Beyond Wind: How CIP’s Carbon Infrastructure Play De-Risks the 2026 CDR Market

From Enabler to Architect: CIP’s Shift from Renewables to Commercial-Scale Carbon Removal

Copenhagen Infrastructure Partners’ strategy has fundamentally evolved from building foundational renewable energy assets to directly developing and financing commercial-scale carbon removal infrastructure, signaling a critical market transition from speculative pilots to bankable projects. This pivot confirms that the core constraint for scaling carbon management is not solely technology invention, but the availability of experienced project finance and development partners capable of executing capital-intensive facilities. By applying its proven infrastructure model to this nascent sector, CIP is actively creating the market for large-scale carbon dioxide removal (CDR).

- Between 2021 and 2024, CIP’s focus was on enabling the energy transition through massive investments in greenfield renewables, such as the landmark partnership with Ørsted to develop approximately 5.2 GW of offshore wind and raising a €3 billion Energy Transition Fund for Power-to-X (Pt X) projects. During this period, direct investments in carbon capture or removal technologies were absent from its portfolio.

- The strategic shift became clear in 2025 with the formation of Gaia Project Co, a joint venture with Danish waste-to-energy company Vestforbrænding. This is not a pilot but a commercial-scale Bioenergy with Carbon Capture and Storage (BECCS) facility in Denmark designed to capture significant emissions from waste incineration.

- The commercial viability of this new strategy was validated in Q 3 2025 by a landmark offtake agreement with Microsoft to purchase 2.9 million tonnes of CDR credits from the Gaia project. This deal provides the long-term revenue certainty required for project financing.

- CIP’s portfolio now demonstrates a multi-faceted carbon management strategy, including a $500 million joint venture with BKV for point-source carbon capture in North America and a €1.44 billion acquisition of Ørsted’s onshore renewable business to secure the green power essential for these energy-intensive operations.

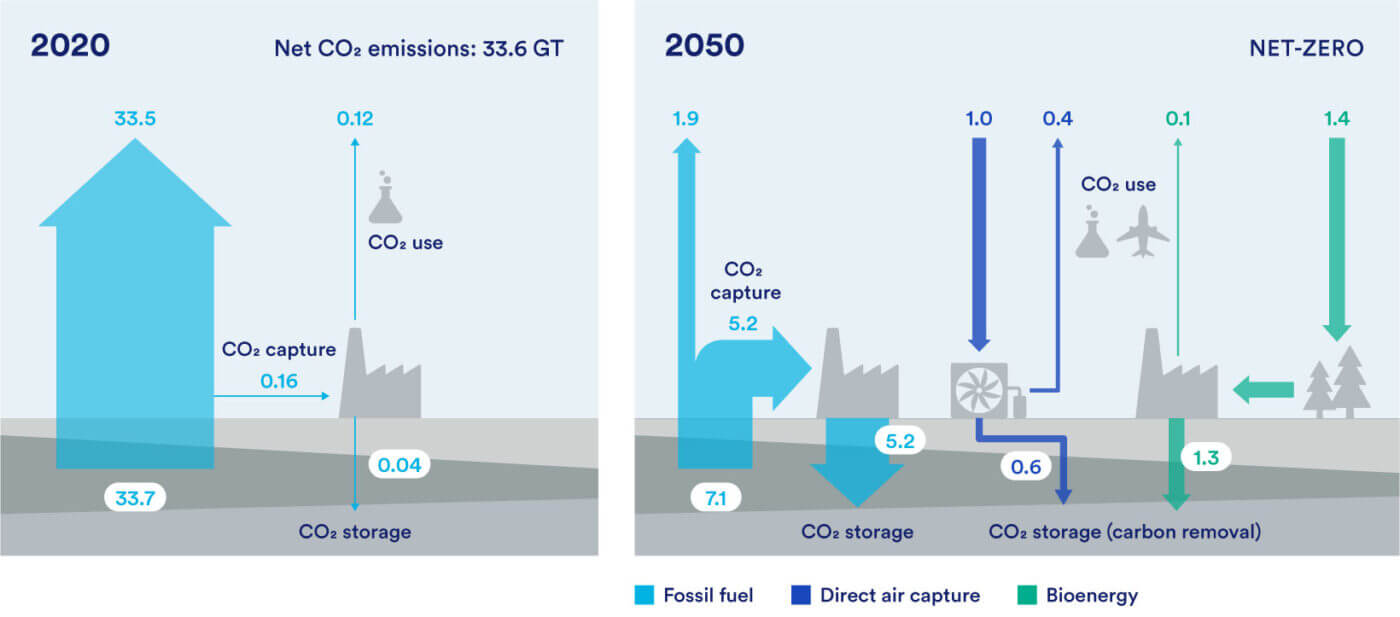

Carbon Capture Must Scale Massively

This chart shows the dramatic increase in carbon capture required to meet 2050 net-zero goals, illustrating the market need driving CIP’s strategic shift to commercial-scale projects.

(Source: Clean Air Task Force)

Investment Strategy Shifts from Broad Funds to Direct Carbon Asset Deployment

CIP’s capital allocation has pivoted from capitalizing broad energy transition funds to making direct, multi-million-dollar commitments into specific carbon capture and removal assets. This change reflects a new phase of the energy transition where investors are moving beyond funding platforms to financing the tangible, complex infrastructure required for deep decarbonization. The establishment of dedicated funds and targeted project-level investments demonstrates a clear intent to build and own the core assets of the emerging carbon management economy.

Trends Driving Carbon Removal Investment

This infographic highlights the key market trends, such as investors backing next-gen technologies, that explain CIP’s pivot from broad funds to direct investments in carbon assets.

(Source: ESG News)

- Prior to 2025, capital deployment was characterized by the creation of large, thematic funds, including the €3 billion CI ETF I, the world’s largest dedicated clean hydrogen fund, and the $3 billion Growth Markets Fund II for renewables in emerging economies.

- In May 2025, the investment approach became more granular with a commitment of up to $500 million for a strategic joint venture with BKV, specifically targeting the development of a pipeline of carbon capture projects in North America.

- The €1.44 billion acquisition of Ørsted’s European onshore business in February 2026 is a critical enabling investment. It secures a vast portfolio of renewable energy generation, providing the clean electricity needed to power future carbon capture and green hydrogen projects sustainably.

- The creation of the Advanced Bioenergy Fund I (ABF I) in June 2025 further institutionalizes this strategy, providing a dedicated vehicle to channel capital directly into BECCS and other advanced bioenergy projects.

Table: Key Copenhagen Infrastructure Partners Investments (2022-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Acquisition of Ørsted’s Onshore Business | 2026-02-03 | €1.44 Billion acquisition of a European onshore renewable portfolio to secure green power for Pt X and carbon management projects. | The Irish Times |

| BKV Joint Venture | 2025-05-08 | Up to $500 Million initial investment commitment for a JV to develop a pipeline of carbon capture projects in North America. | [PDF] Global CCS Institute |

| St. Charles Clean Fuels | 2023-04-19 | Proposed $4.6 billion reduced-carbon ammonia facility in Louisiana, a major Pt X project with integrated carbon capture. | Opportunity Louisiana |

| Energy Transition Fund I (CI ETF I) | 2022-09-07 | Closed at €3 Billion, creating the world’s largest fund dedicated to clean hydrogen and industrial-scale Pt X projects. | Impact Alpha |

Partnership Model Evolves for Carbon Management Project Execution

CIP’s partnership model has matured from forming broad alliances for renewable energy generation to creating highly specific, project-level joint ventures engineered to execute and de-risk complex carbon management facilities. This targeted approach allows CIP to combine its financing and project development expertise with the specialized operational and technological capabilities of its partners, accelerating the path to commercial operation for first-of-a-kind assets in the carbon capture sector.

- The period between 2022-2024 was defined by large-scale renewable energy partnerships, such as the alliance with Ørsted to co-develop 5.2 GW of offshore wind and a consortium with Enagás, Naturgy, and others for green hydrogen production in Spain.

- In February 2025, the model shifted with the creation of Gaia Project Co, a focused JV with waste-management firm Vestforbrænding. This structure isolates project risk and aligns partner incentives for the sole purpose of building and operating the BECCS facility.

- The May 2025 strategic JV with energy producer BKV follows this new model, creating a dedicated entity to pursue carbon capture opportunities in North America by combining CIP’s capital with BKV’s operational footprint.

- This evolution from broad consortia to asset-specific JVs is a clear signal that the carbon management market is moving from planning and road-mapping to project execution and delivery.

Table: Evolution of Copenhagen Infrastructure Partners’ Strategic Alliances

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Statkraft | 2026-01-27 | Joint project for the 500 MW North Irish Sea Array, supporting the broader strategy of powering clean tech with renewable energy. | Off The Record |

| Vestforbrænding (Gaia Project Co) | 2025-02-05 | Joint venture to develop, build, and operate a commercial-scale BECCS facility, with CIP’s fund holding a majority stake. | Carbon Capture Magazine |

| Ørsted | 2022-10-25 | Co-development of approximately 5.2 GW of offshore wind in Denmark to build a massive green energy supply base. | Ørsted |

| Enagás, Naturgy, Fertiberia, Vestas | 2022-02-01 | Consortium to develop a large-scale project for producing green hydrogen and green ammonia in Spain. | Fertiberia |

Geographic Focus Sharpens on Favorable Carbon Markets in Denmark and the US

While maintaining a global renewable energy investment footprint, CIP’s carbon management strategy is initially concentrated in regions with a combination of strong regulatory support, available infrastructure, and accessible offtake markets, primarily Denmark and the United States. This targeted geographic approach minimizes policy risk and maximizes the potential for successful execution of its first wave of large-scale carbon capture and removal projects.

European Carbon Capture Project Map

This map details the location and scale of carbon capture projects across Europe, visualizing the established infrastructure in regions like Denmark that CIP is strategically targeting.

(Source: Clean Air Task Force)

- Between 2021 and 2024, CIP’s greenfield projects were globally dispersed, with major initiatives in Spain (1 GW Teruel Wind Farms), India ($3 billion Ampin partnership), Chile (HNH Green Hydrogen Project), and the Philippines.

- From 2025, the firm’s flagship carbon removal project, Gaia Project Co, is strategically located in Glostrup, Denmark. This location leverages an existing waste-to-energy plant and a supportive national environment for CO 2 storage.

- In North America, the focus is squarely on the US Gulf Coast, a region with favorable geology for carbon storage and established industrial infrastructure. This is evidenced by the proposed St. Charles Clean Fuels project in Louisiana and the carbon capture joint venture with BKV.

Technology Strategy Prioritizes Mature, Bankable Solutions over Early-Stage DAC

CIP has deliberately bypassed the technology risk associated with early-stage Direct Air Capture (DAC), instead focusing its carbon management strategy on commercially mature or adjacent technologies like BECCS and point-source industrial capture. This approach allows the firm to immediately apply its core competency in financing and delivering complex infrastructure projects, making a near-term impact on decarbonization without exposure to the uncertainties of unproven technologies.

Carbon Removal Costs Forecasted to Fall

By showing the high current cost of DAC compared to other methods, this chart explains CIP’s strategy of prioritizing more mature, bankable technologies for near-term projects.

(Source: Carbon Removal Updates – Substack)

- Before 2025, CIP’s technology focus was on scaling proven renewables, including onshore wind, solar PV, and battery storage, as seen in its acquisition of a majority stake in Elgin Energy.

- The choice of BECCS for the Gaia project is strategic. It integrates carbon capture with an existing, operational waste-to-energy plant, significantly reducing the greenfield development risk and complexity associated with a standalone DAC facility.

- Similarly, its involvement in the St. Charles Clean Fuels project focuses on integrating proven carbon capture technology with large-scale hydrogen and ammonia production, a more mature industrial application than DAC.

- CIP’s model is not one of technology innovation but of technology deployment at scale. The firm’s value proposition is its ability to structure and finance bankable projects using existing, capital-intensive solutions that are ready for commercial deployment.

SWOT Analysis: CIP’s 2026 Position in the Carbon Management Market

The analysis shows CIP has successfully leveraged its financial strength and project execution track record to become a formidable player in the carbon management sector. By securing a major corporate offtake for its first large CDR project, it has validated its model of de-risking and commercializing nascent clean energy infrastructure, transforming a potential weakness into a core strength.

- Strengths: Proven ability to finance and deliver multi-billion dollar infrastructure, now validated in the CDR market with the Gaia project and Microsoft deal.

- Weaknesses: The carbon management portfolio is still nascent and its success is heavily concentrated on a few flagship projects, creating significant execution risk.

- Opportunities: First-mover advantage in financing large-scale BECCS and meeting massive corporate demand for durable, high-quality carbon removal credits.

- Threats: Competition from other CDR pathways and developers, alongside regulatory uncertainty surrounding long-term carbon storage and monitoring protocols.

Table: SWOT Analysis for Copenhagen Infrastructure Partners’ Carbon Management Strategy

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Expertise in large-scale renewable energy project finance and development (e.g., Ørsted partnership). Strong fundraising capability (€3 B Energy Transition Fund). | Demonstrated ability to structure and finance commercial-scale CDR projects. Secured a landmark 2.9 million tonne CDR offtake agreement with Microsoft. | The firm validated that its core competency in de-risking and financing complex infrastructure is directly transferable to the nascent carbon removal market. |

| Weaknesses | No direct exposure to the rapidly growing carbon removal and DAC markets. Portfolio was entirely focused on renewable power generation and Pt X. | Carbon management portfolio is still in its early stages and highly concentrated. Success hinges on the execution of a few key projects like Gaia. | The firm moved from having no exposure to having a highly concentrated exposure, shifting the risk profile from market absence to project execution. |

| Opportunities | Growth of the green hydrogen and Power-to-X markets, driven by demand from hard-to-abate sectors. Geographic expansion in emerging markets. | Massive and growing corporate demand for durable, high-integrity CDR. First-mover advantage in financing and delivering large-scale BECCS projects in Europe. | CIP successfully capitalized on corporate net-zero demand to create a bankable revenue stream for a CDR project, a model it can now replicate. |

| Threats | Intense competition in the mature renewable energy sector. Grid connection delays and permitting challenges for large-scale wind and solar. | Project execution risks on first-of-a-kind large BECCS facilities. Competition from other CDR pathways (e.g., Vaulted Deep’s larger 4.9 M tonne deal with Microsoft). Evolving regulations for CDR. | Threats have shifted from conventional project development hurdles in renewables to the more complex technology, market, and policy risks of the new carbon management sector. |

Scenario Modeling for 2026: Execution Success Will Trigger Rapid Portfolio Scaling

If Copenhagen Infrastructure Partners successfully executes the Gaia project on time and budget while securing a Final Investment Decision for its US carbon management ventures, watch for a rapid scaling of its carbon portfolio, likely through new, specialized fund structures. The current strategy has established a powerful, replicable template for turning capital-intensive decarbonization projects into bankable assets, and successful execution of these initial projects will be the primary catalyst for attracting further institutional capital.

Carbon Removal Market Shows Explosive Growth

The explosive growth in purchased carbon removal volumes, particularly in BioCCS, provides the market context for the rapid portfolio scaling CIP could achieve with successful project execution.

(Source: Carbon Removal Updates – Substack)

- The most critical signal to monitor in the near term is the Final Investment Decision (FID) for the St. Charles Clean Fuels Plant in Louisiana and the first major capital deployments from the $500 million BKV joint venture. Positive movement here would confirm momentum in the US market.

- Successful completion and operation of the Gaia BECCS project will serve as the definitive proof-of-concept for CIP’s model. This would likely trigger follow-on investments in similar waste-to-energy or biomass-based carbon removal projects across Europe.

- Growth in the broader durable CDR market, particularly rising prices and transaction volumes as tracked by market platforms, will directly enhance the financial projections for CIP’s assets and increase the attractiveness of its dedicated funds like the Advanced Bioenergy Fund I.

- Conversely, significant delays, cost overruns, or operational challenges at these flagship projects could dampen investor appetite and slow the firm’s expansion in the carbon management sector, forcing a potential retreat to its core renewables strategy.

Frequently Asked Questions

Why is Copenhagen Infrastructure Partners’ (CIP) move into carbon removal considered significant for the 2026 market?

CIP’s move is significant because it signals a market transition from speculative pilot projects to bankable, commercial-scale carbon dioxide removal (CDR). By applying its proven model for financing and developing large infrastructure, CIP is de-risking the sector and demonstrating that the main constraint to scaling CDR is not just technology invention, but the availability of experienced project finance partners.

What is the Gaia Project Co, and why is the Microsoft deal important for it?

Gaia Project Co is a joint venture between CIP and the Danish waste-to-energy company Vestforbrænding to build a commercial-scale Bioenergy with Carbon Capture and Storage (BECCS) facility. The landmark offtake agreement with Microsoft to purchase 2.9 million tonnes of CDR credits is critically important because it provides the long-term revenue certainty required to secure project financing for this first-of-a-kind facility.

How has CIP’s investment strategy evolved from 2024 to 2026?

Prior to 2025, CIP focused on creating large, thematic funds for renewable energy, like its €3 billion Energy Transition Fund. From 2025 onwards, its strategy pivoted to making direct, multi-million-dollar commitments into specific carbon capture and removal assets. This is shown by the $500 million joint venture with BKV and the creation of the dedicated Advanced Bioenergy Fund I (ABF I).

What type of carbon removal technology is CIP focusing on, and why?

CIP is focusing on commercially mature technologies like Bioenergy with Carbon Capture and Storage (BECCS) and point-source industrial capture. It is deliberately avoiding the technology risk associated with early-stage Direct Air Capture (DAC). This strategy allows the firm to leverage its core competency in financing and delivering complex, capital-intensive infrastructure projects that are ready for immediate commercial deployment.

According to the SWOT analysis, what is the biggest weakness or threat to CIP’s new carbon management strategy?

The primary weakness is that CIP’s carbon management portfolio is still in its early stages and highly concentrated, meaning its success hinges on the execution of a few key flagship projects like Gaia. This creates significant execution risk. Threats also include competition from other CDR pathways and developers, as well as evolving regulations for long-term carbon storage and monitoring.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.