DER Market 2026: How Software and Finance Are Unlocking Grid-Scale Value

DER Adoption 2026: Projects Shift from Hardware Pilots to Integrated Software Platforms

The Distributed Energy Resources (DER) market has matured from a focus on isolated hardware projects between 2021 and 2024 to a professionalized ecosystem where integrated software platforms and market access are the primary drivers of adoption in 2025 and 2026. This evolution marks a definitive shift from proving technology viability to deploying it at commercial scale through sophisticated orchestration and financial integration.

- The period between 2021 and 2024 was characterized by foundational work, including the release of EPRI’s Open DER model in June 2022 to standardize planning and the opening of CSA Group’s DER lab in November 2022 to certify hardware. This work established the technical baseline for individual assets.

- By 2025, the focus moved to large-scale management. Oracle enhanced its Advanced Distribution Management System (ADMS) in March 2025 to improve DER orchestration, demonstrating the demand from utilities for enterprise-grade control systems to manage grid complexity.

- The launch of i QGen’s v 1 platform in early 2026 represents the new market paradigm. It provides an end-to-end solution to streamline the entire project lifecycle, from funding to operations, directly addressing the soft costs and logistical bottlenecks that previously hindered smaller projects.

- The partnership between Siemens and Energy Hub, announced in February 2023, solidified this trend by combining industrial-grade grid software with a platform managing a vast ecosystem of third-party DERs. This model of integrating diverse assets under a single software layer is now the industry standard for scalable deployment.

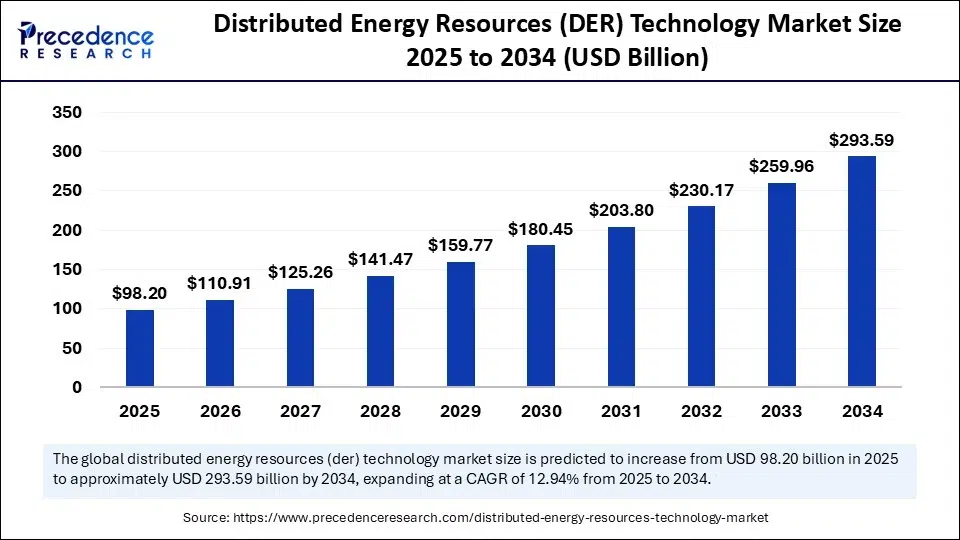

DER Market to Approach $300B by 2034

This chart quantifies the overall market growth discussed in the section, reinforcing the theme of DER adoption reaching commercial scale.

(Source: Precedence Research)

DER Investment Analysis: Private Equity and Strategic Capital Validate the New Market Model

Investment in DERs has decisively shifted from early-stage venture funding for individual technologies to large-scale private equity acquisitions and institutional project finance. This transition, which accelerated between 2024 and 2025, confirms the sector’s maturity as a bankable infrastructure asset class capable of attracting significant institutional capital.

- The acquisition of Scale Microgrids by private equity firm EQT in January 2025 is a landmark event. It validates the vertically integrated developer-owner-operator model for microgrids and signals that the sector’s business models are now considered proven and profitable by major institutional investors.

- The $11 billion financing secured by Pattern Energy for its Sun Zia Transmission and Wind project in January 2024 illustrates the scale of capital now available for DER-enabling infrastructure. This project creates the high-voltage backbone necessary to integrate thousands of megawatts of distributed generation.

- The entrance of new, well-funded players like Dispatch Energy, which launched in September 2024 with $20 million in initial funding, indicates continued strong investor interest in specialized DER development and deployment.

- Direct project investment is also scaling, as seen in the February 2026 agreement where Connect M’s subsidiary committed an initial $16.5 million for distributed solar deployments with Alpex Solar, targeting specific commercial and agricultural applications.

Table: Key Investments in the DER Sector (2024-2026)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Connect M / Alpex Solar | Feb 2026 | Initial $16.5 million deployment agreement for distributed rooftop solar and solar irrigation pump projects. This signals investment in targeted, application-specific DER solutions. | Globe Newswire |

| EQT / Scale Microgrids | Jan 2025 | Acquisition of a leading microgrid developer and operator by a major private equity firm. This transaction validates the vertically integrated DER business model as a mature, investable asset class. | EQT Group |

| Dispatch Energy | Sep 2024 | Company launched with $20 million in initial funding to develop and deploy innovative DER solutions. This shows robust venture and strategic interest in new, specialized market entrants. | PR Newswire |

| Pattern Energy / Sun Zia | Jan 2024 | Secured $11 billion in financing for a 3, 500+ MW wind project and a 550-mile HVDC transmission line. This is a critical DER-enabling infrastructure investment. | Utility Dive |

Global DER Expansion: North America Leads with Advanced Regulatory Frameworks

While DER activity is global, North America, particularly Ontario, Canada, established a clear lead in 2025 by creating sophisticated regulatory and market frameworks that incentivize DER integration. This policy innovation is creating a blueprint for how to align utility business models with a decentralized grid, a model other regions are beginning to follow.

Solar and Storage to Lead US Expansion

This chart illustrates the composition of new energy projects in the U.S., a key part of the leading North American market discussed in the section.

(Source: Turbomachinery Magazine)

- Ontario has become a global leader with its DER Roadmap. The Ontario Energy Board’s (OEB) June 2025 proposal to allow utilities to earn a Margin on Payments (Mo P) of up to 25% on payments to DER providers fundamentally realigns utility financial interests with DER growth.

- To address physical grid constraints, the OEB announced the launch of a Consolidated Capacity Information Map (CCIM) for December 2025. This tool provides transparent data on grid hosting capacity, aiming to streamline and accelerate the interconnection process, a major bottleneck worldwide.

- European industrial markets are also advancing, as shown by Energy Vault’s market entry into Switzerland in December 2025 with contracts to deploy battery storage for industrial and utility clients, confirming the need for DERs to support grid stability in dense economic zones.

- Emerging markets are following suit, with initiatives like the BASE project announced in April 2025 to develop Virtual Power Plants (VPPs) in Brazil, Colombia, and Mexico. This shows a growing recognition of DERs as a solution for grid services, though these markets still lag North America in regulatory maturity.

DER Technology Maturity: Software and Orchestration Reach Commercial Scale

The critical technology shift between the 2021-2024 period and today is the maturation of DER management systems (DERMS) and aggregation platforms from pilot-stage concepts to commercially scalable, enterprise-grade software. Hardware is now a commodity; the key differentiator and source of value is the intelligence layer that controls it.

DER Software Market Shows Explosive Growth

This forecast directly supports the section’s focus on software maturity, providing a strong monetary projection for the growth of DER management systems.

(Source: Zion Market Research)

- The 2022-2024 period focused on establishing technical foundations. Initiatives like EPRI’s Open DER model and GE Vernova’s focus on the IEEE 2030.5 communication standard were about creating the common language needed for devices and systems to interoperate.

- By 2025, the market demand shifted to robust, scalable control systems. Oracle’s ADMS enhancements and Schneider Electric’s launch of Eco Struxure DERMS in October 2024 show that major technology providers are now delivering utility-grade platforms capable of managing complex, bidirectional energy flows.

- The rapid growth of the DERMS market, projected by multiple analysts to have a CAGR between 13% and 19%, provides quantitative proof that the industry is investing heavily in this software layer. This is where the operational complexity of the distributed grid is being solved.

- Platforms like those from Voltus and Leap represent the final piece of technology maturation: market integration. Their software connects aggregated DERs to wholesale energy markets, turning distributed assets into revenue-generating virtual power plants and completing the transition from passive grid components to active market participants.

SWOT Analysis: Assessing Strengths and Risks in the 2026 DER Market

The Distributed Energy Resources market’s strength in 2026 lies in its newly validated business models and supportive regulatory tailwinds, which are attracting significant institutional investment. However, this growth is tempered by the persistent threat of physical grid limitations and the operational challenge of orchestrating a rapidly expanding and diverse fleet of assets.

Hardware Cost Reductions Enabled DER Growth

This chart illustrates a foundational market strength referenced in the SWOT analysis: the historical drop in hardware costs that enabled current business models.

(Source: Steel For Fuel – Substack)

Table: SWOT Analysis for Distributed Energy Resources (2021-2025)

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Technology viability proven in pilots; falling hardware costs (solar, batteries); growing policy support. | Bankable business models (EQT/Scale); sophisticated market access platforms (Voltus, Leap); innovative utility incentive structures (Ontario OEB). | The business case for DERs has been validated, moving from theoretical cost savings to proven revenue generation attractive to private equity. |

| Weaknesses | Fragmented software landscape; high soft costs; complex and slow interconnection queues; lack of utility business case. | Interoperability remains a challenge despite standards; grid infrastructure is a bottleneck; cybersecurity complexity increases with scale. | While software platforms (i QGen, Oracle) are improving, the underlying physical grid and security challenges are becoming more acute with wider deployment. |

| Opportunities | Grid resilience needs; decarbonization goals; early-stage VPP and demand response programs. | Massive demand from AI data centers; “value stacking” in wholesale markets (NYISO); new utility revenue streams (Ontario’s Mo P). There is also less data center risk in stable regions. | The demand drivers for DERs have intensified, and market rules are now being written to capture multiple value streams simultaneously, dramatically improving project economics. |

| Threats | Regulatory uncertainty; utility resistance to DER integration; technology interoperability issues. | Physical grid hosting capacity limits; inconsistent policy implementation across jurisdictions; supply chain constraints for key components (transformers, switchgear). | The primary threat has shifted from policy risk to physical and logistical constraints. The grid itself is now the main barrier to growth. |

2026 DER Outlook: Will Regulatory Innovation Outpace Physical Grid Constraints?

The primary determinant of Distributed Energy Resources growth in 2026 will be the race between innovative regulatory and financial frameworks that unlock value and the physical limitations of grid infrastructure to host these new resources. Success will depend on the ability of policy, technology, and investment to collectively solve the grid’s physical bottlenecks.

- If regulatory models like Ontario’s 25% Margin on Payments are adopted in other jurisdictions, watch for a rapid acceleration in utility-led DER procurements. This would signal a fundamental shift where incumbent utilities become the primary drivers of decentralized energy.

- If interconnection reforms and transparency tools like Ontario’s CCIM prove successful in reducing project backlogs, watch for a surge in deployed capacity, particularly in grid-constrained but economically attractive areas like data center clusters and industrial parks.

- The critical signal to monitor is the deployment rate of DER-enabling infrastructure, such as the Sun Zia transmission line, versus the rate of DER project delays attributed to grid capacity issues. The former indicates the constraint is being addressed, while the latter suggests a potential ceiling on near-term growth.

Frequently Asked Questions

What is the biggest change in the DER market between the 2021-2024 period and 2026?

The primary change is the shift from small, hardware-focused pilot projects to large-scale deployments driven by integrated software platforms and financial models. The market has matured from proving technology works to deploying it commercially through sophisticated software that orchestrates assets and connects them to energy markets for revenue generation.

Why are large private equity firms like EQT now investing in the DER sector?

Large private equity firms are investing because the business models for DERs have been proven profitable and ‘bankable’. The January 2025 acquisition of Scale Microgrids by EQT validated the vertically integrated developer-owner-operator model, signaling to major institutional investors that DERs are a mature, investable infrastructure asset class, not just an early-stage technology.

What is the biggest risk or threat to DER growth in 2026?

The biggest threat has shifted from regulatory uncertainty to the physical limitations of the electrical grid. While policies are becoming more supportive, the grid itself often lacks the capacity to host a large number of new DERs, leading to long interconnection queues and project delays. This physical bottleneck is now considered the main barrier to growth.

The article mentions software is key. What specific role does software play in the modern DER market?

Software now serves as the ‘intelligence layer’ that unlocks the value of DER hardware. Platforms like DERMS (Distributed Energy Resource Management Systems) from providers like Oracle and Schneider Electric help utilities manage grid complexity. Other platforms, such as those from iQGen, streamline the entire project lifecycle, while market integration software from companies like Voltus and Leap aggregates DERs into Virtual Power Plants (VPPs) to participate in wholesale energy markets and generate revenue.

Which region is leading in DER policy, and what makes its approach innovative?

North America, particularly Ontario, Canada, is highlighted as a global leader in DER policy. Its approach is innovative because it directly addresses the utility business model and physical grid constraints. The Ontario Energy Board’s proposal to allow utilities to earn a ‘Margin on Payments’ (MoP) on DER services aligns their financial interests with DER growth. Additionally, its Consolidated Capacity Information Map (CCIM) provides transparency on grid hosting capacity to speed up interconnections.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.