CDR Scaling 2026: How Advance Market Commitments Unlock Carbon Removal Projects

From Pilots to Projects: How Offtake Agreements Are Scaling Carbon Removal

The Carbon Dioxide Removal (CDR) industry shifted from early-stage, speculative pilots before 2025 to bankable, large-scale project execution driven by structured offtake agreements. This transition is defined by the move from technology validation to commercial de-risking, where advance market commitments (AMCs) provide the revenue certainty required to unlock significant private capital and build first-of-a-kind facilities. This model provides a clear pathway for capital-intensive hardware to overcome the initial commercialization valley.

- Before 2025, the AMC model was in its infancy. For example, a December 2022 purchase by the Frontier coalition, which included Arbor, was part of a broader, catalytic $11 million buy across multiple companies to stimulate the market. In contrast, by July 2025, the model matured into a targeted, project-specific financing tool, with Frontier committing $41 million directly to Arbor for 116, 000 tons of removal, explicitly to enable its first commercial plant.

- The direct result of this de-risking was a major influx of private capital. After securing the Frontier deal, Arbor successfully raised a $55 million Series A funding round in November 2025. This demonstrates that guaranteed future revenue from offtakes makes CDR projects attractive to venture capital firms like Lowercarbon Capital and Voyager Ventures.

- The buyer base for CDR has also expanded and solidified. While the initial push came from coordinated efforts like Frontier, by November 2025, individual corporate leaders began making significant direct purchases. Google’s agreement to buy 30, 100 tonnes of carbon removal from Arbor signals a broadening market where single corporations are willing to underwrite new projects to meet their climate goals.

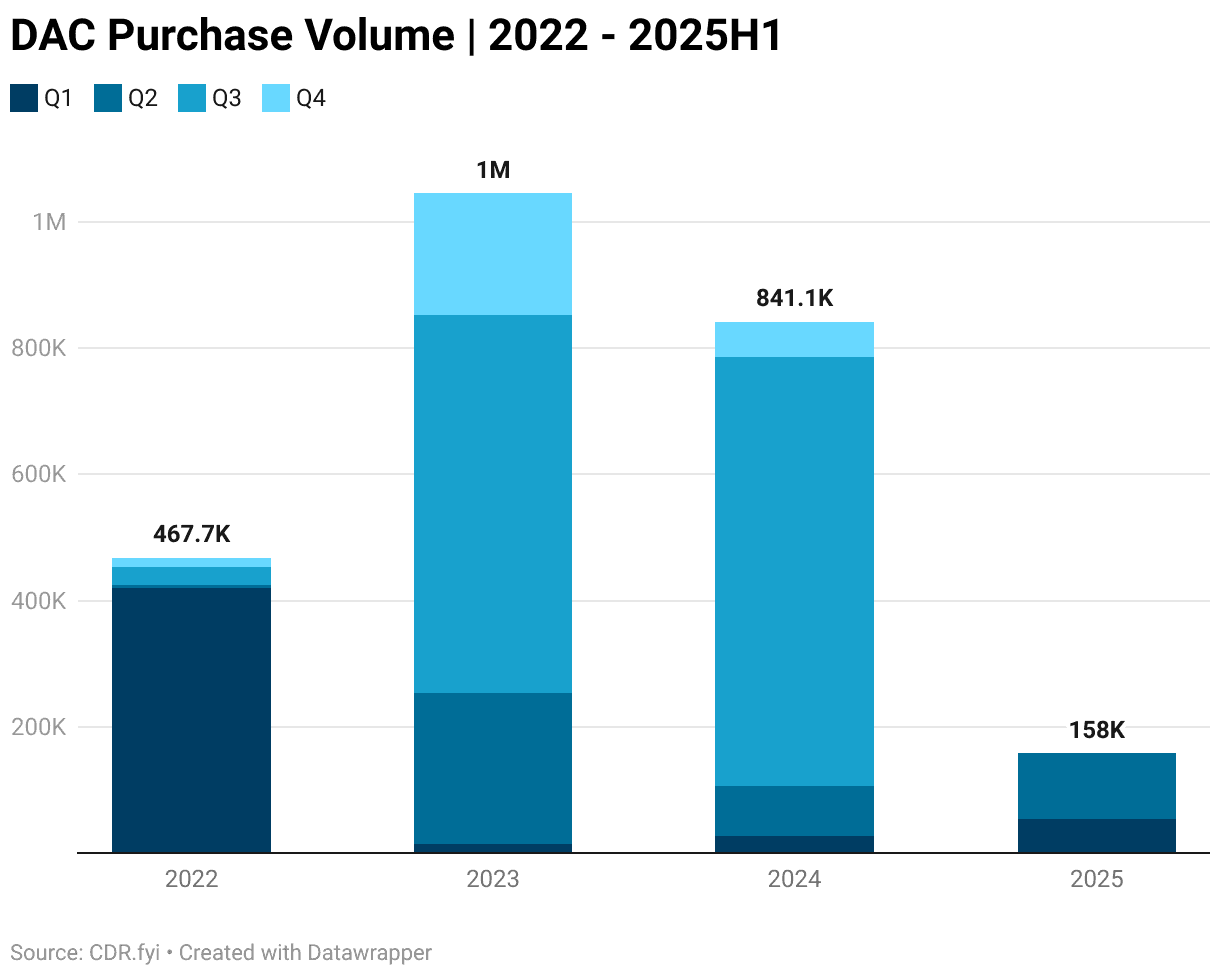

Advance Purchases Signaled CDR Market Shift

This chart shows the volume of advance purchase commitments leading up to 2025, directly illustrating the ‘advance market commitments’ that the section credits with enabling the industry’s shift from pilots to bankable projects.

(Source: CDR.fyi)

Investment Analysis: Offtake Agreements Convert to Equity in 2025

Carbon removal investment evolved from catalytic, demand-side purchases before 2025 to substantial, direct equity injections in 2025, validating the commercial viability of projects with pre-sold capacity. Before this shift, funding was primarily driven by advance purchases that acted as a market signal. Now, these signals have been converted into hard financial commitments from institutional investors, confirming the bankability of the underlying business models.

- In the 2022-2024 period, investment was characterized by demand-side mechanisms like the U.S. Department of Energy’s CDR Purchase Pilot Prize, for which Arbor was a semifinalist in May 2024. These initiatives functioned as market-making investments, promising future revenue rather than providing upfront capital.

- The turning point occurred in Q 3-Q 4 2025 with major equity rounds tied directly to project development. Arbor’s $55 million Series A in November 2025 was predicated on its secured offtake agreements. This followed a similar trend seen with DAC competitor Climeworks AG, which raised $162 million in October 2025 to fund its own large-scale projects.

- This trend indicates that investors now see a clear revenue path for CDR companies. The ability to show multi-year, multi-million-dollar offtake contracts, like Arbor’s $41 million deal with Frontier, has become the key prerequisite for attracting significant growth equity for facility construction.

Table: Key Carbon Removal Investments and Financial Commitments (2025)

| Company | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Arbor Energy | Nov 10, 2025 | Raised a $55, 000, 000 Series A round led by Lowercarbon Capital and Voyager Ventures to fund its first commercial BECCS facility, enabled by prior offtake agreements. | CDR Monthly Recap – October 2025 |

| Climeworks AG | Oct 2, 2025 | Secured a $162, 000, 000 equity investment from Big Point Holding and Partners Group, signaling strong investor appetite for DAC leaders with a clear project pipeline. | Q 3 2025 Carbon Offtakes Analysis |

| Arbor / Frontier | Jul 9, 2025 | Secured a $41 million advance market commitment from Frontier’s buyers for 116, 000 tons of removal, serving as a bankable contract to unlock project financing. | Carbon Capture Magazine |

Partnership Strategy: Securing Commercial Offtakes for Arbor’s BECCS Projects

Strategic partnerships in the CDR sector have matured from foundational technology validation alliances to large-scale commercial offtakes that directly finance first-of-a-kind facilities. Before 2025, partnerships were focused on project development and technology demonstration. By 2025, the primary goal of partnerships shifted to securing bankable, long-term revenue streams to de-risk capital-intensive construction and prove market demand.

Offtake Agreements Link CDR Buyers and Suppliers

This Sankey diagram visualizes the flow of commercial offtake agreements in 2025, perfectly illustrating the strategic partnerships between buyers and CDR technology providers discussed in the section.

(Source: AlliedOffsets)

- An early example of a development partnership was Arbor’s collaboration with Magnolia Renewable Fuels LLC, noted in January 2024, to develop the proposed Port Allen Renewable Gasoline Refinery. This represented an alliance to combine operational and technological capabilities for a specific project.

- The 2025 partnerships with Frontier and Google represent a new class of purely commercial alliances. These are not development partnerships but offtake agreements that provide guaranteed revenue certainty, which is critical for securing project financing.

- The Frontier partnership is the most significant evolution. It acts as a demand aggregator, pooling purchasing power from corporations like Stripe, Alphabet, Shopify, and Mc Kinsey to create a single, substantial contract ($41 million) large enough to catalyze a commercial-scale project.

Table: Key Commercial Partnerships for Carbon Removal (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Nov 6, 2025 | Offtake agreement for Arbor to remove 30, 100 tonnes of CO₂, diversifying the customer base for Arbor’s first commercial facility and adding to its secured revenue pipeline. | 2025 Q 3 Durable CDR Market Update | |

| Frontier | Jul 9, 2025 | Facilitated a $41 million deal for buyers to purchase 116, 000 tons of CO₂ removal from Arbor between 2028-2030. This AMC is explicitly designed to enable the financing and launch of Arbor’s first commercial plant in Louisiana. | Carbon Capture Magazine |

Geographic Focus: Louisiana Emerges as the Hub for Arbor’s Carbon Removal Projects

By 2025, Louisiana has emerged as a central hub for large-scale, commercially-backed carbon removal projects, supplanting earlier, more geographically dispersed and speculative activities. The state’s favorable geology for carbon sequestration, established industrial infrastructure, and supportive policy environment have concentrated major investments and project commitments, making it the focal point for the next stage of CDR deployment in the United States.

USA Leads in Carbon Removal Capacity

This chart highlights the United States’ leadership in announced DAC project capacity, providing the national context for the section’s specific focus on Louisiana as a central hub for CDR deployment.

(Source: Internationale Politik Quarterly)

- In the period between 2021 and 2024, project locations were more tentative. For instance, Arbor’s proposed project with Magnolia Renewable Fuels was sited in Port Allen, Louisiana, but the broader CDR landscape featured pilot projects in various locations without major capital commitments.

- The year 2025 marked a definitive consolidation of commercial efforts in Louisiana. Arbor’s major offtake agreements with Frontier and Google are explicitly tied to a new, first-of-a-kind commercial facility planned for Lake Charles, Louisiana.

- While other potential sites exist, such as the “Arbor Biomass Gasification Facility” listed in a California Air Resources Board filing for Placer, CA, the financial and commercial gravity has clearly centered on Louisiana. This regional focus is reinforced by the presence of other major CDR initiatives, like Climeworks’ Project Cypress, which is also located in the state.

Technology Maturity: Arbor’s BECCS Moves From Concept to Commercial Validation

Arbor’s Bioenergy with Carbon Capture and Storage (BECCS) technology progressed from a novel concept leveraging aerospace principles before 2025 to a commercially validated system with defined performance metrics and financial backing for its first large-scale deployment. This maturation is evidenced by the company’s ability to attract multi-million dollar pre-purchase agreements based on specific, verifiable performance claims, moving the technology beyond the conceptual stage and into the realm of bankable engineering.

CDR Market Growth Driven by Maturing Tech

This forecast shows the rapid growth of the overall Carbon Dioxide Removal (CDR) market, reflecting the financial success that comes from technologies like BECCS achieving commercial validation as described in the section.

(Source: Market Report Analytics)

- In the 2021-2024 period, Arbor’s technology was described more conceptually, such as applying “principles from modern rocket engine technology” to create a low-cost system. While it gained recognition as a semifinalist in the DOE’s CDR prize, specific performance data was not public.

- By 2025, the technology became clearly defined as an integrated system combining biomass gasification, oxycombustion, and carbon capture. The company attached hard performance metrics to this system, claiming a CO₂ capture rate exceeding 99% and a 30% improvement in biomass-to-electricity conversion efficiency.

- The technology’s maturity was ultimately validated by the market. Securing a $41 million offtake agreement from Frontier and a significant deal with Google demonstrates that sophisticated buyers have accepted the technology’s readiness and are confident in its ability to deliver verifiable carbon removal at scale starting in 2028.

SWOT Analysis: De-Risking Arbor’s BECCS Model for Commercial Scale

Arbor’s strategic position was significantly strengthened between 2021 and 2025 by converting the conceptual strength of its BECCS model into tangible financial and commercial validation. This progress successfully mitigated early-stage financial risks but shifted the primary challenge from securing funding to executing a complex, first-of-a-kind industrial project.

- The company’s core strength evolved from a theoretical dual-revenue model to a technically specified system with proven high-efficiency metrics.

- The primary weakness transitioned from a lack of offtake certainty to the inherent operational complexity of deploying a novel, integrated technology at commercial scale.

- Opportunities expanded from participating in a nascent market to leading a defined BECCS segment, backed by blue-chip customers.

- Threats shifted from the existential risk of failing to secure funding to the execution risk of project delays and potential biomass supply chain constraints.

Table: SWOT Analysis for Arbor’s BECCS Initiatives

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Conceptual dual-revenue model (energy + carbon credits) and novel engineering approach (rocket technology). | High-efficiency BECCS technology with validated metrics (>99% capture, >30% energy efficiency gain). Secured Series A and major offtakes. | The conceptual model was validated with specific performance claims and attracted significant financial and commercial backing, proving its economic proposition. |

| Weaknesses | High capital requirement with no secured offtake revenue. Unproven technology at commercial scale. | High operational complexity of integrating gasification, oxycombustion, and capture. Dependence on a single flagship project. | The financial risk was substantially reduced through offtakes and funding. The primary weakness is now execution and operational risk, not financial viability. |

| Opportunities | Participate in emerging CDR markets and DOE prize programs. Differentiate from energy-intensive DAC. | Lead the BECCS market segment. Leverage secured demand from Frontier and Google to build out a project pipeline. | The opportunity matured from market participation to market leadership. Secured demand provides a clear path to scale that was previously theoretical. |

| Threats | Failure to secure catalytic funding or first customers. Competition from more established DAC players. | Execution risk on the first commercial plant in Louisiana (timeline, budget). Potential biomass supply chain vulnerabilities at scale. | The primary threat shifted from an inability to start (existential risk) to an inability to deliver on promises (operational and reputational risk). |

2026 Outlook: Execution is the Critical Signal for the CDR Market

The single most critical factor for the CDR market in 2026 is the successful physical deployment of first-of-a-kind commercial facilities like Arbor’s Louisiana plant. If this execution succeeds, it will validate the AMC model as a bankable offtake structure, likely triggering a new wave of project financing and corporate purchases for similar capital-intensive climate technologies. Failure or significant delays, however, would signal that the gap between financial commitments and operational reality remains a major industry hurdle.

CDR Market Projected for Steady Growth

This chart projects the long-term growth of the carbon removal market through 2034, visualizing the ‘new wave of project financing’ and future market trajectory discussed in this outlook section.

(Source: Precedence Research)

- Watch this signal: The groundbreaking and construction progress of the Lake Charles, Louisiana, BECCS facility is the key milestone. Adherence to the project timeline is paramount, as it is required to meet the 2028 delivery start date for the Frontier agreement. Any delays would indicate challenges in translating offtake agreements into physical assets.

- If this happens: Successful construction progress will likely lead to the announcement of a larger Series B or a dedicated project finance vehicle to cover the full capital expenditure of the plant. The ability to secure this next round of funding will confirm investor confidence in Arbor’s execution capabilities.

- This could be happening: Monitor for additional offtake announcements. With foundational customers like Frontier and Google secured, Arbor will likely focus on selling the remaining capacity of its first plant. New agreements would signal broadening market confidence and build a demand pipeline for future facilities.

Frequently Asked Questions

What is an Advance Market Commitment (AMC) and how is it helping the carbon removal industry?

An Advance Market Commitment (AMC) is a structured offtake agreement where a buyer or coalition of buyers commits to purchasing a product—in this case, carbon removal—in the future at a set price. According to the analysis, AMCs are crucial for the carbon removal industry because they provide guaranteed future revenue. This revenue certainty de-risks projects for investors, making it possible for companies like Arbor to secure the private capital needed to build their first large-scale commercial facilities, as seen with the $41 million Frontier deal.

What were Arbor’s three most significant achievements in 2025?

In 2025, Arbor achieved several critical milestones. The three most significant were: 1) Securing a $41 million advance market commitment from the Frontier coalition in July to enable its first commercial plant. 2) Signing another major offtake agreement with Google in November for 30,100 tonnes of removal. 3) Raising a $55 million Series A funding round in November, which was made possible by the previously secured offtake agreements.

How did the role of investors in carbon removal change in 2025?

Before 2025, investment was primarily driven by catalytic, demand-side signals like prizes or small-scale purchases designed to stimulate the market. In 2025, a significant shift occurred where these market signals converted into direct, substantial equity investments. Investors, seeing that companies like Arbor and Climeworks had secured multi-million-dollar offtake contracts (pre-sold capacity), became confident in their bankability, leading to major funding rounds to finance the construction of commercial facilities.

What technology does Arbor use and why is it considered commercially validated?

Arbor uses a Bioenergy with Carbon Capture and Storage (BECCS) system that integrates biomass gasification, oxycombustion, and carbon capture. The technology is considered commercially validated because it moved beyond the conceptual stage to having specific performance metrics (e.g., >99% CO₂ capture rate). Most importantly, its maturity was confirmed by the market when sophisticated buyers like the Frontier coalition and Google signed large, multi-million-dollar offtake agreements, demonstrating their confidence that Arbor’s technology can deliver verifiable carbon removal at scale.

Why is Louisiana identified as a key hub for Arbor’s carbon removal projects?

Louisiana has emerged as a key hub for carbon removal projects due to a combination of factors. The article points to the state’s favorable geology for permanently storing captured CO₂, its established industrial infrastructure which can support large-scale construction, and a supportive policy environment. This concentration of advantages has attracted major commercial projects, including Arbor’s first BECCS facility in Lake Charles, making it a focal point for investment and deployment.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.