Repsol CCUS Initiatives, $223 M EU Grant, 54 M-Tonne Hub, and US Expansion Project (2021 to 2025)

3 Major Projects, Repsol Shifts CCUS from Pilot to Commercial Scale

In 2025, Repsol transitioned its carbon capture, utilization, and storage (CCUS) strategy from planning and pilot phases to tangible, commercial-scale execution, underpinned by major public funding and international project development. This marks a significant shift from the 2021-2024 period, which was characterized by research, smaller-scale pilots, and strategic planning. The company is now actively deploying capital and advancing projects designed for material impact on its emissions footprint and to establish new low-carbon business lines.

- In March 2025, Repsol secured a critical €205 million ($223 million) grant from the European Union Innovation Fund for a large-scale offshore CO₂ storage project near Tarragona, Spain. The project is designed with a potential storage capacity of 54 million tons of CO₂ and an initial injection target of 2 million tons annually, validating its ability to attract non-dilutive funding to de-risk major capital expenditures.

- Expanding its geographic footprint, Repsol announced plans in August 2025 to drill a stratigraphic test well off the Texas coast in 2026. This is the first concrete step toward establishing a major CCS hub in the US Gulf Coast, a strategic move to capitalize on the favorable 45 Q tax credit policy, which was not a factor in the company’s primarily European-focused activities prior to 2025.

- Repsol is diversifying its technological portfolio beyond conventional point-source capture by launching a Direct Air Capture (DAC) pilot project in Brazil. This partnership with the Pontifical Catholic University of Rio Grande do Sul (PUCRS) represents an investment in next-generation technologies, contrasting with earlier efforts that focused mainly on abating emissions from its own industrial facilities and exploring alternative approaches like Microalgae Carbon Capture.

- The company’s utilization strategy also reached commercial maturity in 2025 with its Cartagena advanced biofuels facility coming online and the signing of the first commercial offtake agreement with Norwegian Cruise Line Holdings for methanol from its Ecoplanta project, proving a viable market for its CCU-derived products.

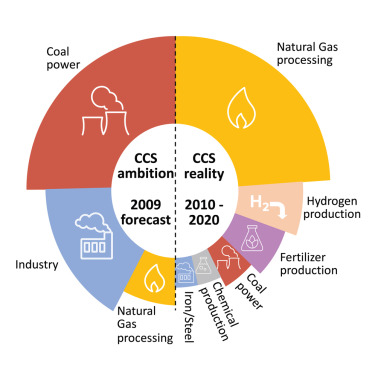

CCS Reality Diverged Sharply From 2009 Ambition

This chart provides historical context, showing that large-scale CCS ambitions have previously failed. This underscores the significance and challenge of Repsol’s current strategic shift from pilot projects to successful commercial-scale operations.

(Source: ScienceDirect.com)

Repsol €205 M EU Grant, CCUS Financing Strategy (2025)

Repsol’s 2025 investment strategy for carbon capture is defined by a sophisticated blend of non-dilutive public funding, dedicated internal capital allocation through a new sustainable financing framework, and strategic asset optimization to fund its long-term decarbonization goals. This formalized financial structure provides a clear pathway to deploy capital into a portfolio of projects that range from commercially mature CCS to emerging DAC technologies.

- The cornerstone of Repsol’s 2025 funding success is the €205 million ($223 million) grant from the EU Innovation Fund. This public financing is critical for de-risking the high upfront capital costs of the Tarragona offshore storage project, a multi-billion-dollar undertaking.

- The company reinforced its commitment by formalizing a target to allocate over 35% of its total net capital expenditure to low-carbon businesses, a framework that explicitly includes investments in upstream CCS and geothermal projects. This moves CCUS from a peripheral R&D item to a core part of its investment strategy.

- In March 2025, Repsol launched a Sustainable Financing Framework that officially qualifies CCUS and DAC projects as eligible for green financing. This financial innovation creates a dedicated capital pipeline, aligning its treasury operations with its climate objectives and attracting sustainability-focused investors.

- The company is also investing in enabling technologies, such as a €16 million investment to replace natural gas with biomethane for hydrogen production at its Puertollano refinery. This reduces the carbon intensity of its operations and supports the production of low-carbon fuels, a model also being explored by firms like Clean Energy Fuels.

Table: Repsol Low-Carbon Investments and Strategic Capital Moves in 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Stonepeak Asset Sale | Nov 2025 | Sold a 46.3% stake in a 777 MW US solar and storage portfolio. This move recycles capital from mature renewable assets to help fund new, capital-intensive low-carbon ventures like CCUS. | Stonepeak |

| Biomethane for H 2 Production | Jul 2025 | Invested €16 million to use biomethane instead of natural gas for hydrogen production at the Puertollano refinery, reducing the carbon intensity of its hydrogen supply for refining and synthetic fuel operations. | Hydrogen Insight |

| Brazil DAC Pilot | Apr 2025 | Committed an initial R$ 60 million as part of a joint project with PUCRS to develop and pilot Direct Air Capture technology, representing a seed investment in a future-facing carbon removal solution. | PUCRS |

| Tarragona Offshore CO₂ Hub | Mar 2025 | Secured a €205 million ($223 million) grant from the EU Innovation Fund to develop a large-scale offshore CO₂ storage project, providing critical non-dilutive funding to advance the project toward a final investment decision. | Carbon Herald |

| NEO Energy Consolidation | Mar 2025 | Consolidated its UK North Sea upstream business with NEO Energy. This strategic move optimizes its oil and gas portfolio, streamlining operations and potentially freeing up capital and resources for its energy transition projects. | Europétrole |

Carbon Capture Market To Reach $50.7B by 2034

The chart’s projection of a multi-billion dollar market provides the rationale for Repsol’s substantial low-carbon investments and strategic capital allocations detailed in the accompanying table.

(Source: Precedence Research)

CCUS Alliances, Repsol’s EU and Aramco Partnerships

In 2025, Repsol solidified its CCUS strategy through critical partnerships that provide a combination of funding, technical expertise, and market access, effectively de-risking its entry into new and capital-intensive carbon management value chains. These collaborations are fundamental to both its storage (CCS) and utilization (CCU) ambitions, spanning public institutions, academic centers, and industrial peers.

- The partnership with the EU Innovation Fund is the most significant financial enabler, providing the $223 million grant that makes the Tarragona offshore storage hub economically viable and signals strong regulatory and political backing for CCS infrastructure in the Iberian Peninsula.

- Repsol’s collaboration with Aramco on a synthetic fuel facility in Bilbao directly links carbon capture with utilization. This partnership combines Repsol’s refining and green hydrogen capabilities with Aramco’s scale to produce low-carbon fuels from captured CO₂, creating a circular business model.

- The R&D collaboration with the Pontifical Catholic University of Rio Grande do Sul (PUCRS) in Brazil provides Repsol with access to cutting-edge research in Direct Air Capture, allowing it to explore next-generation technologies without bearing the full R&D cost and risk internally.

- To execute its projects, Repsol awarded engineering services contracts to Technip Energies for its Ecoplanta Molecular Recycling Solutions project. This partnership secures the specialized technical expertise needed to build complex waste-to-chemical facilities that integrate with carbon capture.

Decarbonization Imperatives Drive New Revenue Models

This chart explains the fundamental driver—the need for new revenue models due to decarbonization—that compels companies like Repsol to form strategic alliances to share risk, technology, and market access.

(Source: MarketsandMarkets)

Table: Repsol’s Key Carbon Capture Partnerships and Alliances in 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Norwegian Cruise Line Holdings | Oct 2025 | Signed the first commercial offtake agreement for methanol produced at the Ecoplanta project. This 8-year agreement validates the market for CCU-derived chemicals and secures a long-term customer. | Repsol |

| Technip Energies | Oct 2025 | Awarded two engineering services contracts for the Ecoplanta Molecular Recycling Solutions project, securing technical expertise for a key circular economy and CCU initiative. | Technip Energies |

| Aramco | Aug 2025 | Collaborating on a synthetic fuel facility in Bilbao to produce low-carbon fuels by combining green hydrogen with captured CO₂, directly applying CCU technology to create value-added products. | MEES |

| PUCRS | Apr 2025 | Launched a joint R&D project to develop and pilot Direct Air Capture technology in Brazil, giving Repsol a low-cost entry point to explore and de-risk an emerging carbon removal technology. | PUCRS |

| EU Innovation Fund | Mar 2025 | Secured a $223 million grant to develop the Tarragona offshore CO₂ storage project. This partnership provides critical, non-dilutive public funding and validates the project’s strategic importance to the EU. | Carbon Herald |

Oil & Gas Dominates CCS Market Applications

This chart explains the strategic importance of CCUS to the oil and gas sector. It provides context for why industry leaders like Repsol are forming key alliances to build a competitive advantage in this critical application area.

(Source: Global Market Insights)

Europe vs. Americas, Repsol’s Geographic CCUS Strategy

Repsol’s 2025 geographic strategy for carbon capture represents a deliberate and strategic diversification away from its historical European focus, establishing new operational beachheads in North and South America to capitalize on distinct regulatory incentives, geological advantages, and technological opportunities. While Spain remains its foundational hub, the company’s moves in 2025 signal a global ambition.

- Prior to 2025, Repsol’s CCUS activities were concentrated in Europe, primarily focused on decarbonizing its industrial complexes in Spain. In 2025, this focus was solidified and scaled with the EU-funded Tarragona project, which aims to create a major sequestration hub for the Iberian Peninsula.

- The announcement of plans to drill a stratigraphic test well in the US Gulf of Mexico marks the most significant geographic expansion in 2025. This move is explicitly designed to leverage the supportive policy environment in the US, particularly the lucrative $85 per ton 45 Q tax credit for geological sequestration.

- By launching a Direct Air Capture pilot in Brazil, Repsol is establishing a foothold in South America. This move is less about immediate commercial scale and more about strategic positioning, allowing the company to explore a different technological pathway in a region with significant renewable energy potential and vast land resources.

Global CCS Market Shows Strong Growth

This chart establishes the context of a strong, growing global market, which serves as the backdrop for the section’s analysis of Repsol’s specific geographic strategy and allocation of resources between Europe and the Americas.

(Source: Global Market Insights)

2 Distinct Paths, Repsol’s CCUS and DAC Technology Maturity

In 2025, Repsol is executing a dual-track technology strategy, concurrently advancing mature point-source capture and storage (CCS) toward commercial scale for immediate industrial decarbonization, while also seeding investments in earlier-stage Direct Air Capture (DAC) and utilization (CCU) technologies to build future capabilities and revenue streams. This portfolio approach balances near-term execution with long-term strategic options.

- Mature CCS for Commercial Scale: The Tarragona hub in Spain and the planned US Gulf Coast project are firmly in the category of mature technology deployment. They leverage established post-combustion capture processes and geological storage techniques, moving them out of the pilot phase (2021-2024) and into large-scale commercial development backed by substantial funding in 2025.

- Commercializing CCU for Value Creation: Repsol’s expertise in refining is being repurposed for CCU. The 250, 000 tonnes-per-year advanced biofuels plant in Cartagena went online in 2025, and a second is under construction in Puertollano. The October 2025 offtake agreement with Norwegian Cruise Line Holdings for CCU-derived methanol is a critical validation point, proving a commercial market exists for these products.

- Seeding Emerging DAC Technology: The launch of the DAC pilot in Brazil in April 2025 marks a strategic investment in a less mature technology. Unlike point-source capture, DAC addresses legacy emissions and offers a different value proposition. This 2025 initiative moves DAC from the lab to a field-testing environment for Repsol, positioning it to be a knowledgeable adopter if the technology becomes economically viable.

Chart Illustrates Technology Adoption Lifecycle

The chart visually represents the concept of technology maturity, which is central to the section’s discussion of the different development stages of conventional CCUS versus emerging Direct Air Capture (DAC) technologies.

(Source: Nature)

SWOT Analysis, Repsol’s CCUS Strengths and Market Risks

Repsol’s 2025 strategic pivot into commercial-scale carbon capture reveals a company successfully leveraging its core industrial integration and public funding capabilities to build a new business line. However, this move also exposes it to significant execution risks in new markets and a reliance on nascent carbon pricing mechanisms and policy support for long-term profitability.

CCUS Projects Historically Underperform Capture Goals

This chart highlights a key market risk and historical challenge (a ‘Threat’ or ‘Weakness’), which is a core component of a SWOT analysis, providing a data-driven perspective on the operational difficulties Repsol faces.

(Source: Clean Air Task Force)

Table: SWOT Analysis for Repsol’s Carbon Capture Initiatives

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Existing integrated industrial assets; in-house R&D and engineering capabilities. | Secured $223 M EU grant; commitment of >35% capex to low-carbon; proven ability to commercialize CCU products with biofuels plants. | The company validated its ability to translate its industrial footprint into an anchor for a major CCS hub and attract significant non-dilutive public funding. |

| Weaknesses | Limited operational experience at commercial CCUS scale; high dependence on legacy fossil fuel revenue. | Major projects (Tarragona, US) are still in pre-FID development stages; high capital intensity requires sustained external funding and policy support. | The weakness shifted from a lack of projects to the significant execution risk associated with a large, geographically diverse, and capital-intensive project pipeline. |

| Opportunities | Growing EU decarbonization mandates and carbon pricing (ETS). | Expansion into the US market to capture 45 Q tax credits; creation of a first-mover storage hub in the Iberian Peninsula; new revenue from CCU products (methanol, synfuels). | The opportunity expanded from European regulatory compliance to global revenue generation, driven by US policy and new markets for low-carbon products. |

| Threats | Uncertainty of long-term carbon prices; public and political opposition to CCS technology. | Competition from larger players (Exxon, Shell) in the US Gulf Coast; potential delays in CO₂ transport infrastructure; lower-cost decarbonization alternatives emerging. | Threats evolved from conceptual political risks to concrete competitive and logistical challenges in the markets where Repsol is now actively developing projects. |

CCUS Market Forecast to Reach $17.75B by 2030

This chart quantifies the significant market growth potential (an ‘Opportunity’ in a SWOT analysis), providing the financial incentive that underpins Repsol’s strategic carbon capture initiatives.

(Source: MarketsandMarkets)

Repsol 2026 Outlook, Tarragona FID and Texas Well Results

The success of Repsol’s carbon capture strategy through 2026 hinges on two critical project-level milestones: reaching a Final Investment Decision (FID) on the EU-backed Tarragona storage hub and obtaining positive geological data from the stratigraphic test well planned off the coast of Texas. These events will determine whether the company’s 2025 ambitions translate into long-term, value-accretive business lines.

- If a positive FID is reached for the Tarragona hub, watch for major contracts to be awarded for offshore platform construction, pipeline laying, and onshore compression facilities. This will be the ultimate signal of commitment, unlocking billions in capital expenditure and solidifying the project’s timeline.

- The results from the Texas well will be a go/no-go decision point for Repsol’s entire US CCS strategy. If the data confirms sufficient and safe storage capacity, watch for announcements of partnerships with local industrial emitters and the filing of Class VI well permits with the EPA.

- If these milestones are achieved, expect Repsol to accelerate the development of a broader funnel of CCS projects in other industrial clusters, as outlined in its 2025 base prospectus. Conversely, negative outcomes could force a strategic reassessment and a pivot back toward its European base or a stronger focus on CCU over CCS.

- Concurrently, the commissioning of the Puertollano biofuels plant in 2026 will be a key indicator of its ability to execute and scale its CCU strategy. Success there, coupled with more offtake agreements like the one with Norwegian Cruise Line Holdings, would prove the commercial viability of its renewable fuels business.

E-fuels Market Forecasts Strong Growth

The chart showing strong growth in the e-fuels market provides the commercial rationale for Repsol’s major CCUS projects like Tarragona, which plans to use captured CO2 to produce e-fuels, justifying the upcoming Final Investment Decision (FID).

(Source: Transparency Market Research)

The questions your competitors are already asking

This report covers one angle of Repsol’s CCUS commercialization strategy. The questions that matter most depend on your work.

- Repsol investments and funding. Is the Tarragona offshore storage project on track for its 2 million tons per year injection target following the €205M EU grant?

- Repsol activities in the US Gulf Coast. Is the CCS hub initiative progressing from a test well to a commercial project to capitalize on the 45Q tax credit?

- Which European industrial emitters are the most likely customers for Repsol’s 54 million-tonne Tarragona CO₂ storage hub?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.