Top 10 Carbon Capture Incentives: US DOE’s $12.1 B BIL, $180/ton 45 Q credit, and 6 key programs (2024-2025)

The global carbon capture landscape has fundamentally shifted from research-focused pilots to commercial-scale deployment, driven almost entirely by substantial government financial mechanisms. Analysis of activity in 2024 and 2025 reveals that a handful of powerful incentives, predominantly from the United States, have created a bankable business case for both point-source Carbon Capture, Utilization, and Storage (CCUS) and Direct Air Capture (DAC). The passage of the Inflation Reduction Act (IRA), with its enhanced Section 45 Q tax credit now offering up to $180 per metric ton for DAC, provides the long-term revenue certainty needed to secure financing. This is powerfully combined with the Bipartisan Infrastructure Law (BIL), which de-risks enormous upfront capital costs with approximately $12.1 billion in direct funding for carbon management projects. The dominant theme for 2025 is the race to deploy, as companies move to capitalize on these programs to build the world’s first large-scale carbon management facilities.

Top Government Incentives Accelerating Deployment

The following list details the key government programs and financial mechanisms that defined carbon capture investment and project development in 2024 and 2025.

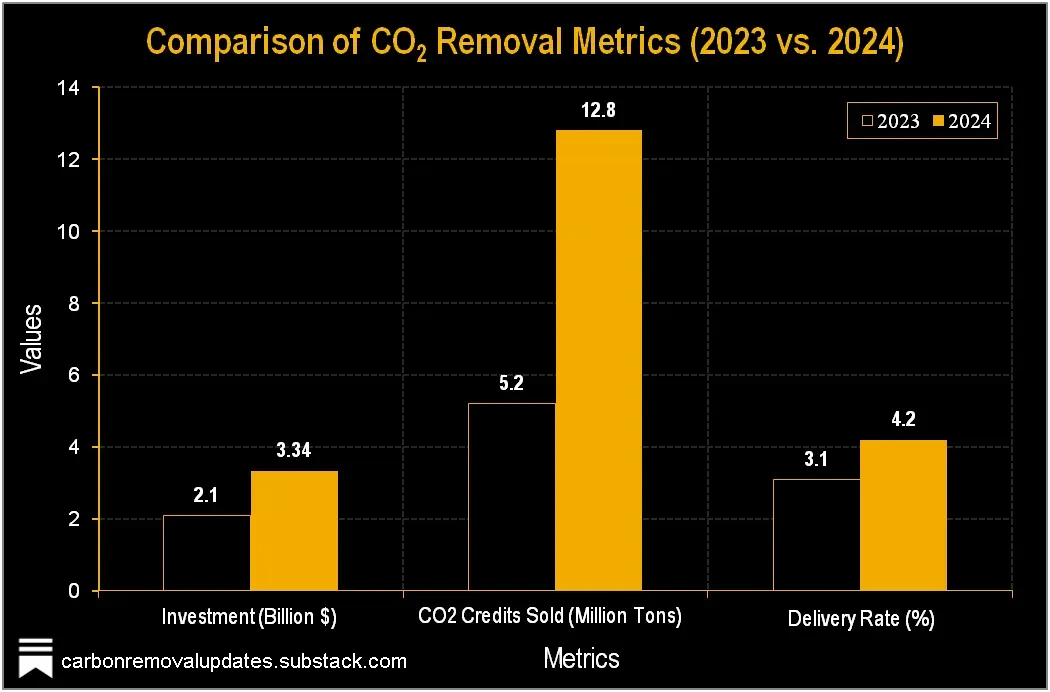

CO2 Removal Investment Surges in 2024

The section heading discusses ‘Government Incentives Accelerating Deployment.’ This chart, showing a surge in investment, provides direct evidence of the market’s response to these incentives, effectively illustrating the acceleration mentioned.

(Source: Carbon Removal Updates – Substack)

1. U.S. Section 45 Q Tax Credit (IRA Enhancement)

Jurisdiction/Program: United States (Federal)

Funding/Value: $85/ton (Point-Source CCS), $180/ton (DAC)

Targeted Technology: Performance-based tax credit for geologic storage of CO 2 from industrial sources and direct air capture. This is the primary financial driver for U.S. projects.

Source: STAYING THE COURSE – Global CCS Institute

2. U.S. Bipartisan Infrastructure Law (BIL) Funding

Jurisdiction/Program: United States (Federal)

Funding/Value: $12.1 Billion

Targeted Technology: A wide range of carbon management technologies, including large-scale demonstration, commercial deployment, and CO 2 transport and storage infrastructure.

Source: 2025 FEDERAL POLICY BLUEPRINT – Carbon Capture Coalition

3. U.S. DOE Regional Direct Air Capture (DAC) Hubs Program

Jurisdiction/Program: United States (Department of Energy)

Funding/Value: $3.5 Billion (initial) + $1.8 Billion (new funding announced Dec. 2024)

Targeted Technology: Development of four regional hubs, each designed to capture and store at least 1 million metric tons of CO 2 annually using DAC technology.

Source: OCED Announces up to $1.8 Billion in New Funding

DAC Costs Decrease with Increased Deployment

The Regional DAC Hubs Program is designed to build large-scale projects to drive down costs. This chart perfectly illustrates the economic principle behind the program’s strategy: costs fall as deployment increases.

(Source: Kleinman Center for Energy Policy – University of Pennsylvania)

4. UK CCUS Cluster Sequencing Program

Jurisdiction/Program: United Kingdom

Funding/Value: Up to £22 Billion (~$28 Billion)

Targeted Technology: Funding for shared transport and storage infrastructure to develop two major industrial carbon capture clusters (Hy Net and East Coast Cluster).

Source: Power Systems Transformation – Energy Transitions Commission

5. U.S. DOE Carbon Management Funding Opportunities (Jan 2025)

Jurisdiction/Program: United States (Department of Energy)

Funding/Value: $3.1 Billion

Targeted Technology: A second round of funding under the BIL for carbon capture technology development, deployment, and associated transport infrastructure.

Source: DOE Announces $3.1 Billion Now Available for Carbon Management Tech

6. U.S. Carbon Capture Demonstration Projects Program

Jurisdiction/Program: United States (Department of Energy)

Funding/Value: $2.5 Billion

Targeted Technology: Cooperative agreements for six commercial-scale demonstration projects, with $890 million already awarded to sites in Texas and North Dakota.

Source: Why Wind and Solar Need Natural Gas: A Realistic Approach

Chart Details Carbon Capture Costs By Industrial Source

The Demonstration Projects Program aims to prove carbon capture technology across various sectors. This chart, detailing cost variations by industrial source, provides the rationale for why such demonstrations are necessary.

(Source: ScienceDirect.com)

7. Canada’s CCUS Investment Tax Credit (ITC)

Jurisdiction/Program: Canada (Federal)

Funding/Value: 60% (DAC), 50% (Point-Source), 37.5% (Transport/Storage) of CAPEX

Targeted Technology: A refundable tax credit on the capital cost of equipment for CCUS and DAC projects, designed to compete with the U.S. 45 Q incentive.

Source: STAYING THE COURSE – Global CCS Institute

8. EU Innovation Fund

Jurisdiction/Program: European Union

Funding/Value: ~€40 Billion (2020-2030)

Targeted Technology: Grant funding for a wide range of innovative low-carbon technologies, with CCUS being a key eligible category to meet Europe’s carbon management goals.

Source: State of CCU/S in Europe 2024/2025

9. Australia’s Carbon Capture Technologies Program

Jurisdiction/Program: Australia (Federal)

Funding/Value: $65 Million

Targeted Technology: Grant funding awarded in 2024 to projects aimed at reducing emissions in hard-to-abate industrial sectors through CCUS technology deployment.

Source: Developments with Carbon Management (CCUS and CDR)

10. U.S. Carbon Negative Shot™ Initiative

Jurisdiction/Program: United States (Department of Energy)

Funding/Value: R&D funding with a target of <$100/ton CO 2 removal

Targeted Technology: An R&D initiative to drive down the cost of CO 2 removal technologies, including next-generation DAC. A $10 million funding round was announced in January 2026.

Source: Congress invests in carbon removal innovation

Table: Top Government Incentives for Carbon Capture (2024-2025)

| Incentive Name | Jurisdiction | Total Funding / Value | Source |

|---|---|---|---|

| Section 45 Q Tax Credit (IRA Enhanced) | United States | $85/ton (CCS), $180/ton (DAC) | Global CCS Institute |

| Bipartisan Infrastructure Law (BIL) Carbon Management | United States | $12.1 Billion | Carbon Capture Coalition |

| Regional DAC Hubs Program | United States (DOE) | $1.8 Billion (New Funding) | U.S. Department of Energy |

| UK CCUS Cluster Sequencing | United Kingdom | £22 Billion (~$28 B) | Energy Transitions Commission |

| Carbon Management Funding (BIL Round 2) | United States (DOE) | $3.1 Billion | Holland & Knight |

| Carbon Capture Demonstration Projects Program | United States (DOE) | $2.5 Billion | ITIF |

| CCUS Investment Tax Credit (ITC) | Canada | 37.5% – 60% of CAPEX | Global CCS Institute |

| EU Innovation Fund | European Union | ~€40 Billion (2020-2030) | dena |

| Carbon Capture Technologies Program | Australia | $65 Million | Clean Energy Ministerial |

| Carbon Negative Shot™ Initiative | United States (DOE) | Target <$100/ton | Carbon Removal Alliance |

CCUS and DAC Applications, A Multi-Layered Incentive Strategy for Deployment

The diversity of government incentives reflects a sophisticated, multi-layered strategy to nurture the entire carbon capture value chain. These are not one-size-fits-all programs. For mature, point-source capture technologies at industrial facilities, performance-based tax credits like the U.S. 45 Q and Canada’s ITC provide a crucial long-term revenue stream that makes projects bankable. For capital-intensive, first-of-a-kind commercial facilities like DAC plants, direct grants and funding from programs like the U.S. BIL ($12.1 billion) and the UK’s cluster program (£22 billion) are essential to de-risk the high upfront investment. This tiered approach signals to the market that support is available for different applications, from retrofitting a cement plant to building a greenfield DAC facility.

Power and Industry are Top Sources for Carbon Capture

The section heading explicitly refers to ‘CCUS and DAC Applications.’ This chart directly answers what those applications are by identifying power and industrial facilities as the top sources for carbon capture.

(Source: Congressional Budget Office)

United States Leads, The Global Race to Incentivize Carbon Capture Projects

While multiple nations are advancing carbon capture policies, the United States has established an undeniable lead in 2024-2025. The sheer scale and directness of its financial support—combining the 45 Q tax credit with billions in BIL funding—creates an investment environment that no other region currently matches. This has made the U.S. the primary destination for global capital and technology leaders like Occidental Petroleum (via 1 Point Five). In response, other countries are tailoring competitive policies. Canada’s CCUS ITC directly targets capital expenditures, offering up to a 60% credit for DAC projects. The UK is focusing on infrastructure, committing £22 billion to create “super clusters” that share transport and storage networks to reduce costs for individual emitters. The EU’s €40 billion Innovation Fund provides significant capital but is spread across a wider range of low-carbon technologies, making it a less concentrated incentive for CCUS compared to the U.S. model.

US IIJA & IRA Decarbonization Funding Detailed

The section claims the ‘United States Leads’ the global race to incentivize projects. This chart provides the key evidence for that claim by detailing the massive funding available through the IIJA (BIL) and IRA, which are the cornerstones of U.S. policy leadership.

(Source: National Academies of Sciences, Engineering, and Medicine)

$12.1 Billion, US BIL Funding Accelerates Commercial Scale-Up and Infrastructure

The array of incentives clearly illustrates how governments are nurturing carbon capture technologies at different stages of maturity. At the earliest stage, initiatives like the U.S. Carbon Negative Shot provide R&D funding to drive down costs for next-generation technologies, with a clear target of achieving carbon removal for less than $100 per ton. Moving up the maturity curve, the $2.5 billion Carbon Capture Demonstration Projects Program and the $3.5 billion Regional DAC Hubs Program are designed specifically to bridge the “valley of death” between pilot and commercial scale. These programs prove that technologies can operate reliably at megaton-per-year capacities. Finally, for mature and commercially ready technologies, the 45 Q tax credit acts as a long-term operational subsidy, guaranteeing a price for every ton of CO 2 captured and stored, thereby ensuring profitability and attracting private investment for widespread deployment.

Map Shows US Carbon Utilization Project Deployment

This section highlights how the $12.1 billion in BIL funding accelerates project scale-up. The map chart visually demonstrates the outcome of this funding by showing the geographic deployment of carbon utilization projects across the U.S.

(Source: ClearPath)

Carbon Capture Policy Risk, Monitoring US EPA Permitting and 2025 Political Shifts

For 2025 and beyond, the single most critical factor for project success will be navigating policy and regulatory frameworks. While funding is now robust, execution depends on factors outside of finance. Stakeholders must closely monitor the pace of EPA Class VI well permitting for geologic sequestration and acknowledge the risk of policy instability from political shifts.

- The significant backlog for Class VI well permits remains a primary bottleneck. Any acceleration or further delay in approvals by the EPA will directly dictate project construction timelines and final investment decisions.

- Political uncertainty in the U.S. poses a tangible risk. As one source noted, a potential pullback in federal support could “chill investment, ” making policy stability and durability a key variable for investors to watch through 2025.

- Advocacy continues for even stronger support. The push by groups to increase the point-source 45 Q credit to $120/ton shows that the policy landscape is still evolving, with potential for further upside.

- The steady rollout of funding, including $1.8 billion for DAC hubs in December 2024 and another $3.1 billion announced in January 2025, demonstrates strong current administrative commitment. However, future funding rounds could become political targets, making their status a key signal of long-term government support.