CNOOC CCUS Expansion: 10 M-Tonne Hub, Shell LNG Deal, and $18 B 2025 Capex for EOR Projects (2021-2025)

CNOOC CCUS Commercial Scale, Enping 15-1 EOR Project

In 2025, CNOOC advanced its carbon capture strategy from planning to large-scale execution, operationalizing an offshore Carbon Capture, Utilization, and Storage (CCUS) project directly integrated with its core oil production. This pragmatic model, which links sequestration to profitable Enhanced Oil Recovery (EOR), provides a robust economic justification that distinguishes it from many Western projects that are more dependent on government subsidies. The move signals a clear strategy to decarbonize existing fossil fuel operations rather than divesting from them.

- Between 2021 and 2024, CNOOC was in the development and engineering phase for its CCUS ambitions, laying the geological and technical groundwork for future projects while its primary commercial focus remained on expanding conventional oil and gas output.

- The strategic inflection point occurred on May 22, 2025, with the commissioning of the Enping 15-1 facility, China’s first offshore CCUS project. This facility is not a standalone pilot but a commercially integrated part of the oilfield’s operations.

- By September 2025, the project demonstrated significant operational success, having sequestered over 100 million cubic meters of CO 2. The facility began with an injection rate of 8 tonnes per hour, with plans to increase this to 17 tonnes per hour.

- The project’s primary purpose is to facilitate EOR, with a long-term goal to inject over 1 million tonnes of CO 2 to help increase crude oil production by an estimated 200, 000 tonnes. This dual-benefit approach establishes a clear commercial model for its carbon capture activities.

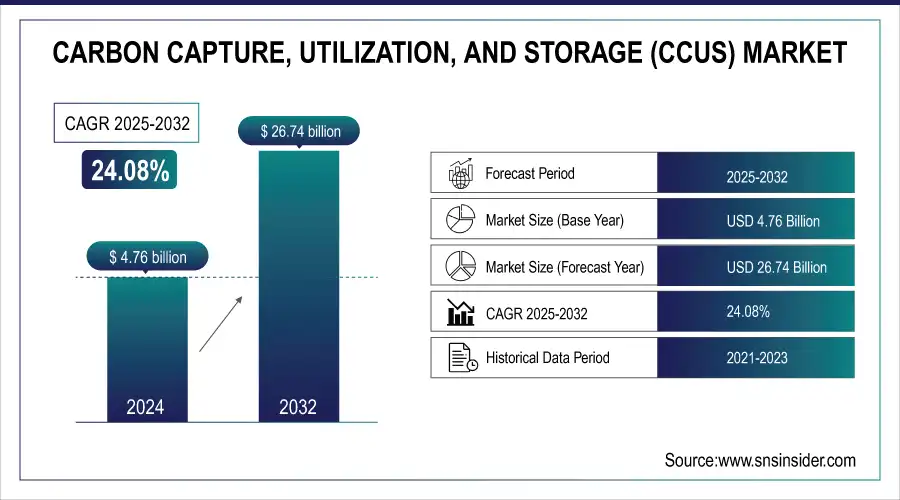

CCUS Market to See 24% Annual Growth

The chart’s projection of 24% annual growth in the CCUS market provides a strong business case for CNOOC’s investment in a commercial-scale project like Enping 15-1.

(Source: SNS Insider)

$18.7 B Capex, CNOOC CCUS and Production Growth

CNOOC‘s $115.72 billion market capitalization underpins a substantial 2025 capital expenditure program designed to fund both aggressive production growth and integrated decarbonization projects. The company’s financial strength enables it to self-fund capital-intensive CCUS initiatives as a tool to manage emissions from its expanding fossil fuel asset base. This level of investment in decarbonizing fossil assets runs parallel to major funding in other low-carbon technologies, such as the development of advanced reactors by firms like X-energy or the build-out of new energy storage supply chains.

- For 2025, CNOOC budgeted total capital expenditures between RMB 125 billion and RMB 135 billion (approximately $17.3 billion to $18.7 billion).

- This budget directly supports a 2025 net production target of 760 million to 780 million Barrels of Oil Equivalent (BOE), with growth targets of 810-830 million BOE by 2026.

- A portion of this capital is allocated to green and low-carbon initiatives, which are critical for achieving the company’s stated goal of reducing its greenhouse gas emissions intensity.

- The investment strategy indicates that CNOOC views CCUS not as a separate environmental, social, and governance (ESG) cost but as an operational expenditure that supports its primary business of hydrocarbon extraction while managing its carbon footprint.

Table: CNOOC and Competitor Low-Carbon Investments (2025)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| CNOOC / 2025 Capital Expenditure | Jan 2025 | Budget of up to $18.7 billion to fund production growth (780-800 M BOE) and integrated low-carbon projects like CCUS. | PR Newswire |

| Shell / Polaris CCS Project | Mar 2025 | Advancing a project in Scotford, Canada, to capture approximately 750, 000 tonnes of CO 2 per year from its refinery and chemicals plant. | Shell Global |

| Total Energies / Carbon Sinks Goal | Feb 2025 | Targeting 5 Mt of CO 2 stored per year by 2030 through a global portfolio of CCS and nature-based solutions projects. | Total Energies |

| Heidelberg Materials / Brevik CCS Project | Nov 2025 | Developing a project in Brevik, Norway, to capture 400, 000 tonnes of CO 2 per year from cement production as part of the Longship initiative. | Pre Scouter |

Energy Firms Dominate 2024 Carbon Market

The chart headline directly supports the section’s theme by establishing that energy firms are the primary players in the carbon market, setting the stage for a comparison of investments between CNOOC and its competitors.

(Source: CarbonCredits.com)

CNOOC 3 Major LNG Joint Ventures, Shell and Total Energies (2025)

CNOOC‘s CCUS initiatives are supported by its deep, long-standing joint ventures in the global energy market, particularly in Liquefied Natural Gas (LNG). These alliances with major international oil companies like Shell, Conoco Phillips, and Total Energies provide a foundation of technical expertise in complex offshore engineering and a collaborative framework that is now being extended to decarbonize the energy supply chain.

- Throughout 2025, CNOOC‘s participation in large-scale LNG projects like Queensland Curtis LNG (QCLNG) and Australia Pacific LNG (APLNG) remained central to its global gas strategy. These ventures require sophisticated offshore technology and project management skills that are directly transferable to offshore CCUS development.

- A supply agreement in August 2025 with Shell for the purchase of carbon-neutral LNG demonstrates a direct partnership on decarbonization efforts. This type of agreement shows a willingness to collaborate on managing emissions across the value chain.

- While no direct CCUS partnerships were announced in 2025, the existing JV structures and relationships with Western supermajors create a network for knowledge sharing, de-risking technology, and potentially co-investing in future large-scale carbon storage hubs.

Table: CNOOC Strategic Energy Partnerships (2025)

| Partner(s) / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Shell | Dec 2024 – Aug 2025 | Long-term partner in the QCLNG joint venture in Australia. In 2025, CNOOC was advised on a purchase of carbon-neutral LNG from Shell, showing direct collaboration on decarbonization. | Fangda Law |

| Conoco Phillips, Origin Energy, Sinopec | Dec 2024 | Member of the Australia Pacific LNG (APLNG) joint venture, securing LNG supply and building expertise in large-scale gas project execution alongside international partners. | DCCEEW |

China Focus, CNOOC Offshore CCUS Deployment Strategy

CNOOC‘s CCUS strategy is geographically concentrated in its domestic offshore assets, primarily in the South China Sea and Bohai Sea. This approach allows the company to leverage its extensive regional infrastructure, deep operational expertise, and controlled regulatory environment to de-risk and scale carbon storage technology close to its primary emissions sources. This domestic energy security strategy contrasts with the global scramble for resources seen in critical minerals, where supply chains are internationally contested.

- While CNOOC‘s activities between 2021 and 2024 included major international investments in Australia (QCLNG, Ichthys) and Africa (EACOP), its 2025 decarbonization efforts pivoted to its home territory.

- The landmark Enping 15-1 project is located in the eastern South China Sea, situated to capture CO 2 from the company’s own oilfields in the Pearl River Mouth Basin.

- The newly initiated 10-million-ton CCUS cluster project is based in Huizhou City, Guangdong, a major industrial zone in southern China, positioning it to potentially serve third-party emitters in the region.

- This domestic focus aligns with China’s national “dual-carbon” policy, allowing CNOOC to position itself as a key enabler of industrial decarbonization within the country’s borders, using its offshore expertise as a distinct competitive advantage.

CCUS at Commercial Scale, CNOOC Enping 15-1 Validation

In 2025, CNOOC successfully advanced its offshore CCUS technology from the pilot and development stage to a commercially integrated application. The operational launch of the Enping 15-1 project serves as a critical validation point, establishing a proven technical and operational template for linking large-scale carbon storage with ongoing hydrocarbon production through EOR.

- Prior to 2025, the company’s CCUS efforts were largely confined to feasibility studies, geological surveys, and engineering design for future offshore storage sites. The technology was considered to be in a pre-commercial, developmental phase for CNOOC.

- The commissioning of Enping 15-1 in May 2025 marked the transition to commercial operation. The project involves the entire CCUS chain: capturing CO 2 from gas processing, pressurizing it, and injecting it into a sub-seabed saline aquifer for permanent storage.

- The achievement of sequestering over 100 million cubic meters of CO 2 by September 2025 provided tangible proof of the technology’s effectiveness and the integrity of the storage formation.

- This milestone moves offshore CCUS from a theoretical decarbonization pathway to a demonstrated, operational reality for CNOOC, de-risking the technology for future, larger-scale deployments like the planned Huizhou cluster.

CCUS Market to Triple Between 2025-2030

The projection that the CCUS market will triple provides powerful validation for CNOOC’s decision to move forward with commercial-scale projects, indicating a rapidly expanding market for the technology being validated at Enping 15-1.

(Source: MarketsandMarkets)

SWOT Analysis, CNOOC EOR-Linked CCUS Strategy

CNOOC‘s core strength is its capacity to self-fund and integrate CCUS with profitable EOR, creating an economically sustainable model without reliance on external subsidies. However, this pragmatic approach firmly entrenches its fossil fuel business, posing a long-term strategic risk as global policy and investor sentiment accelerate toward full decarbonization, creating opportunities for technologies like advanced nuclear.

Table: CNOOC CCUS SWOT Analysis (2021-2025)

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong balance sheet and extensive offshore engineering expertise based on decades of oil and gas development. | Proven operational capability with the successful launch of Enping 15-1. Supported by a $115.72 B market cap and an $18.7 B annual capex budget. | The company translated its theoretical engineering strength into a tangible, operational CCUS project, validating its ability to execute complex carbon storage. |

| Weaknesses | High and growing carbon footprint from expanding fossil fuel production. CCUS plans were largely theoretical. | The scale of CCUS (1 M tonnes over a decade at Enping) remains minimal compared to emissions from producing nearly 800 M BOE/year. The EOR link deepens dependency on oil production. | The economic model for CCUS was validated, but it simultaneously exposed the strategy’s core weakness: it serves to prolong, not replace, fossil fuel extraction. |

| Opportunities | Potential to become a CCUS leader in Asia by aligning with China’s “dual-carbon” policy. | Initiated a 10-million-ton CCUS cluster in Huizhou, signaling ambition to build a carbon sequestration service business. The global CCUS market is growing at over 18%. | The opportunity shifted from a concept to a concrete project (Huizhou hub), indicating a strategic move to capitalize on the growing industrial decarbonization market. |

| Threats | Increasing global pressure to transition away from oil and gas. Regulatory uncertainty around carbon pricing. | Competitors like Shell and ADNOC are also scaling up CCUS projects. A global shift toward policies that favor pure sequestration over EOR could undermine CNOOC‘s economic model. | The competitive environment for CCUS leadership intensified, and the specific risk of CNOOC’s EOR-centric model became more pronounced as global policy discussions evolve. |

CCUS Market Growth Projected Through 2030

This general market growth chart serves as a strong introduction to a SWOT analysis table, framing the ‘Opportunities’ available to CNOOC in a growing market and providing context for the strategic assessment.

(Source: MarketsandMarkets)

CNOOC Scenario: From EOR Tool to Carbon Service Business

The most critical strategic development to monitor is whether CNOOC can successfully evolve its CCUS capability from an internal tool for enhanced oil recovery into a profitable, standalone carbon management service for third-party industrial emitters. Progress on the planned 10-million-ton Huizhou hub will be the primary indicator of this transition.

- If CNOOC announces significant partnerships with industrial players in the Pearl River Delta to offtake capacity at the Huizhou hub, this will signal a definitive move toward a carbon-as-a-service business model.

- Watch for official reports on the Enping 15-1 project successfully achieving its upgraded injection rate of 17 tonnes per hour. This milestone would validate the technology’s scalability and reliability, building confidence for much larger projects.

- The introduction of a meaningful carbon price or stricter emissions regulations by the Chinese government would fundamentally alter the economics, making pure sequestration projects viable and accelerating the business case for the Huizhou hub beyond EOR.

- Keep track of whether capital allocation in future business plans explicitly carves out funding for CCUS infrastructure that is not tied to EOR projects, which would confirm a strategic pivot toward a diversified carbon management portfolio.

Decarbonization Imperatives Drive New Revenue Models

The chart headline is a perfect thematic match for the section, as it explicitly discusses the emergence of new revenue models (like a carbon service business) driven by decarbonization, which is the core concept of the CNOOC scenario.

(Source: MarketsandMarkets)

The questions your competitors are already asking

This report covers one angle of CNOOC’s strategy for commercializing carbon capture. The questions that matter most depend on your work.

- What is actually happening with CNOOC’s Enping 15-1 project since its May 2025 commissioning?

- Is the Enping 15-1 project on track to meet its goal of injecting over 1 million tonnes of CO2 for enhanced oil recovery?

- Which other offshore oil and gas operators are adopting the CCUS-for-EOR commercial model pioneered by CNOOC?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.