Deep Sky DAC Project Finance, 28 k Tonnes from TD Bank & RBC, and $19.6 M in Offtakes (2023-2026)

The PPA Playbook for DAC: How Offtake Agreements are De-Risking Commercial Projects

Long-term offtake agreements have become the primary mechanism for de-risking capital-intensive Direct Air Capture (DAC) projects, shifting the industry from speculative venture funding toward bankable project finance. This model mirrors the Power Purchase Agreement (PPA) playbook that successfully financed the first utility-scale wind and solar farms. Between 2021 and 2024, early deals were novel but small in scale. The period from 2025 to today shows a clear acceleration in both the volume and strategic importance of these contracts, with major corporations securing multi-year supply to meet net-zero targets and de-risk future price volatility.

- The market’s evolution is highlighted by the contrast between early-stage agreements and recent large-scale commitments. In 2021, the 10-year, $10 million deal between Swiss Re and Climeworks was a landmark event. By 2026, this structure has become the standard, exemplified by TD Bank Group‘s agreement to purchase over 18, 000 tonnes of DAC credits from Deep Sky over ten years.

- Corporate buyers are moving from exploration to execution, using offtakes to secure a scarce supply of high-permanence carbon removals. Amazon committed to purchasing 250, 000 tonnes from 1 Point Five‘s DAC facility over 10 years, while Microsoft has built a diverse portfolio of offtakes, including deals with both Deep Sky and Climeworks.

- The structure of these deals provides the revenue certainty required for project financing. For a developer like Deep Sky, a bankable contract with a creditworthy counterparty like TD Bank is a critical asset that unlocks the debt and equity needed for construction, turning pilot projects into commercial realities.

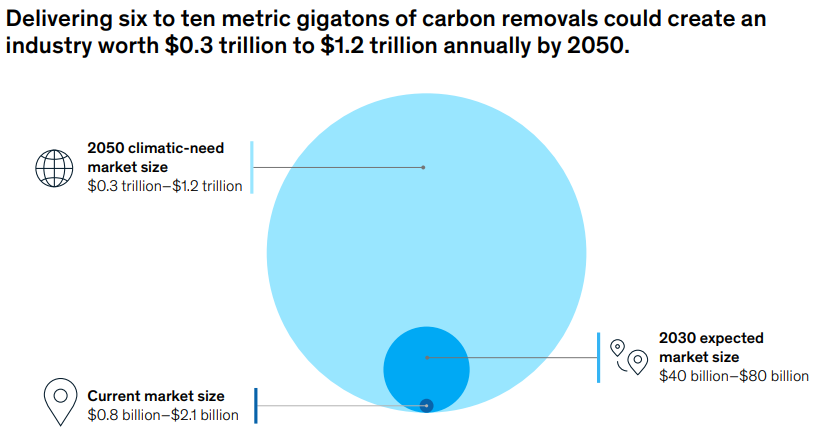

Carbon Removal Market to Reach $1.2T by 2050

The section describes a financial playbook (PPA/offtake model) to de-risk commercial DAC projects. The chart, showing a potential $1.2T market, perfectly establishes the massive economic opportunity that this playbook aims to unlock, providing the core commercial incentive for developing such projects.

(Source: Substack)

Deep Sky 28, 000 Tonne Offtake Pipeline (2023 to 2026)

Strategic partnerships are evolving from technology-validation pilots to large-scale, multi-year commercial offtakes, establishing a bankable playbook for the DAC industry. This shift is most visible in the emergence of two primary models: the technology-agnostic project developer, such as Deep Sky, and the vertically integrated technology owner, like Occidental’s 1 Point Five subsidiary. Both models rely on securing long-term offtake commitments to finance the enormous capital expenditures required for commercial-scale deployment.

- Deep Sky‘s business model leverages its position as a project developer to aggregate demand and de-risk technology. By securing offtake agreements with blue-chip partners like TD Bank, RBC, and Microsoft, it creates a bankable revenue stream before selecting the final technology for its large-scale hubs. This allows it to remain flexible and deploy the most efficient technology as the sector matures.

- The 10-year term has become the market standard, providing the long-term revenue visibility necessary for project finance. The pioneering $10 million deal between Swiss Re and Climeworks in 2021 established this precedent, which has since been adopted in major agreements, including Deep Sky‘s deals and Amazon’s commitment to 1 Point Five.

- These agreements are creating a competitive environment among DAC technology providers. Project developers like Deep Sky host multiple technologies at their pilot facilities, creating a “bake-off” where performance data will determine which technologies secure a place in future commercial-scale plants.

Charts Show Massive Carbon Removal Supply Gap

The section details a specific, near-term offtake pipeline for one company (Deep Sky’s 28,000 tonnes). The chart, showing a massive supply gap, provides the macro context for this micro-level action. It effectively frames the company’s project as a concrete first step towards closing the vast gap between required removal and current supply.

(Source: Carbon Removal Updates – Substack)

Table: Notable Corporate Offtake Agreements in Direct Air Capture (DAC)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| RBC & Microsoft / Deep Sky | Nov 13, 2024 | A 10-year agreement for 10, 000 tonnes of DAC credits. The deal provides Deep Sky with another anchor offtaker to support project financing and demonstrates a portfolio approach from Microsoft. | The Globe and Mail |

| Amazon / 1 Point Five (Occidental) | Sep 13, 2023 | A 10-year agreement to purchase 250, 000 metric tons of carbon removal from the Stratos DAC plant. This represents one of the largest single offtake agreements to date and provides a key revenue stream for the project. | Amazon |

| TD Bank Group / Deep Sky | May 9, 2023 | A 10-year offtake agreement for over 18, 000 tonnes of DAC credits. The contract serves as a critical project finance catalyst for Deep Sky and secures a supply of high-quality credits for TD Bank‘s net-zero strategy. | Deep Sky |

| Swiss Re / Climeworks | Aug 25, 2021 | The world’s first long-term purchase agreement for DAC, worth $10 million over 10 years. This deal established a benchmark for structuring offtakes to support the scaling of capital-intensive climate technology. | Swiss Re |

Carbon Removal Market Dominated by Few Actors

The section is a table listing notable corporate offtake agreements. The chart, which shows the market is dominated by a few actors, provides a high-level visual summary of this competitive landscape. It gives context to the table by showing how the listed agreements contribute to a market structure concentrated around a small number of key players.

(Source: Carbon Removal Updates – Substack)

US vs. Canada, Deep Sky DAC Policy and Geography

While U.S. policy has created the world’s most attractive investment environment for DAC, Canada is emerging as a key hub for project development by leveraging its clean energy resources, geological storage advantages, and a growing domestic buyer base. The period between 2021 and 2024 was defined by the global reaction to U.S. incentives. The years 2025 and 2026 are marked by other nations, particularly Canada, developing distinct regional advantages to compete for these projects.

- The U.S. Inflation Reduction Act (IRA) and its enhanced Section 45 Q tax credit, offering $180 per metric ton for stored CO₂, made the U.S. the default location for DAC projects post-2022. This catalyzed major investments, including Occidental‘s 1 Point Five Stratos facility in Texas, which attracted a major offtake from Amazon.

- Canada is establishing itself as a competitive alternative by combining its natural advantages with commercial innovation. In 2025 and 2026, companies like Deep Sky have leveraged Canada’s abundant, low-cost hydroelectric power and suitable geology for sequestration to build a strong project pipeline. Planned facilities in Quebec and Manitoba are supported by domestic buyers like TD Bank and RBC.

- Europe remains a hub for technology innovation but faces different economic and geographical constraints. Climeworks has successfully deployed its technology in Iceland, utilizing geothermal energy for its Orca and Mammoth plants, but scaling across the continent presents challenges related to energy costs and consistent policy support compared to North America.

Carbon Removal Technologies Compared by Cost & Permanence

This section compares US and Canadian policy for DAC. The chart, comparing carbon removal technologies, justifies the section’s focus on DAC. It explains DAC’s strategic value (high permanence) relative to other technologies, setting the stage for why it is a technology worthy of specific policy and geographical consideration.

(Source: Substack)

TRL 7 to 9, Deep Sky and the Commercialization Leap

Direct Air Capture technology has advanced from pilot-scale demonstrations (TRL 6-7) to the verge of first-of-a-kind commercial deployment (TRL 8-9), with long-term offtake agreements functioning as the critical catalyst needed to bridge the commercial “valley of death.” In the 2021-2024 period, the industry focused on proving the technology worked. The strategic focus in 2025 and 2026 has shifted to proving it can be deployed at scale and at a viable cost.

- The primary challenge for the DAC market is scaling production while driving down costs from the current range of $600 to $1, 000 per tonne of CO₂. While academic models project costs could fall to between $230 and $540 per tonne by 2050, early projects face significant “First-of-a-Kind” (FOAK) cost premiums.

- Offtake agreements provide the financial foundation for this scaling. The guaranteed revenue from a 10-year contract with a buyer like TD Bank is essential for a developer like Deep Sky to secure the hundreds of millions of dollars in project financing required to jump from a pilot facility to a commercial plant.

- This dynamic creates a feedback loop where commercial agreements accelerate technological maturity. By providing a bankable revenue stream, offtakes enable developers to place orders for equipment, finalize engineering designs, and move from demonstration to continuous operation, which is the only way to achieve cost reductions through learning-by-doing.

Chart Shows Gigaton-Scale Carbon Removal Needed

The section focuses on the ‘Commercialization Leap’ from demonstration (TRL 7) to full operation (TRL 9). The chart, showing a need for gigaton-scale removal, quantifies why this leap is so critical. It illustrates that achieving commercial scale is necessary to meet the immense challenge shown in the chart.

(Source: Google Groups)

SWOT Analysis, Deep Sky and the DAC Offtake Model

The Direct Air Capture market’s primary strength lies in the powerful combination of rising corporate demand for high-quality offsets and robust policy support, creating a compelling investment environment. However, the sector faces significant threats from extremely high upfront costs and the inherent execution risks associated with scaling complex, first-of-a-kind industrial facilities. The period from 2024 to 2025 validated the demand side of the equation, but the true test of the model now rests on successful project delivery.

- The key change between 2021-2023 and 2024-2025 was the validation of corporate demand. Early commitments were small and experimental, whereas recent offtakes from companies like Amazon and TD Bank are large, strategic, and integrated into corporate net-zero plans.

- Strengths in policy, such as the U.S. IRA, are creating opportunities for new business models. Deep Sky‘s technology-agnostic developer model is an opportunistic response, allowing it to partner with multiple DAC companies seeking to access favorable geographies and demand signals.

- The primary threat remains execution. The history of large-scale carbon capture projects is mixed, with many suffering from cost overruns and failing to meet operational targets. The success of the DAC industry hinges on the ability of leading firms to deliver their first commercial plants on time and on budget.

Table: SWOT Analysis for the DAC Offtake-Driven Business Model

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Technology proven at pilot scale; high permanence of removal (>1, 000 years). | Strong policy support (IRA 45 Q at $180/ton); growing list of blue-chip corporate buyers (TD, RBC, Microsoft). | Policy incentives and corporate demand have aligned to create a bankable offtake market, confirming a viable, albeit expensive, pathway to decarbonization. |

| Weaknesses | Extremely high cost ($600-$1000/ton); high energy intensity. | Lack of commercial-scale operational data; supply chain for key components (sorbents, reactors) is nascent. | The core weaknesses of high cost and energy use remain unresolved. The focus has shifted to accepting these costs for FOAK plants and proving they can be reduced through scaled deployment. |

| Opportunities | Nascent but growing voluntary carbon market; potential for government support. | Massive projected market growth ($19.8 B by 2035 for VCM); first-mover advantage for buyers and developers. | The scale of the opportunity was validated. Early, vague interest solidified into multi-million dollar, 10-year contracts, confirming a robust market for durable removals. |

| Threats | Reputational risk from unproven technology; competition from cheaper, lower-quality offsets. | Execution risk (scaling from pilot to commercial); potential for cost overruns and delays; policy uncertainty or reversal. | The primary threat has shifted from whether the technology works to whether it can be built and operated affordably at scale. The proposal of the “OBBBA” bill in the U.S. in 2025 highlighted the persistent risk of policy reversals. |

Chart Shows Carbon Removal is Essential for Climate Goals

As a SWOT analysis table, this section details the pros and cons of the business model. The chart, showing carbon removal is essential for climate goals, provides the fundamental justification for the entire endeavor. It contextualizes the SWOT by showing that despite any weaknesses or threats, the model supports a technology that is non-negotiable for meeting climate targets.

(Source: Google Groups)

Deep Sky: From Offtake to FID

The single most critical action for the DAC sector in the next 12-18 months is the conversion of large-scale offtake agreements into Final Investment Decisions (FIDs) and the commencement of construction on commercial-scale plants. The market has validated demand; now, developers must prove they can deliver the supply. Failure to transition from contracts to concrete will undermine confidence in the entire offtake-as-finance model.

- The most important forward-looking signal is an FID announcement from a company like Deep Sky for its first commercial-scale facility. This would be the definitive validation that offtake agreements with partners like TD Bank are successfully unlocking project finance.

- Watch for price discovery in the market. While most current deals are private, any future offtake agreements from competitors like Climeworks or 1 Point Five that disclose pricing will set a crucial benchmark for the durable CDR market and influence the perceived value of existing contracts.

- Monitor the response from competing financial institutions. If other major banks follow TD Bank’s lead by signing their own large, multi-year DAC offtake agreements, it will confirm a sector-wide strategic shift and intensify the race to secure a limited supply of high-quality CDR credits.

Chart Shows Widening Carbon Removal Gap

This section describes the critical project development stage ‘From Offtake to FID’ (Final Investment Decision). The chart, showing a widening removal gap, adds a sense of urgency to this process. It visually demonstrates that the problem is growing, highlighting the importance of successfully reaching FID to bring new removal capacity online.

(Source: Carbon Removal Updates – Substack)

The questions your competitors are already asking

This report covers one angle of the project finance and offtake strategy for Direct Air Capture. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the DAC offtake market?

- Deep Sky investments and funding. Are its projects on track to deliver the 28,000 tonnes secured by TD Bank and RBC?

- What are the opportunities for project finance banks in the emerging DAC market?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.