructure-led strategy.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.