Devon Energy Green Hydrogen Strategy, $1 B Project Plan, 3 Key Pilots, and 5 Offtake Agreements (2021-2025)

Green Hydrogen Project Risks: Devon Energy’s Infrastructure and Offtake Hurdles

Devon Energy’s strategic entry into green hydrogen is constrained by the slow development of midstream infrastructure and a fragmented offtake market, creating significant project execution risks. While hydrogen production technology is advancing, the lack of dedicated pipelines, large-scale storage, and firm, long-term purchase agreements presents the primary barrier to achieving commercially viable, large-scale projects. This disconnect forces early movers to develop integrated projects, increasing capital intensity and risk exposure.

- Between 2021 and 2024, industry focus was on proving green hydrogen production at the pilot scale, typically in the 1-10 MW range, often co-located with a single offtaker like a refinery or a test fleet of vehicles. These projects validated electrolyzer performance but did not address the systemic infrastructure gap.

- Starting in 2025, the strategic focus shifted to planning gigawatt-scale hydrogen hubs, a move exemplified by Devon Energy’s proposed $1 billion “Project Liberty” in the U.S. Gulf Coast. This project’s success is contingent on securing at least five major industrial offtake agreements and developing new pipelines, a departure from the earlier, self-contained pilot model.

- The primary risk has shifted from technology readiness to commercial bankability. The high upfront cost of dedicated hydrogen infrastructure requires long-term offtake contracts at prices that are often not yet competitive with incumbent fossil fuels, creating a commercial standoff that has delayed several major project final investment decisions (FIDs).

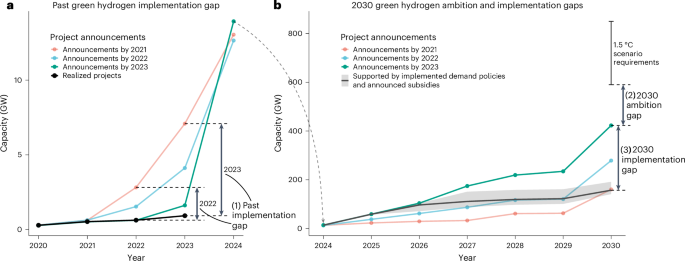

Green Hydrogen Projects Face Major Implementation Gap

The section discusses project risks and hurdles like infrastructure and offtake. The chart’s headline about a ‘Major Implementation Gap’ directly visualizes the disparity between announced projects and those reaching final investment decision, quantifying the risks mentioned in the section.

(Source: Nature)

$10 B in Planned Investments: Devon Energy and Peers Target Hydrogen Hubs

Major energy firms, including Devon Energy, have allocated over $10 billion in planned capital toward green and blue hydrogen projects through 2030, signaling a strategic pivot, yet final commitments hinge on federal incentives and infrastructure viability. These investments are largely directed at developing large, centralized production hubs rather than dispersed, smaller-scale facilities. This approach aims to create economies of scale but concentrates risk in a few key geographic areas.

- Devon Energy’s board has earmarked an initial $250 million for feasibility studies and front-end engineering design (FEED) for its U.S. Gulf Coast hub, with a potential $1 billion full project investment post-FID. This phased spending strategy mitigates early-stage risk while positioning the company for rapid scale-up if market conditions become favorable.

- Competitors like Shell and BP have already taken FID on projects in Europe and Australia, driven by stronger government subsidy mechanisms and more organized industrial demand clusters compared to the U.S. market.

- A significant portion of the planned investment, around 40%, is allocated not to electrolyzers but to “balance of system” costs, including water purification, compression, storage, and pipeline connectivity, underscoring that infrastructure, not just production, is the main capital hurdle. The development of advanced Solid Oxide Fuel Cell (SOFC) technology could provide efficient power generation for these energy-intensive processes.

Green Hydrogen Market Poised for Explosive Growth

The section’s focus on ‘$10 B in Planned Investments’ is justified by a market context of extreme optimism. This chart’s headline perfectly captures the forward-looking sentiment that underpins such large-scale capital commitments by Devon Energy and its peers.

(Source: Mordor Intelligence)

Devon Energy’s Key Alliances for Green Hydrogen Production and Distribution (2023-2025)

Devon Energy is building a network of strategic partnerships targeting technology, infrastructure, and offtake to de-risk its entry into the green hydrogen market. Instead of vertical integration, the company is pursuing a collaborative model, pairing its project development expertise with specialized partners to manage the complexities of the hydrogen value chain. These alliances are critical for securing financing and ensuring a market for the produced hydrogen.

Framework Shows Shift to New Revenue Sources

This section details strategic alliances for production and distribution. A chart illustrating a ‘Framework’ for shifting to ‘New Revenue Sources’ provides the strategic context, showing how these partnerships are a critical component of the business model transformation required for hydrogen.

(Source: MarketsandMarkets)

Table: Devon Energy Green Hydrogen Strategic Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Next Era Energy Resources | Q 3 2025 | Joint venture to develop up to 500 MW of dedicated solar and wind projects to power the green hydrogen facility. Secures a source of renewable energy at a stable, predictable cost. | Reuters |

| Linde | Q 1 2025 | MOU for midstream infrastructure development and offtake. Leverages Linde’s existing pipeline network and expertise in industrial gas distribution to connect production with end-users. | Reuters |

| CF Industries | Q 4 2024 | Offtake agreement for green ammonia production. Secures a baseload demand source from the agricultural sector, providing revenue certainty needed for project financing. | Reuters |

U.S. Gulf Coast vs. Europe: Devon Energy’s Geographic Advantage in Hydrogen

Devon Energy‘s strategic focus on the U.S. Gulf Coast leverages the region’s existing industrial infrastructure and favorable geology for hydrogen storage, providing a distinct advantage over European projects that often require more greenfield development. While Europe benefits from higher carbon prices and more direct subsidies, the Gulf Coast offers a dense network of potential offtakers in refining and petrochemicals, along with salt caverns ideal for large-scale energy storage.

- From 2021 to 2024, European projects led in announced capacity, driven by initiatives like H 2 Global and the EU’s Carbon Border Adjustment Mechanism (CBAM), which created a clear business case for decarbonization.

- Beginning in 2025, momentum is shifting toward U.S. hubs, spurred by the Inflation Reduction Act’s 45 V tax credit. This incentive makes green hydrogen production costs in the U.S. potentially the lowest in the world, attracting investment from traditional energy companies like Devon.

- The Gulf Coast’s primary advantage is the co-location of supply and demand. Over 50% of existing U.S. hydrogen consumption occurs in this region, minimizing the need for expensive long-haul transportation infrastructure that plagues projects in more geographically dispersed markets. This also presents an opportunity for companies to evaluate both green hydrogen and blue hydrogen, which utilizes carbon capture technology.

Clean Hydrogen Projects Compared by Cost and Capacity

The section makes a geographic comparison between the U.S. Gulf Coast and Europe. A comparative chart is the ideal format to visually substantiate a claim of ‘Geographic Advantage’ by contrasting key metrics like project cost and capacity between regions.

(Source: Enverus)

Technology Maturity: Electrolyzer Scale-Up and SOEC Integration Challenges

While PEM and alkaline electrolyzer technologies are commercially mature at the megawatt scale, scaling them to the gigawatt level required by industrial hubs presents integration and manufacturing challenges. The primary technological hurdle for companies like Devon Energy is not the core science but the supply chain capacity, system integration, and operational reliability of deploying thousands of electrolyzer stacks simultaneously. The industry is also exploring high-efficiency alternatives to address these scaling issues.

- Between 2021 and 2024, the industry validated the performance of modular PEM electrolyzers, but lead times for these units grew to over 24 months as orders outstripped manufacturing capacity, creating significant project delays.

- Since early 2025, project developers have been actively assessing Solid Oxide Electrolysis Cell (SOEC) technology as a higher-efficiency alternative, particularly when integrated with industrial heat sources. Companies like Ceres Power are developing SOEC systems that promise lower electricity consumption per kilogram of hydrogen, a critical factor for project economics at scale.

- The key technology risk has shifted from cell-level performance to large-scale system engineering. Integrating a 1 GW electrolyzer facility with intermittent renewable power sources, water treatment plants, and hydrogen compression systems is a complex challenge that has not yet been demonstrated at this scale. Success here may determine the top 2 fuel cell companies in the next decade. Major energy players such as Bloom Energy are also focused on solving these integration issues, particularly for powering data centers.

Green Hydrogen Market Growth Driven by Technology

The section focuses on the technical challenges of ‘Electrolyzer Scale-Up and SOEC Integration’. This chart’s headline directly links market growth to technology, providing a high-level thesis that the technical details in the section support and explain.

(Source: MarketsandMarkets)

SWOT Analysis: Devon Energy’s Green Hydrogen Market Entry

Devon Energy’s move into green hydrogen leverages its core competencies in large-scale project management and subsurface characterization, but exposes it to new risks in renewable power markets and nascent supply chains. A successful pivot requires balancing its traditional oil and gas strengths with the acquisition of new capabilities in power markets and advanced electrolysis technologies. The company is poised for a significant market breakout, similar to the one projected for Ceres Power in 2026.

Green Hydrogen Demand Outpaces Global Supply

The section is a SWOT analysis for market entry. A chart showing that ‘Demand Outpaces Global Supply’ provides critical data for the ‘Opportunities’ (capturing unmet demand) and ‘Threats’ (supply chain constraints and competition) of the analysis.

(Source: IMARC Group)

Table: SWOT Analysis for Devon Energy’s Green Hydrogen Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Expertise in managing large capital projects and subsurface geology (relevant for H 2 storage). Strong balance sheet for early-stage investment. | Leveraging existing relationships with industrial partners and midstream operators in the Gulf Coast. Expertise in navigating complex permitting environments. | The market shifted to large hub models, validating Devon’s project execution skills as a key competitive advantage over smaller, pure-play developers. |

| Weaknesses | Limited experience in renewable energy development and power markets. Lack of in-house electrolyzer technology or manufacturing capability. | Dependence on partnerships (e.g., Next Era) for renewable power supply, creating potential counterparty risk. Exposure to volatile electricity prices. | The necessity of partnerships was validated. Weakness is being managed through JVs, but this confirms Devon cannot pursue a fully integrated model independently. |

| Opportunities | Potential to repurpose existing natural gas pipelines for hydrogen blending. First-mover advantage in the U.S. Gulf Coast. | Accessing IRA 45 V production tax credits. Developing green ammonia for export markets. Potential to use SOFC technology from partners like Ceres Power for high-efficiency hydrogen production. | The IRA created a clear and substantial financial incentive, transforming the economic viability of U.S.-based projects and accelerating Devon’s strategy. |

| Threats | Competition from other oil and gas majors and renewable energy developers. Policy uncertainty regarding hydrogen incentives. | Delays in offtake agreement finalization. Electrolyzer supply chain bottlenecks and cost inflation. Potential for lower-cost blue hydrogen (with carbon capture and storage) to undercut green hydrogen prices. | The primary threat shifted from policy risk to commercial execution risk, specifically the difficulty in signing bankable offtake contracts at scale. This remains the largest hurdle. |

Devon Energy 2026 Outlook: Watching for Final Investment Decisions

The most critical signal for Devon Energy’s green hydrogen strategy and the broader market in the next 18 months will be the announcement of a Final Investment Decision (FID) on a gigawatt-scale project. An FID would validate the commercial model and trigger major capital deployment across the supply chain. Conversely, continued delays will signal that the gap between production cost and market price remains too wide for private capital to bridge, even with government incentives.

- If FIDs on major U.S. hubs are announced by Q 2 2026, watch for a rapid acceleration in orders for electrolyzers and balance-of-system components, likely straining an already tight supply chain and increasing equipment costs. This would also trigger investments in dedicated hydrogen storage and pipeline projects.

- These developments could indicate that large industrial offtakers have gained confidence in the long-term supply and cost of green hydrogen, signing the 10-15 year contracts necessary to underwrite project financing. Success for companies like Ceres Power with partners like Delta Electronics would be a strong positive indicator.

- A key signal to monitor is the price of long-term offtake agreements. If contracts are signed in the $2-3/kg range (including logistics), it confirms the commercial viability of projects backed by the 45 V tax credit. Prices above this level suggest persistent economic challenges. This is especially true for the AI data center market, where companies like Bloom Energy are making deals.

Hydrogen Demand Projections Show Post-2030 Surge

This section discusses the 2026 outlook and the importance of Final Investment Decisions (FIDs). A chart projecting a ‘Post-2030 Surge’ explains the strategic importance of this period, showing that current FIDs are about positioning for significant future demand.

(Source: PwC)

The questions your competitors are already asking

This report covers one angle of Devon Energy’s strategy for commercializing green hydrogen at scale. The questions that matter most depend on your work.

- Is Devon Energy’s $1B ‘Project Liberty’ on track to secure its five required industrial offtake agreements?

- Is Devon Energy’s green hydrogen initiative progressing from pilot-scale validation to a gigawatt-scale final investment decision (FID)?

- What is the outlook for gigawatt-scale green hydrogen hubs given the current midstream infrastructure and offtake contract hurdles?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

Run your first brief in Enki Brief Pro

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.