Thea Energy Stellarator Commercialization, $100 M Series B, DOE Certification, and 2 Hyperscaler PPAs (2021 to 2026)

Fusion Adoption Risk, Thea Energy Faces Execution Hurdles Despite $100 M Funding

Fusion energy’s commercial adoption for data centers transitioned from a theoretical concept to a validated business model, shifting the primary challenge from proving market demand to overcoming execution risk. While competitor power purchase agreements have validated the hyperscaler market, companies like Thea Energy now face intensified pressure to deliver on manufacturing, cost, and deployment timelines.

- Between 2021 and 2024, the industry focus was on fundamental research, with companies raising over $7.1 billion in cumulative private funding to advance different technology concepts. During this period, commercial agreements for fusion power were non-existent, and the data center market was a hypothetical target.

- The landscape shifted dramatically from 2025 onward. Competitor Helion’s landmark Power Purchase Agreement (PPA) with Microsoft, set for 2028, and Commonwealth Fusion Systems’ (CFS) PPA with Google provided concrete validation of the business model.

- This market validation reframed Thea Energy’s mission. After securing $100 million in funding and its DOE pilot plant design certification in 2026, its primary hurdle is no longer market potential but the execution risk of manufacturing its novel stellarator magnets at scale and on schedule.

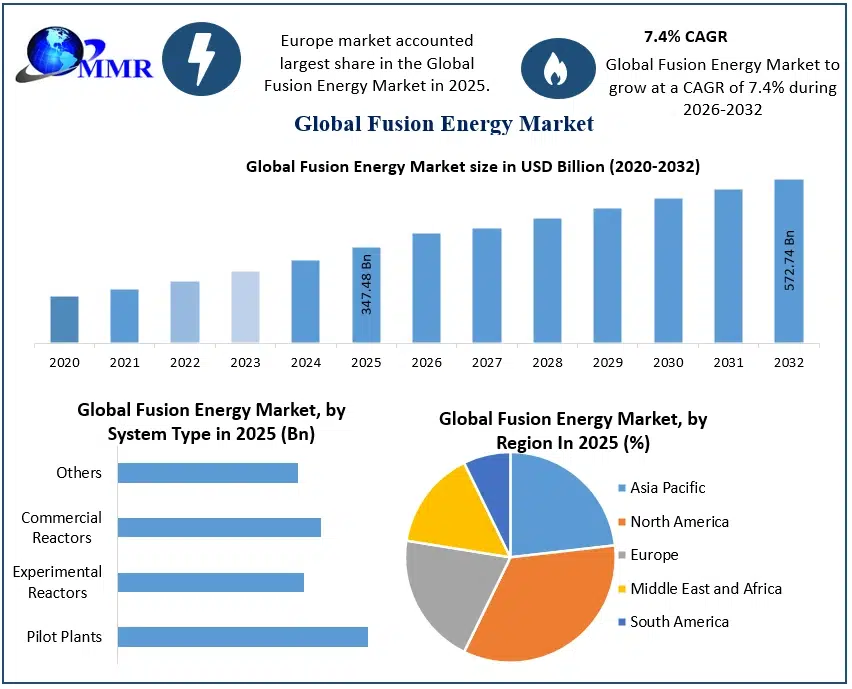

Fusion Energy Market to Reach $572B by 2032

The chart provides the macro-level market potential and opportunity, which serves as a compelling backdrop to the section discussing the risks and hurdles associated with fusion adoption.

(Source: maximize market research)

$100 M Series B, Thea Energy Funding for Stellarator Manufacturing Scale-Up

Recent funding rounds in the fusion sector, including Thea Energy’s $100 million Series B, signal a market shift from long-term R&D investment to funding specific, near-term hardware manufacturing and pilot plant milestones. Investors are now allocating capital based on the ability to execute tangible engineering and supply chain objectives, rather than solely on physics breakthroughs.

- Thea Energy’s $100 million Series B, secured in May 2026, is explicitly targeted at scaling up its unique planar-coil magnet manufacturing capabilities and advancing its integrated ‘Eos’ fusion system, a clear pivot from design to hardware production.

- This contrasts with the investment climate from 2021 to 2024, where capital was deployed more broadly across the industry to support general R&D and company growth, leading to a total of over $7.1 billion in private investment without such specific hardware-centric goals.

- Competitor funding in 2026, such as Helion’s $465 million Series G and Inertia’s $450 million round for a new laser system, also targets commercialization milestones. This indicates investor appetite is now directly tied to tangible progress toward grid-ready systems.

Table: Thea Energy Strategic Investments and Competitor Funding

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Helion | Jun 2026 | Raised $465 million in a Series G funding round to support commercialization efforts, reaching a $15.5 billion valuation. This capital is intended to advance its Polaris prototype and meet its 2028 PPA commitment with Microsoft. | Geek Wire |

| Thea Energy | May 2026 | Secured $100 million in Series B funding. The capital is designated to expand its unique magnet manufacturing capabilities and advance the integrated ‘Eos’ fusion system, moving from design to hardware. | POWER Magazine |

| Inertia | Feb 2026 | Raised $450 million to build a next-generation fusion laser system. The funding targets the construction of a system intended to achieve commercial power generation by 2030. | Carbon Credits |

| X-Energy | Nov 2025 | While a Small Modular Reactor (SMR) company, its $700 million Series D funding is relevant as it targets the same data center power market. The capital is for developing standardized deployment and financing models. | Neutron Bytes |

Fusion and Fission Competitive Landscape Mapped

This chart visually represents the competitive environment, aligning perfectly with the section’s focus on competitor funding and Thea Energy’s strategic investments within that landscape.

(Source: HackSummit – Beehiiv)

Thea Energy 2 Key Alliances, DOE and AWS Partnerships (2025 to 2026)

Strategic partnerships have evolved from academic collaborations into critical public-private and commercial alliances designed to de-risk specific technology and business models. For Thea Energy, its recent agreements with the Department of Energy (DOE) and Amazon Web Services (AWS) provide crucial technical validation and computational resources, serving as vital precursors to securing commercial offtake agreements.

- Thea Energy’s January 2026 certification for its ‘Helios’ pilot plant under the DOE’s Milestone-Based Fusion Development Program is a crucial form of public-private validation. This provides a level of technical credibility that was largely absent in the 2021-2024 period and signals federal confidence in its stellarator approach.

- The October 2025 collaboration with AWS demonstrates a practical shift toward leveraging commercial high-performance computing for stellarator design optimization. This move is intended to accelerate development timelines and solve complex engineering challenges more efficiently.

- These foundational partnerships are stepping stones toward the industry’s ultimate goal: Power Purchase Agreements. While competitors like Helion (Microsoft) and Commonwealth Fusion Systems (Google) have already secured PPAs, Thea Energy has not, making this a critical next step for full commercial validation.

Table: Thea Energy Strategic Partnerships vs. Competitor PPAs

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Thea Energy / DOE | Jan 2026 | Became the first company to have its pilot plant design (‘Helios’) certified under the DOE’s Milestone-Based Fusion Development Program, validating the physics and engineering feasibility of its stellarator design. | The Ridgewood Blog |

| Thea Energy / AWS | Oct 2025 | Partnered with Amazon Web Services to use high-performance computing for advancing stellarator design and optimization, aiming to accelerate the path to a commercial power plant. | NJBIZ |

| Commonwealth Fusion Systems / Google | Jul 2025 | Google signed a PPA to purchase 200 MW of power from CFS’s first commercial power plant, ARC. This agreement validated the commercial model of targeting hyperscalers for baseload clean power. | Energy Industry Review |

| Helion / Microsoft | Jul 2025 | Began construction on a fusion power plant aiming to deliver electricity to Microsoft data centers by 2028. This PPA was the first of its kind, setting a major precedent for the industry. | SAN |

US-Centric Development, Thea Energy’s Focus on the DOE Milestone Program

While fusion research remains a global endeavor, the strategic push toward commercialization for data center power is heavily concentrated in the United States. This convergence is driven by a unique combination of substantial private capital, targeted federal support programs, and the physical location of the world’s largest cluster of hyperscale electricity demand.

- From 2021 to 2024, the fusion landscape appeared more geographically distributed, with significant public research projects in Europe, such as the Wendelstein 7-X stellarator in Germany and the UK’s Culham Science Centre, home to General Fusion’s demonstration plant.

- Since 2025, the commercial center of gravity has sharpened on the U.S. Thea Energy’s base in Kearny, New Jersey, and its deep integration with the U.S. DOE’s Milestone-Based Fusion Development Program exemplify this trend, tying its success directly to American policy and funding.

- The landmark data center power agreements secured by Helion and CFS are with U.S. hyperscalers (Microsoft and Google, respectively). This directly links the first commercial fusion plants to American grid infrastructure and corporate demand, solidifying the U.S. as the primary market for initial deployment.

Stellarator Maturity, Thea Energy Advances Past Theoretical Design

The perceived maturity of stellarator technology advanced significantly, transitioning from a complex academic concept with high construction barriers to a commercially credible path. This shift was driven by innovations in magnet design and computational modeling, validated by Thea Energy’s progress and its formal certification by the U.S. Department of Energy.

- Before 2025, stellarators were widely regarded as technically promising for their inherent plasma stability but too complex and expensive to build, causing most private investment to flow toward the more mature tokamak design.

- Thea Energy’s core innovation, a computer-optimized, planar-coil magnet system, directly addresses this historical weakness by simplifying manufacturing and maintenance. Its selection for the DOE’s Milestone Program in 2023 was an early signal of confidence in this approach.

- The successful certification of the ‘Helios’ pilot plant design in January 2026 marked a major validation point, moving the technology from theoretical advantage to an engineered, reviewable system. While still less mature than tokamaks, Thea’s challenge is to prove it can close the gap through rapid manufacturing and integration of its ‘Eos’ system.

Diagram Details Thea Energy’s Fusion-to-Molecule Strategy

This diagram illustrates a concrete technological strategy, supporting the section’s theme that Thea Energy’s stellarator technology has advanced beyond a purely theoretical design stage and into a mature, applicable concept.

(Source: note)

SWOT Analysis, Thea Energy Strengths and Execution Risks

Thea Energy’s strategic position is defined by the strength of its validated, simplified stellarator design targeting a high-demand market. However, this is counterbalanced by the significant execution risk in scaling manufacturing and the urgent need to secure commercial offtake agreements to keep pace with competitors.

Table: SWOT Analysis for Thea Energy’s Commercial Path

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Technology based on promising PPPL stellarator research with theoretical advantages in steady-state operation. | ‘Helios’ pilot plant design certified by the DOE; novel planar-coil magnet design addresses historical complexity issues; secured $100 M to fund hardware development. | The core technology concept moved from a theoretical advantage to a government-validated engineering design, attracting specific, hardware-focused funding. |

| Weaknesses | Less mature technology compared to tokamaks; lack of significant funding; no commercial validation for the data center market. | No Power Purchase Agreements (PPAs) secured, unlike key competitors (Helion, CFS); manufacturing of novel magnets at scale is unproven. | While funding and design validation have been addressed, the lack of a commercial offtake agreement has become a more pronounced competitive weakness as rivals sign deals. |

| Opportunities | Growing awareness of data center power needs created a potential future market for clean, baseload power. | Surging AI-driven electricity demand creates an urgent 945-1, 000 TWh market by 2030; competitor PPAs prove the business model is viable. | The market opportunity is no longer hypothetical. It is now a quantified, urgent, and validated high-growth sector actively seeking solutions like fusion. |

| Threats | Risk that fusion would not be commercially viable in time; competition from other clean energy sources like advanced renewables and SMRs. | Competitors are moving to construction, potentially locking in key customers and supply chains; cost-competitiveness with SMRs (projected at $65-75/MWh) remains a major hurdle. | The competitive timeline has accelerated. The primary threat is now being outpaced by other fusion companies and more mature technologies like SMRs, such as those from X-energy. |

Thea Energy’s Next Milestone: Securing a Data Center PPA

The single most critical action for Thea Energy in the next 18-24 months is to secure a Power Purchase Agreement with a hyperscale data center operator. This would commercially validate its stellarator technology and provide the financial de-risking necessary to move toward pilot plant construction.

- If Thea Energy demonstrates tangible progress on manufacturing its planar-coil magnets for the ‘Eos’ system, watch for the company to enter advanced offtake negotiations with a major data center operator. This is the next logical step after its DOE design certification.

- A successful PPA announcement would be a significant catalyst, proving that its stellarator approach is commercially attractive and unlocking access to the much larger pools of capital required for project financing and construction.

- Without a PPA, investor confidence may be challenged as competitors like Helion and CFS advance from agreements to physical construction. This could widen the competitive gap and make it more difficult for Thea Energy to attract the necessary resources to maintain its development schedule.

The questions your competitors are already asking

This report covers one angle of Thea Energy’s path to commercializing its stellarator technology for data centers. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the fusion energy for data centers market?

- Is Thea Energy a good investment now that the primary risk has shifted from market validation to manufacturing execution?

- Stellarator magnet performance and manufacturing. What are the technical risks to Thea Energy’s cost and deployment timelines?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.