Critical Minerals Supply Risk, $5.4 T Investment Gap, 70% Chinese Processing, and 2 Major Policy Shifts (2021 to 2026)

Critical Minerals Supply Chain Risks, $5.4 T Gap & Geopolitical Concentration

The estimated $5.4 trillion investment gap in critical minerals is not a simple market failure but a structural crisis driven by extreme geopolitical concentration and volatile policy, which makes new mining projects unbankable despite soaring demand. The period between 2021 and 2024 was characterized by a growing awareness of this problem, with reports from the IEA and others highlighting China’s market dominance and the long lead times for new mines. The period from 2025 to today has validated these concerns, showing that private capital alone cannot solve the problem as Western governments shift from purely market-based incentives to direct, albeit sometimes contradictory, interventions.

- The core of the supply risk lies in processing, where China refines 60-70% of the world’s lithium and cobalt and over 90% of rare earth elements (REEs), a position of dominance established prior to 2024. This allows Beijing to influence global markets through subsidies and export controls, creating prohibitive risk for private investors considering projects in other nations.

- The market’s failure to self-correct prompted government action, but this has created new risks. The Inflation Reduction Act (IRA) of 2022 introduced permanent production tax credits, but the One Big Beautiful Bill Act (OBBBA), enacted in July 2025, scheduled these same credits for a phase-out beginning in 2031. This policy reversal undermines the long-term revenue certainty required for 10-20 year mining investments.

- In response to this volatility and concentration, governments are now acting as direct market participants. The U.S. launched Project Vault in February 2026, a new $12 billion strategic stockpile designed to act as a stable source of demand for domestic and allied producers, signaling a strategic shift away from relying solely on private offtake agreements.

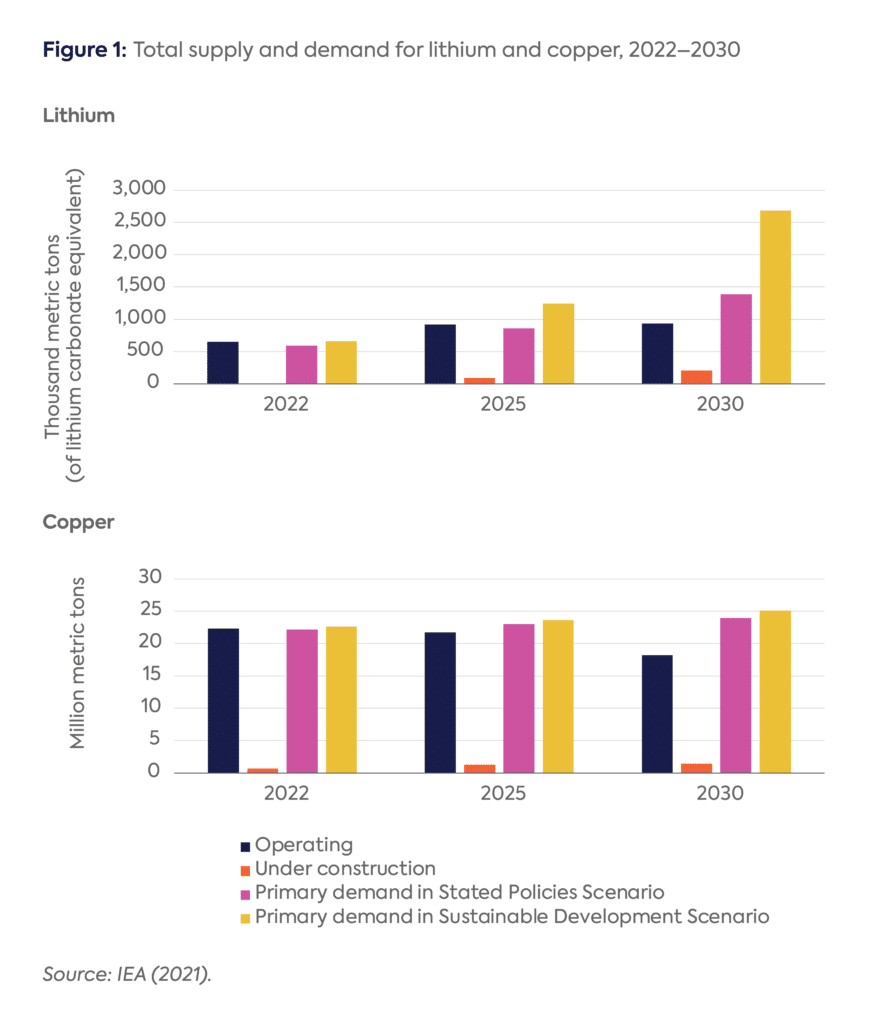

Major Lithium and Copper Supply Gaps Projected

This chart provides a concrete visualization of the supply chain risks and gaps mentioned in the section heading. The projected shortfalls in key minerals like lithium and copper directly illustrate the scale of the challenge and a primary driver of the ‘$5.4 T gap’.

(Source: Center on Global Energy Policy – Columbia University)

$12 B Project Vault, US Government Direct Investment in Critical Minerals

Direct government financial intervention has become a primary tool to de-risk the mining investment climate, marking a significant strategic shift from the demand-side incentives that defined policy between 2022 and 2024. While policies like the IRA aimed to stimulate demand for ethically sourced minerals, they failed to address the fundamental capital risk of bringing new supply online, a gap that newer, more direct funding mechanisms now seek to close, albeit with mixed success.

- The most significant recent intervention is the $12 billion Project Vault initiative, announced by the U.S. government in February 2026. Unlike defense stockpiles, this fund is designed to act as a buyer of last resort, creating guaranteed offtake for new producers and de-risking projects enough to attract private financing.

- This direct-support model contrasts sharply with the policy whiplash created by the One Big Beautiful Bill Act (OBBBA) in July 2025. By scheduling a phase-out of the Section 45 X production credits that were a cornerstone of the IRA, the act eroded the long-term financial certainty investors require, effectively increasing risk and making direct government support more necessary.

- Other governments are also deploying capital. Canada’s Critical Minerals Strategy committed nearly $4 billion to expedite project development, while the multi-national Minerals Security Partnership (MSP) aims to channel public and private investment into a portfolio of globally diverse projects.

EVs Dramatically Increase Critical Mineral Demand

This chart explains the ‘why’ behind the significant US government investment. The dramatic increase in mineral demand driven by electric vehicles, a key policy area, provides the strategic rationale for committing $12 billion to secure domestic supply chains.

(Source: Mining.com)

Table: Key Government Interventions in Critical Minerals

| Policy / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Project Vault | Feb 2026 | A new $12 billion strategic stockpile created by the U.S. government to provide a stable source of demand for new, allied critical mineral producers and de-risk project financing. | Fastmarkets |

| One Big Beautiful Bill Act (OBBBA) | Jul 2025 | U.S. legislation that introduced a phase-out for Section 45 X tax credits beginning in 2031, reversing a key permanent incentive from the IRA and creating long-term uncertainty for investors. | Bloomberg Tax |

| Inflation Reduction Act (IRA) | Aug 2022 | U.S. act providing significant demand-side incentives, including the Section 45 X Advanced Manufacturing Production Tax Credit, which offered a 10% subsidy for critical mineral production. | [PDF] OIA |

Critical Minerals Offtake Agreements, 2 Key JVs and 1 Stockpile Initiative (2025 to 2026)

To counteract extreme price volatility and policy risk, miners, processors, and end-users are increasingly forming strategic joint ventures and long-term offtake agreements to secure financing and guarantee supply. This trend accelerated in 2025 and 2026 as it became clear that relying on spot market prices for projects with decade-plus development timelines is not a viable strategy for closing the supply gap.

- In March 2026, Lithium Americas secured a 20-year offtake agreement as part of a joint venture structure to complete financing for its Thacker Pass project. This model, which locks in a future buyer, provides the revenue certainty needed to obtain project debt.

- In January 2026, Critical Metals Corp. (CRML) executed a term sheet for a 50/50 joint venture with Arabian New Energy for a rare earth processing facility. The deal included long-term offtake rights for 25% of the Tanbreez Project’s REE concentrate production, demonstrating a strategy to link upstream supply directly with downstream industrial partners in new regions like Saudi Arabia.

- These private agreements are complemented by public initiatives like the U.S. Export-Import Bank (EXIM), which finances international projects on the condition that long-term offtake contracts ensure the output flows to U.S.-allied supply chains, effectively using public finance to secure private supply commitments.

Technical Hurdles Limit Critical Mineral Substitution

This chart provides the underlying context for the actions described in the section. The difficulty of substituting critical minerals, as shown in the chart, forces companies and governments to secure supply through direct means like offtake agreements, joint ventures, and strategic stockpiling.

(Source: Center on Global Energy Policy – Columbia University)

Table: Recent Strategic Alliances in Critical Minerals

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Lithium Americas | Mar 2026 | A 20-year offtake agreement was announced as part of a joint venture to complete the financing for the Thacker Pass lithium project, anchoring future revenue to make the project bankable. | [PDF] Lithium Americas |

| Critical Metals Corp. & Arabian New Energy | Jan 2026 | Executed a term sheet for a 50/50 JV to build a REE processing facility, including long-term offtake rights for 25% of production to a Saudi Arabian industrial partner. | Critical Metals Corp. |

China vs. West, Critical Minerals Geographic Concentration

The global geography of critical minerals is defined by a stark imbalance, with China controlling the midstream processing segment while Western nations and their allies attempt to build a parallel but currently much smaller supply chain. While resource extraction is concentrated in a few nations like the DRC (cobalt) and Indonesia (nickel), it is China’s strategic decision to dominate the complex, high-value refining stage that presents the most significant bottleneck and investment risk for the rest of the world.

- China’s processing dominance is near-total in some areas, accounting for 92% of global REE refining, 75% of cobalt, and 65% of lithium as of 2023-2024. This gives Beijing immense leverage over the global energy transition and deters private investment in competing facilities that cannot match China’s state-subsidized scale and pricing.

- In response, a bloc of Western-aligned nations is attempting to build alternative supply chains. The U.S. is using the IRA to incentivize sourcing from free-trade partners, and key players like MP Materials are receiving government support to build out domestic processing capacity.

- The Minerals Security Partnership (MSP), a coalition of 14 countries and the EU, represents a diplomatic effort to coordinate investment in “friendly” jurisdictions. However, its financial commitments and project pipeline remain a fraction of what is needed to meaningfully challenge China’s established infrastructure.

- New geopolitical axes are forming, such as the January 2026 JV between U.S.-based CRML and a Saudi Arabian conglomerate for REE processing. This signals a strategy of diversifying away from China by building capacity in capital-rich third-party nations.

China’s Dominance in Critical Mineral Production Visualized

The chart is a direct and powerful illustration of the section’s topic. It visually quantifies China’s dominant role in the production of critical minerals, which is the central theme of the ‘China vs. West’ geopolitical dynamic.

(Source: LinkedIn)

Mining Project Timelines, 16.5 Year Lead Times vs. Urgent Demand

The fundamental maturity issue facing the critical minerals supply chain is not a lack of technology but an extreme misalignment between the slow, capital-intensive reality of mine development and the rapid, exponential growth in demand. The “technology” of finding and digging minerals out of the ground is well-established, but its deployment is crippled by multi-decade timelines and administrative paralysis, a problem that no near-term technological innovation can solve.

- It takes an average of 16.5 years to move a mining project from discovery to first production. Some estimates place the capital investment cycle at 10-20 years. This means mines needed to meet 2035 demand targets should have started development years ago, but the investment was not made due to market and policy risks.

- Permitting issues are the single largest cause of project delays. The protracted timelines for environmental and social reviews in Western jurisdictions like the U.S. and Canada can add years or even decades to a project, inflating risk and deterring investment.

- The problem is compounded by declining resource quality. The average grade of copper ore, for instance, has fallen by nearly 30% in the last decade. Lower grades require more ore to be mined and processed for the same amount of metal, increasing CAPEX, OPEX, and the environmental footprint, which in turn fuels further ESG-based opposition and delays.

- New demand vectors, such as the need for copper in the AI-driven data center boom, are adding further pressure to a supply pipeline that is structurally incapable of responding quickly.

US and Canada Face Decades-Long Mine Development Timelines

The chart and section headings are in perfect alignment. The chart provides specific data on the ‘decades-long’ timelines for mine development in North America, directly supporting the section’s focus on the ‘16.5 year lead times’.

(Source: The Oregon Group)

SWOT Analysis: Critical Minerals Investment Climate and Supply Risks

The investment climate for critical minerals is defined by a deep contradiction: while unprecedented demand and high potential profitability create powerful strengths and opportunities, they are largely neutralized by structural weaknesses and existential threats from geopolitics and policy instability. The period from 2025 onward has validated that without strategic, state-level de-risking, the threats and weaknesses are significant enough to prevent the $5.4 trillion investment gap from closing.

Critical Mineral Prices Show Extreme Volatility

This chart illustrates a key ‘Threat’ or ‘Risk’ within a SWOT analysis of the critical minerals investment climate. The extreme price volatility shown is a major factor that investors must consider, making it a perfect fit for this section.

(Source: Center on Global Energy Policy – Columbia University)

Table: SWOT Analysis for Critical Minerals Investment

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | High EBITDA margins (e.g., 30% for extraction). Growing recognition of the supply/demand imbalance. | Demand growth continues, now with added pressure from AI data centers. Prices for key minerals remain well above historical averages despite volatility. | The core thesis that critical minerals are essential and potentially highly profitable was validated. Demand is not the problem. |

| Weaknesses | Long project lead times (avg. 16.5 years). Extreme price volatility (e.g., lithium price collapse in 2023). High CAPEX requirements. | These weaknesses remain unchanged and are the primary deterrent to investment. Permitting paralysis in Western jurisdictions continues to be a major bottleneck. | It was validated that market price signals alone are insufficient to overcome these inherent structural weaknesses. Private capital will not take on this level of long-term risk. |

| Opportunities | Demand-side incentives (IRA). Formation of alliances like the Minerals Security Partnership (MSP). | Shift to direct government support (Project Vault). Formation of strategic JVs and offtake agreements (Lithium Americas, CRML). New geographic partners emerge (Saudi Arabia). | The market shifted from relying on incentives to creating new financing and partnership structures to de-risk investment, validating the need for non-market solutions. |

| Threats | China’s dominance of processing (70-90% market share). Geopolitical risk in producing countries (e.g., DRC). | Western policy instability (OBBBA reversing IRA certainty). Continued Chinese market control and potential for export restrictions. | The threat of policy risk was validated in the West, proving it is not just a risk in developing nations. Geopolitical competition, not cooperation, became the dominant theme. |

Critical Minerals Scenario: Watch for NATO-like Minerals Alliance

If the current fragmented policies and project-by-project agreements fail to meaningfully close the investment gap by 2027, watch for a strategic pivot toward a formal, coordinated minerals security alliance among Western nations to pool capital, harmonize standards, and create a unified trading bloc with sufficient market power.

- The current model is not working. The policy whiplash from the IRA to the OBBBA proved that a stable, long-term investment framework is missing in the U.S. Initiatives like the $12 billion Project Vault are a step in the right direction but are an order of magnitude too small to address a $5.4 trillion problem.

- A signal for this shift would be the evolution of the Minerals Security Partnership (MSP) from a loose diplomatic forum into a true strategic alliance with a dedicated, multi-hundred-billion-dollar joint financing facility.

- Watch for moves to harmonize and fast-track permitting regulations across member countries. If a project meets a jointly agreed-upon environmental and social standard, it would receive expedited approval in any member state, creating a powerful incentive for investment within the bloc.

- Another key indicator would be the creation of a joint strategic stockpile, far larger than any single nation’s current reserves, that could be used to stabilize prices and guarantee offtake for major projects across the alliance.

Geopolitical Concentration of Critical Minerals Supply

This chart illustrates the core problem that a ‘NATO-like Minerals Alliance’ would aim to solve. By showing the high geopolitical concentration of mineral supply, the chart provides the strategic rationale for why Western nations might form an alliance to diversify and secure their access.

(Source: Gemcorp Capital)

The questions your competitors are already asking

This report covers one angle of the financial and policy risks stalling the critical minerals supply chain. The questions that matter most depend on your work.

- What is the actual impact of conflicting government policies, such as the IRA and OBBBA, on long-term investment certainty?

- What is the outlook for private capital closing the $5.4 trillion mining investment gap, given China’s dominance in processing?

- Which nations are gaining or losing ground in the race to build non-Chinese critical mineral supply chains?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.