Wiwynn Data Center Constraints, $7 B Liquid Cooling Market, 100 k W Racks, and 11 Supply Agreements (2021 to 2026)

AI Infrastructure Risks Shift From Silicon To Systems

The primary constraint on deploying artificial intelligence at scale is no longer the production of GPUs but the physical infrastructure required to power and cool them. Server original design manufacturer (ODM) Wiwynn has identified emerging bottlenecks in liquid cooling and power delivery systems, warning that these supply pressures could extend to 2028 and threaten the pace of AI data center construction. The industry’s focus on securing silicon in the 2021-2024 period has given way to a systems-level challenge, where the ability to manage thermal and electrical loads is the new rate-limiting factor for growth.

- Prior to 2025, the AI build-out was largely defined by the availability of high-performance GPUs, with supply chain discussions centered on companies like NVIDIA and their manufacturing capacity.

- Starting in late 2024 and accelerating through 2026, the bottleneck shifted to foundational infrastructure as next-generation chips with Thermal Design Power (TDP) exceeding 700 W began widespread deployment, rendering traditional air cooling insufficient for high-density racks.

- The power density of AI server racks now regularly exceeds 100 k W, a more than 10 x increase from the 7-15 k W standard of traditional enterprise data centers, demanding a complete re-architecture of cooling and power systems.

- As a result, the market for data center liquid cooling is projected to reach nearly $7 billion by 2029, as its adoption is expected to almost double to 39% of data centers by 2026, straining a supply chain that is still considered immature.

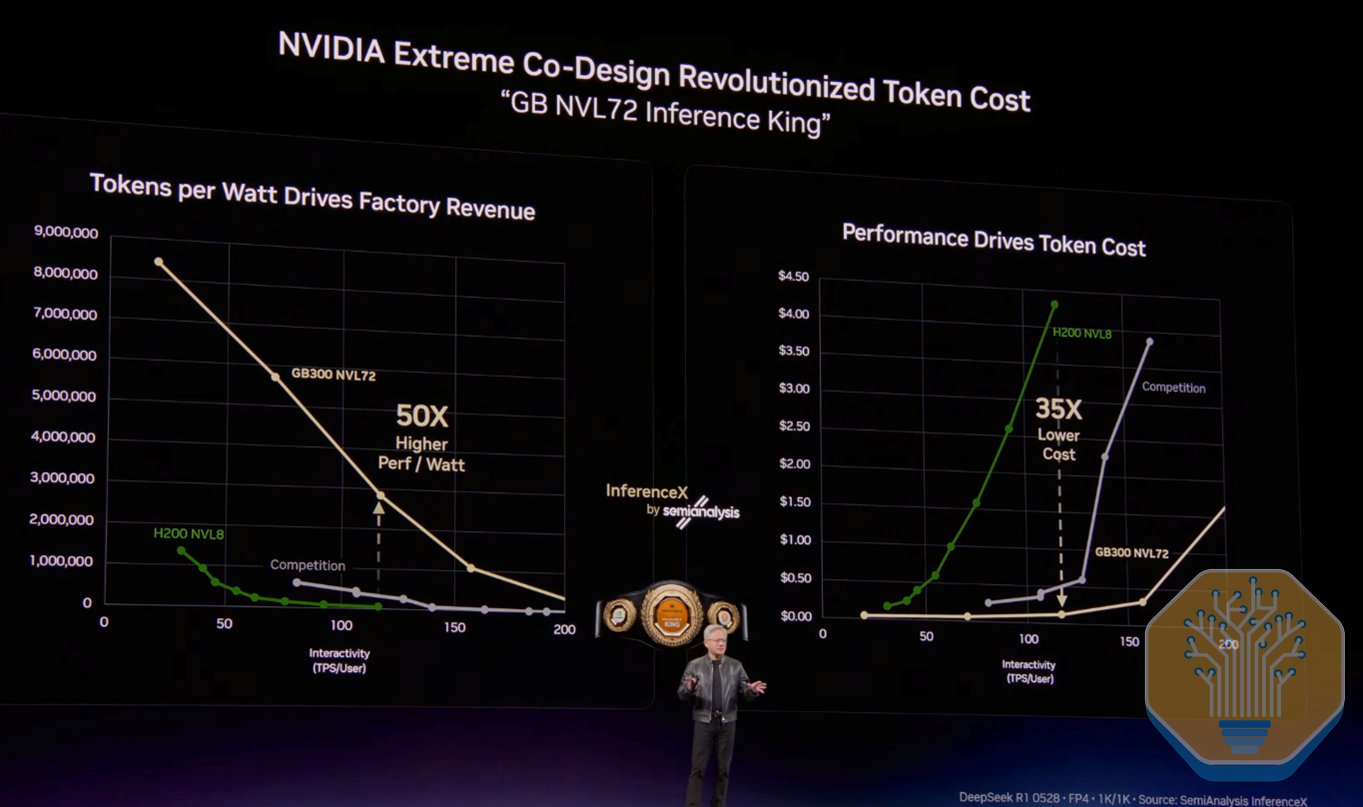

NVIDIA GPUs Show Massive Perf-Per-Watt Gains

This chart illustrates the significant efficiency gains in silicon (GPUs), which serves as a counterpoint to the section’s main argument: that despite these chip-level improvements, the overall infrastructure risk is shifting to system-level problems like power and cooling.

(Source: SemiAnalysis)

$6.8 B in Cooling and Power System Investments

Capital is flowing rapidly into companies that can solve the power and cooling bottlenecks, with major acquisitions and supply agreements in 2025 and 2026 underscoring the high strategic value of this infrastructure. These investments are no longer about incremental component upgrades but are focused on securing the capacity to deliver rack-scale, integrated systems capable of supporting next-generation AI clusters. This contrasts with the 2021-2024 period, where investment was more heavily concentrated on software and chip-level innovations.

- In late 2025, Schneider Electric signed a $1.9 billion agreement with data center operator Switch to provide power and cooling infrastructure for its AI data centers, signaling the scale of capital required for new builds.

- The market recognized the value of specialized expertise when Ecolab acquired direct liquid cooling specialist Cool IT Systems for $4.75 billion, a clear move to integrate thermal management into a broader industrial services portfolio.

- Supplier order books reflect the surging demand, with Modine Manufacturing securing $180 million in new orders for its data center cooling systems in early 2025.

- The shift to on-site power generation is also attracting investment, highlighted by Borg Warner’s strategic entry into the data center market in February 2026 with an award to supply modular turbine generator systems.

Direct-to-Chip Cooling Market to Hit $17.3B

The section discusses $6.8B in specific investments. This chart provides the broader market context, showing the multi-billion dollar market size for a key cooling technology, thereby justifying the scale and strategic importance of the investments mentioned.

(Source: MarketsandMarkets)

Table: Strategic Investments in Data Center Cooling and Power

| Company / Acquirer | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Ecolab / Cool IT Systems | April 2026 | Ecolab acquired Cool IT Systems, a specialist in direct liquid cooling (DLC), for $4.75 billion. The deal signals the high strategic value placed on specialized cooling technology to serve the AI market. | Marketwise |

| Schneider Electric / Switch | November 2025 | Schneider Electric secured a $1.9 billion supply capacity agreement with Switch to provide power infrastructure for its AI “factories, ” demonstrating the scale of investment in foundational systems. | PR Newswire |

| Modine Manufacturing | February 2025 | Secured $180 million in new orders for its data center cooling systems. This highlights strong market demand from colocation and hyperscale customers for specialized thermal management hardware. | Modine |

Data Center Cooling Technologies Drive Market Shift

This chart provides the high-level visual context for the detailed table. It shows the macro trend of a market shift in cooling technologies, which is then substantiated by the specific strategic investments listed in the table.

(Source: MarketsandMarkets)

Power and Cooling Partnership Data, Wiwynn

Strategic partnerships are forming to create integrated ecosystems that address the entire power and cooling chain, from the grid to the chip. Unlike the component-focused alliances of the 2021-2024 period, partnerships in 2025-2026 are systems-oriented, aimed at delivering pre-validated, rack-scale solutions. These collaborations are essential to de-risk the deployment of new, high-density AI infrastructure and accelerate time to market.

- NVIDIA is driving an industry-wide architectural shift by building an 800 V DC ecosystem. This initiative involves partnerships with power supply manufacturers like Delta Electronics and FSP Group to create a standardized “playbook” for AI factories that minimizes power conversion losses.

- The line between technology and energy sectors is blurring, with automotive and industrial companies like Borg Warner partnering with data center operators to supply on-site power generation, a direct response to grid limitations.

- Server ODMs like Wiwynn are collaborating more deeply with ecosystem partners on innovations beyond the server itself, including co-packaged optics and advanced liquid cooling manifolds, to deliver fully integrated rack solutions.

AI Server Racks Contain $15k in Power Components

The section focuses on partnerships. This chart quantifies the high value of power components within a single AI rack, explaining the strong financial incentive for a rack-scale integrator like Wiwynn to form strategic partnerships with power and cooling specialists.

(Source: Tech Investments)

Table: Key Data Center Infrastructure Partnerships

| Lead Partner(s) | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| NVIDIA and Power Supply Partners | 2025-2026 | NVIDIA is leading the creation of an 800 V DC ecosystem, collaborating with PSU makers to standardize high-efficiency power delivery from the grid to the rack, reducing copper and energy losses for AI factories. | NVIDIA |

| Wiwynn and Ecosystem Partners | 2026 | Wiwynn is showcasing collaborations on next-generation technologies like co-packaged optics (CPO) and advanced cooling, integrating these components at the rack level for hyperscale clients. | Wiwynn |

| Borg Warner and Data Center Operators | February 2026 | An automotive supplier entering the data center market by supplying on-site power generation solutions. This move addresses grid constraints and provides reliable power for mission-critical AI workloads. | Borg Warner |

US Power Grid Constraints Reshape Data Center Geography

The geographic expansion of data centers is now dictated more by power availability than by network latency or land costs, a significant reversal from the growth patterns of 2021-2024. Previously, development was concentrated in established hubs like Northern Virginia. Now, grid capacity limitations and lengthy interconnection queues are forcing developers to seek out new regions with available power, fundamentally altering the map of digital infrastructure.

- In the U.S., planned data center projects for 2026 face delays of 30% to 50% due to a severe, long-term shortage of high-voltage transformers and other critical grid components.

- Legacy data center hubs are under extreme strain. In Virginia, utilities like Dominion Energy have had to pause new connections to manage grid stability, illustrating how power has become the primary local constraint on growth.

- The total U.S. power demand from data centers is projected to rise from 61.8 GW in 2025 to 134.4 GW by 2028, forcing operators and utilities to contend with massive grid upgrade requirements across regional transmission organizations like PJM.

- This is driving a “great data center migration” to new states and regions with surplus power capacity, including those with access to significant renewable or nuclear generation.

AI Rack Power Density Explodes Past Facility Limits

This chart visually explains the core problem driving the geographic trend described in the section. The fact that AI rack power density is exceeding the limits of existing facilities is the direct cause for companies to seek new locations, reshaping data center geography.

(Source: Citrini Research)

Liquid Cooling Reaches Commercial Scale Under AI Pressure

Liquid cooling technology has transitioned from a niche solution for high-performance computing (HPC) to a mainstream, mandatory requirement for deploying AI at scale. While the technology was considered mature but optional for most data centers between 2021 and 2024, the release of server platforms like NVIDIA’s Blackwell in 2025-2026 has made it non-negotiable. This rapid shift to commercial scale has exposed supply chain immaturity and created a significant new market.

- Before 2025, liquid cooling was primarily adopted for specialized scientific computing and supercomputers, with most enterprise data centers relying on established air-cooling methods.

- The commercial catalyst was the widespread availability of GPUs and AI accelerators with TDPs exceeding 700 W, making direct-to-chip and other forms of liquid cooling essential for thermal management.

- By EOY 2024, over 1 GW of liquid cooling capacity was deployed in Google’s TPU data centers alone, marking a critical transition from R&D to industrial-scale implementation.

- Despite this progress, a 2025 survey found that 83% of data center experts believe current supply chains are not equipped to deliver the advanced cooling systems needed, highlighting a critical gap between demand and manufacturing capacity.

Decade of R&D Enables Scaled Liquid Cooling

The chart directly supports the section’s headline. As the section discusses liquid cooling reaching commercial scale, the chart explains how this was achieved through a sustained, decade-long R&D effort, linking past development to current market readiness.

(Source: Chips and Cheese)

SWOT Analysis: Wiwynn and AI Infrastructure Bottlenecks

The market for AI infrastructure is defined by immense demand but constrained by physical limitations in power and cooling, creating a complex risk and opportunity profile. The period from 2024 to 2025 validated the scale of the AI-driven demand while simultaneously revealing that the most significant long-term growth barriers are not in silicon but in the systems and grids that support it. This has fundamentally changed the competitive dynamics and strategic priorities for suppliers, operators, and investors.

Data Center Trends Point to Power, Cooling Bottlenecks

A SWOT analysis requires an understanding of the external environment. This chart perfectly summarizes the key industry-wide challenges (threats) and opportunities by identifying power and cooling as the new primary bottlenecks for data centers.

(Source: IoT Analytics)

Table: SWOT Analysis for AI Data Center Infrastructure

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Explosive demand for AI compute, driven by large language models (LLMs). Strong pricing power for GPU manufacturers. | Sustained, multi-year demand for AI infrastructure is validated. High-density rack deployments become standard. | The market confirmed that AI is a long-term infrastructure build-out, shifting value to system-level enablers like Wiwynn and Supermicro beyond just chip suppliers. |

| Weaknesses | Focus on GPU supply chain (e.g., HBM, advanced packaging) as the primary bottleneck. Underestimation of physical infrastructure needs. | Supply chains for liquid cooling components (pumps, CDUs) and power transformers are revealed as immature and insufficient. High Cap Ex for retrofits. | The weakness shifted from the chip supply chain to the physical plant. A 2025 survey showed 83% of experts see cooling supply chains as unready for AI demand. |

| Opportunities | Incremental efficiency gains in air cooling. Software-based workload optimization to manage thermals. | Architectural shifts to high-voltage DC (800 V). M&A of specialized cooling firms. On-site power generation (fuel cells, SMRs). | The opportunity expanded from component-level fixes to system-wide architectural innovation, creating markets for firms like Bloom Energy and driving deals like Ecolab’s acquisition of Cool IT. |

| Threats | Rising electricity prices and sustainability concerns. Geopolitical risks impacting semiconductor supply chains. | Grid instability, transformer shortages, and multi-year interconnection queues delaying 30-50% of 2026 projects. Regulatory pushback on new data center builds. | The primary threat moved from a specific component shortage (GPUs) to a systemic, infrastructure-level crisis. Grid access is now the main threat to project timelines and regional growth. |

Scenario Modelling: Wiwynn and the On-Site Power Pivot

The single most critical variable for AI data center expansion in the year ahead is the lead time for grid-level power infrastructure. If transformer shortages and interconnection delays persist through 2026, expect a significant acceleration in the adoption of “behind-the-meter” power solutions as hyperscalers and data center operators pivot to secure power certainty. This will shift billions in capital from traditional grid upgrades toward on-site generation assets.

- If this happens: Lead times for high-voltage transformers remain over two years, and utilities continue to announce pauses on new data center connections in key markets.

- Watch this: An increase in announcements for large-scale deployments of natural gas turbines, solid-oxide fuel cells, and even initial agreements for small modular reactors (SMRs) directly at data center campuses.

- This could be happening: Hyperscalers like Microsoft and Amazon Web Services (AWS) are already actively hiring nuclear energy experts and exploring new power sources. The strategic entrance of companies like Borg Warner into the data center market in February 2026 is a clear signal that this trend is already in motion.

Liquid Cooling Delivers 20x Power Density

The section models a future scenario involving an ‘On-Site Power Pivot’. This chart provides the technological premise for such a scenario, illustrating the extreme power density that liquid cooling enables, which in turn necessitates radical new power solutions.

(Source: semivision – Substack)

The questions your competitors are already asking

This report covers one angle of the emerging bottlenecks in data center cooling and power for AI workloads. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the data center liquid cooling and power supply market?

- What is the outlook for liquid cooling deployment in high-density AI data centers by 2028?

- How does liquid cooling compare to air cooling for 100 kW+ AI server racks?

- Which hyperscalers are adopting liquid cooling for next-generation AI deployments?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.